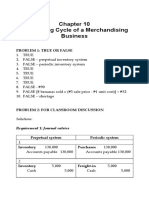

Merchandising Concern 09-26-2022

Merchandising Concern 09-26-2022

You might also like

- Icici Bank StatementDocument22 pagesIcici Bank StatementVIJAY BHASAKAR100% (1)

- Nedbank Statement Nov2023Document36 pagesNedbank Statement Nov2023ernest.mmilaNo ratings yet

- Chapter 1-Introduction To The World of RetailingDocument29 pagesChapter 1-Introduction To The World of RetailingAshaAnwar83% (6)

- Sol. Man. - Chapter 10 - Acctg Cycle of A Merchandising BusinessDocument65 pagesSol. Man. - Chapter 10 - Acctg Cycle of A Merchandising BusinessPeter Piper67% (3)

- Journalizing Merchandising Transactions, Problem #13Document2 pagesJournalizing Merchandising Transactions, Problem #13Feiya Liu80% (10)

- The McGraw-Hill 36-Hour Course: Finance for Non-Financial Managers 3/EFrom EverandThe McGraw-Hill 36-Hour Course: Finance for Non-Financial Managers 3/ERating: 4.5 out of 5 stars4.5/5 (6)

- Task 5Document9 pagesTask 5Honey TolentinoNo ratings yet

- Alternate Demonstration Problem MerchandisingDocument5 pagesAlternate Demonstration Problem MerchandisingmoNo ratings yet

- Answer InventoryDocument7 pagesAnswer InventoryAllen Carl60% (5)

- Sallys Struthers - Answer KeyDocument7 pagesSallys Struthers - Answer KeyLlyod Francis LaylayNo ratings yet

- 6th Sem Project ReportDocument93 pages6th Sem Project ReportSwati Kataria67% (3)

- Chapter 7 Problems: Problem #14 P. 7-57 Problem #15 P. 7-58Document3 pagesChapter 7 Problems: Problem #14 P. 7-57 Problem #15 P. 7-58Zyrene Kei ReyesNo ratings yet

- Review Quiz Inter1Document9 pagesReview Quiz Inter1Vanessa vnssNo ratings yet

- Latihan Siklus Dagang 1Document26 pagesLatihan Siklus Dagang 1AFIFA SAQIFANo ratings yet

- Lec Merchandising Perpetual PeriodicDocument8 pagesLec Merchandising Perpetual PeriodicAiddan Clark De JesusNo ratings yet

- Midterms FAR Quiz 1Document15 pagesMidterms FAR Quiz 1mariejoyceaggabaoNo ratings yet

- Inventories and Related Expenses: Multiple Choice - TheoryDocument14 pagesInventories and Related Expenses: Multiple Choice - TheoryMadielyn Santarin MirandaNo ratings yet

- Merchandise Business Class Performance AnswersDocument14 pagesMerchandise Business Class Performance AnswersLerry RosellNo ratings yet

- Myrna C. Calma, CPA, Ph.D. Associate Professor 1Document11 pagesMyrna C. Calma, CPA, Ph.D. Associate Professor 1Jessica PangilinanNo ratings yet

- General Journal: Date Description PR DebitDocument4 pagesGeneral Journal: Date Description PR DebitBenjaminJrMoroniaNo ratings yet

- Accounting 2 - Teresita BuenaflorDocument14 pagesAccounting 2 - Teresita BuenaflorElmeerajh JudavarNo ratings yet

- FAR AssignmentDocument8 pagesFAR AssignmentpaololegardoNo ratings yet

- Buenaflor WorksheetDocument10 pagesBuenaflor WorksheetRaff LesiaaNo ratings yet

- Prepare Financial Statements Wo AdjDocument4 pagesPrepare Financial Statements Wo Adjnavidasif555No ratings yet

- ActivityDocument49 pagesActivityAshanti ashley gueseNo ratings yet

- Accounting EquationDocument2 pagesAccounting Equationunknown PersonNo ratings yet

- OIS Finals & Answer KeyDocument2 pagesOIS Finals & Answer Keyeianna_05No ratings yet

