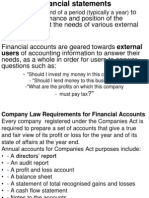

Financial Modeling

Financial Modeling

You might also like

- D196 Study Guide Answers & NotesDocument21 pagesD196 Study Guide Answers & NotesAsril Doank100% (1)

- Cheat Sheet Exam 1Document1 pageCheat Sheet Exam 1Shashi Gavini Keil100% (2)

- The Master Budget - 1st QTRDocument41 pagesThe Master Budget - 1st QTRqueene50% (4)

- SAP Business Planning and Consolidation OverviewDocument33 pagesSAP Business Planning and Consolidation Overviewmayurnanda86100% (1)

- P2P and Assets EntriesDocument7 pagesP2P and Assets Entriessudheer1112No ratings yet

- Funds Flow Statement Tirumala MilkDocument101 pagesFunds Flow Statement Tirumala MilkSakhamuri Ram's100% (3)

- Accounting ReviewerDocument3 pagesAccounting ReviewerK ByeNo ratings yet

- Financial Management Midterm Reviewer 1Document3 pagesFinancial Management Midterm Reviewer 1Margaret Joy SobredillaNo ratings yet

- FAR Module 4Document13 pagesFAR Module 4Michael Angelo DawisNo ratings yet

- Impacting The Financial StatementsclassDocument23 pagesImpacting The Financial StatementsclassMonkey2111No ratings yet

- Financial Analysis, Depreciation and Time Value Analysis: Presented By: Najat AlbuhendiDocument33 pagesFinancial Analysis, Depreciation and Time Value Analysis: Presented By: Najat AlbuhendiNagnoaga AlNo ratings yet

- Financial Statement Analys Lecture 1stDocument16 pagesFinancial Statement Analys Lecture 1stSaeed UllahNo ratings yet

- Financial ManagementDocument50 pagesFinancial ManagementLEO FRAGGERNo ratings yet

- Basic FS - Income Statement For Service Business and Statement of Changes in Owner's EquityDocument11 pagesBasic FS - Income Statement For Service Business and Statement of Changes in Owner's Equityckbeom0No ratings yet

- Understanding Financial StatementsDocument32 pagesUnderstanding Financial StatementsAravinda RuwanNo ratings yet

- Qualifying Exam Reviewer 1Document26 pagesQualifying Exam Reviewer 1dlaronyvette100% (2)

- Report in Business Finance: Group 2 - Review of Financial Statement Preparation, Analysis, and InterpretationDocument14 pagesReport in Business Finance: Group 2 - Review of Financial Statement Preparation, Analysis, and InterpretationKOUJI N. MARQUEZNo ratings yet

- Final Accounts 1Document25 pagesFinal Accounts 1ken philipsNo ratings yet

- Chapter - 11 Financial Statement AnalysisDocument14 pagesChapter - 11 Financial Statement AnalysisAntora Hoque100% (1)

- Buss1030 Notes: 1.1 Factors Affecting The Complexity of A Changing Business EnvironmentDocument56 pagesBuss1030 Notes: 1.1 Factors Affecting The Complexity of A Changing Business EnvironmentTINo ratings yet

- Chapter 2 Analysis of Financial Statement IDocument33 pagesChapter 2 Analysis of Financial Statement ISuku Thomas SamuelNo ratings yet

- Financial Analysis GuideDocument6 pagesFinancial Analysis GuideRomelyn Joy JangaoNo ratings yet

- 01 Lecture - MT - ch01 - 0607-082023 - Acctg Concepts 01Document22 pages01 Lecture - MT - ch01 - 0607-082023 - Acctg Concepts 01JIM KYRONE GENOBISANo ratings yet

- What Is Financial Management?Document43 pagesWhat Is Financial Management?Jonas AlcantaraNo ratings yet

- ReviewerDocument3 pagesReviewerMelanie AmandoronNo ratings yet

- Self Study - Financial Accounting Chapter 1 To Chapter 4Document23 pagesSelf Study - Financial Accounting Chapter 1 To Chapter 4Ana Saggio0% (1)

- Chapter 2 Financial AnalysisDocument26 pagesChapter 2 Financial AnalysisCarl JovianNo ratings yet

