Evaluation of Ethical Mutual Fund

Evaluation of Ethical Mutual Fund

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5834)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (350)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (824)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (405)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Indonesia Flexible Packaging Market Growth, Trends, COVID 19 ImpactDocument135 pagesIndonesia Flexible Packaging Market Growth, Trends, COVID 19 ImpactIndah YuneNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Theories of Crime CausationDocument59 pagesTheories of Crime CausationRey John Dizon88% (32)

- Revisiting The Jalong Ambush Site (Hussars)Document41 pagesRevisiting The Jalong Ambush Site (Hussars)stmcipohNo ratings yet

- Occupational Health and Safety ReportDocument6 pagesOccupational Health and Safety Reportخالد نسیمNo ratings yet

- How To Cite: Marikyan, D. & Papagiannidis, S. (2022) Technology Acceptance Model: ADocument12 pagesHow To Cite: Marikyan, D. & Papagiannidis, S. (2022) Technology Acceptance Model: AvineethkmenonNo ratings yet

- Performance Evaluation of Systematic Investment Plans in Top Rated Conservative Hybrid Mutual Funds During 2016-18Document4 pagesPerformance Evaluation of Systematic Investment Plans in Top Rated Conservative Hybrid Mutual Funds During 2016-18vineethkmenonNo ratings yet

- Journal of Destination Marketing & Management: Giacomo Del Chiappa, Rodolfo BaggioDocument6 pagesJournal of Destination Marketing & Management: Giacomo Del Chiappa, Rodolfo BaggiovineethkmenonNo ratings yet

- PG Project PPT (Revathykrishna PS)Document24 pagesPG Project PPT (Revathykrishna PS)vineethkmenonNo ratings yet

- Camel AnalysisDocument12 pagesCamel AnalysisvineethkmenonNo ratings yet

- Chapter 14 Foundations of Behavior: True/False QuestionsDocument35 pagesChapter 14 Foundations of Behavior: True/False QuestionsvineethkmenonNo ratings yet

- Project PPT (ASHA V S)Document18 pagesProject PPT (ASHA V S)vineethkmenonNo ratings yet

- Emotional Finance: Financial Anxiety Among Salaried Individuals With Special Reference To Life InsuranceDocument13 pagesEmotional Finance: Financial Anxiety Among Salaried Individuals With Special Reference To Life InsurancevineethkmenonNo ratings yet

- Sruthy Vineeth STC Full PaperDocument5 pagesSruthy Vineeth STC Full PapervineethkmenonNo ratings yet

- Teaching Aptitude For UGCDocument13 pagesTeaching Aptitude For UGCvineethkmenonNo ratings yet

- Bcom - Semester V Cm05Baa02 - Special Accounting Multiple Choice QuestionsDocument14 pagesBcom - Semester V Cm05Baa02 - Special Accounting Multiple Choice QuestionsvineethkmenonNo ratings yet

- Accounting For Managerial DecisionsDocument22 pagesAccounting For Managerial DecisionsvineethkmenonNo ratings yet

- KMRL ProjectDocument48 pagesKMRL Projectvineethkmenon80% (10)

- Famous Festivals in Kerala PDFDocument19 pagesFamous Festivals in Kerala PDFvineethkmenonNo ratings yet

- Bcom - Semester V1 Cm06Baa02 - Practcal Auditing Multiple Choice QuestionsDocument19 pagesBcom - Semester V1 Cm06Baa02 - Practcal Auditing Multiple Choice Questionsvineethkmenon100% (2)

- Core 13 Applied Ethics (4) 20 - 02Document3 pagesCore 13 Applied Ethics (4) 20 - 02vineethkmenonNo ratings yet

- KFC FORM 7 Report of Transfer of Charge PDFDocument2 pagesKFC FORM 7 Report of Transfer of Charge PDFvineethkmenon100% (1)

- Kerala Service Rules Full - Uploaded by T James Joseph Adhikarathil, Deputy Collector Alappuzha.Document215 pagesKerala Service Rules Full - Uploaded by T James Joseph Adhikarathil, Deputy Collector Alappuzha.James AdhikaramNo ratings yet

- MCQ GST Answer KeyDocument23 pagesMCQ GST Answer KeyvineethkmenonNo ratings yet

- UG Model QP MergedDocument93 pagesUG Model QP MergedvineethkmenonNo ratings yet

- Kwÿm/ Ktωf/W: D∂X Hnzym-'Ymk A≤Ym-) I KwlwDocument2 pagesKwÿm/ Ktωf/W: D∂X Hnzym-'Ymk A≤Ym-) I KwlwvineethkmenonNo ratings yet

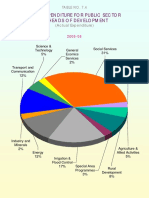

- Five Yaer Plan: Plan Expenditure For Public Sector by Heads of DevelopmentDocument1 pageFive Yaer Plan: Plan Expenditure For Public Sector by Heads of DevelopmentvineethkmenonNo ratings yet

