Download as docx, pdf, or txt

You might also like

- Gas Billing Format For ClientDocument2 pagesGas Billing Format For ClientRyan Williams100% (2)

- Valuation Apr 05Document10 pagesValuation Apr 05justine reine cornicoNo ratings yet

- FinDocument4 pagesFinTintin Brusola Salen67% (3)

- Invoice - 2019-12-24T121855.363Document2 pagesInvoice - 2019-12-24T121855.363garima kathuriaNo ratings yet

- 10 Overseas Bank Vs CA & Tapia PDFDocument10 pages10 Overseas Bank Vs CA & Tapia PDFNicoleAngeliqueNo ratings yet

- BPI Vs FMIC PDFDocument3 pagesBPI Vs FMIC PDFMark John Geronimo BautistaNo ratings yet

- Abacus v. Manila BankingDocument3 pagesAbacus v. Manila BankingSean GalvezNo ratings yet

- 1-Cruz Vs Judge AreolaDocument1 page1-Cruz Vs Judge AreolaJeselle Ann VegaNo ratings yet

- Paris Manila Vs Phoenix Assurance G.R. No. L-25845 December 17, 1926Document1 pageParis Manila Vs Phoenix Assurance G.R. No. L-25845 December 17, 1926Emrico CabahugNo ratings yet

- NIDC v. CADocument2 pagesNIDC v. CAluisjfg21No ratings yet

- Sta. Maria vs. Hongkong and Shanghai, 89 PHIL 780Document4 pagesSta. Maria vs. Hongkong and Shanghai, 89 PHIL 780VINCENTREY BERNARDONo ratings yet

- Cruz v. Areola DG 23Document3 pagesCruz v. Areola DG 23Mark Angelo CabilloNo ratings yet

- Aznar vs. CitibankDocument12 pagesAznar vs. CitibankKenneth RafolsNo ratings yet

- Bar Examination 2013Document13 pagesBar Examination 2013Heber BacolodNo ratings yet

- 39 Carpo v. ChuaDocument2 pages39 Carpo v. ChuaAngelette BulacanNo ratings yet

- Bog & Co. v. Hanover Fire InsuranceDocument5 pagesBog & Co. v. Hanover Fire InsuranceKristineSherikaChyNo ratings yet

- 77-Government Service Insurance System vs. Court of Appeals, 308 SCRA 559, 21 June 1999Document8 pages77-Government Service Insurance System vs. Court of Appeals, 308 SCRA 559, 21 June 1999Jopan SJNo ratings yet

- Blue Cross Health Care, Inc. V Neomi and Danilo Olivares: FactsDocument3 pagesBlue Cross Health Care, Inc. V Neomi and Danilo Olivares: FactsGenesis LealNo ratings yet

- Petitioner vs. vs. Respondents: en BancDocument6 pagesPetitioner vs. vs. Respondents: en BancJessica Magsaysay CrisostomoNo ratings yet

- Professional Services Inc. vs. AganaDocument3 pagesProfessional Services Inc. vs. AganaAkeem AmistadNo ratings yet

- Republic Vs ST Vincent de Paul DigestDocument3 pagesRepublic Vs ST Vincent de Paul DigestJan Rhoneil SantillanaNo ratings yet

- Union Bank V Court of Appeals G.R. No. 134068. June 25, 2001Document1 pageUnion Bank V Court of Appeals G.R. No. 134068. June 25, 2001Anonymous Xhp28mToJNo ratings yet

- Sanidad v. Comelec, 181 Scra 529 (1990)Document6 pagesSanidad v. Comelec, 181 Scra 529 (1990)ag832bNo ratings yet

- Martires V ChuaDocument11 pagesMartires V Chuajade123_129No ratings yet

- Ietts Vs CA DigestDocument2 pagesIetts Vs CA DigestoabeljeanmoniqueNo ratings yet

- Civil Procedure Batch 2Document51 pagesCivil Procedure Batch 2Nicole Ziza100% (1)