- Learning Objectives: Review of Financial Statement Preparation: Analysis and InterpretationDocument4 pagesLearning Objectives: Review of Financial Statement Preparation: Analysis and InterpretationArleneNo ratings yet

- Corporate FinanceDocument51 pagesCorporate FinanceAnna FossiNo ratings yet

- Week 14 IMPLEMENT THE BUSINESS PLANDocument16 pagesWeek 14 IMPLEMENT THE BUSINESS PLANJuan Miguel SalvadorNo ratings yet

- Introduction To Financial AccountingDocument64 pagesIntroduction To Financial AccountingGurkirat Singh100% (1)

- FINANCIAL REPORTING - ScriptDocument9 pagesFINANCIAL REPORTING - ScriptMutesa ChrisNo ratings yet

- Assessment 3 Task 1 MONITOR AND CONTROLDocument3 pagesAssessment 3 Task 1 MONITOR AND CONTROLvalegiraldoNo ratings yet

- WK 1 Introduction To Accounting - CutDocument59 pagesWK 1 Introduction To Accounting - CutThùy Linh Lê ThịNo ratings yet

- Funds Flow StatementDocument101 pagesFunds Flow StatementSakhamuri Ram'sNo ratings yet

- FS ReviewerDocument11 pagesFS Reviewertiniee0510No ratings yet

- SHS Business Finance Chapter 2Document24 pagesSHS Business Finance Chapter 2Ji BaltazarNo ratings yet

- RatiosDocument6 pagesRatiosFaisal AwanNo ratings yet

- FINMAN Notes - April 14, 2021Document10 pagesFINMAN Notes - April 14, 2021Nicole Andrea TuazonNo ratings yet

- Acct1501 Notes: 1. Introduction To Financial AccountingDocument11 pagesAcct1501 Notes: 1. Introduction To Financial AccountingLena ZhengNo ratings yet

- LESSON 1 ReviewerDocument8 pagesLESSON 1 ReviewerJehan VonneNo ratings yet

- Abm FM Unit 1Document16 pagesAbm FM Unit 1Indu MazumdarNo ratings yet

- Key Steps Involved in Financial Statement AnalysisDocument2 pagesKey Steps Involved in Financial Statement AnalysisManzil ShresthaNo ratings yet

- Branches of AccountingDocument54 pagesBranches of AccountingAbby Rosales - Perez100% (1)

- V. Basic Interprestation and Use of Financial StatementsDocument12 pagesV. Basic Interprestation and Use of Financial StatementsJHERICA SURELLNo ratings yet

- Finman ReviewerDocument17 pagesFinman ReviewerSheila Mae Guerta LaceronaNo ratings yet

- ACCOUNTING-WPS OfficeDocument6 pagesACCOUNTING-WPS OfficeNorjehanie AliNo ratings yet

- 03 04 Analysis Financial StatementDocument216 pages03 04 Analysis Financial StatementShanique Y. Harnett100% (1)

- Do 1221Document27 pagesDo 1221muluabebaw287No ratings yet

- Lec 2Document38 pagesLec 2Mohamed AliNo ratings yet

- Financial StatementsDocument31 pagesFinancial StatementsJeahMaureenDominguez100% (2)

- Analysis of Financial StatementDocument9 pagesAnalysis of Financial Statementmorcoangelicafaith8No ratings yet

- Answer 1.: Straight Line DepreciationDocument11 pagesAnswer 1.: Straight Line DepreciationDanish ShaikhNo ratings yet

- Int I Midterm ReviewDocument7 pagesInt I Midterm ReviewshevinakNo ratings yet

- Assessing A New Venture's Financial Strength and ViabilityDocument6 pagesAssessing A New Venture's Financial Strength and ViabilityAsif KureishiNo ratings yet

- 1Document34 pages1TOLENTINO, Julius Mark VirayNo ratings yet

- Information Sheet - BKKPG-8 - Preparing Financial StatementsDocument10 pagesInformation Sheet - BKKPG-8 - Preparing Financial StatementsEron Roi Centina-gacutanNo ratings yet

- Section 1: Introduction To Principles of AccountsDocument6 pagesSection 1: Introduction To Principles of AccountsArcherAcsNo ratings yet

