Download as pdf or txt

You might also like

- Hidden Games Enemies To Lovers Football Romance Stand Alone Hallowed Saints University Brandy Silver 2 Full ChapterDocument68 pagesHidden Games Enemies To Lovers Football Romance Stand Alone Hallowed Saints University Brandy Silver 2 Full Chapterlouis.cook744100% (13)

- American Jurispurdence - Banks and FInancial InstitutionsDocument1,409 pagesAmerican Jurispurdence - Banks and FInancial InstitutionsRon GaylesNo ratings yet

- All Bank Policy HL & LapDocument25 pagesAll Bank Policy HL & LapmadirajunaveenNo ratings yet

- Print To Be Taken On Annexure 1 - Declaration From Borrowers With Foreign Currency ExposureDocument1 pagePrint To Be Taken On Annexure 1 - Declaration From Borrowers With Foreign Currency Exposureshyam kayal50% (2)

- CIBIL Scores ExplainedDocument4 pagesCIBIL Scores ExplainedOmkar Bhoye100% (1)

- What Is CIBIL Score and How To Improve It?Document4 pagesWhat Is CIBIL Score and How To Improve It?sahilkuNo ratings yet

- CIBILDocument11 pagesCIBILViji RangaNo ratings yet

- CIBIL Report UnderstandingDocument3 pagesCIBIL Report UnderstandingSujan NaikNo ratings yet

- SanctionDocument6 pagesSanctionKriti GoodNo ratings yet

- Allahabad Bank: Appraisal FormatDocument5 pagesAllahabad Bank: Appraisal FormatDEVENDRA BHARDWAJNo ratings yet

- 3 - CamDocument3 pages3 - CamKavit Thakkar100% (2)

- IDBI Bank Home LoanDocument11 pagesIDBI Bank Home Loansahil7827No ratings yet

- Mortgage Loans Check List For SalariedDocument2 pagesMortgage Loans Check List For SalariedVelagala Lokeshwara ReddyNo ratings yet

- Vijaya EnterprisesDocument1 pageVijaya EnterprisesBhaskar Teja AtluriNo ratings yet

- Finova - PD Format Oct 2019Document8 pagesFinova - PD Format Oct 2019Madhusudan ParwalNo ratings yet

- WORDPAD - CREDIT ANALYSIS OF PERSONAL LOAN" at ABN AMRO BANK FINALDocument53 pagesWORDPAD - CREDIT ANALYSIS OF PERSONAL LOAN" at ABN AMRO BANK FINALAMIT K SINGHNo ratings yet

- HDFC Ltd. Home Loan FeaturesDocument8 pagesHDFC Ltd. Home Loan FeaturesVishv SharmaNo ratings yet

- IPPB Recruitment 2022Document14 pagesIPPB Recruitment 2022NDTVNo ratings yet

- HDFC Twoweeler LoanDocument93 pagesHDFC Twoweeler Loanashish100% (22)

- Kotak Mahindra BankDocument11 pagesKotak Mahindra BankOmkar KudtarkarNo ratings yet

- Undertaking From BorrowerDocument7 pagesUndertaking From BorrowerDivyesh Varun D VNo ratings yet

- India Home Loans LTD Credit Policy of India Home Loans LTDDocument9 pagesIndia Home Loans LTD Credit Policy of India Home Loans LTDvinayak_cNo ratings yet

- JoginderDocument2 pagesJoginderVikash Kumar100% (1)

- PD SHEET - SENPv1Document2 pagesPD SHEET - SENPv1Mritunjai SinghNo ratings yet

- Sample Valuation ReportDocument17 pagesSample Valuation ReportabhidadNo ratings yet

- Sanction LetterDocument6 pagesSanction Letterpssahoo1334No ratings yet

- V5 Global Services (A First Meridian Company) Business DevelopmentDocument4 pagesV5 Global Services (A First Meridian Company) Business DevelopmentradhikaNo ratings yet

- CC Loan ProjectDocument11 pagesCC Loan ProjectAjay ThakurNo ratings yet

- CIBIL Score in DetailDocument11 pagesCIBIL Score in DetailOmkar BhoyeNo ratings yet

- Cash Credit Proposal For Bank FinanceDocument15 pagesCash Credit Proposal For Bank Financeajaya thakurNo ratings yet

- Sanction LetterDocument1 pageSanction LetterShanmugasundaram DhandapaniNo ratings yet

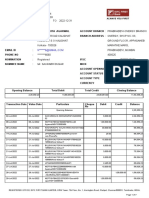

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument2 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balancekunjal mistryNo ratings yet

