Download as docx, pdf, or txt

You might also like

- Mirror For Humanity: A Concise Introduction To Cultural Anthropology by Conrad Kottak - 9e, TEST BANK 0078035058Document12 pagesMirror For Humanity: A Concise Introduction To Cultural Anthropology by Conrad Kottak - 9e, TEST BANK 0078035058jksmtnNo ratings yet

- Danbury November 2023 Municipal Election Returns (Amended)Document91 pagesDanbury November 2023 Municipal Election Returns (Amended)Alfonso RobinsonNo ratings yet

- Constitutional Bases of Public Finance in The Philippines (Taxation)Document23 pagesConstitutional Bases of Public Finance in The Philippines (Taxation)DARLENE100% (1)

- Lesson I - The Role and Scope of Public FinanceDocument3 pagesLesson I - The Role and Scope of Public Financemarygracepronquillo100% (10)

- Case 1 - Iguazu Offices Financial ModelDocument32 pagesCase 1 - Iguazu Offices Financial ModelapoorvnigNo ratings yet

- Public Sector Accounting: Mr. Evans AgalegaDocument50 pagesPublic Sector Accounting: Mr. Evans AgalegaElvis Yarig100% (2)

- GOVERNMENT ACCOUNTING - Accounting Responsibilities.Document19 pagesGOVERNMENT ACCOUNTING - Accounting Responsibilities.Hannah Verano86% (7)

- Psa Class Notes Daf 2020-21Document22 pagesPsa Class Notes Daf 2020-21kitderoger_391648570No ratings yet

- Chapter 1Document6 pagesChapter 1Dùķe HPNo ratings yet

- AfPS&CS Ch-01Document10 pagesAfPS&CS Ch-01Amelwork AlchoNo ratings yet

- Introduction To Public Sector Accounting and FinanceDocument9 pagesIntroduction To Public Sector Accounting and FinanceBabah Silas VersilaNo ratings yet

- PSAF - Note 1Document39 pagesPSAF - Note 1Grace HenryNo ratings yet

- NFP Chapter 1-9 2023 EditedDocument63 pagesNFP Chapter 1-9 2023 Editednegamedhane58No ratings yet

- Ipsas ExitDocument24 pagesIpsas ExitAbdiNo ratings yet

- Public Sector Handout 222Document29 pagesPublic Sector Handout 222HarusiNo ratings yet

- 518 Hand-Out (Resti)Document5 pages518 Hand-Out (Resti)RALLISON100% (1)

- Government and NFP Entities Accounting Chapter 1: IntroductionDocument8 pagesGovernment and NFP Entities Accounting Chapter 1: IntroductionFiriehiwot BirhanieNo ratings yet

- Pa 22 - Public Accounting & Budgeting Second Semester, Sy 2023 - 2024 Hand-OutsDocument82 pagesPa 22 - Public Accounting & Budgeting Second Semester, Sy 2023 - 2024 Hand-OutsCharles Elquime GalaponNo ratings yet

- Afin321 FPD 4 2015 2Document27 pagesAfin321 FPD 4 2015 2Thomas nyadeNo ratings yet

- Chapter OneDocument14 pagesChapter OneChera HabebawNo ratings yet

- Chapter III International Public Sector Accounting Stanadards IPSASDocument26 pagesChapter III International Public Sector Accounting Stanadards IPSASnatnaelsleshi3No ratings yet

- Document .1234Document20 pagesDocument .1234Tasebe GetachewNo ratings yet

- GOVERNMENT ACCOUNTING Accounting ResponsibilitiesDocument19 pagesGOVERNMENT ACCOUNTING Accounting ResponsibilitiesColor BlueNo ratings yet

- Ethiopian Gov't AssignmentDocument7 pagesEthiopian Gov't AssignmentHasen Yib0% (1)

- Accounting For Public Sector Chapter 2 - 082036Document14 pagesAccounting For Public Sector Chapter 2 - 082036ilifnahomNo ratings yet

- Accounting For Government and Non-Profit Organizations BSA32E1Document40 pagesAccounting For Government and Non-Profit Organizations BSA32E1Christine Joyce Magote100% (1)

- Government Accounting Defined (Section 109 of PD 1445)Document7 pagesGovernment Accounting Defined (Section 109 of PD 1445)Harley GumaponNo ratings yet