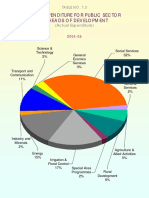

- Five Yaer Plan: Plan Expenditure For Public Sector by Heads of DevelopmentDocument1 pageFive Yaer Plan: Plan Expenditure For Public Sector by Heads of DevelopmentvineethkmenonNo ratings yet

- Dialogue Cause and Effect About Global WarmingDocument4 pagesDialogue Cause and Effect About Global WarmingGrace HanyNo ratings yet

- Customer Satisfaction On TATA Motors-7Document40 pagesCustomer Satisfaction On TATA Motors-7VampsiukNo ratings yet

- Topic: Student Politics in PakistanDocument7 pagesTopic: Student Politics in PakistanIrfan FarooqNo ratings yet

- Nnadili v. Chevron U.s.a., Inc.Document10 pagesNnadili v. Chevron U.s.a., Inc.RavenFoxNo ratings yet

- Copia de The Green Banana Lecturas I 2020Document4 pagesCopia de The Green Banana Lecturas I 2020Finn SolórzanoNo ratings yet

- Indian Institute of Information Technology, Surat: SVNIT Campus, Ichchanath, Surat - 395007Document1 pageIndian Institute of Information Technology, Surat: SVNIT Campus, Ichchanath, Surat - 395007gopalgeniusNo ratings yet

- Practical 2 Mohd Fahmi Bin Ahmad Jamizi BEHP22106112Document138 pagesPractical 2 Mohd Fahmi Bin Ahmad Jamizi BEHP22106112Tunnel The4thAvenueNo ratings yet

- ThesisDocument5 pagesThesisSampayan Angelica A.No ratings yet

- AFC Asian Cup China 2023 Qualifiers Final Round Match ScheduleDocument6 pagesAFC Asian Cup China 2023 Qualifiers Final Round Match ScheduleretalintoNo ratings yet

- 2 - AC Corporation (ACC) v. CIRDocument20 pages2 - AC Corporation (ACC) v. CIRCarlota VillaromanNo ratings yet

- Qazi Zahed IqbalDocument95 pagesQazi Zahed IqbalMus'ab AhnafNo ratings yet

- "Apocalypsis" - Future Revealed-Study 1Document14 pages"Apocalypsis" - Future Revealed-Study 1Aleksandar Miriam PopovskiNo ratings yet

- The Insiders Game How Elites Make War and Peace Elizabeth N Saunders Full ChapterDocument67 pagesThe Insiders Game How Elites Make War and Peace Elizabeth N Saunders Full Chapterjoann.lamb584100% (16)

- MINORS TRAVELLING ABROAD Application Form Affidavit of Support and Consent Affidavit of UndertakingDocument3 pagesMINORS TRAVELLING ABROAD Application Form Affidavit of Support and Consent Affidavit of UndertakingBhong caneteNo ratings yet

- Servant-Leadership in Higher Education: A Look Through Students' EyesDocument30 pagesServant-Leadership in Higher Education: A Look Through Students' Eyeschrist_wisnuNo ratings yet

- Khelo India Event Wise Bib ListDocument20 pagesKhelo India Event Wise Bib ListSudhit SethiNo ratings yet

- Ers. Co M: JANA Master Fund, Ltd. Performance Update - December 2010 Fourth Quarter and Year in ReviewDocument10 pagesErs. Co M: JANA Master Fund, Ltd. Performance Update - December 2010 Fourth Quarter and Year in ReviewVolcaneum100% (2)

- Current Trends Issues and Problems in Education SystemDocument49 pagesCurrent Trends Issues and Problems in Education SystemfuellasjericNo ratings yet

- Unit-5 Pollution Notes by AmishaDocument18 pagesUnit-5 Pollution Notes by AmishaRoonah KayNo ratings yet

- Quiambao v. Bamba (2005)Document2 pagesQuiambao v. Bamba (2005)JD DX100% (1)

- Equatorial Realty Vs Mayfair TheaterDocument2 pagesEquatorial Realty Vs Mayfair TheaterSaji Jimeno100% (1)

- Week 9 Jose Rizal's Second Travel AbroadDocument6 pagesWeek 9 Jose Rizal's Second Travel AbroadShervee PabalateNo ratings yet

- 03 Tiongson Cayetano Et Al Vs Court of Appeals Et AlDocument6 pages03 Tiongson Cayetano Et Al Vs Court of Appeals Et Alrandelrocks2No ratings yet

- Melaka in China Ming TextsDocument40 pagesMelaka in China Ming Textsmifago8887No ratings yet

