Download as doc, pdf, or txt

You might also like

- Confirmation of Enrolment: Customer Number For Work Provider UseDocument1 pageConfirmation of Enrolment: Customer Number For Work Provider Useallan endoNo ratings yet

- Question Paper - Fundamentals of Insurance 2021 - Question & AnswersDocument14 pagesQuestion Paper - Fundamentals of Insurance 2021 - Question & Answersjeganrajraj100% (4)

- Tushar Varshney SIP ReportDocument47 pagesTushar Varshney SIP ReportTushar VarshneyNo ratings yet

- Bachelor of Commerce: Submitted For The Partial Fulfillment of The Requirement For The Award of The Degree ofDocument75 pagesBachelor of Commerce: Submitted For The Partial Fulfillment of The Requirement For The Award of The Degree ofmr copy xeroxNo ratings yet

- Anamika PDFDocument29 pagesAnamika PDFAdarsh VermaNo ratings yet

- Performance Analysis of Mutual Funds - 220923 - 153628Document73 pagesPerformance Analysis of Mutual Funds - 220923 - 153628KshitishNo ratings yet

- Project Marketing Spe. Sem - 6Document50 pagesProject Marketing Spe. Sem - 6Parikshit Ashok ManeNo ratings yet

- PortfolioDocument64 pagesPortfolioPratik GuravNo ratings yet

- Universal Banking HDFCDocument62 pagesUniversal Banking HDFCrajesh bathulaNo ratings yet

- A Study On Portfolio Construction/ManagementDocument81 pagesA Study On Portfolio Construction/ManagementAshickNo ratings yet

- Final Project - AZIZDocument73 pagesFinal Project - AZIZsmart boyNo ratings yet

- Annual Project On Piramal Finance Abhishek UpadhyayDocument20 pagesAnnual Project On Piramal Finance Abhishek UpadhyayAbhishek UpadhyayNo ratings yet

- Internship ProjectDocument105 pagesInternship ProjectChandrakant Rana SinghNo ratings yet

- (Arts, Science, Commerce & Self Finance Course) I, MR. ANSARIDocument90 pages(Arts, Science, Commerce & Self Finance Course) I, MR. ANSARISarfaraz AnsariNo ratings yet

- Anand Final ReportDocument66 pagesAnand Final ReportImran KhanNo ratings yet

- Sbi Project PDFDocument80 pagesSbi Project PDFALLU SRISAINo ratings yet

- Capital StructureDocument69 pagesCapital StructureRadha ChoudhariNo ratings yet

- Sarfaraz Sip Report 2018 Final.Document53 pagesSarfaraz Sip Report 2018 Final.Yugi 101anupNo ratings yet

- Gaurav PDFDocument70 pagesGaurav PDFSandesh GajbhiyeNo ratings yet

- Demant AccountDocument78 pagesDemant AccountAmanjotNo ratings yet

- Sejal MhatreDocument64 pagesSejal MhatrePranav PasteNo ratings yet

- "SEO and Social Media Marketing": A Project Report OnDocument58 pages"SEO and Social Media Marketing": A Project Report Onrashmi choudharyNo ratings yet

- A Study On Risk and Return Analysis of Mutual Fund at SBI Mutual Funds, Bangalore PDFDocument58 pagesA Study On Risk and Return Analysis of Mutual Fund at SBI Mutual Funds, Bangalore PDFYash WahaneNo ratings yet

- SIP (FinalReport)Document125 pagesSIP (FinalReport)Nikhil Goyal 141No ratings yet

- Consumer Behaviour Towards Royal Enfield of JanakDocument56 pagesConsumer Behaviour Towards Royal Enfield of JanaksrNo ratings yet

- " Consumer Percepton Towards Kara Products": Page - 1Document61 pages" Consumer Percepton Towards Kara Products": Page - 1karishmaNo ratings yet

- Sample Project HRDocument81 pagesSample Project HRRVS INSTITUTE OF MANAGEMENT STUDIES COIMBATORENo ratings yet

- Project Customer Toward E-Banking ADITYA - 220706 - 173422Document64 pagesProject Customer Toward E-Banking ADITYA - 220706 - 173422Prabhu SahuNo ratings yet

- Amity University RaipurDocument57 pagesAmity University RaipurPRAKNo ratings yet

- A Study On Commodity Market With Reference PDFDocument46 pagesA Study On Commodity Market With Reference PDFPraveen B ENo ratings yet

- Abhishek GeneralDocument51 pagesAbhishek GeneralTasmay EnterprisesNo ratings yet