- Lesson 1 Overview of Government AccountingDocument12 pagesLesson 1 Overview of Government AccountingkimberlyroseabianNo ratings yet

- Aa 4102 Hand Outs Part 1Document12 pagesAa 4102 Hand Outs Part 1Ace Hulsey TevesNo ratings yet

- PFM Hand BookDocument53 pagesPFM Hand BookWaqar AhmadNo ratings yet

- APSAF TERM PAPER CompleteDocument15 pagesAPSAF TERM PAPER CompleteOyeleye TofunmiNo ratings yet

- Ac 518 Hand-Outs Government Accounting and Auditing TNCR: The National Government of The PhilippinesDocument53 pagesAc 518 Hand-Outs Government Accounting and Auditing TNCR: The National Government of The PhilippinesHarley Gumapon100% (1)

- Nature and Scope of Financial AdministrationDocument29 pagesNature and Scope of Financial AdministrationAng libuderaNo ratings yet

- Ethics in Public Sector Accounting PracticeDocument11 pagesEthics in Public Sector Accounting PracticeAulia AlfianitaNo ratings yet

- Chapter 2 Social Account and TransactionDocument33 pagesChapter 2 Social Account and TransactionNanye AbichNo ratings yet

- Ch.2 PGDocument12 pagesCh.2 PGkasimNo ratings yet

- Intro of PSA-1Document47 pagesIntro of PSA-1sami ullahNo ratings yet

- Review of LiteratureDocument33 pagesReview of LiteratureArah OpalecNo ratings yet

- Wa0000.Document5 pagesWa0000.Shawon Moshiur RahamanNo ratings yet

- PSAF - Summarized TextDocument204 pagesPSAF - Summarized TextCosmos LeeNo ratings yet

- Government Accounting Handouts PDFDocument50 pagesGovernment Accounting Handouts PDFureka6arnicaNo ratings yet

- Chapter 1 Governmental AccountingDocument12 pagesChapter 1 Governmental AccountingMoh ShiineNo ratings yet

- Chapter 2 GADocument69 pagesChapter 2 GAsimaNo ratings yet

- Psa 1Document47 pagesPsa 1Emmanuel OpokuNo ratings yet

- 1 Chapter One Govt and NFPDocument27 pages1 Chapter One Govt and NFPantex nebyu100% (1)

- Bsa 3204 Accouting For Government and Not For Profit Entities - IntroductionDocument4 pagesBsa 3204 Accouting For Government and Not For Profit Entities - IntroductionjenieNo ratings yet

- Introduction To Public Sector Accounting Learning ObjectivesDocument14 pagesIntroduction To Public Sector Accounting Learning ObjectivesRoite BeteroNo ratings yet

- PublicDocument66 pagesPublicObsa QabaadhuNo ratings yet

- LGD 218 BusayoDocument39 pagesLGD 218 BusayoayomideogundipeNo ratings yet

- AC 518 Summer Term 2013 1st Hand-OutDocument29 pagesAC 518 Summer Term 2013 1st Hand-OutSergszel AliserNo ratings yet

- Accounting For Public Sector and Civic SocietyDocument65 pagesAccounting For Public Sector and Civic Societynunyatzewdie1No ratings yet

- Finanzas PublicaDocument4 pagesFinanzas Publicamiyereth PiedrahitaNo ratings yet

- Public Sector Accounting and Finance AssignmentDocument5 pagesPublic Sector Accounting and Finance AssignmentBabah Silas VersilaNo ratings yet

- CH 2 fundGNFPDocument78 pagesCH 2 fundGNFPGena Alisuu100% (1)

- Local Govovernment Work-1Document10 pagesLocal Govovernment Work-1Tracey Owusu AbabioNo ratings yet

- AA 4102 1st Hand OutDocument9 pagesAA 4102 1st Hand OutMana XDNo ratings yet

- Beechy 7e Tif ch11Document5 pagesBeechy 7e Tif ch11mashta04No ratings yet

- Chapter 1Document10 pagesChapter 1abdirazakhNo ratings yet

- Accounting Standards For The Public and Non-Profit Organization in The USADocument11 pagesAccounting Standards For The Public and Non-Profit Organization in The USAvishalravi04No ratings yet

- Ch1 TaxDocument96 pagesCh1 Taxnatnaelsleshi3No ratings yet

- New Ac 518 Hand OutsDocument16 pagesNew Ac 518 Hand OutsJieve Licca G. FanoNo ratings yet