- IDFC FIRST Bank Limited (Formerly IDFC Bank Limited)Document7 pagesIDFC FIRST Bank Limited (Formerly IDFC Bank Limited)Sarath KumarNo ratings yet

- AttachmentDocument60 pagesAttachmentTahseen banuNo ratings yet

- SMFG - Fullerton Personal LoanDocument14 pagesSMFG - Fullerton Personal LoanAshwani KumarNo ratings yet

- IDFCFIRSTBankstatement 10051513509Document7 pagesIDFCFIRSTBankstatement 10051513509Saurabh DugarNo ratings yet

- GRC Application Form For Obtaining CardDocument2 pagesGRC Application Form For Obtaining Cardnvn.nnd370182% (11)

- Balance Sheet of HDFC LTDDocument1 pageBalance Sheet of HDFC LTDAkshat Sharma Roll no 21No ratings yet

- Subject: Financial Management: Yes Bank CrisisDocument9 pagesSubject: Financial Management: Yes Bank Crisisaryan sharmaNo ratings yet

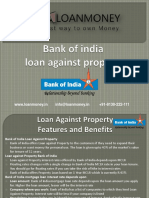

- Bank of India Loan Against Property Through LoanmoneyDocument10 pagesBank of India Loan Against Property Through LoanmoneyMAYUURESH RAVALENo ratings yet

- Annexure - 1: Mode of RepaymentDocument2 pagesAnnexure - 1: Mode of RepaymentJyoti SharmaNo ratings yet

- Company Introduction of Punjab Sind BankDocument9 pagesCompany Introduction of Punjab Sind BankHarsh GogiaNo ratings yet

- Inprinciple LetterDocument1 pageInprinciple LetterDeep PratyakshNo ratings yet

- HL Pni V1 NTR 3596132948944013913 NTR 7818877607244788448Document2 pagesHL Pni V1 NTR 3596132948944013913 NTR 7818877607244788448KanakaReddyKannaNo ratings yet

- MSME Application Up To Rs.2.00 CRDocument9 pagesMSME Application Up To Rs.2.00 CRsayanNo ratings yet

- RBL Mitc FinalDocument40 pagesRBL Mitc Finalwebs adwordNo ratings yet

- DCBDocument10 pagesDCBsaurs2100% (1)

- Transaction StatementDocument2 pagesTransaction StatementSatya GopalNo ratings yet

- Cash MemoDocument7 pagesCash Memovishalsolshe100% (1)

- MUTHOOTDocument14 pagesMUTHOOTnideeshrNo ratings yet

- GanuDocument39 pagesGanuRushikesh JagtapNo ratings yet

- Tata AIA Life Diamond Savings PlanDocument4 pagesTata AIA Life Diamond Savings Plansree db2No ratings yet

- Education LoanDocument9 pagesEducation LoanPriya Tiku KoulNo ratings yet

- Dealer Credit Sale ModuleDocument15 pagesDealer Credit Sale ModuleNakul DixitNo ratings yet

- Commercial Credit Information Report (CCR) - GuideDocument22 pagesCommercial Credit Information Report (CCR) - Guidecyber ageNo ratings yet

- Statement of Account: Date Tran Id Remarks UTR Number Instr. ID Withdrawals Deposits BalanceDocument2 pagesStatement of Account: Date Tran Id Remarks UTR Number Instr. ID Withdrawals Deposits BalanceNAGENDRA SINGH ShekhawatNo ratings yet

- Credit Card Policy Retail 2022Document27 pagesCredit Card Policy Retail 2022Raghav SharmaNo ratings yet

- Project ReportDocument15 pagesProject ReportMichael AdonikarNo ratings yet

- Indian Financial System - An OverviewDocument2 pagesIndian Financial System - An OverviewMadhavKishoreNo ratings yet

- Cibil Score ReportDocument8 pagesCibil Score ReportrogersNo ratings yet

- Credit Information BureauDocument15 pagesCredit Information BureaurishiomkumarNo ratings yet

- Cibil ScoreDocument6 pagesCibil ScoreAnkitNo ratings yet

- This PDF Document Was Edited With Icecream PDF Editor.: Upgrade To PRO To Remove WatermarkDocument4 pagesThis PDF Document Was Edited With Icecream PDF Editor.: Upgrade To PRO To Remove Watermarkgoku spadeNo ratings yet

- School LogoDocument11 pagesSchool Logogoku spadeNo ratings yet

- Final Print File of Standee Design For Capstone ProjectDocument1 pageFinal Print File of Standee Design For Capstone Projectgoku spadeNo ratings yet