- 74-Perla Compania de Seguro, Inc. vs. Hon. Constante Ancheta, 164 SCRA 144Document3 pages74-Perla Compania de Seguro, Inc. vs. Hon. Constante Ancheta, 164 SCRA 144Jopan SJNo ratings yet

- Banco Filipino Savings and Mortgage Bank vs. Central Bank G.R. No. 70054, December 11, 1991Document14 pagesBanco Filipino Savings and Mortgage Bank vs. Central Bank G.R. No. 70054, December 11, 1991Ronald LasinNo ratings yet

- 2015 - Sia v. Arcenas PDFDocument7 pages2015 - Sia v. Arcenas PDFDerick TorresNo ratings yet

- Garcia vs. Velasco, 72 Phil 248 (Case Digest)Document1 pageGarcia vs. Velasco, 72 Phil 248 (Case Digest)AycNo ratings yet

- Ridgewood Estate Vs BelaosDocument2 pagesRidgewood Estate Vs BelaosJanil Jay S. EquizaNo ratings yet

- GENERAL CREDIT CORP v. ALDEVINCODocument2 pagesGENERAL CREDIT CORP v. ALDEVINCOJued CisnerosNo ratings yet

- Agra Gsis CasesDocument15 pagesAgra Gsis CasesCarla VirtucioNo ratings yet

- Credit Transactions Case DigestsDocument4 pagesCredit Transactions Case DigestsKMNo ratings yet

- Berman Memorial Park Vs Cheng (GR No. 154630. May 6, 2005)Document2 pagesBerman Memorial Park Vs Cheng (GR No. 154630. May 6, 2005)Theresa Faye De GuzmanNo ratings yet

- 37-Casumpang vs. CortejoDocument79 pages37-Casumpang vs. CortejoFatzie MendozaNo ratings yet

- Benjamin P. Gomez vs. Enrico PalomarDocument3 pagesBenjamin P. Gomez vs. Enrico PalomarChaDiazNo ratings yet

- GR 195580Document2 pagesGR 195580Marifel Lagare100% (1)

- Peoples Bank and Trust Company vs. Tambunting, G.R. No. L-2966, 29oct1971Document1 pagePeoples Bank and Trust Company vs. Tambunting, G.R. No. L-2966, 29oct1971Evangelyn Egusquiza100% (1)

- Caltex vs. Palomar DigestDocument3 pagesCaltex vs. Palomar DigestAdrian Gabriel S. AtienzaNo ratings yet

- Caltex (Philippines) Vs CA 212 SCRA 448 August 10, 1992 FactsDocument3 pagesCaltex (Philippines) Vs CA 212 SCRA 448 August 10, 1992 FactsHal JordanNo ratings yet

- ARCELLANA - Alcantara V Reta (2017)Document1 pageARCELLANA - Alcantara V Reta (2017)huhah303No ratings yet

- Case 28 Laborte Et Al. vs. Pagsanjan Tourism Consumers' Corp Et Al (Jan 2014)Document2 pagesCase 28 Laborte Et Al. vs. Pagsanjan Tourism Consumers' Corp Et Al (Jan 2014)Frances Abigail BubanNo ratings yet

- Corpo Digest FinalsDocument15 pagesCorpo Digest Finalskaren mariz manaNo ratings yet

- Robinson & Co. v. Belt, 187 U.S. 41 (1902)Document8 pagesRobinson & Co. v. Belt, 187 U.S. 41 (1902)Scribd Government DocsNo ratings yet

- Mendoza Vs COADocument1 pageMendoza Vs COAHudson CeeNo ratings yet

- Filipinas Compania de Seguros vs. Nava, G.R. No. L-19638, June 20, 1966 17 SCRA 216Document5 pagesFilipinas Compania de Seguros vs. Nava, G.R. No. L-19638, June 20, 1966 17 SCRA 216Rochelle Othin Odsinada MarquesesNo ratings yet