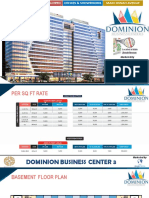

- Dominion Business Center 3 FinalDocument6 pagesDominion Business Center 3 FinalBlue Earth PropertiesNo ratings yet

- Resolution No. 3 S 2021 First Time Jobseekers Act Today March 19Document9 pagesResolution No. 3 S 2021 First Time Jobseekers Act Today March 19BARANGAY MOLINO IINo ratings yet

- 1973 ConstitutionDocument37 pages1973 Constitutionmaqbool ur rehmanNo ratings yet

- House Hearing, 112TH Congress - Harmonizing Global Derivatives Reform: Impact On U.S. Competitiveness and Market StabilityDocument117 pagesHouse Hearing, 112TH Congress - Harmonizing Global Derivatives Reform: Impact On U.S. Competitiveness and Market StabilityScribd Government DocsNo ratings yet

- 21-05-14 VLSI Opposition To Intel's Rule 52 Motion (Unclean Hands)Document27 pages21-05-14 VLSI Opposition To Intel's Rule 52 Motion (Unclean Hands)Florian MuellerNo ratings yet

- Igcse - Final AccountsDocument4 pagesIgcse - Final AccountsMUSTHARI KHANNo ratings yet

- (Download PDF) Introduction To Algorithms 3rd Edition Cormen Solutions Manual Full ChapterDocument15 pages(Download PDF) Introduction To Algorithms 3rd Edition Cormen Solutions Manual Full Chapterrajgiroberio100% (7)

- TATA CARA Shalat-TathawwuDocument30 pagesTATA CARA Shalat-TathawwuSyamNo ratings yet

- ShakushainDocument30 pagesShakushainJosé manuel BlancoNo ratings yet

- Asharab Aamir SheikhDocument7 pagesAsharab Aamir Sheikhhumair chauhdaryNo ratings yet

- Roland Gérard BarthesDocument17 pagesRoland Gérard BarthesEducation147No ratings yet

- Unit 6 - Lets Talk About English - ISL CollectiveDocument1 pageUnit 6 - Lets Talk About English - ISL CollectiveSilvia Juliana Navarro AranaNo ratings yet

- Chapter 1: Introduction To Accounting: Activity 1: A Chapter DiscussionDocument9 pagesChapter 1: Introduction To Accounting: Activity 1: A Chapter DiscussionFaith ClaireNo ratings yet

- Hybristophilia White PaperDocument14 pagesHybristophilia White Paperxenoalt.ethanNo ratings yet

- Revilla v. Office of The Ombudsman20170125-898-5i1u8sDocument76 pagesRevilla v. Office of The Ombudsman20170125-898-5i1u8sAngelicaNo ratings yet

- Women DirectorDocument6 pagesWomen DirectorMayank Sen100% (1)

- Criminal Law Art 293-294Document22 pagesCriminal Law Art 293-294Zen ArinesNo ratings yet

- DOM ManualDocument874 pagesDOM ManualDavid BivensNo ratings yet

- EnglishDocument24 pagesEnglishyesica rojasNo ratings yet

- US Vs JavierDocument2 pagesUS Vs JavierMarivic Asilo Zacarias-Lozano100% (1)

- Maybank Ezycash/Ezycash-I - Terms and ConditionsDocument4 pagesMaybank Ezycash/Ezycash-I - Terms and Conditionsk fineNo ratings yet

- Wasim Property CasesDocument10 pagesWasim Property Casestahmoor ahmedNo ratings yet

- Environment in Twenty Pages - For UPSC Civi - Baranwal, Varunkumar Baranwal, VarunkumarDocument36 pagesEnvironment in Twenty Pages - For UPSC Civi - Baranwal, Varunkumar Baranwal, Varunkumaramit100% (1)

- Case Doctrines - DamagesDocument10 pagesCase Doctrines - DamagesJoseph John Santos RonquilloNo ratings yet

- ქირავნობა - EngDocument4 pagesქირავნობა - Engluka daneliaNo ratings yet

- Postal RuleDocument6 pagesPostal Rulesvb charyNo ratings yet

- IPA Neerathon - Employee EngagementDocument14 pagesIPA Neerathon - Employee EngagementSujal ShahNo ratings yet