Download as pdf or txt

You might also like

- Complete Material SRI 111 CCPDocument51 pagesComplete Material SRI 111 CCPAnimesh Sen50% (2)

- An Internship Report On Kumari Bank, NepalDocument33 pagesAn Internship Report On Kumari Bank, NepalAmul Shrestha63% (8)

- Do You Think It Was Important For Michael To Stipulate That He Wanted A Business That HeDocument17 pagesDo You Think It Was Important For Michael To Stipulate That He Wanted A Business That Hemiss_hazel85100% (1)

- What Is A Bank ? Introduction: - CrowtherDocument29 pagesWhat Is A Bank ? Introduction: - CrowtherHarbrinder GurmNo ratings yet

- Growth of Banking Sector in India IntroductionDocument12 pagesGrowth of Banking Sector in India IntroductionShaktee Varma0% (1)

- Econtent - Unit 1 - BankingDocument15 pagesEcontent - Unit 1 - BankingMRS.NAMRATA KISHNANI BSSSNo ratings yet

- Banking LawDocument22 pagesBanking LawRASHIKA TRIVEDINo ratings yet

- 10 Chapter 1Document49 pages10 Chapter 1Jay upadhyayNo ratings yet

- Banking System in IndiaDocument25 pagesBanking System in Indiaranikulkarni4uNo ratings yet

- Anitha HDFCDocument84 pagesAnitha HDFCchaluvadiinNo ratings yet

- Banking and Working System of BanksDocument25 pagesBanking and Working System of BanksMohitJangidNo ratings yet

- Management of Banking OperationDocument208 pagesManagement of Banking OperationmanojNo ratings yet

- 00000114-Banking Law Inculding Negotiable Instrument ActDocument47 pages00000114-Banking Law Inculding Negotiable Instrument Actakshay yadavNo ratings yet

- Management of Banking OperationDocument206 pagesManagement of Banking OperationAtul BharshankarNo ratings yet

- Banking: For Other Uses, See - "Banker" and "Bankers" Redirect Here. For Other Uses, SeeDocument20 pagesBanking: For Other Uses, See - "Banker" and "Bankers" Redirect Here. For Other Uses, SeeAnantdeep Singh PuriNo ratings yet

- Introduction To BankingDocument35 pagesIntroduction To Bankingকাশী নাথNo ratings yet

- Banking TheoryDocument56 pagesBanking TheoryChella KuttyNo ratings yet

- What Is A Bank ? IntroductionDocument7 pagesWhat Is A Bank ? IntroductionmanikaNo ratings yet

- Types of Bank DepositsDocument55 pagesTypes of Bank DepositsrocksonNo ratings yet

- Unit IDocument11 pagesUnit IShahid AfreedNo ratings yet

- Training ReportDocument71 pagesTraining ReportHardeep MalikNo ratings yet

- 10 Chapter 3.outputDocument33 pages10 Chapter 3.outputajith kumarNo ratings yet

- Perception of Bankers Toward Merger of ICICI and Bank of RajasthanDocument68 pagesPerception of Bankers Toward Merger of ICICI and Bank of RajasthanBhawana BhagwaniNo ratings yet

- OutsourcingDocument55 pagesOutsourcingNagesh MoreNo ratings yet

- Lending PoliciesDocument68 pagesLending PoliciesAshok Hanumanth HNo ratings yet

- Evolution of BankingDocument73 pagesEvolution of BankingKavita KohliNo ratings yet

- Review of LiteratureDocument64 pagesReview of LiteratureRUTUJA PATILNo ratings yet

- Review of LiteratureDocument65 pagesReview of LiteratureRUTUJA PATILNo ratings yet

- Banking Maths ProjectDocument16 pagesBanking Maths ProjectAakash Sarkar60% (5)

- General Services On BanksDocument38 pagesGeneral Services On Banksdipenparikh91No ratings yet

- Chapter - 01 Introduction of BankDocument37 pagesChapter - 01 Introduction of BankJeeva JeevaNo ratings yet

- History: The, Established in 1694Document19 pagesHistory: The, Established in 1694Kāŕąñ JëthãñíNo ratings yet

- Sbaa 7001Document221 pagesSbaa 7001rishijain9h1No ratings yet

- Importance of The Bank System To The EconomyDocument12 pagesImportance of The Bank System To The EconomyEmil SalmanliNo ratings yet

- Chapter 1 BankingDocument23 pagesChapter 1 BankingKalpana GundumoluNo ratings yet

- Banking TheoryDocument299 pagesBanking TheoryMohammedNo ratings yet

- What Is BankDocument4 pagesWhat Is BankRizwan Akram100% (1)