- VIVAS Vs THE MONETARY BOARDDocument4 pagesVIVAS Vs THE MONETARY BOARDIan Joshua RomasantaNo ratings yet

- Effects of The Contract When The Thing Sold Has Been Lost 1. Loss (1493-1494)Document3 pagesEffects of The Contract When The Thing Sold Has Been Lost 1. Loss (1493-1494)ChaNo ratings yet

- Module 3 Admin LawDocument16 pagesModule 3 Admin LawMau AntallanNo ratings yet

- Political Law Digest - 11 SepDocument28 pagesPolitical Law Digest - 11 SepJean Mary AutoNo ratings yet

- Corpo Code CasesDocument14 pagesCorpo Code Casessabrina gayoNo ratings yet

- Ralla v. RallaDocument2 pagesRalla v. RallaGlenz LagunaNo ratings yet

- DOLE DO No. 10, S. 1998Document3 pagesDOLE DO No. 10, S. 1998lemwel_jl288636No ratings yet

- THE INSULAR LIFE ASSURANCE COMPANY, LTD. vs. CARPONIA T. EBRADO and PASCUALA VDA. DE EBRADODocument2 pagesTHE INSULAR LIFE ASSURANCE COMPANY, LTD. vs. CARPONIA T. EBRADO and PASCUALA VDA. DE EBRADOReynaldo DizonNo ratings yet

- Cases On Writs of Habeas Corpus, Data, Amparo, EtcDocument5 pagesCases On Writs of Habeas Corpus, Data, Amparo, EtcJP DCNo ratings yet

- Definition of The Term Capital To Satisfy The Nationality Requirement Under Sec. 11, Art. XIIDocument9 pagesDefinition of The Term Capital To Satisfy The Nationality Requirement Under Sec. 11, Art. XIIMiko TabandaNo ratings yet

- People vs. de LunaDocument2 pagesPeople vs. de LunaAnonymous 6Xc2R53xNo ratings yet

- The Overseas Bank of Manila VsDocument2 pagesThe Overseas Bank of Manila VsVance CeballosNo ratings yet

- Integrated Realty Corporation vs. Philippine National BankDocument2 pagesIntegrated Realty Corporation vs. Philippine National BankSernande Pen100% (1)

- 9 Preventive and Precautionary Principles RevisedDocument2 pages9 Preventive and Precautionary Principles RevisedGraceNo ratings yet

- 9 Ramos Vs Central BankDocument3 pages9 Ramos Vs Central BankTelle MarieNo ratings yet

- Overseas Bank of Manila Vs CorderoDocument4 pagesOverseas Bank of Manila Vs CorderoReghEllorimoNo ratings yet

- Consolidated Bank vs. Court of AppealsDocument6 pagesConsolidated Bank vs. Court of AppealsMark TeaNo ratings yet

- People Vs LimacoDocument6 pagesPeople Vs LimacoClaudia LapazNo ratings yet

- Simex International (Manila), Inc. vs. Court of AppealsDocument6 pagesSimex International (Manila), Inc. vs. Court of AppealsClaudia LapazNo ratings yet

- People vs. Bago, 330 SCRA 115, G.R. No. 122290 April 6, 2000Document16 pagesPeople vs. Bago, 330 SCRA 115, G.R. No. 122290 April 6, 2000Claudia LapazNo ratings yet

- Heirs of Eduardo Manlapat vs. Court of AppealsDocument12 pagesHeirs of Eduardo Manlapat vs. Court of AppealsClaudia LapazNo ratings yet

- Samsung Construction Company Philippines, Inc. vs. Far East Bank and Trust CompanyDocument21 pagesSamsung Construction Company Philippines, Inc. vs. Far East Bank and Trust CompanyClaudia LapazNo ratings yet

- Philippine Banking Corporation vs. Court of Appeals and Marcos.Document16 pagesPhilippine Banking Corporation vs. Court of Appeals and Marcos.Claudia LapazNo ratings yet