- VertudezDocument4 pagesVertudezralph yapNo ratings yet

- June 5 June 18 June 23: Sales CollectionDocument3 pagesJune 5 June 18 June 23: Sales CollectionKim FloresNo ratings yet

- Module 2Document11 pagesModule 2Deanne LumakangNo ratings yet

- AlferezDocument1 pageAlfereza.alferez.142838.tcNo ratings yet

- 61oq678rf - CD - CHAPTER 10 - ACCTG CYCLE OF A MERCHANDISING BUSINESSDocument17 pages61oq678rf - CD - CHAPTER 10 - ACCTG CYCLE OF A MERCHANDISING BUSINESSLyra Mae De BotonNo ratings yet

- 61oq678rf - CD - Chapter 10 - Acctg Cycle of A Merchandising BusinessDocument17 pages61oq678rf - CD - Chapter 10 - Acctg Cycle of A Merchandising BusinessLyra Mae De BotonNo ratings yet

- Castro Company ZABALLADocument11 pagesCastro Company ZABALLAHelping Five (H5)No ratings yet

- Activity Review StatementDocument5 pagesActivity Review Statementangel ciiiNo ratings yet

- Audit of Inventory: Download NowDocument1 pageAudit of Inventory: Download NowMariz Julian Pang-aoNo ratings yet

- Lecture Discussion On Worksheet Preparation To Post Closing Trial Balance November 092020Document18 pagesLecture Discussion On Worksheet Preparation To Post Closing Trial Balance November 092020Garp BarrocaNo ratings yet

- Lecture - Discussion On Worksheet Preparation To Post Closing Trial BalanceDocument16 pagesLecture - Discussion On Worksheet Preparation To Post Closing Trial BalanceGarp BarrocaNo ratings yet

- Chapter 10 Accounting Cycle of A Merchandising BusinessDocument37 pagesChapter 10 Accounting Cycle of A Merchandising BusinessArlyn Ragudos BSA1No ratings yet

- 01 Elms Activity 2 Ia3Document1 page01 Elms Activity 2 Ia3Jen DeloyNo ratings yet

- Bsa Midterm Graded Exercises From Worksheet To Financial Statements FinalDocument4 pagesBsa Midterm Graded Exercises From Worksheet To Financial Statements FinalGarp BarrocaNo ratings yet

- AccountancyDocument16 pagesAccountancyevangiebalunsat9No ratings yet

- UASDocument2 pagesUASMuhammad Agil FadilahNo ratings yet

- Ex 3-Jounal (Periodic)Document14 pagesEx 3-Jounal (Periodic)yeshaNo ratings yet

- Merchandising JE and ISDocument5 pagesMerchandising JE and ISAGATHA REINNo ratings yet

- Any 20 Transactions of A Company (PGPMX2022-24, Batch 1, Avinash Sharma)Document7 pagesAny 20 Transactions of A Company (PGPMX2022-24, Batch 1, Avinash Sharma)Gaurav HiraniNo ratings yet

- Bsa Midterm Non Graded Exercises Worksheet and Financial Statements Preparation Answer KeyDocument7 pagesBsa Midterm Non Graded Exercises Worksheet and Financial Statements Preparation Answer KeyGarp BarrocaNo ratings yet

- Acc 1 - Financial Accounting and Reporting QUIZ NO. 15 - Accounting Cycle of A Merchandising Business (Application)Document1 pageAcc 1 - Financial Accounting and Reporting QUIZ NO. 15 - Accounting Cycle of A Merchandising Business (Application)nicole bancoroNo ratings yet

- Comprehensive Problem 1 SolutionDocument20 pagesComprehensive Problem 1 SolutionRJ 1100% (1)

- FS MerchandisingDocument14 pagesFS MerchandisingDesirre TransonaNo ratings yet

- MidtermDocument11 pagesMidtermdumpanonymouslyNo ratings yet

- Chapter 10 Accounting Cycle of A Merchandising BusinessDocument40 pagesChapter 10 Accounting Cycle of A Merchandising BusinessOmelkhair YahyaNo ratings yet