- Appraisal of The Role of Commercial BankDocument3 pagesAppraisal of The Role of Commercial BankKelly O NwosehNo ratings yet

- Shipping and BankingDocument20 pagesShipping and BankingMamia PoushiNo ratings yet

- BankingDocument123 pagesBankingRohit MehraNo ratings yet

- Chapter 1. Lecture 1.3 Def. of BankDocument6 pagesChapter 1. Lecture 1.3 Def. of BankvibhuNo ratings yet

- The Banking System in Bangladesh: History of BankDocument7 pagesThe Banking System in Bangladesh: History of Bankmirmoinul100% (1)

- The Sealing of The Charter (1694)Document4 pagesThe Sealing of The Charter (1694)Monika KshetriNo ratings yet

- Project On Banking Sector in IndiaDocument45 pagesProject On Banking Sector in IndiaPunit Rao77% (13)

- Bank DXDDocument51 pagesBank DXDbhatiasabNo ratings yet

- Introduction To BanksDocument81 pagesIntroduction To Banksjignas cyberNo ratings yet

- Relationship Between Banker-CustomerDocument14 pagesRelationship Between Banker-Customerrkrakib073No ratings yet

- The Banking System in Bangladesh: Definition of BankDocument10 pagesThe Banking System in Bangladesh: Definition of BankmirmoinulNo ratings yet

- Commercial Banking Final PrintDocument71 pagesCommercial Banking Final PrintnidhiNo ratings yet

- Banking Innovation.: EtymologyDocument78 pagesBanking Innovation.: EtymologyFaisal AnsariNo ratings yet

- Introduction To BankingDocument17 pagesIntroduction To BankingmashalNo ratings yet

- Chapter:-1 Introduction of BankDocument54 pagesChapter:-1 Introduction of BankOmkar ChavanNo ratings yet

- Unit 1: P Sunanda Contract Lecturer in CommerceDocument12 pagesUnit 1: P Sunanda Contract Lecturer in Commerceclashofkinggame3No ratings yet

- History of BankDocument10 pagesHistory of BankSadaf KhanNo ratings yet

- Banking and Banking FundamentalsDocument65 pagesBanking and Banking FundamentalsSirak AynalemNo ratings yet

- Black Book (Sarika)Document56 pagesBlack Book (Sarika)Smruti VasavadaNo ratings yet

- BankingDocument141 pagesBankingc4chita9700No ratings yet

- Fundamental of BankingDocument10 pagesFundamental of BankingAnonymous y3E7iaNo ratings yet

- The Project On Pragathi BankDocument85 pagesThe Project On Pragathi BankPrashanth PBNo ratings yet

- What Is A Payment Bank PDFDocument76 pagesWhat Is A Payment Bank PDFsmithNo ratings yet

- Probation and Parole PresentationDocument6 pagesProbation and Parole PresentationMAYANK GUPTANo ratings yet

- Writ Petition of Zafar HussainDocument10 pagesWrit Petition of Zafar HussainMAYANK GUPTANo ratings yet

- 1968 Page 1 To 195Document201 pages1968 Page 1 To 195MAYANK GUPTANo ratings yet

- No DocumentDocument98 pagesNo DocumentMAYANK GUPTANo ratings yet

- Banking Law 1Document21 pagesBanking Law 1MAYANK GUPTANo ratings yet

- """"""Rill : OooeonDocument7 pages""""""Rill : OooeonMAYANK GUPTANo ratings yet

- Assignment Legal MaximsDocument10 pagesAssignment Legal MaximsMAYANK GUPTANo ratings yet

- Hindu Law - College Notes - For Exames PDFDocument49 pagesHindu Law - College Notes - For Exames PDFMAYANK GUPTANo ratings yet

- Assignment On Droit AdministratifDocument6 pagesAssignment On Droit AdministratifMAYANK GUPTANo ratings yet

- Indication Shall: GustrationaDocument1 pageIndication Shall: GustrationaMAYANK GUPTANo ratings yet

- Indications: Registration of GeographicalDocument1 pageIndications: Registration of GeographicalMAYANK GUPTANo ratings yet

- B.A.LL.B. Syllabus 6th SemesterDocument13 pagesB.A.LL.B. Syllabus 6th SemesterMAYANK GUPTANo ratings yet

- Geographical Incation: RemediesDocument1 pageGeographical Incation: RemediesMAYANK GUPTANo ratings yet

- GI2Document1 pageGI2MAYANK GUPTANo ratings yet

- However,: RegisteredDocument1 pageHowever,: RegisteredMAYANK GUPTANo ratings yet

- Hindi 3rd Semester PDFDocument103 pagesHindi 3rd Semester PDFMAYANK GUPTANo ratings yet

