Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5824)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Most Important Biblical Discovery of Our TimeDocument21 pagesThe Most Important Biblical Discovery of Our Timececampillo100% (1)

- Crescent All CAF Mocks QP With Solutions Compiled by Saboor AhmadDocument124 pagesCrescent All CAF Mocks QP With Solutions Compiled by Saboor AhmadAr Sal AnNo ratings yet

- Challan #: Challan #: Challan #:: Total Total TotalDocument1 pageChallan #: Challan #: Challan #:: Total Total TotalAr Sal AnNo ratings yet

- Far 2 Vol1 by Sir Jawad - 2022-08-03 10-11-29Document298 pagesFar 2 Vol1 by Sir Jawad - 2022-08-03 10-11-29Ar Sal AnNo ratings yet

- My Suggestions For Upcoming Council MeetingDocument10 pagesMy Suggestions For Upcoming Council MeetingAr Sal AnNo ratings yet

- Basics of PhotographyDocument25 pagesBasics of PhotographyAr Sal AnNo ratings yet

- El Ensayo Del Gato NegroDocument4 pagesEl Ensayo Del Gato Negroafefhrxqv100% (1)

- Roman AchievementsDocument22 pagesRoman Achievementsapi-294843376No ratings yet

- FEU: Annual ReportDocument266 pagesFEU: Annual ReportBusinessWorldNo ratings yet

- Brooklyn Mitsubishi Petition Notice To Respondents Schedules A-GDocument98 pagesBrooklyn Mitsubishi Petition Notice To Respondents Schedules A-GQueens PostNo ratings yet

- Lesson 9. Phylum Mollusca PDFDocument44 pagesLesson 9. Phylum Mollusca PDFJonard PedrosaNo ratings yet

- Barcode Scanner, Wireless Barcode Scanner, DC5112 Barcode ScannerDocument3 pagesBarcode Scanner, Wireless Barcode Scanner, DC5112 Barcode ScannerdcodeNo ratings yet

- POLEFDNDocument10 pagesPOLEFDNcoolkaisyNo ratings yet

- Primary Gingival Squamous Cell CarcinomaDocument7 pagesPrimary Gingival Squamous Cell CarcinomaMandyWilsonNo ratings yet

- Karakteristik Material Baja St.37 Dengan Temperatur Dan Waktu Pada Uji Heat Treatment Menggunakan FurnaceDocument14 pagesKarakteristik Material Baja St.37 Dengan Temperatur Dan Waktu Pada Uji Heat Treatment Menggunakan FurnaceYudii NggiNo ratings yet

- Contemporary World: Colt Ian U. Del CastilloDocument34 pagesContemporary World: Colt Ian U. Del CastilloNORBERT JAY DECLARONo ratings yet

- Intra Asia 20240129 083100041155315Document19 pagesIntra Asia 20240129 083100041155315joegesang07No ratings yet

- Practical Work 1 EventDocument19 pagesPractical Work 1 EventNur ShakirinNo ratings yet

- Santiago City, Isabela: University of La Salette, IncDocument1 pageSantiago City, Isabela: University of La Salette, IncLUCAS, PATRICK JOHNNo ratings yet

- ProfEd9 Module 9Document6 pagesProfEd9 Module 9Roxanne GuzmanNo ratings yet

- Studies On Soil Structure Interaction of Multi Storeyed Buildings With Rigid and Flexible FoundationDocument8 pagesStudies On Soil Structure Interaction of Multi Storeyed Buildings With Rigid and Flexible FoundationAayush jhaNo ratings yet

- BBB October 2023 Super SpecialsDocument4 pagesBBB October 2023 Super Specialsactionrazor38No ratings yet

- Learn Computer in Simple StepsDocument104 pagesLearn Computer in Simple StepsSparkle SocietyNo ratings yet

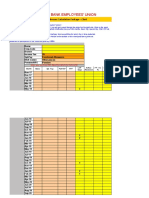

- Karur Vysya Bank Employees' Union: 11th Bipartite Arrears Calculation Package - ClerkDocument10 pagesKarur Vysya Bank Employees' Union: 11th Bipartite Arrears Calculation Package - ClerkDeepa ManianNo ratings yet

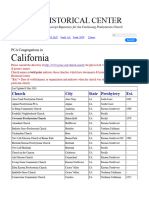

- PCA Churches in CaliforniaDocument4 pagesPCA Churches in CaliforniaLIGHT GNo ratings yet

- Petitioner vs. VS.: Third DivisionDocument12 pagesPetitioner vs. VS.: Third DivisionAnonymous QR87KCVteNo ratings yet

- ICF Team Coaching Competencies: Moving Beyond One-to-One CoachingDocument21 pagesICF Team Coaching Competencies: Moving Beyond One-to-One CoachingMarko PyNo ratings yet

- 08 Package Engineering Design Testing PDFDocument57 pages08 Package Engineering Design Testing PDFLake HouseNo ratings yet

- Adebabay AbayDocument23 pagesAdebabay Abaymaheder wegayehuNo ratings yet

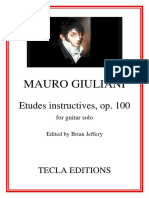

- Mauro Giuliani: Etudes Instructives, Op. 100Document35 pagesMauro Giuliani: Etudes Instructives, Op. 100Thiago Camargo Juvito de Souza100% (1)

- ModulationDocument7 pagesModulationSyeda MiznaNo ratings yet

- Small Unit Operations: PMA Core Values: Selfless Service To God and Country, Honor, ExcellenceDocument33 pagesSmall Unit Operations: PMA Core Values: Selfless Service To God and Country, Honor, ExcellenceAbay GeeNo ratings yet

- En 12245 (2022) (E)Document9 pagesEn 12245 (2022) (E)David Chirinos100% (1)

- TDS Conbextra GP2 BFLDocument4 pagesTDS Conbextra GP2 BFLsabbirNo ratings yet

- Sample Thesis 2Document127 pagesSample Thesis 2Carlo Troy AcelottNo ratings yet