Download as pdf or txt

You might also like

- Mortgage Dispute LetterDocument14 pagesMortgage Dispute Letterhalcino100% (11)

- Mba PDFDocument93 pagesMba PDFRenjumul MofidNo ratings yet

- Comperative Analysis of Products and Services of Axis Bank and Its Compatiter RajneeshDocument96 pagesComperative Analysis of Products and Services of Axis Bank and Its Compatiter RajneeshRanjeet singhNo ratings yet

- The Impact of Corporate SocialDocument41 pagesThe Impact of Corporate SocialCraft Joy100% (1)

- Pidsdps 2034Document80 pagesPidsdps 2034Glaydel Mae JavillonarNo ratings yet

- Dave Final PropsalDocument21 pagesDave Final PropsalDeavoNo ratings yet

- HRM 611 Reserch Paper On Dhaka Bank Ltd. Tarif Rahman 19264045Document25 pagesHRM 611 Reserch Paper On Dhaka Bank Ltd. Tarif Rahman 19264045darkmail6969No ratings yet

- Comprehensive Study On Credit Programs To SmallholdersDocument67 pagesComprehensive Study On Credit Programs To SmallholdersKeb CuevasNo ratings yet

- India Stressed Assets - Alvarez & MarsalDocument32 pagesIndia Stressed Assets - Alvarez & MarsalheenaieibsNo ratings yet

- Determinants of Dividend Payout RatioDocument16 pagesDeterminants of Dividend Payout RatioSabin Subedi100% (1)

- Financial Statement Analysis of Habib BankDocument51 pagesFinancial Statement Analysis of Habib BankrashidwarsiNo ratings yet

- 22 Rollercoaster of Indian NPAs PR RMDocument51 pages22 Rollercoaster of Indian NPAs PR RMDEVESH SINGHNo ratings yet

- CSR Practices in Developing Countries.Document44 pagesCSR Practices in Developing Countries.Nithin OmanakuttanNo ratings yet

- Assessment On The Management of Financial Resources of The Baguio Market Vendors Multi-Purpose CooperativeDocument34 pagesAssessment On The Management of Financial Resources of The Baguio Market Vendors Multi-Purpose CooperativeSarah WilliamsNo ratings yet

- Ffective Trategies: For Community Development FinanceDocument103 pagesFfective Trategies: For Community Development FinanceJohn CarneyNo ratings yet

- Eshetiemekoneneresearchpaper 201114075135Document43 pagesEshetiemekoneneresearchpaper 201114075135Eshetie Mekonene AmareNo ratings yet

- The Impact of Credit Policy On Improving Vietnamese Household Living Standards in The Time of Covid 19 Pandemic - 20230228 - 020555Document49 pagesThe Impact of Credit Policy On Improving Vietnamese Household Living Standards in The Time of Covid 19 Pandemic - 20230228 - 020555Phương ThảoNo ratings yet

- Care Bangladesh Research Proposal FinalDocument24 pagesCare Bangladesh Research Proposal FinalMuhibur Rahman AbirNo ratings yet

- MRP On NpaDocument65 pagesMRP On Npaanindya_kundu100% (2)

- Research Proposal - Determinants of Local Islamic Bank's Profitability in Malaysia 1Document44 pagesResearch Proposal - Determinants of Local Islamic Bank's Profitability in Malaysia 1Khairi Izuan100% (1)

- Use of Credit Evaluation Procedures at Agricultural Banks in Minnesota 1991 Survey Results 1991 40p SKDocument40 pagesUse of Credit Evaluation Procedures at Agricultural Banks in Minnesota 1991 Survey Results 1991 40p SKdainesecowboyNo ratings yet

- Revisiting The Debt Sustainability Framework For Low-Income CountriesDocument70 pagesRevisiting The Debt Sustainability Framework For Low-Income CountriesJustin TalbotNo ratings yet

- MGT201 BRAC Bank ReportDocument30 pagesMGT201 BRAC Bank Report2221979No ratings yet

- MOSES KINYANJUI EMPIRICAL FINANCE SEMINAR PAPER RevisedDocument24 pagesMOSES KINYANJUI EMPIRICAL FINANCE SEMINAR PAPER RevisedMIRADOR ACCOUNTANTS KENYANo ratings yet

- YESBank ReportDocument26 pagesYESBank ReportPreeti MishraNo ratings yet

- Studerande 215410 GRINICK - MICHAEL - SEMI2 - 237904 - 1758636731Document35 pagesStuderande 215410 GRINICK - MICHAEL - SEMI2 - 237904 - 1758636731abaasNo ratings yet