- Python ProjectDocument4 pagesPython Projectgoku spadeNo ratings yet

- U 5: M Money: Personal Best B1+ Word ListsDocument6 pagesU 5: M Money: Personal Best B1+ Word Listsxiomara servonesNo ratings yet

- Simple and Compund InterestDocument42 pagesSimple and Compund InterestRayezeus Jaiden Del RosarioNo ratings yet

- Chapter 9 Personal Loans: Personal Finance, 6e (Madura)Document26 pagesChapter 9 Personal Loans: Personal Finance, 6e (Madura)Huỳnh Lữ Thị NhưNo ratings yet

- Arthigamya E-Brochure PDFDocument12 pagesArthigamya E-Brochure PDFAbhinav AnandNo ratings yet

- HL To Salaried ApplicantDocument1 pageHL To Salaried Applicantmaggi14No ratings yet

- Unit-2 The Sale of Goods Act 1930Document15 pagesUnit-2 The Sale of Goods Act 1930angelinstanley2003No ratings yet

- Osg V. Ayala Land IncDocument23 pagesOsg V. Ayala Land IncGLORILYN MONTEJONo ratings yet

- 7AWEFuG2YT3f4RAMH9WLx9raea6HTUSUhcTmRSg1 PDFDocument24 pages7AWEFuG2YT3f4RAMH9WLx9raea6HTUSUhcTmRSg1 PDFNguyễn Thị Hường 3TC-20ACNNo ratings yet

- FOF Group Assignment (Essay)Document9 pagesFOF Group Assignment (Essay)Jie Yin SiowNo ratings yet

- Capital BudgetingDocument6 pagesCapital BudgetingSahil DhingraNo ratings yet

- Circular 257Document5 pagesCircular 257Carlos VelascoNo ratings yet

- 02A C12 Audit Question BankDocument19 pages02A C12 Audit Question Bankyogesh manglaniNo ratings yet

- DBP v. Confesor G.R. No. 48889Document1 pageDBP v. Confesor G.R. No. 48889Rizchelle Sampang-ManaogNo ratings yet

- Real Estate Purchase Offer Form PDFDocument1 pageReal Estate Purchase Offer Form PDFEd williamsonNo ratings yet

- Indemnity Bond From Purchaser: (On Rs-200/-Stamp Paper)Document1 pageIndemnity Bond From Purchaser: (On Rs-200/-Stamp Paper)Shahab ComputersNo ratings yet

- CreditTransactions Reviewer IncompleteDocument41 pagesCreditTransactions Reviewer IncompleteMary Ann Isanan0% (1)

- LB ph2 Sample Paper 20032019Document20 pagesLB ph2 Sample Paper 20032019Tikendra ChandraNo ratings yet

- The Law of Corporate Finance & Securities RegulationDocument26 pagesThe Law of Corporate Finance & Securities Regulationchandni.ambaniandassociatesNo ratings yet

- Ruiz V DimailigDocument2 pagesRuiz V Dimailigneil peirceNo ratings yet

- Tax 3 Chapter 14 Documentary Stamp Tax EditedDocument10 pagesTax 3 Chapter 14 Documentary Stamp Tax Editedokay alexNo ratings yet

- Encompass Loan TrainingDocument9 pagesEncompass Loan TrainingClemente GonzalezNo ratings yet

- LegForms ReportDocument23 pagesLegForms ReportVikki AmorioNo ratings yet

- Lecture 5Document84 pagesLecture 5Lee Li HengNo ratings yet

- NISM-Series-VIII: Equity Derivatives Certification ExaminationDocument20 pagesNISM-Series-VIII: Equity Derivatives Certification ExaminationHitisha agrawalNo ratings yet

- Recommendations of Dahejia and Chore CommitteeDocument3 pagesRecommendations of Dahejia and Chore CommitteeMUDITSAHANINo ratings yet

- Approved CAE - BSA BSMA BSAIS BSIA - ACC 212 - Tenedero - Enriquez 1Document144 pagesApproved CAE - BSA BSMA BSAIS BSIA - ACC 212 - Tenedero - Enriquez 1hdejnNo ratings yet

- Esigned Agreement FormDocument6 pagesEsigned Agreement FormAbdul raheem syedNo ratings yet

- Kraken Intelligence's Crypto Yields - Deconstructing CeFiDocument20 pagesKraken Intelligence's Crypto Yields - Deconstructing CeFiSuraj UmarNo ratings yet