- Jeopardy SolutionsDocument14 pagesJeopardy SolutionsMirkan OrdeNo ratings yet

- Commerce PPT AmbedkarDocument14 pagesCommerce PPT Ambedkarpritesh.ks1409No ratings yet

Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5834)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (350)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (824)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (405)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Indonesia Flexible Packaging Market Growth, Trends, COVID 19 ImpactDocument135 pagesIndonesia Flexible Packaging Market Growth, Trends, COVID 19 ImpactIndah YuneNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Theories of Crime CausationDocument59 pagesTheories of Crime CausationRey John Dizon88% (32)

- Revisiting The Jalong Ambush Site (Hussars)Document41 pagesRevisiting The Jalong Ambush Site (Hussars)stmcipohNo ratings yet

- Occupational Health and Safety ReportDocument6 pagesOccupational Health and Safety Reportخالد نسیمNo ratings yet

- How To Cite: Marikyan, D. & Papagiannidis, S. (2022) Technology Acceptance Model: ADocument12 pagesHow To Cite: Marikyan, D. & Papagiannidis, S. (2022) Technology Acceptance Model: AvineethkmenonNo ratings yet

- Performance Evaluation of Systematic Investment Plans in Top Rated Conservative Hybrid Mutual Funds During 2016-18Document4 pagesPerformance Evaluation of Systematic Investment Plans in Top Rated Conservative Hybrid Mutual Funds During 2016-18vineethkmenonNo ratings yet

- Journal of Destination Marketing & Management: Giacomo Del Chiappa, Rodolfo BaggioDocument6 pagesJournal of Destination Marketing & Management: Giacomo Del Chiappa, Rodolfo BaggiovineethkmenonNo ratings yet

- PG Project PPT (Revathykrishna PS)Document24 pagesPG Project PPT (Revathykrishna PS)vineethkmenonNo ratings yet

- Camel AnalysisDocument12 pagesCamel AnalysisvineethkmenonNo ratings yet

- Chapter 14 Foundations of Behavior: True/False QuestionsDocument35 pagesChapter 14 Foundations of Behavior: True/False QuestionsvineethkmenonNo ratings yet

- Project PPT (ASHA V S)Document18 pagesProject PPT (ASHA V S)vineethkmenonNo ratings yet

- Emotional Finance: Financial Anxiety Among Salaried Individuals With Special Reference To Life InsuranceDocument13 pagesEmotional Finance: Financial Anxiety Among Salaried Individuals With Special Reference To Life InsurancevineethkmenonNo ratings yet

- Sruthy Vineeth STC Full PaperDocument5 pagesSruthy Vineeth STC Full PapervineethkmenonNo ratings yet

- Teaching Aptitude For UGCDocument13 pagesTeaching Aptitude For UGCvineethkmenonNo ratings yet

- Bcom - Semester V Cm05Baa02 - Special Accounting Multiple Choice QuestionsDocument14 pagesBcom - Semester V Cm05Baa02 - Special Accounting Multiple Choice QuestionsvineethkmenonNo ratings yet

- Accounting For Managerial DecisionsDocument22 pagesAccounting For Managerial DecisionsvineethkmenonNo ratings yet

- KMRL ProjectDocument48 pagesKMRL Projectvineethkmenon80% (10)

- Famous Festivals in Kerala PDFDocument19 pagesFamous Festivals in Kerala PDFvineethkmenonNo ratings yet

- Bcom - Semester V1 Cm06Baa02 - Practcal Auditing Multiple Choice QuestionsDocument19 pagesBcom - Semester V1 Cm06Baa02 - Practcal Auditing Multiple Choice Questionsvineethkmenon100% (2)

- Core 13 Applied Ethics (4) 20 - 02Document3 pagesCore 13 Applied Ethics (4) 20 - 02vineethkmenonNo ratings yet

- KFC FORM 7 Report of Transfer of Charge PDFDocument2 pagesKFC FORM 7 Report of Transfer of Charge PDFvineethkmenon100% (1)

- Kerala Service Rules Full - Uploaded by T James Joseph Adhikarathil, Deputy Collector Alappuzha.Document215 pagesKerala Service Rules Full - Uploaded by T James Joseph Adhikarathil, Deputy Collector Alappuzha.James AdhikaramNo ratings yet

- MCQ GST Answer KeyDocument23 pagesMCQ GST Answer KeyvineethkmenonNo ratings yet

- UG Model QP MergedDocument93 pagesUG Model QP MergedvineethkmenonNo ratings yet

- Kwÿm/ Ktωf/W: D∂X Hnzym-'Ymk A≤Ym-) I KwlwDocument2 pagesKwÿm/ Ktωf/W: D∂X Hnzym-'Ymk A≤Ym-) I KwlwvineethkmenonNo ratings yet

