Download as docx, pdf, or txt

You might also like

- Advanced CivAdv - Vegoil Lecture Note 2. A Brief Overview of The Substantive Law. 2022Document5 pagesAdvanced CivAdv - Vegoil Lecture Note 2. A Brief Overview of The Substantive Law. 2022Ee Fey TehNo ratings yet

- Export Process in PakistanDocument14 pagesExport Process in Pakistanazeemtahir56625% (4)

- Accounting Policies in Bharat ElectronicsDocument4 pagesAccounting Policies in Bharat ElectronicsNafis SiddiquiNo ratings yet

- Analysis of Indian CompaniesDocument7 pagesAnalysis of Indian CompaniesSiddhant MalhotraNo ratings yet

- IntAcc1 - CHAPTER 23 and 25Document10 pagesIntAcc1 - CHAPTER 23 and 25Clyde Justine CablingNo ratings yet

- ASSIGNMENTDocument7 pagesASSIGNMENTRahulNo ratings yet

- Master NoteDocument9 pagesMaster NoteCA Paramesh HemanathNo ratings yet

- Accounting Standard of Mahindra and Mahindra LTDDocument9 pagesAccounting Standard of Mahindra and Mahindra LTDDheeraj shettyNo ratings yet

- Schedule - Specimen of Statement of Significant Accounting PoliciesDocument16 pagesSchedule - Specimen of Statement of Significant Accounting Policiesav_meshramNo ratings yet

- Non-Current Assets - Ppe: Conceptual Framework & Accounting StandardsDocument14 pagesNon-Current Assets - Ppe: Conceptual Framework & Accounting StandardsDebbie Grace Latiban LinazaNo ratings yet

- Chapter 10 PropertyDocument10 pagesChapter 10 Propertymaria isabellaNo ratings yet

- FA Materials - Chapter 8Document18 pagesFA Materials - Chapter 8Nazrin HasanzadehNo ratings yet

- Accounting PolicyDocument28 pagesAccounting PolicyAkshay AnandNo ratings yet

- Chapter 17 - Ppe - AssignmentDocument16 pagesChapter 17 - Ppe - Assignmentsabina del monteNo ratings yet

- Studet Practical Accounting Ch17 PPE AcquisitionDocument16 pagesStudet Practical Accounting Ch17 PPE Acquisitionsabina del monteNo ratings yet

- FRA - Accounting PoliciesDocument4 pagesFRA - Accounting PoliciesGarima SharmaNo ratings yet

- Chapter 10 NotesDocument22 pagesChapter 10 NotesSittie Ainna Acmed UnteNo ratings yet

- (Acctg 112) Pas 16 & 23Document4 pages(Acctg 112) Pas 16 & 23Mae PandoraNo ratings yet

- Statement of ComplianceDocument21 pagesStatement of ComplianceFaiz Smile BuddyNo ratings yet

- Fama AssignmentDocument7 pagesFama AssignmentAdityaNo ratings yet

- Tata Motors Notes Forming Part of Financial StatementsDocument36 pagesTata Motors Notes Forming Part of Financial StatementsSwarup RanjanNo ratings yet

- Significant Accounting Policies TVS MotorsDocument12 pagesSignificant Accounting Policies TVS MotorsArjun Singh Omkar100% (1)

- Accounting Policy As Per FSDocument17 pagesAccounting Policy As Per FSShubham TiwariNo ratings yet

- 2.7 Intangible Assets (A) GoodwillDocument8 pages2.7 Intangible Assets (A) GoodwillLolita IsakhanyanNo ratings yet

- Accounting Policies of DaburDocument10 pagesAccounting Policies of DaburMkNo ratings yet

- Probiotec Annual Report 2022 6Document8 pagesProbiotec Annual Report 2022 6楊敬宇No ratings yet

- Picwise Mart - Notes To Financial Statements - 31dec2021Document1 pagePicwise Mart - Notes To Financial Statements - 31dec2021Thomas Daniel CuarteroNo ratings yet

- Accounting Policies - Study Group 4IDocument24 pagesAccounting Policies - Study Group 4ISatish Ranjan PradhanNo ratings yet

- Significant Accounting PoliciesDocument4 pagesSignificant Accounting PoliciesAdarsh NethwewalaNo ratings yet

- International Accounting Standard 16 Property, Plant and EquipmentDocument29 pagesInternational Accounting Standard 16 Property, Plant and EquipmentAbdullah Shaker TahaNo ratings yet