- Inventories&Inventoryestimation GAPASINAODocument25 pagesInventories&Inventoryestimation GAPASINAOGerly GapasinaoNo ratings yet

- Riska Kartika Marufa Ginting - Soal Lanjutan Hal 337Document15 pagesRiska Kartika Marufa Ginting - Soal Lanjutan Hal 337Riska GintingNo ratings yet

- Merchsample 2Document14 pagesMerchsample 2LAZARO III DILEMNo ratings yet

- Mortel-BSA1202 (Inventories)Document5 pagesMortel-BSA1202 (Inventories)Aphol Joyce MortelNo ratings yet

- Mortel Bsa1202 Inventories PDF FreeDocument5 pagesMortel Bsa1202 Inventories PDF FreexicoyiNo ratings yet

- Mortel Bsa1202 Inventories PDF FreeDocument5 pagesMortel Bsa1202 Inventories PDF FreexicoyiNo ratings yet

- Statement of Comprehensive IncomeDocument4 pagesStatement of Comprehensive Incomezacharaya abegailNo ratings yet

- Comprehensive Problem For Merchandising OperationsDocument8 pagesComprehensive Problem For Merchandising OperationsSam Rae LimNo ratings yet

- Teresita Buenaflor Shoes 5 PDF FreeDocument19 pagesTeresita Buenaflor Shoes 5 PDF FreeAlexandrea San Buenaventura Baay100% (1)

- Wealth Management Planning: The UK Tax PrinciplesFrom EverandWealth Management Planning: The UK Tax PrinciplesRating: 4.5 out of 5 stars4.5/5 (2)

- CVP - FinalDocument4 pagesCVP - FinalRhandy OyaoNo ratings yet

- Regine QuantiDocument3 pagesRegine QuantiRhandy OyaoNo ratings yet

- Analyzing and JournalizingDocument12 pagesAnalyzing and JournalizingRhandy OyaoNo ratings yet

- Adjusting EntriesDocument14 pagesAdjusting EntriesRhandy OyaoNo ratings yet

- Completed PCB10 HandoutsDocument1,196 pagesCompleted PCB10 Handoutsjevinthomas420No ratings yet

- Main - Economics Edexcel Notes ChapterwseDocument67 pagesMain - Economics Edexcel Notes Chapterwse7a4374 hisNo ratings yet

- Artikel Teks Bahasa Inggris Tentang EKONOMI Lengkap Dengan Terjemahan Dan Daftar Kosakata BaruDocument8 pagesArtikel Teks Bahasa Inggris Tentang EKONOMI Lengkap Dengan Terjemahan Dan Daftar Kosakata BaruDewi Ayu SaraswatiNo ratings yet

- Cultures DiscovermentsDocument5 pagesCultures DiscovermentsMurilo Zulian CollaNo ratings yet

- FDNECON NotesDocument4 pagesFDNECON Notesneo leeNo ratings yet

- Brokerlist 20221220125918Document13,631 pagesBrokerlist 20221220125918Ashutosh ChaturvediNo ratings yet

- 10 Currency MarketsDocument10 pages10 Currency MarketsNicole Daphne FigueroaNo ratings yet

- VAT Accounting Computation and Double EntryDocument31 pagesVAT Accounting Computation and Double EntryEdewo James JeremiahNo ratings yet

- Atp Assv1 Pl72888213 LetterDocument1 pageAtp Assv1 Pl72888213 LetterNarin SangrungNo ratings yet

- Permintaan Approved Client Talang Air JO.14 CVDocument12 pagesPermintaan Approved Client Talang Air JO.14 CVTolol BegoNo ratings yet

- Incoterms and Stowage - ExercisesDocument1 pageIncoterms and Stowage - ExercisesErika Gonzalez100% (1)

- Naveen State Bank of India Acc StatementDocument26 pagesNaveen State Bank of India Acc StatementSRV MOTORSSNo ratings yet

- 0262025256.MIT Press - Mario I. Blejer, Marko Skreb (Editors) .Markets, Financial Policies in Emerging - May.1999Document265 pages0262025256.MIT Press - Mario I. Blejer, Marko Skreb (Editors) .Markets, Financial Policies in Emerging - May.1999Branko NikolicNo ratings yet