- (Departmentofmanagementstudies) MDocument54 pages(Departmentofmanagementstudies) MHarshpreet Kaur 20204No ratings yet

- Internship Report: N. M. Baki Billah Lecturer, BRAC Business School Brac UniversityDocument35 pagesInternship Report: N. M. Baki Billah Lecturer, BRAC Business School Brac Universityanisul islamNo ratings yet

- Kalyani Black BookDocument100 pagesKalyani Black BookUjjwal Joseph fernanded100% (1)

- Guide CertificateDocument69 pagesGuide CertificateRoopam Chandel100% (1)

- Riddhi VadherDocument79 pagesRiddhi VadherPratik MahajanNo ratings yet

- A Project Report ON Real Estate Pasia Developers Pvt. LTDDocument68 pagesA Project Report ON Real Estate Pasia Developers Pvt. LTDaslam khanNo ratings yet

- ReportDocument76 pagesReportSRI RAM MANOJNo ratings yet

- A Summer Internship Project Report OnDocument91 pagesA Summer Internship Project Report Onshubham kumawatNo ratings yet

- 2 Final ReportDocument103 pages2 Final ReportChandan SrivastavaNo ratings yet

- Project ReportDocument65 pagesProject ReportstafanaNo ratings yet

- Petromin Pakistan MBA Final Report 2023 Full MondayDocument55 pagesPetromin Pakistan MBA Final Report 2023 Full MondaySaad ShahzadNo ratings yet

- Ilovepdf MergedDocument100 pagesIlovepdf MergedsaiyuvatechNo ratings yet

- Khushpreet MbaDocument55 pagesKhushpreet MbaKaran SandhuNo ratings yet

- SIP Sanika 20110Document70 pagesSIP Sanika 20110Kshitija BorhadeNo ratings yet

- Sip ReportDocument64 pagesSip ReportYogyataMishraNo ratings yet

- Project Report12 PDFDocument55 pagesProject Report12 PDFNatthu WaykosNo ratings yet

- Aviva Life InsuranceDocument85 pagesAviva Life InsuranceArpan SinghalNo ratings yet

- 20221020195836+ (2) Abcdpdf PDF To WordDocument66 pages20221020195836+ (2) Abcdpdf PDF To WordAbhishek gaushalaNo ratings yet

- Ajay Anada Chormale Project Tybba Sem VDocument53 pagesAjay Anada Chormale Project Tybba Sem VParikshit Ashok ManeNo ratings yet

- Sawan Gupta123456789Document82 pagesSawan Gupta123456789SERP Rank PlusNo ratings yet

- Segmentation and Penetration HDFC BankDocument41 pagesSegmentation and Penetration HDFC Banksuraj bhagwat100% (1)

- Various Financial Services Product Provided by HDFC BANKDocument82 pagesVarious Financial Services Product Provided by HDFC BANKVipul TandonNo ratings yet

- Vishal Mega MartDocument94 pagesVishal Mega MartreplynimeshNo ratings yet

- Dissertation Submitted in Partial Fulfilment of The Requirements For The Award of The Two-Year Full-TimeDocument52 pagesDissertation Submitted in Partial Fulfilment of The Requirements For The Award of The Two-Year Full-TimeMuskan GuptaNo ratings yet

- Anand Dani Project SAPMDocument70 pagesAnand Dani Project SAPMJiavidhi SharmaNo ratings yet

- "Understand The Ecosystem in Digital Media Marketing Referance To Atishay LimitedDocument59 pages"Understand The Ecosystem in Digital Media Marketing Referance To Atishay LimitedBRC POLURNo ratings yet

- SIP REPORT Akashay (AutoRecovered)Document67 pagesSIP REPORT Akashay (AutoRecovered)Akashay JainNo ratings yet

- Summer Intenship Report On Flipkart FC by ShashankDocument125 pagesSummer Intenship Report On Flipkart FC by ShashankAbhinav RandevNo ratings yet

- HDFC LifeDocument64 pagesHDFC Lifevandana photostateNo ratings yet

- A Summer Training Project Report On: Performance Appraisal "HDFC Life Insurance Co. LTD."Document58 pagesA Summer Training Project Report On: Performance Appraisal "HDFC Life Insurance Co. LTD."Rakesh MandalNo ratings yet

- A Case Study of "Employee Satisfaction" of HDFC Standard Life InsuranceDocument57 pagesA Case Study of "Employee Satisfaction" of HDFC Standard Life InsuranceKushan SudanNo ratings yet