- StalasaDocument23 pagesStalasajessa mae zerdaNo ratings yet

- 5 Long Term Construction Contract 3e5ca4a29cf252303 Ffcc2ab83e9ecba CompressDocument12 pages5 Long Term Construction Contract 3e5ca4a29cf252303 Ffcc2ab83e9ecba Compressgelly studiesNo ratings yet

- Chapter 15 - Pas 16 PpeDocument36 pagesChapter 15 - Pas 16 PpeMarriel Fate CullanoNo ratings yet

- Accounting For PPE - PAS 16Document39 pagesAccounting For PPE - PAS 16Marriel Fate Cullano100% (1)

- 11 PED Accounting Policy For PETCO and PESCODocument18 pages11 PED Accounting Policy For PETCO and PESCOrkmv1922No ratings yet

- Lesson 9 Long Term ConstructionDocument13 pagesLesson 9 Long Term ConstructionheyheyNo ratings yet

- Section 4 IDocument22 pagesSection 4 ISatish Ranjan PradhanNo ratings yet

- Chapter 15 - Property, Plant, and EquipmentDocument3 pagesChapter 15 - Property, Plant, and EquipmentFerb CruzadaNo ratings yet

- Standalone Notes To AccountsDocument31 pagesStandalone Notes To AccountsJP Jeya PrasannaNo ratings yet

- PPEDocument5 pagesPPERodelia MalacastaNo ratings yet

- Major Accounting PoliciesDocument8 pagesMajor Accounting Policies325KAIVALYAPAINo ratings yet

- IAS16Document2 pagesIAS16Atif RehmanNo ratings yet

- Chapter 7 Revenue From Contracts With Customers SVDocument21 pagesChapter 7 Revenue From Contracts With Customers SV21073141No ratings yet

- Chapter 1 Property Plant and EquipmentDocument26 pagesChapter 1 Property Plant and EquipmentJellai TejeroNo ratings yet

- PFRS 15Document3 pagesPFRS 15Micaella DanoNo ratings yet

- Ias 16 PropertyDocument11 pagesIas 16 PropertyFolarin EmmanuelNo ratings yet

- PSBA - Property, Plant and EquipmentDocument13 pagesPSBA - Property, Plant and EquipmentAbdulmajed Unda MimbantasNo ratings yet

- 9 - Property, Plant & Equipment (PPE)Document84 pages9 - Property, Plant & Equipment (PPE)chingNo ratings yet

- Consolidated Financial Statements Indian GAAP Dec07Document15 pagesConsolidated Financial Statements Indian GAAP Dec07martynmvNo ratings yet

- 5 Long-Term Construction ContractDocument12 pages5 Long-Term Construction ContractMark TaysonNo ratings yet

- Summary PpeDocument8 pagesSummary PpeJenilyn CalaraNo ratings yet

- PAS 16 Property, Plant and EquipmentDocument4 pagesPAS 16 Property, Plant and Equipmentpanda 1No ratings yet

- Module 4Document10 pagesModule 4bhettyna noayNo ratings yet

- Revenue From Contracts With CustomersDocument5 pagesRevenue From Contracts With Customers70fugnayjanetNo ratings yet

- Part D-8 Tangible Non Current Assests (ch06)Document68 pagesPart D-8 Tangible Non Current Assests (ch06)hyangNo ratings yet

- Historical Cost of Property, Plant and EquipmentDocument9 pagesHistorical Cost of Property, Plant and EquipmentChinchin Ilagan DatayloNo ratings yet

- Contract CostingDocument27 pagesContract CostingNishit BaralNo ratings yet

- Chapter 7: Audit of Intangibles and Other Assets: Internal Control Over IntangiblesDocument28 pagesChapter 7: Audit of Intangibles and Other Assets: Internal Control Over IntangiblesUn knownNo ratings yet

- Notes To Balance Sheet and Statement of Profit and Loss: Hundred and Seventh Annual Report 2013-14Document44 pagesNotes To Balance Sheet and Statement of Profit and Loss: Hundred and Seventh Annual Report 2013-14galacticwormNo ratings yet

- Audit Report: Accounting Standard and The Enterprise Accounting System Issued by Our Country, andDocument8 pagesAudit Report: Accounting Standard and The Enterprise Accounting System Issued by Our Country, andStefy DyaNo ratings yet

- OBDocument8 pagesOBNikunj WaghelaNo ratings yet

- 23 - Nikunj WaghelaDocument2 pages23 - Nikunj WaghelaNikunj WaghelaNo ratings yet

- Statistic Project Roll No. 23Document4 pagesStatistic Project Roll No. 23Nikunj WaghelaNo ratings yet