- Import & Export ProcedureDocument17 pagesImport & Export ProcedureKrishan BhardwajNo ratings yet

- Financial Ratios - Non Financial Sector-May 22Document8 pagesFinancial Ratios - Non Financial Sector-May 22SoubhikNo ratings yet

- Lifelines of National EconomyDocument14 pagesLifelines of National EconomyUnicomp ComputerNo ratings yet

- Merchandising Handout - Perpetual Vs PeriodicDocument1 pageMerchandising Handout - Perpetual Vs PeriodicTineNo ratings yet

- Monetary Policy and The Federal Reserve System: ObjectivesDocument25 pagesMonetary Policy and The Federal Reserve System: ObjectivesKamal HossainNo ratings yet

- 2.1.2 As External FinanceDocument49 pages2.1.2 As External FinanceEhtesham UmerNo ratings yet

- Lembar Soal Ukk 2016-2017 Kls XiDocument3 pagesLembar Soal Ukk 2016-2017 Kls Xialif fajriNo ratings yet

- Pesco Online BillDocument1 pagePesco Online Billta5745219No ratings yet

- Adobe Scan 01042021 - CompressedDocument6 pagesAdobe Scan 01042021 - CompressedKartik ShuklaNo ratings yet

- Quiz 2 Lecturer - Answer - Accounting and FinanceDocument5 pagesQuiz 2 Lecturer - Answer - Accounting and FinancehenryNo ratings yet

- LM Business Math - Q1 W6 - MELC3 Module 8Document15 pagesLM Business Math - Q1 W6 - MELC3 Module 8Cristina C MarianoNo ratings yet

- Hele 4 Lesson 2 Business Opportunities in The CommunityDocument19 pagesHele 4 Lesson 2 Business Opportunities in The CommunityTimotheus Raemer De GuzmanNo ratings yet

- Agenda Item 2 (2) - ITC RulesDocument9 pagesAgenda Item 2 (2) - ITC Rulesfintech ConsultancyNo ratings yet

Download as xlsx, pdf, or txt

You might also like

- Icici Bank StatementDocument22 pagesIcici Bank StatementVIJAY BHASAKAR100% (1)

- Nedbank Statement Nov2023Document36 pagesNedbank Statement Nov2023ernest.mmilaNo ratings yet

- Chapter 1-Introduction To The World of RetailingDocument29 pagesChapter 1-Introduction To The World of RetailingAshaAnwar83% (6)

- Sol. Man. - Chapter 10 - Acctg Cycle of A Merchandising BusinessDocument65 pagesSol. Man. - Chapter 10 - Acctg Cycle of A Merchandising BusinessPeter Piper67% (3)

- Journalizing Merchandising Transactions, Problem #13Document2 pagesJournalizing Merchandising Transactions, Problem #13Feiya Liu80% (10)

- The McGraw-Hill 36-Hour Course: Finance for Non-Financial Managers 3/EFrom EverandThe McGraw-Hill 36-Hour Course: Finance for Non-Financial Managers 3/ERating: 4.5 out of 5 stars4.5/5 (6)

- Task 5Document9 pagesTask 5Honey TolentinoNo ratings yet

- Alternate Demonstration Problem MerchandisingDocument5 pagesAlternate Demonstration Problem MerchandisingmoNo ratings yet

- Answer InventoryDocument7 pagesAnswer InventoryAllen Carl60% (5)

- Sallys Struthers - Answer KeyDocument7 pagesSallys Struthers - Answer KeyLlyod Francis LaylayNo ratings yet

- 6th Sem Project ReportDocument93 pages6th Sem Project ReportSwati Kataria67% (3)

- Chapter 7 Problems: Problem #14 P. 7-57 Problem #15 P. 7-58Document3 pagesChapter 7 Problems: Problem #14 P. 7-57 Problem #15 P. 7-58Zyrene Kei ReyesNo ratings yet