- Group PolicyDocument14 pagesGroup PolicyMahesh DivakarNo ratings yet

- Richard Sabo v. Metropolitan Life Insurance Company Gary Antonino Joel Sherman Ronald Schram United Food and Commercial Workers International Union, Afl-Cio, CLC, 137 F.3d 185, 3rd Cir. (1998)Document17 pagesRichard Sabo v. Metropolitan Life Insurance Company Gary Antonino Joel Sherman Ronald Schram United Food and Commercial Workers International Union, Afl-Cio, CLC, 137 F.3d 185, 3rd Cir. (1998)Scribd Government DocsNo ratings yet

- Actuarial ScienceDocument10 pagesActuarial ScienceAkinNo ratings yet

- Annual Report 2010-11Document336 pagesAnnual Report 2010-11Mansi Latawa AgrawalNo ratings yet

- Lumibao v. IACDocument5 pagesLumibao v. IACErnie GultianoNo ratings yet

- 50+ FREE SMS Message Templates For Financial BusinessesDocument16 pages50+ FREE SMS Message Templates For Financial Businessesbarmanpuja209No ratings yet

- Dia Mae A. Generoso - Learning Activity 3Document10 pagesDia Mae A. Generoso - Learning Activity 3Dia Mae Ablao GenerosoNo ratings yet

- Predicting Individuals Car Accident Risk by Traje 2022 Computers EnvironmeDocument12 pagesPredicting Individuals Car Accident Risk by Traje 2022 Computers EnvironmeNikita PokharkarNo ratings yet

- Marine Insurance in MalaysiaDocument6 pagesMarine Insurance in MalaysiaLisa Sofie AdamNo ratings yet

- Labor - AzucenaDocument70 pagesLabor - AzucenaLirio Iringan100% (7)

- Mercantile Law - Paramount Insurance Corp. v. Sps. Remondeulaz, G.R. No. 173773, November 28, 2012Document2 pagesMercantile Law - Paramount Insurance Corp. v. Sps. Remondeulaz, G.R. No. 173773, November 28, 2012Dayday Able0% (1)

- Business Analytics and Research Major ProjectDocument17 pagesBusiness Analytics and Research Major ProjectIshaan KumarNo ratings yet

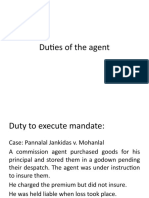

- Duties of The AgentDocument11 pagesDuties of The AgentNitish Kumar NaveenNo ratings yet

- IntAcc 3 Non-Financial LiabilitiesDocument10 pagesIntAcc 3 Non-Financial LiabilitiesKim EllaNo ratings yet

- Edisonlearning, Inc. 2013-2014 Schedule of Insurance: Coverage and Location Amount Insured PropertyDocument2 pagesEdisonlearning, Inc. 2013-2014 Schedule of Insurance: Coverage and Location Amount Insured PropertyYork Daily Record/Sunday NewsNo ratings yet

- BROCHUREDocument1 pageBROCHUREJarvisNo ratings yet

- Law of InsuranceDocument37 pagesLaw of Insuranceshubham kumarNo ratings yet

- Creche GuidelinesDocument20 pagesCreche GuidelinesspringboardyNo ratings yet

- On The Fintech Revolution Interpreting The Forces of Innovation 2018Document47 pagesOn The Fintech Revolution Interpreting The Forces of Innovation 2018Albert Kirby TardeoNo ratings yet

- Tibay v. CADocument1 pageTibay v. CAEva TrinidadNo ratings yet

- Make A Budget: My Income This MonthDocument2 pagesMake A Budget: My Income This MonthjuanNo ratings yet

- Location Agreement - SAMPLEDocument4 pagesLocation Agreement - SAMPLEDino TomljanovićNo ratings yet

- Kotak Mahindra Life InsuranceDocument51 pagesKotak Mahindra Life InsuranceRiddhi GalaNo ratings yet

- Lifemark ON MVA Billing AgreementDocument1 pageLifemark ON MVA Billing AgreementRavi KaushikNo ratings yet

- Notice: Investment Company Act of 1940: Guardian Cash Fund, Inc., Et Al.Document4 pagesNotice: Investment Company Act of 1940: Guardian Cash Fund, Inc., Et Al.Justia.comNo ratings yet

- Reshop Your Car Insurance: FundamentalsDocument3 pagesReshop Your Car Insurance: FundamentalsAlejandra RoseroNo ratings yet

- Answers To Test Yourunderstanding QuestionsDocument5 pagesAnswers To Test Yourunderstanding QuestionsDean Rodriguez100% (2)

- Accommodation in Wolfson CollegeDocument48 pagesAccommodation in Wolfson CollegeAnonymous 84SDqAVLPnNo ratings yet