- Loan Management of Agriculture Development BankDocument36 pagesLoan Management of Agriculture Development BankanisheshkNo ratings yet

- Mekelle UniversityDocument46 pagesMekelle UniversityMelese LegamoNo ratings yet

- WVK Guidelines For Working With CBOsDocument64 pagesWVK Guidelines For Working With CBOscherogonyaNo ratings yet

- CDFIs Stepping Into The Breach - An Impact Evaluation - Summary RepoDocument58 pagesCDFIs Stepping Into The Breach - An Impact Evaluation - Summary RepoAdam SaferNo ratings yet

- ABdiDocument27 pagesABdiferewe tesfayeNo ratings yet

- 2016 - Nr.3 - Potential For Cost Reducing and Efficiency - ENDocument65 pages2016 - Nr.3 - Potential For Cost Reducing and Efficiency - ENUnanimous ClientNo ratings yet

- Sip Report On Punjab National BankDocument75 pagesSip Report On Punjab National BankIshaan YadavNo ratings yet

- Adbi wp581Document24 pagesAdbi wp581خاور عباسیNo ratings yet

- Identification and Analysis of Causative Factors Driving The Failure of Cooperative Society Banks in KarnatakaDocument60 pagesIdentification and Analysis of Causative Factors Driving The Failure of Cooperative Society Banks in KarnatakaTilak Raj100% (3)

- Diagnositic SurveyReport Women SMEsDocument141 pagesDiagnositic SurveyReport Women SMEsAyza FatimaNo ratings yet

- Asian Development Bank Institute: ADBI Working Paper SeriesDocument16 pagesAsian Development Bank Institute: ADBI Working Paper SeriesMoona AfreenNo ratings yet

- StrategicExternalEnvironmentalAnalysis CommercialBankPLCSriLankaDocument19 pagesStrategicExternalEnvironmentalAnalysis CommercialBankPLCSriLankaArif HasanNo ratings yet

- Banking Paper Very NewDocument23 pagesBanking Paper Very NewTanishq MishraNo ratings yet

- Accunting ResarchDocument45 pagesAccunting ResarchMubarakNo ratings yet

- Merger of Public Sector Banks Details of The LearnerDocument23 pagesMerger of Public Sector Banks Details of The LearnerUnnatiNo ratings yet

- The Strategic Implications of Corporate Responsibility and Sustainability in The UK Banking SectorDocument87 pagesThe Strategic Implications of Corporate Responsibility and Sustainability in The UK Banking SectorSaniya KhanNo ratings yet

- Leah's ProjectDocument44 pagesLeah's ProjectLucy Muthoni machariaNo ratings yet

- 3.changing Landscape in Banking SectorDocument27 pages3.changing Landscape in Banking Sectorcrazysucessap44448No ratings yet

- PSM Approach PDFDocument25 pagesPSM Approach PDFAtty Jeanne SarmientoNo ratings yet

- Iip ProjectDocument64 pagesIip ProjectSukumar ReddyNo ratings yet

- An Examination of The Credit Management Practices of Rural Banks: A Case Study of Asokore Rural Bank LimitedDocument37 pagesAn Examination of The Credit Management Practices of Rural Banks: A Case Study of Asokore Rural Bank LimitedKumar KnNo ratings yet

- Full Text 01Document48 pagesFull Text 01pmthogoNo ratings yet

- Governance Institutional Risks Challenges Nepal ASIAN DEVELOPMENT BANKDocument130 pagesGovernance Institutional Risks Challenges Nepal ASIAN DEVELOPMENT BANKRanjan KCNo ratings yet

- Berhan Debero First DraftDocument41 pagesBerhan Debero First DraftMwalimu Hachalu FayeNo ratings yet

- West Bank Gaza Financial Literacy Survey PDFDocument60 pagesWest Bank Gaza Financial Literacy Survey PDFDavit EvoyanNo ratings yet

- SFBLDocument22 pagesSFBLafrana Priety0% (1)

- Spoorthi BennurDocument58 pagesSpoorthi BennurSarva ShivaNo ratings yet

- WP 2018 001 PDFDocument29 pagesWP 2018 001 PDFsarikachandaliyaNo ratings yet

- Industry Analysis Banking Day 10 TaskDocument21 pagesIndustry Analysis Banking Day 10 TaskKatta AshishNo ratings yet

- Nasir Abdela SaidDocument46 pagesNasir Abdela SaidBobasa S AhmedNo ratings yet

- LIDIYA Final PAPERDocument56 pagesLIDIYA Final PAPERrobelNo ratings yet

- Tiglu Hyle PaperDocument47 pagesTiglu Hyle Paperkassahun meseleNo ratings yet

- Global Financial Development Report 2015/2016: Long-Term FinanceFrom EverandGlobal Financial Development Report 2015/2016: Long-Term FinanceNo ratings yet