- Review Quiz Inter1Document9 pagesReview Quiz Inter1Vanessa vnssNo ratings yet

- Latihan Siklus Dagang 1Document26 pagesLatihan Siklus Dagang 1AFIFA SAQIFANo ratings yet

- Lec Merchandising Perpetual PeriodicDocument8 pagesLec Merchandising Perpetual PeriodicAiddan Clark De JesusNo ratings yet

- Midterms FAR Quiz 1Document15 pagesMidterms FAR Quiz 1mariejoyceaggabaoNo ratings yet

- Inventories and Related Expenses: Multiple Choice - TheoryDocument14 pagesInventories and Related Expenses: Multiple Choice - TheoryMadielyn Santarin MirandaNo ratings yet

- Merchandise Business Class Performance AnswersDocument14 pagesMerchandise Business Class Performance AnswersLerry RosellNo ratings yet

- Myrna C. Calma, CPA, Ph.D. Associate Professor 1Document11 pagesMyrna C. Calma, CPA, Ph.D. Associate Professor 1Jessica PangilinanNo ratings yet

- General Journal: Date Description PR DebitDocument4 pagesGeneral Journal: Date Description PR DebitBenjaminJrMoroniaNo ratings yet

- Accounting 2 - Teresita BuenaflorDocument14 pagesAccounting 2 - Teresita BuenaflorElmeerajh JudavarNo ratings yet

- FAR AssignmentDocument8 pagesFAR AssignmentpaololegardoNo ratings yet

- Buenaflor WorksheetDocument10 pagesBuenaflor WorksheetRaff LesiaaNo ratings yet

- Prepare Financial Statements Wo AdjDocument4 pagesPrepare Financial Statements Wo Adjnavidasif555No ratings yet

- ActivityDocument49 pagesActivityAshanti ashley gueseNo ratings yet

- Accounting EquationDocument2 pagesAccounting Equationunknown PersonNo ratings yet

- OIS Finals & Answer KeyDocument2 pagesOIS Finals & Answer Keyeianna_05No ratings yet

- VertudezDocument4 pagesVertudezralph yapNo ratings yet

- June 5 June 18 June 23: Sales CollectionDocument3 pagesJune 5 June 18 June 23: Sales CollectionKim FloresNo ratings yet

- Module 2Document11 pagesModule 2Deanne LumakangNo ratings yet

- AlferezDocument1 pageAlfereza.alferez.142838.tcNo ratings yet

- 61oq678rf - CD - CHAPTER 10 - ACCTG CYCLE OF A MERCHANDISING BUSINESSDocument17 pages61oq678rf - CD - CHAPTER 10 - ACCTG CYCLE OF A MERCHANDISING BUSINESSLyra Mae De BotonNo ratings yet

- 61oq678rf - CD - Chapter 10 - Acctg Cycle of A Merchandising BusinessDocument17 pages61oq678rf - CD - Chapter 10 - Acctg Cycle of A Merchandising BusinessLyra Mae De BotonNo ratings yet

- Castro Company ZABALLADocument11 pagesCastro Company ZABALLAHelping Five (H5)No ratings yet

- Activity Review StatementDocument5 pagesActivity Review Statementangel ciiiNo ratings yet

- Audit of Inventory: Download NowDocument1 pageAudit of Inventory: Download NowMariz Julian Pang-aoNo ratings yet

- Lecture Discussion On Worksheet Preparation To Post Closing Trial Balance November 092020Document18 pagesLecture Discussion On Worksheet Preparation To Post Closing Trial Balance November 092020Garp BarrocaNo ratings yet

- Lecture - Discussion On Worksheet Preparation To Post Closing Trial BalanceDocument16 pagesLecture - Discussion On Worksheet Preparation To Post Closing Trial BalanceGarp BarrocaNo ratings yet

- Chapter 10 Accounting Cycle of A Merchandising BusinessDocument37 pagesChapter 10 Accounting Cycle of A Merchandising BusinessArlyn Ragudos BSA1No ratings yet

- 01 Elms Activity 2 Ia3Document1 page01 Elms Activity 2 Ia3Jen DeloyNo ratings yet