- Metropolitan Bank and Trust Company vs. ChiokDocument33 pagesMetropolitan Bank and Trust Company vs. ChiokClaudia LapazNo ratings yet

- Philippine National Bank v. PikeDocument13 pagesPhilippine National Bank v. PikeClaudia LapazNo ratings yet

- Philippine Banking Corporation vs. Court of Appeals and MarcosDocument16 pagesPhilippine Banking Corporation vs. Court of Appeals and MarcosClaudia LapazNo ratings yet

- Dinoy vs. RosalDocument3 pagesDinoy vs. RosalClaudia LapazNo ratings yet

- SPEC PRO 259. Civil Service Commission v. Rasuman, GR No. 239011, June 17, 2019Document8 pagesSPEC PRO 259. Civil Service Commission v. Rasuman, GR No. 239011, June 17, 2019Claudia LapazNo ratings yet

- SPEC PRO 258. Tan v. Office of The Local Civil Registrar of Manila and The PSA, GR No. 211435, April 10, 2019Document11 pagesSPEC PRO 258. Tan v. Office of The Local Civil Registrar of Manila and The PSA, GR No. 211435, April 10, 2019Claudia LapazNo ratings yet

- SPEC PRO 255. Republic v. Cantor, GR No. 184621, December 10, 2013Document15 pagesSPEC PRO 255. Republic v. Cantor, GR No. 184621, December 10, 2013Claudia LapazNo ratings yet

- SPEC PRO 254. Tadeo-Matias v. Republic, GR No. 230751, April 25, 2018Document9 pagesSPEC PRO 254. Tadeo-Matias v. Republic, GR No. 230751, April 25, 2018Claudia LapazNo ratings yet

- SPEC PRO 257. Fox v. Philippine Statistics Authority and The Office of The Solicitor General, GR No. 233520, March 6, 2019Document5 pagesSPEC PRO 257. Fox v. Philippine Statistics Authority and The Office of The Solicitor General, GR No. 233520, March 6, 2019Claudia LapazNo ratings yet

- SPEC PRO 256. Republic v. CA, GR No. 163604, May 6, 2005Document6 pagesSPEC PRO 256. Republic v. CA, GR No. 163604, May 6, 2005Claudia LapazNo ratings yet

- SPEC PRO 56. in The Matter of The Intestate Estate of Reynaldo Rodriguez, Anita Ong Tan v. Rodriguez, GR No. 230404, January 31, 2018Document10 pagesSPEC PRO 56. in The Matter of The Intestate Estate of Reynaldo Rodriguez, Anita Ong Tan v. Rodriguez, GR No. 230404, January 31, 2018Claudia LapazNo ratings yet

- SPEC PRO 253. Republic v. Tampus, GR No. 214243, March 16, 2016Document6 pagesSPEC PRO 253. Republic v. Tampus, GR No. 214243, March 16, 2016Claudia LapazNo ratings yet

- SPEC PRO 43. Ermac vs. Medelo, 64 SCRA 358, No. L-32281 June 19, 1975Document2 pagesSPEC PRO 43. Ermac vs. Medelo, 64 SCRA 358, No. L-32281 June 19, 1975Claudia LapazNo ratings yet

- SPEC PRO 55. Mayor vs. Tiu, 810 SCRA 256, G.R. No. 203770 November 23, 2016Document23 pagesSPEC PRO 55. Mayor vs. Tiu, 810 SCRA 256, G.R. No. 203770 November 23, 2016Claudia LapazNo ratings yet

- SPEC PRO 57. Pacioles, Jr. vs. Chuatoco-Ching, 466 SCRA 90, G.R. No. 127920 August 9, 2005Document16 pagesSPEC PRO 57. Pacioles, Jr. vs. Chuatoco-Ching, 466 SCRA 90, G.R. No. 127920 August 9, 2005Claudia LapazNo ratings yet