- Five Yaer Plan: Plan Expenditure For Public Sector by Heads of DevelopmentDocument1 pageFive Yaer Plan: Plan Expenditure For Public Sector by Heads of DevelopmentvineethkmenonNo ratings yet

- Five Yaer Plan: Plan Expenditure For Public Sector by Heads of DevelopmentDocument1 pageFive Yaer Plan: Plan Expenditure For Public Sector by Heads of DevelopmentvineethkmenonNo ratings yet

- Dialogue Cause and Effect About Global WarmingDocument4 pagesDialogue Cause and Effect About Global WarmingGrace HanyNo ratings yet

- Customer Satisfaction On TATA Motors-7Document40 pagesCustomer Satisfaction On TATA Motors-7VampsiukNo ratings yet

- Topic: Student Politics in PakistanDocument7 pagesTopic: Student Politics in PakistanIrfan FarooqNo ratings yet

- Nnadili v. Chevron U.s.a., Inc.Document10 pagesNnadili v. Chevron U.s.a., Inc.RavenFoxNo ratings yet

- Copia de The Green Banana Lecturas I 2020Document4 pagesCopia de The Green Banana Lecturas I 2020Finn SolórzanoNo ratings yet

- Indian Institute of Information Technology, Surat: SVNIT Campus, Ichchanath, Surat - 395007Document1 pageIndian Institute of Information Technology, Surat: SVNIT Campus, Ichchanath, Surat - 395007gopalgeniusNo ratings yet

- Practical 2 Mohd Fahmi Bin Ahmad Jamizi BEHP22106112Document138 pagesPractical 2 Mohd Fahmi Bin Ahmad Jamizi BEHP22106112Tunnel The4thAvenueNo ratings yet

- ThesisDocument5 pagesThesisSampayan Angelica A.No ratings yet

- AFC Asian Cup China 2023 Qualifiers Final Round Match ScheduleDocument6 pagesAFC Asian Cup China 2023 Qualifiers Final Round Match ScheduleretalintoNo ratings yet

- 2 - AC Corporation (ACC) v. CIRDocument20 pages2 - AC Corporation (ACC) v. CIRCarlota VillaromanNo ratings yet

- Qazi Zahed IqbalDocument95 pagesQazi Zahed IqbalMus'ab AhnafNo ratings yet

- "Apocalypsis" - Future Revealed-Study 1Document14 pages"Apocalypsis" - Future Revealed-Study 1Aleksandar Miriam PopovskiNo ratings yet

- The Insiders Game How Elites Make War and Peace Elizabeth N Saunders Full ChapterDocument67 pagesThe Insiders Game How Elites Make War and Peace Elizabeth N Saunders Full Chapterjoann.lamb584100% (16)

- MINORS TRAVELLING ABROAD Application Form Affidavit of Support and Consent Affidavit of UndertakingDocument3 pagesMINORS TRAVELLING ABROAD Application Form Affidavit of Support and Consent Affidavit of UndertakingBhong caneteNo ratings yet

- Servant-Leadership in Higher Education: A Look Through Students' EyesDocument30 pagesServant-Leadership in Higher Education: A Look Through Students' Eyeschrist_wisnuNo ratings yet

- Khelo India Event Wise Bib ListDocument20 pagesKhelo India Event Wise Bib ListSudhit SethiNo ratings yet

- Ers. Co M: JANA Master Fund, Ltd. Performance Update - December 2010 Fourth Quarter and Year in ReviewDocument10 pagesErs. Co M: JANA Master Fund, Ltd. Performance Update - December 2010 Fourth Quarter and Year in ReviewVolcaneum100% (2)

- Current Trends Issues and Problems in Education SystemDocument49 pagesCurrent Trends Issues and Problems in Education SystemfuellasjericNo ratings yet

- Unit-5 Pollution Notes by AmishaDocument18 pagesUnit-5 Pollution Notes by AmishaRoonah KayNo ratings yet

- Quiambao v. Bamba (2005)Document2 pagesQuiambao v. Bamba (2005)JD DX100% (1)

- Equatorial Realty Vs Mayfair TheaterDocument2 pagesEquatorial Realty Vs Mayfair TheaterSaji Jimeno100% (1)

- Week 9 Jose Rizal's Second Travel AbroadDocument6 pagesWeek 9 Jose Rizal's Second Travel AbroadShervee PabalateNo ratings yet

- 03 Tiongson Cayetano Et Al Vs Court of Appeals Et AlDocument6 pages03 Tiongson Cayetano Et Al Vs Court of Appeals Et Alrandelrocks2No ratings yet

- Melaka in China Ming TextsDocument40 pagesMelaka in China Ming Textsmifago8887No ratings yet

- Jeopardy SolutionsDocument14 pagesJeopardy SolutionsMirkan OrdeNo ratings yet

- Commerce PPT AmbedkarDocument14 pagesCommerce PPT Ambedkarpritesh.ks1409No ratings yet