- Bsa Midterm Graded Exercises From Worksheet To Financial Statements FinalDocument4 pagesBsa Midterm Graded Exercises From Worksheet To Financial Statements FinalGarp BarrocaNo ratings yet

- AccountancyDocument16 pagesAccountancyevangiebalunsat9No ratings yet

- UASDocument2 pagesUASMuhammad Agil FadilahNo ratings yet

- Ex 3-Jounal (Periodic)Document14 pagesEx 3-Jounal (Periodic)yeshaNo ratings yet

- Merchandising JE and ISDocument5 pagesMerchandising JE and ISAGATHA REINNo ratings yet

- Any 20 Transactions of A Company (PGPMX2022-24, Batch 1, Avinash Sharma)Document7 pagesAny 20 Transactions of A Company (PGPMX2022-24, Batch 1, Avinash Sharma)Gaurav HiraniNo ratings yet

- Bsa Midterm Non Graded Exercises Worksheet and Financial Statements Preparation Answer KeyDocument7 pagesBsa Midterm Non Graded Exercises Worksheet and Financial Statements Preparation Answer KeyGarp BarrocaNo ratings yet

- Acc 1 - Financial Accounting and Reporting QUIZ NO. 15 - Accounting Cycle of A Merchandising Business (Application)Document1 pageAcc 1 - Financial Accounting and Reporting QUIZ NO. 15 - Accounting Cycle of A Merchandising Business (Application)nicole bancoroNo ratings yet

- Comprehensive Problem 1 SolutionDocument20 pagesComprehensive Problem 1 SolutionRJ 1100% (1)

- FS MerchandisingDocument14 pagesFS MerchandisingDesirre TransonaNo ratings yet

- MidtermDocument11 pagesMidtermdumpanonymouslyNo ratings yet

- Chapter 10 Accounting Cycle of A Merchandising BusinessDocument40 pagesChapter 10 Accounting Cycle of A Merchandising BusinessOmelkhair YahyaNo ratings yet

- Inventories&Inventoryestimation GAPASINAODocument25 pagesInventories&Inventoryestimation GAPASINAOGerly GapasinaoNo ratings yet

- Riska Kartika Marufa Ginting - Soal Lanjutan Hal 337Document15 pagesRiska Kartika Marufa Ginting - Soal Lanjutan Hal 337Riska GintingNo ratings yet

- Merchsample 2Document14 pagesMerchsample 2LAZARO III DILEMNo ratings yet

- Mortel-BSA1202 (Inventories)Document5 pagesMortel-BSA1202 (Inventories)Aphol Joyce MortelNo ratings yet

- Mortel Bsa1202 Inventories PDF FreeDocument5 pagesMortel Bsa1202 Inventories PDF FreexicoyiNo ratings yet

- Mortel Bsa1202 Inventories PDF FreeDocument5 pagesMortel Bsa1202 Inventories PDF FreexicoyiNo ratings yet

- Statement of Comprehensive IncomeDocument4 pagesStatement of Comprehensive Incomezacharaya abegailNo ratings yet

- Comprehensive Problem For Merchandising OperationsDocument8 pagesComprehensive Problem For Merchandising OperationsSam Rae LimNo ratings yet

- Teresita Buenaflor Shoes 5 PDF FreeDocument19 pagesTeresita Buenaflor Shoes 5 PDF FreeAlexandrea San Buenaventura Baay100% (1)

- Wealth Management Planning: The UK Tax PrinciplesFrom EverandWealth Management Planning: The UK Tax PrinciplesRating: 4.5 out of 5 stars4.5/5 (2)

- CVP - FinalDocument4 pagesCVP - FinalRhandy OyaoNo ratings yet

- Regine QuantiDocument3 pagesRegine QuantiRhandy OyaoNo ratings yet

- Analyzing and JournalizingDocument12 pagesAnalyzing and JournalizingRhandy OyaoNo ratings yet

- Adjusting EntriesDocument14 pagesAdjusting EntriesRhandy OyaoNo ratings yet

- Completed PCB10 HandoutsDocument1,196 pagesCompleted PCB10 Handoutsjevinthomas420No ratings yet