- Maths AssignmentDocument13 pagesMaths AssignmentNikunj WaghelaNo ratings yet

- APM draftSPA01NAR55深圳坤成 10 APRIL 2023Document16 pagesAPM draftSPA01NAR55深圳坤成 10 APRIL 2023ances fanleo sinagaNo ratings yet

- Purchase Order/Contract: Date: PO#: Supplier: BuyerDocument6 pagesPurchase Order/Contract: Date: PO#: Supplier: BuyerQuynh HoNo ratings yet

- Mẫu Giấy yêu cầu phát hành LC WordDocument4 pagesMẫu Giấy yêu cầu phát hành LC WordHuyền Linh100% (1)

- Sale of Goods Oxford.Document38 pagesSale of Goods Oxford.Alexandru I. Diaconu0% (1)

- Đáp Án Đề Thi Hk 3 - Năm Học 2020-2021: BM02a/QT01/KTDocument27 pagesĐáp Án Đề Thi Hk 3 - Năm Học 2020-2021: BM02a/QT01/KTThị Anh Thư LêNo ratings yet

- Delgado Marrufo Ing 1 PafDocument107 pagesDelgado Marrufo Ing 1 PafmathiasNo ratings yet

- BL-T321WSB-4 Tran My Phuong B1112014584 Individual-EssayDocument8 pagesBL-T321WSB-4 Tran My Phuong B1112014584 Individual-EssayMy Phuong TranNo ratings yet

- Internship Report Apparel ManufacturingDocument29 pagesInternship Report Apparel ManufacturingRoshan Pandey100% (1)

- Rickmers Terms and Definitions 76 PagesDocument76 pagesRickmers Terms and Definitions 76 Pagessarath_babu_14100% (1)

- Tender DocumentDocument29 pagesTender DocumentPrakash ArthurNo ratings yet

- Bid - Doc Freight 2023Document53 pagesBid - Doc Freight 2023Geodelyn TolentinoNo ratings yet

- Bidding ZESCO-095-2018 Volume 1 of 3 Bidding Procedures-Contract and FormsDocument257 pagesBidding ZESCO-095-2018 Volume 1 of 3 Bidding Procedures-Contract and FormsChaitanya AdkarNo ratings yet

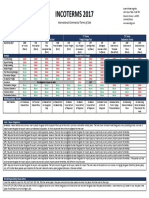

- Incoterms 2017Document1 pageIncoterms 2017iogenrNo ratings yet

- SSDP School Level Procurement ManualDocument107 pagesSSDP School Level Procurement ManualShiva Ram ShresthaNo ratings yet

- Exim ProspectusDocument4 pagesExim ProspectusArup ChakrabortyNo ratings yet

- Supply Chain ManagementDocument19 pagesSupply Chain ManagementmrkspnzNo ratings yet

- YANFENG Supplier Standards ManualDocument42 pagesYANFENG Supplier Standards Manualwulfgang66100% (1)

- (1949) A.C. 293Document33 pages(1949) A.C. 293Ifeoluwa Oladeji-Oduola0% (1)

- Atlas Honda ReportDocument26 pagesAtlas Honda ReportQamar TanauliNo ratings yet

- Pricing Strategy of Export Oriented Garment: Vertex Fashion LimitedDocument9 pagesPricing Strategy of Export Oriented Garment: Vertex Fashion LimitedIqbal HasanNo ratings yet

- Toa 1404Document9 pagesToa 1404chowchow123No ratings yet

- Insurable Interest of Insured in Marine Insurance (Sec 102-108)Document1 pageInsurable Interest of Insured in Marine Insurance (Sec 102-108)EileenShiellaDialimasNo ratings yet

- Sales Contract: 1. Commodity - Quantity - Price Product Description Quantity (Ton) Unit Price AmountDocument3 pagesSales Contract: 1. Commodity - Quantity - Price Product Description Quantity (Ton) Unit Price AmountNam TrịnhNo ratings yet

- Ibl Fin SP20Document2 pagesIbl Fin SP20Onyando NyabutoNo ratings yet

- ATMI CFR - CIF - DES August 2012Document38 pagesATMI CFR - CIF - DES August 2012KERVINNo ratings yet

- Europe Africa Refined Products MethodologyDocument29 pagesEurope Africa Refined Products MethodologyOssama bohamdNo ratings yet

- Incoterms 2020Document94 pagesIncoterms 2020dc-183158No ratings yet

- Fashion Merchandising TDDocument62 pagesFashion Merchandising TDpmthanveerNo ratings yet