- SPEC PRO 39. Utulo vs. Pasion Viuda de Garcia, 66 Phil. 302, No. 45904 September 30, 1938Document4 pagesSPEC PRO 39. Utulo vs. Pasion Viuda de Garcia, 66 Phil. 302, No. 45904 September 30, 1938Claudia LapazNo ratings yet

- File 5e9dad3275db4Document3 pagesFile 5e9dad3275db4Saravana skNo ratings yet

- MATH - 2280 - Assignment 4Document1 pageMATH - 2280 - Assignment 4Bludimir ClawgsburgNo ratings yet

- Lone Pine Cafe SolutionDocument5 pagesLone Pine Cafe SolutionRitu ChhipaNo ratings yet

- Bir Ruling Da 427 06Document5 pagesBir Ruling Da 427 06JM Dela PazNo ratings yet

- Objection Letter - 9Document4 pagesObjection Letter - 9stockboardguyNo ratings yet

- Economy English 500 Important Questions & AnswersDocument49 pagesEconomy English 500 Important Questions & AnswersvenkannaNo ratings yet

- .Recovery Management in Jaipur Central Cooperative BankDocument6 pages.Recovery Management in Jaipur Central Cooperative BanknithyaNo ratings yet

- Answer KeyDocument4 pagesAnswer KeyParth BhatiaNo ratings yet

- Oracle R12 Payments White PaperDocument11 pagesOracle R12 Payments White PaperjayapavanNo ratings yet

- Credit Management and Debt Collection StrategiesDocument5 pagesCredit Management and Debt Collection StrategiesRohanNo ratings yet

- Sourses of FinanceDocument9 pagesSourses of FinanceN Durga MBANo ratings yet

- Effects of Changes in Foreign Exchange RatesDocument8 pagesEffects of Changes in Foreign Exchange RatesJaemina ParallagNo ratings yet

- Notes For Bank AccountsDocument18 pagesNotes For Bank Accountscs LakshmiNo ratings yet

- SFM - Important Questions Nov 22 - May 23Document14 pagesSFM - Important Questions Nov 22 - May 23SrihariNo ratings yet

- Resume Li Cui JhuDocument1 pageResume Li Cui Jhuapi-340127718No ratings yet

- Chapter 22 Current LiabilitiesDocument17 pagesChapter 22 Current Liabilitiesnoryn40% (5)

- Equity Research and Valuation B Kemp Dolliver-0935015213Document69 pagesEquity Research and Valuation B Kemp Dolliver-0935015213rockkey76No ratings yet

- Definition of LoanDocument8 pagesDefinition of LoanShah Alam Palash0% (1)

- My Courses AMCAT Quantitative Ability Cram Up SI & CI PreviewDocument4 pagesMy Courses AMCAT Quantitative Ability Cram Up SI & CI PreviewInsignia D.No ratings yet

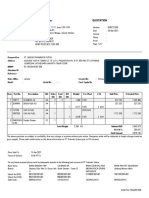

- Qout - 8300727209 - PT - BasukiDocument2 pagesQout - 8300727209 - PT - BasukiDeden PramikaNo ratings yet

- Measuring National Output and National Income: Fernando & Yvonn QuijanoDocument36 pagesMeasuring National Output and National Income: Fernando & Yvonn QuijanoYunita AngelicaNo ratings yet

- Construction Economics and Finance - Cash Flow ManagementDocument50 pagesConstruction Economics and Finance - Cash Flow ManagementMilashuNo ratings yet

- MyGlamm Invoice 1662877168-20Document1 pageMyGlamm Invoice 1662877168-20Movies AddaNo ratings yet

- Financial Statement Analysis Tools and TechniquesDocument25 pagesFinancial Statement Analysis Tools and TechniquesmNo ratings yet

- Indian Financial SystemDocument6 pagesIndian Financial SystemManmeet Kaur100% (1)

- Loan Type Definition 2018Document1 pageLoan Type Definition 2018Johayr TasilNo ratings yet