- Main - Economics Edexcel Notes ChapterwseDocument67 pagesMain - Economics Edexcel Notes Chapterwse7a4374 hisNo ratings yet

- Artikel Teks Bahasa Inggris Tentang EKONOMI Lengkap Dengan Terjemahan Dan Daftar Kosakata BaruDocument8 pagesArtikel Teks Bahasa Inggris Tentang EKONOMI Lengkap Dengan Terjemahan Dan Daftar Kosakata BaruDewi Ayu SaraswatiNo ratings yet

- Cultures DiscovermentsDocument5 pagesCultures DiscovermentsMurilo Zulian CollaNo ratings yet

- FDNECON NotesDocument4 pagesFDNECON Notesneo leeNo ratings yet

- Brokerlist 20221220125918Document13,631 pagesBrokerlist 20221220125918Ashutosh ChaturvediNo ratings yet

- 10 Currency MarketsDocument10 pages10 Currency MarketsNicole Daphne FigueroaNo ratings yet

- VAT Accounting Computation and Double EntryDocument31 pagesVAT Accounting Computation and Double EntryEdewo James JeremiahNo ratings yet

- Atp Assv1 Pl72888213 LetterDocument1 pageAtp Assv1 Pl72888213 LetterNarin SangrungNo ratings yet

- Permintaan Approved Client Talang Air JO.14 CVDocument12 pagesPermintaan Approved Client Talang Air JO.14 CVTolol BegoNo ratings yet

- Incoterms and Stowage - ExercisesDocument1 pageIncoterms and Stowage - ExercisesErika Gonzalez100% (1)

- Naveen State Bank of India Acc StatementDocument26 pagesNaveen State Bank of India Acc StatementSRV MOTORSSNo ratings yet

- 0262025256.MIT Press - Mario I. Blejer, Marko Skreb (Editors) .Markets, Financial Policies in Emerging - May.1999Document265 pages0262025256.MIT Press - Mario I. Blejer, Marko Skreb (Editors) .Markets, Financial Policies in Emerging - May.1999Branko NikolicNo ratings yet

- Import & Export ProcedureDocument17 pagesImport & Export ProcedureKrishan BhardwajNo ratings yet

- Financial Ratios - Non Financial Sector-May 22Document8 pagesFinancial Ratios - Non Financial Sector-May 22SoubhikNo ratings yet

- Lifelines of National EconomyDocument14 pagesLifelines of National EconomyUnicomp ComputerNo ratings yet

- Merchandising Handout - Perpetual Vs PeriodicDocument1 pageMerchandising Handout - Perpetual Vs PeriodicTineNo ratings yet

- Monetary Policy and The Federal Reserve System: ObjectivesDocument25 pagesMonetary Policy and The Federal Reserve System: ObjectivesKamal HossainNo ratings yet

- 2.1.2 As External FinanceDocument49 pages2.1.2 As External FinanceEhtesham UmerNo ratings yet

- Lembar Soal Ukk 2016-2017 Kls XiDocument3 pagesLembar Soal Ukk 2016-2017 Kls Xialif fajriNo ratings yet

- Pesco Online BillDocument1 pagePesco Online Billta5745219No ratings yet

- Adobe Scan 01042021 - CompressedDocument6 pagesAdobe Scan 01042021 - CompressedKartik ShuklaNo ratings yet

- Quiz 2 Lecturer - Answer - Accounting and FinanceDocument5 pagesQuiz 2 Lecturer - Answer - Accounting and FinancehenryNo ratings yet

- LM Business Math - Q1 W6 - MELC3 Module 8Document15 pagesLM Business Math - Q1 W6 - MELC3 Module 8Cristina C MarianoNo ratings yet

- Hele 4 Lesson 2 Business Opportunities in The CommunityDocument19 pagesHele 4 Lesson 2 Business Opportunities in The CommunityTimotheus Raemer De GuzmanNo ratings yet

- Agenda Item 2 (2) - ITC RulesDocument9 pagesAgenda Item 2 (2) - ITC Rulesfintech ConsultancyNo ratings yet