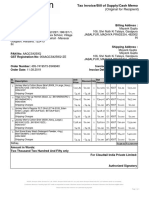

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document2 pagesTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)MAYANK GUPTANo ratings yet

- Supreme Court of IndiaDocument20 pagesSupreme Court of IndiaMAYANK GUPTANo ratings yet

- POLITICAL SCIENCE PresidentialDocument16 pagesPOLITICAL SCIENCE PresidentialMAYANK GUPTANo ratings yet

- Cover Page of ProjectDocument1 pageCover Page of ProjectMAYANK GUPTANo ratings yet

- The Sociological Jurisprudence of Roscoe Pound (Part I)Document27 pagesThe Sociological Jurisprudence of Roscoe Pound (Part I)MAYANK GUPTA100% (1)

- Project-Female As Karta: Chanakya National Law University, PatnaDocument25 pagesProject-Female As Karta: Chanakya National Law University, PatnaMAYANK GUPTANo ratings yet

- Jiubj: Perbandingan Sistem Kesehatan Di Negara Berkembang Dan Negara MajuDocument8 pagesJiubj: Perbandingan Sistem Kesehatan Di Negara Berkembang Dan Negara MajuAnonymous 0XKBEo7j1No ratings yet

- MidtermsDocument8 pagesMidtermsRhea BadanaNo ratings yet

- Map PDFDocument48 pagesMap PDFuwuniverse dailyNo ratings yet

- Retail ManagementDocument19 pagesRetail ManagementAnonymous uxd1ydNo ratings yet

- L3 - Books of Prime Entry & Trial BalanceDocument36 pagesL3 - Books of Prime Entry & Trial BalanceIntan SyuhadaNo ratings yet

- Comandos MPLS Huawei NE y AlcatelDocument6 pagesComandos MPLS Huawei NE y AlcatelJohanna TorresNo ratings yet

- Bookkeeping Essentials For Small BusinessDocument17 pagesBookkeeping Essentials For Small BusinessAccounts and Legal100% (6)

- Chapter Five: Fraud, Internal Control and CashDocument64 pagesChapter Five: Fraud, Internal Control and Cashsamuel asratNo ratings yet

- FSP 3000 Open Fabric Data SheetDocument2 pagesFSP 3000 Open Fabric Data Sheet贾鑫No ratings yet

- Rais12 IM CH13Document13 pagesRais12 IM CH13Alan OsorioNo ratings yet

- Soal Lengkap Pertemuan 6Document4 pagesSoal Lengkap Pertemuan 6tsziNo ratings yet

- BillDocument5 pagesBilldanilacorceNo ratings yet

- Debit CardDocument16 pagesDebit CardAvinash Sahu100% (2)

- Data Analytics in Banking IndustryDocument29 pagesData Analytics in Banking IndustryAnonymous 9n2yDJ0xRNo ratings yet

- PreInt WB Unit1Document4 pagesPreInt WB Unit1Agustín EchevarríaNo ratings yet

- Describe The Problems That Amazon Faced During The 2013 Holiday SeasonDocument8 pagesDescribe The Problems That Amazon Faced During The 2013 Holiday SeasonAbdullah Fahim NabizadaNo ratings yet

- A HandBook On Finacle Work Flow Process 1st EditionDocument79 pagesA HandBook On Finacle Work Flow Process 1st EditionShekhar Suman100% (2)

- Cri 179 Summative AssessmentDocument7 pagesCri 179 Summative AssessmentRegie SalidagaNo ratings yet

- Intermediate Accounting Practice QuestionsDocument4 pagesIntermediate Accounting Practice QuestionsYsa Acupan100% (1)

- Iteb G621 275 C 2007 1Document2 pagesIteb G621 275 C 2007 1saket reddyNo ratings yet

- Viclink Journey Planner - Your Guide ToDocument1 pageViclink Journey Planner - Your Guide Toapi-22292888No ratings yet

- E-Ticket Receipt & Itinerary: Passenger and Ticket InformationDocument3 pagesE-Ticket Receipt & Itinerary: Passenger and Ticket InformationKathy GardnerNo ratings yet

- Learning Activity No. 6Document13 pagesLearning Activity No. 6Jonah MaasinNo ratings yet

- Process Change Log 202404Document31 pagesProcess Change Log 202404praneet891No ratings yet

- Gogo Brochure BizDocument16 pagesGogo Brochure BizSilas AntoniolliNo ratings yet

- BFI Topic 1 2 3Document17 pagesBFI Topic 1 2 3Arnold LuayonNo ratings yet

- Bjain Statement PDFDocument2 pagesBjain Statement PDFManish JainNo ratings yet