- Accounting and Financial StatementsDocument14 pagesAccounting and Financial StatementsMitha LarasNo ratings yet

- FAC1502 Accounting Study Guide QuestionsDocument34 pagesFAC1502 Accounting Study Guide QuestionszinesunduzaNo ratings yet

- The Entrepreneur’S Dictionary of Business and Financial TermsFrom EverandThe Entrepreneur’S Dictionary of Business and Financial TermsNo ratings yet

- Inventories and Cost of SalesDocument18 pagesInventories and Cost of SalesAmor HalitimNo ratings yet

- Financial StatementsDocument23 pagesFinancial StatementsShin Shan JeonNo ratings yet

- MGMT 30A: Practice FinalDocument18 pagesMGMT 30A: Practice FinalFUSION AcademicsNo ratings yet

- Earnings Release: 9 Months - 2009Document34 pagesEarnings Release: 9 Months - 2009DGC_thenationalNo ratings yet

- Admission and Retirement Long QuestionDocument11 pagesAdmission and Retirement Long QuestionMenu GargNo ratings yet

- Soal Soal AklanDocument30 pagesSoal Soal AklanFikri Sya'bana100% (1)

- Term Paper On Capital Budgeting TechniquesDocument5 pagesTerm Paper On Capital Budgeting Techniquesc5pcnpd6100% (1)

- Bfe 425 Assignment 3 2023Document3 pagesBfe 425 Assignment 3 2023Chikarakara LloydNo ratings yet

- Profit PlanningDocument43 pagesProfit PlanningLouiseNo ratings yet

- Dividend Discount AND Dividend Growth Model: BY Raman Surajit Rajesh PriyankaDocument14 pagesDividend Discount AND Dividend Growth Model: BY Raman Surajit Rajesh Priyankapriyanka2538No ratings yet

- Final Exam - Fall 2023Document5 pagesFinal Exam - Fall 2023hani.sharma324No ratings yet

- ACC 203 Ch08 SolutionsDocument7 pagesACC 203 Ch08 Solutionsomaritani2005No ratings yet

- Sole Trader: Final Accounts - The Income StatementDocument12 pagesSole Trader: Final Accounts - The Income StatementAnisahNo ratings yet

- Cost of CapitalDocument41 pagesCost of CapitalMCDABCNo ratings yet

- New Chapter 17 - Cash FlowDocument17 pagesNew Chapter 17 - Cash FlowCheyenne Dawhitegurl GuillNo ratings yet

- Format of Financial StatementsDocument2 pagesFormat of Financial StatementsAmeerul HarithNo ratings yet

- ACCA102 - 13 Noncurrent Asset Held For SaleDocument20 pagesACCA102 - 13 Noncurrent Asset Held For SaleMary Kate OrobiaNo ratings yet

- BDP Financial Final PartDocument14 pagesBDP Financial Final PartDeepak G.C.No ratings yet

- Group 1 Section A PDFDocument14 pagesGroup 1 Section A PDFNayeem Md Sakib100% (1)

- CFAS - Midterm Exam Set ADocument7 pagesCFAS - Midterm Exam Set ADesiree Angelique RebonquinNo ratings yet

- LECTURE 7 - Chapter 10 Auditing The Revenue ProcessDocument35 pagesLECTURE 7 - Chapter 10 Auditing The Revenue ProcessamyNo ratings yet

- Cima p4Document3 pagesCima p4fawad aslamNo ratings yet

- Chapter 5 Incomplete RecordDocument20 pagesChapter 5 Incomplete RecordNUR ADLIN ZAFIRAH BINTI NORAZLI KTNNo ratings yet

- Customizing ISS PIS COFINS For Classic V1 2Document19 pagesCustomizing ISS PIS COFINS For Classic V1 2renatopennaNo ratings yet

- ch03 SM Leo 10eDocument72 pagesch03 SM Leo 10ePyae PhyoNo ratings yet

- Bachelor of Business Administration (BBA) : Programme Project Report & Detailed SyllabusDocument73 pagesBachelor of Business Administration (BBA) : Programme Project Report & Detailed SyllabusSapna 03No ratings yet