- Global Financial Development Report 2019/2020: Bank Regulation and Supervision a Decade after the Global Financial CrisisFrom EverandGlobal Financial Development Report 2019/2020: Bank Regulation and Supervision a Decade after the Global Financial CrisisRating: 5 out of 5 stars5/5 (2)

- Financial Management 1.2Document8 pagesFinancial Management 1.2Sashwat AgarwalNo ratings yet

- Unit 6: Rectification of Errors: Learning OutcomesDocument32 pagesUnit 6: Rectification of Errors: Learning OutcomesKhushi MehtaNo ratings yet

- Business Finance Reviewer 1Document12 pagesBusiness Finance Reviewer 1John Delf GabrielNo ratings yet

- Right of The Mortgagee To Recover DeficiencyDocument4 pagesRight of The Mortgagee To Recover Deficiencyesmeralda de guzmanNo ratings yet

- DLL General-Mathematics Q2 W5Document13 pagesDLL General-Mathematics Q2 W5Princess DeramasNo ratings yet

- Ch12 - Restructuring in BankruptcyDocument41 pagesCh12 - Restructuring in BankruptcyVY NGUYỄN HUYỀN100% (1)

- Pas 1, Pas 2, Pas 7Document29 pagesPas 1, Pas 2, Pas 7MPCINo ratings yet

- Company AccountsDocument24 pagesCompany Accountsdeo omachNo ratings yet

- Banking Law NotesDocument50 pagesBanking Law NotesSYAMALA YASHWANTH REDDYNo ratings yet

- Provision of Automatic Fire Detection and Alarm System at 70 Stations of KIR Division N F RailwayDocument44 pagesProvision of Automatic Fire Detection and Alarm System at 70 Stations of KIR Division N F RailwayJohnJamallamudiNo ratings yet

- Tugas Ifrs Chapter 7Document11 pagesTugas Ifrs Chapter 7Nabilla salsaNo ratings yet

- Counter GuaranteeDocument2 pagesCounter Guaranteesunil kumarNo ratings yet

- Bullet Revisions Chapter 6Document28 pagesBullet Revisions Chapter 6mrkabir1600No ratings yet

- Bank GuaranteeDocument10 pagesBank GuaranteesaidrajanNo ratings yet

- Ae18-004-The Philippine Financial SystemDocument30 pagesAe18-004-The Philippine Financial SystemLaezelie PalajeNo ratings yet

- 61a6cbec682c8 - Book Keeping and AccountingDocument16 pages61a6cbec682c8 - Book Keeping and AccountingAnuska ThapaNo ratings yet

- Resume Prospectus BCP EOS 2020 VAngDocument30 pagesResume Prospectus BCP EOS 2020 VAngIsmail bnjNo ratings yet

- Trial QuestionsDocument14 pagesTrial QuestionsRichmond Kofi AgyareNo ratings yet

- The Accounting Equation & Double EntryDocument13 pagesThe Accounting Equation & Double EntryJukunda Shikongo100% (1)

- Answers To Problem Sets: How Much Should A Corporation Borrow?Document8 pagesAnswers To Problem Sets: How Much Should A Corporation Borrow?priyanka GayathriNo ratings yet

- Ns 01 2013 PDFDocument136 pagesNs 01 2013 PDFchunochunoNo ratings yet

- Deed of English Mortgage in Favor of A Bank: FactsDocument6 pagesDeed of English Mortgage in Favor of A Bank: FactsKUSHAGRA AMRITNo ratings yet

- Loan Restructuring App FormDocument3 pagesLoan Restructuring App FormLilibeth Allosada LapathaNo ratings yet

- CMA Volume 2 MergedDocument153 pagesCMA Volume 2 MergedShyaambhavi NsNo ratings yet

- CH 08Document46 pagesCH 08NuryaniNo ratings yet

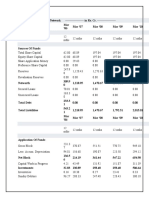

- Balance Sheet of Sun TV NetworkDocument2 pagesBalance Sheet of Sun TV NetworkMehadi NawazNo ratings yet

- 翻查Document40 pages翻查bomif45831No ratings yet

- The Brazilian EconomyDocument37 pagesThe Brazilian Economyرامي أبو الفتوحNo ratings yet

- Unit 6Document6 pagesUnit 6Tiếng Anh 7No ratings yet