- Partnership4 (1) DissolutionDocument64 pagesPartnership4 (1) DissolutionBinexNo ratings yet

Download as pdf or txt

You might also like

- D196 Study Guide Answers & NotesDocument21 pagesD196 Study Guide Answers & NotesAsril Doank100% (1)

- Cheat Sheet Exam 1Document1 pageCheat Sheet Exam 1Shashi Gavini Keil100% (2)

- The Master Budget - 1st QTRDocument41 pagesThe Master Budget - 1st QTRqueene50% (4)

- SAP Business Planning and Consolidation OverviewDocument33 pagesSAP Business Planning and Consolidation Overviewmayurnanda86100% (1)

- P2P and Assets EntriesDocument7 pagesP2P and Assets Entriessudheer1112No ratings yet

- Funds Flow Statement Tirumala MilkDocument101 pagesFunds Flow Statement Tirumala MilkSakhamuri Ram's100% (3)

- Accounting ReviewerDocument3 pagesAccounting ReviewerK ByeNo ratings yet

- Financial Management Midterm Reviewer 1Document3 pagesFinancial Management Midterm Reviewer 1Margaret Joy SobredillaNo ratings yet

- FAR Module 4Document13 pagesFAR Module 4Michael Angelo DawisNo ratings yet

- Impacting The Financial StatementsclassDocument23 pagesImpacting The Financial StatementsclassMonkey2111No ratings yet

- Financial Analysis, Depreciation and Time Value Analysis: Presented By: Najat AlbuhendiDocument33 pagesFinancial Analysis, Depreciation and Time Value Analysis: Presented By: Najat AlbuhendiNagnoaga AlNo ratings yet

- Financial Statement Analys Lecture 1stDocument16 pagesFinancial Statement Analys Lecture 1stSaeed UllahNo ratings yet

- Financial ManagementDocument50 pagesFinancial ManagementLEO FRAGGERNo ratings yet

- Basic FS - Income Statement For Service Business and Statement of Changes in Owner's EquityDocument11 pagesBasic FS - Income Statement For Service Business and Statement of Changes in Owner's Equityckbeom0No ratings yet

- Understanding Financial StatementsDocument32 pagesUnderstanding Financial StatementsAravinda RuwanNo ratings yet

- Qualifying Exam Reviewer 1Document26 pagesQualifying Exam Reviewer 1dlaronyvette100% (2)

- Report in Business Finance: Group 2 - Review of Financial Statement Preparation, Analysis, and InterpretationDocument14 pagesReport in Business Finance: Group 2 - Review of Financial Statement Preparation, Analysis, and InterpretationKOUJI N. MARQUEZNo ratings yet

- Final Accounts 1Document25 pagesFinal Accounts 1ken philipsNo ratings yet

- Chapter - 11 Financial Statement AnalysisDocument14 pagesChapter - 11 Financial Statement AnalysisAntora Hoque100% (1)

- Buss1030 Notes: 1.1 Factors Affecting The Complexity of A Changing Business EnvironmentDocument56 pagesBuss1030 Notes: 1.1 Factors Affecting The Complexity of A Changing Business EnvironmentTINo ratings yet

- Chapter 2 Analysis of Financial Statement IDocument33 pagesChapter 2 Analysis of Financial Statement ISuku Thomas SamuelNo ratings yet

- Financial Analysis GuideDocument6 pagesFinancial Analysis GuideRomelyn Joy JangaoNo ratings yet

- 01 Lecture - MT - ch01 - 0607-082023 - Acctg Concepts 01Document22 pages01 Lecture - MT - ch01 - 0607-082023 - Acctg Concepts 01JIM KYRONE GENOBISANo ratings yet

- What Is Financial Management?Document43 pagesWhat Is Financial Management?Jonas AlcantaraNo ratings yet

- ReviewerDocument3 pagesReviewerMelanie AmandoronNo ratings yet

- Self Study - Financial Accounting Chapter 1 To Chapter 4Document23 pagesSelf Study - Financial Accounting Chapter 1 To Chapter 4Ana Saggio0% (1)

- Chapter 2 Financial AnalysisDocument26 pagesChapter 2 Financial AnalysisCarl JovianNo ratings yet

- Learning Objectives: Review of Financial Statement Preparation: Analysis and InterpretationDocument4 pagesLearning Objectives: Review of Financial Statement Preparation: Analysis and InterpretationArleneNo ratings yet

- Corporate FinanceDocument51 pagesCorporate FinanceAnna FossiNo ratings yet

- Week 14 IMPLEMENT THE BUSINESS PLANDocument16 pagesWeek 14 IMPLEMENT THE BUSINESS PLANJuan Miguel SalvadorNo ratings yet

- Introduction To Financial AccountingDocument64 pagesIntroduction To Financial AccountingGurkirat Singh100% (1)

- FINANCIAL REPORTING - ScriptDocument9 pagesFINANCIAL REPORTING - ScriptMutesa ChrisNo ratings yet

- Assessment 3 Task 1 MONITOR AND CONTROLDocument3 pagesAssessment 3 Task 1 MONITOR AND CONTROLvalegiraldoNo ratings yet

- WK 1 Introduction To Accounting - CutDocument59 pagesWK 1 Introduction To Accounting - CutThùy Linh Lê ThịNo ratings yet

- Funds Flow StatementDocument101 pagesFunds Flow StatementSakhamuri Ram'sNo ratings yet

- FS ReviewerDocument11 pagesFS Reviewertiniee0510No ratings yet

- SHS Business Finance Chapter 2Document24 pagesSHS Business Finance Chapter 2Ji BaltazarNo ratings yet

- RatiosDocument6 pagesRatiosFaisal AwanNo ratings yet

- FINMAN Notes - April 14, 2021Document10 pagesFINMAN Notes - April 14, 2021Nicole Andrea TuazonNo ratings yet

- Acct1501 Notes: 1. Introduction To Financial AccountingDocument11 pagesAcct1501 Notes: 1. Introduction To Financial AccountingLena ZhengNo ratings yet

- LESSON 1 ReviewerDocument8 pagesLESSON 1 ReviewerJehan VonneNo ratings yet

- Abm FM Unit 1Document16 pagesAbm FM Unit 1Indu MazumdarNo ratings yet

- Key Steps Involved in Financial Statement AnalysisDocument2 pagesKey Steps Involved in Financial Statement AnalysisManzil ShresthaNo ratings yet

- Branches of AccountingDocument54 pagesBranches of AccountingAbby Rosales - Perez100% (1)

- V. Basic Interprestation and Use of Financial StatementsDocument12 pagesV. Basic Interprestation and Use of Financial StatementsJHERICA SURELLNo ratings yet

- Finman ReviewerDocument17 pagesFinman ReviewerSheila Mae Guerta LaceronaNo ratings yet

- ACCOUNTING-WPS OfficeDocument6 pagesACCOUNTING-WPS OfficeNorjehanie AliNo ratings yet

- 03 04 Analysis Financial StatementDocument216 pages03 04 Analysis Financial StatementShanique Y. Harnett100% (1)

- Do 1221Document27 pagesDo 1221muluabebaw287No ratings yet

- Lec 2Document38 pagesLec 2Mohamed AliNo ratings yet

- Financial StatementsDocument31 pagesFinancial StatementsJeahMaureenDominguez100% (2)

- Analysis of Financial StatementDocument9 pagesAnalysis of Financial Statementmorcoangelicafaith8No ratings yet

- Answer 1.: Straight Line DepreciationDocument11 pagesAnswer 1.: Straight Line DepreciationDanish ShaikhNo ratings yet

- Int I Midterm ReviewDocument7 pagesInt I Midterm ReviewshevinakNo ratings yet

- Assessing A New Venture's Financial Strength and ViabilityDocument6 pagesAssessing A New Venture's Financial Strength and ViabilityAsif KureishiNo ratings yet

- 1Document34 pages1TOLENTINO, Julius Mark VirayNo ratings yet

- Information Sheet - BKKPG-8 - Preparing Financial StatementsDocument10 pagesInformation Sheet - BKKPG-8 - Preparing Financial StatementsEron Roi Centina-gacutanNo ratings yet

- Section 1: Introduction To Principles of AccountsDocument6 pagesSection 1: Introduction To Principles of AccountsArcherAcsNo ratings yet

- Accounting and Financial StatementsDocument14 pagesAccounting and Financial StatementsMitha LarasNo ratings yet

- FAC1502 Accounting Study Guide QuestionsDocument34 pagesFAC1502 Accounting Study Guide QuestionszinesunduzaNo ratings yet

- The Entrepreneur’S Dictionary of Business and Financial TermsFrom EverandThe Entrepreneur’S Dictionary of Business and Financial TermsNo ratings yet

- Inventories and Cost of SalesDocument18 pagesInventories and Cost of SalesAmor HalitimNo ratings yet

- Financial StatementsDocument23 pagesFinancial StatementsShin Shan JeonNo ratings yet

- MGMT 30A: Practice FinalDocument18 pagesMGMT 30A: Practice FinalFUSION AcademicsNo ratings yet

- Earnings Release: 9 Months - 2009Document34 pagesEarnings Release: 9 Months - 2009DGC_thenationalNo ratings yet

- Admission and Retirement Long QuestionDocument11 pagesAdmission and Retirement Long QuestionMenu GargNo ratings yet

- Soal Soal AklanDocument30 pagesSoal Soal AklanFikri Sya'bana100% (1)

- Term Paper On Capital Budgeting TechniquesDocument5 pagesTerm Paper On Capital Budgeting Techniquesc5pcnpd6100% (1)

- Bfe 425 Assignment 3 2023Document3 pagesBfe 425 Assignment 3 2023Chikarakara LloydNo ratings yet

- Profit PlanningDocument43 pagesProfit PlanningLouiseNo ratings yet

- Dividend Discount AND Dividend Growth Model: BY Raman Surajit Rajesh PriyankaDocument14 pagesDividend Discount AND Dividend Growth Model: BY Raman Surajit Rajesh Priyankapriyanka2538No ratings yet

- Final Exam - Fall 2023Document5 pagesFinal Exam - Fall 2023hani.sharma324No ratings yet

- ACC 203 Ch08 SolutionsDocument7 pagesACC 203 Ch08 Solutionsomaritani2005No ratings yet

- Sole Trader: Final Accounts - The Income StatementDocument12 pagesSole Trader: Final Accounts - The Income StatementAnisahNo ratings yet

- Cost of CapitalDocument41 pagesCost of CapitalMCDABCNo ratings yet

- New Chapter 17 - Cash FlowDocument17 pagesNew Chapter 17 - Cash FlowCheyenne Dawhitegurl GuillNo ratings yet

- Format of Financial StatementsDocument2 pagesFormat of Financial StatementsAmeerul HarithNo ratings yet

- ACCA102 - 13 Noncurrent Asset Held For SaleDocument20 pagesACCA102 - 13 Noncurrent Asset Held For SaleMary Kate OrobiaNo ratings yet

- BDP Financial Final PartDocument14 pagesBDP Financial Final PartDeepak G.C.No ratings yet

- Group 1 Section A PDFDocument14 pagesGroup 1 Section A PDFNayeem Md Sakib100% (1)

- CFAS - Midterm Exam Set ADocument7 pagesCFAS - Midterm Exam Set ADesiree Angelique RebonquinNo ratings yet

- LECTURE 7 - Chapter 10 Auditing The Revenue ProcessDocument35 pagesLECTURE 7 - Chapter 10 Auditing The Revenue ProcessamyNo ratings yet

- Cima p4Document3 pagesCima p4fawad aslamNo ratings yet

- Chapter 5 Incomplete RecordDocument20 pagesChapter 5 Incomplete RecordNUR ADLIN ZAFIRAH BINTI NORAZLI KTNNo ratings yet

- Customizing ISS PIS COFINS For Classic V1 2Document19 pagesCustomizing ISS PIS COFINS For Classic V1 2renatopennaNo ratings yet

- ch03 SM Leo 10eDocument72 pagesch03 SM Leo 10ePyae PhyoNo ratings yet

- Bachelor of Business Administration (BBA) : Programme Project Report & Detailed SyllabusDocument73 pagesBachelor of Business Administration (BBA) : Programme Project Report & Detailed SyllabusSapna 03No ratings yet

- Partnership4 (1) DissolutionDocument64 pagesPartnership4 (1) DissolutionBinexNo ratings yet