Download as pdf or txt

You might also like

- EPB Lakeview Lodge FNDocument50 pagesEPB Lakeview Lodge FNSimon Tembo100% (1)

- Fact Sheet-CANSLIM PDFDocument4 pagesFact Sheet-CANSLIM PDFAmirul HafizNo ratings yet

- Energy Management Handbook - 6th EditionDocument11 pagesEnergy Management Handbook - 6th EditionmerinaNo ratings yet

- Mineral Asset Valuation James - GilbertsonDocument15 pagesMineral Asset Valuation James - GilbertsonCalitoo IGNo ratings yet

- Kotak Business Cycle Fund Product LeafletDocument4 pagesKotak Business Cycle Fund Product Leafletrohitis_me2169No ratings yet

- WH Tis ?: Fundamental Analysis A Fundamental AnalysisDocument7 pagesWH Tis ?: Fundamental Analysis A Fundamental AnalysisAbhinandan ChatterjeeNo ratings yet

- 4 Trades and FinanceDocument37 pages4 Trades and Financevuong ngaNo ratings yet

- BA449 Chap 005Document50 pagesBA449 Chap 005mashalerahNo ratings yet

- Derby Management: Sales Force Size and Territory Alignment ProcessDocument17 pagesDerby Management: Sales Force Size and Territory Alignment Processanon_162166416No ratings yet

- BR Cashflow Jul2020 D2Document11 pagesBR Cashflow Jul2020 D2TheCuriousMindNo ratings yet

- International Financial Statement Analysis: BU7504 Trinity Business School Caroline Kirrane, CFA, MBADocument31 pagesInternational Financial Statement Analysis: BU7504 Trinity Business School Caroline Kirrane, CFA, MBAJingquan (Adele) ZhaoNo ratings yet

- Corporate Risk ManagementDocument8 pagesCorporate Risk ManagementMontserrat DelgadoNo ratings yet

- 4.financial Statement AnalysisDocument54 pages4.financial Statement Analysisyadavbhauk30No ratings yet

- SPE Introduction To E&P Petroleum Economics & Commercial: November 28, 2019 Lamé VerreDocument43 pagesSPE Introduction To E&P Petroleum Economics & Commercial: November 28, 2019 Lamé Verrejhon berez223344No ratings yet

- Outsourcing Slideshow MasterDocument39 pagesOutsourcing Slideshow MasterJames BondNo ratings yet

- Comprehensive Finance Cheat Sheet Collection 1698244606Document52 pagesComprehensive Finance Cheat Sheet Collection 1698244606muratgreywolf100% (1)

- BNA SWIFT For SecuritiesDocument16 pagesBNA SWIFT For SecuritiesTelmo CabetoNo ratings yet

- Profitability AnalysisDocument23 pagesProfitability Analysismmaria.salmannNo ratings yet

- Andrew NjobaDocument33 pagesAndrew NjobaSemeeeJuniorNo ratings yet

- Oracle E-Business Suite:: Eliminate Promotional Fund Management Headaches With Channel Revenue ManagementDocument19 pagesOracle E-Business Suite:: Eliminate Promotional Fund Management Headaches With Channel Revenue ManagementMajidMahmoodNo ratings yet

- Axis Business Cycle Fund NFO-LEAFLETDocument2 pagesAxis Business Cycle Fund NFO-LEAFLETamarnathb2001No ratings yet

- Presentation Financial Risk ManagementDocument33 pagesPresentation Financial Risk ManagementDeniz OnalNo ratings yet

- Cross-Border M&A Valuation - Issues: Jayasimha P Director - Investment BankingDocument17 pagesCross-Border M&A Valuation - Issues: Jayasimha P Director - Investment Bankingmansavi bihaniNo ratings yet

- 6 Economics 1 PDFDocument44 pages6 Economics 1 PDFjhon berez223344No ratings yet

- Management ProjectDocument21 pagesManagement ProjectShivam KapoorNo ratings yet

- IREF IV Brochure June 19 - 6 PagerDocument6 pagesIREF IV Brochure June 19 - 6 PagerSandyNo ratings yet

- CygnusDocument34 pagesCygnuskskumarr100% (1)

- EsourcingDocument37 pagesEsourcingsarin15juneNo ratings yet

- Comprehansive Process. TamerDocument2 pagesComprehansive Process. TamerMarco IbrahimNo ratings yet

- L0193 Neuberger Berman Profile EmeaDocument4 pagesL0193 Neuberger Berman Profile EmeaBenz Lystin Carcuevas YbañezNo ratings yet

- External Environment ANALYSIS (Competitive Analysis)Document13 pagesExternal Environment ANALYSIS (Competitive Analysis)Putri AnisaNo ratings yet

- FIN - Chap 4 - Analyzing Financial StatementsDocument1 pageFIN - Chap 4 - Analyzing Financial Statementsduyennthds170525No ratings yet

- W2 WCorporateDocument14 pagesW2 WCorporateWay2 WealthNo ratings yet

- Business Requirements For The IT Strategy (Zurich, Euroforum, 27 August 2008)Document24 pagesBusiness Requirements For The IT Strategy (Zurich, Euroforum, 27 August 2008)rsieb100% (1)

- IUBAV - Lecture 4 - Module 2 Financial Ratios Analysis and Market Tests (S1 2023 2024)Document27 pagesIUBAV - Lecture 4 - Module 2 Financial Ratios Analysis and Market Tests (S1 2023 2024)nguyengianhi1913316118No ratings yet

- ALM Life InsuranceDocument22 pagesALM Life InsuranceIbnu NugrohoNo ratings yet

- CH 4 - Trade Cycles - NOTESDocument12 pagesCH 4 - Trade Cycles - NOTESHarini MudaliyarNo ratings yet

- FINANCIAL MANAGEMENT MODULE 1 6 1st MeetingDocument69 pagesFINANCIAL MANAGEMENT MODULE 1 6 1st MeetingMarriel Fate CullanoNo ratings yet

- 03fulfillment CostingDocument22 pages03fulfillment Costingsujit nayakNo ratings yet

- ICAI Jan 30 2016Document34 pagesICAI Jan 30 2016Devasish Parmar100% (1)

- Building Wealth2018 JTBDocument34 pagesBuilding Wealth2018 JTBNicole OfalsaNo ratings yet

- Economic EvaluationDocument17 pagesEconomic Evaluationadryan castroNo ratings yet

- Palm Oil: Supply DemandDocument5 pagesPalm Oil: Supply DemandMudit ChauhanNo ratings yet

- Morningstar Equities Research MethodologyDocument2 pagesMorningstar Equities Research Methodologykanika sengarNo ratings yet

- Transaction ManagementDocument58 pagesTransaction ManagementhalimabiNo ratings yet

- Alternate Funding Solution For Life Insurers?: Paul CaputoDocument16 pagesAlternate Funding Solution For Life Insurers?: Paul CaputorobcannonNo ratings yet

- IMB Imperial Brands 2018Document36 pagesIMB Imperial Brands 2018Ala BasterNo ratings yet

- Strategic Cost ManagementDocument11 pagesStrategic Cost ManagementSanjay ShrivastavNo ratings yet

- FrameworksDocument13 pagesFrameworksShonit ChamadiaNo ratings yet

- 2 - TICMI-MPE-Mekanisme Perdagangan Efek Merged 13012018 PDFDocument53 pages2 - TICMI-MPE-Mekanisme Perdagangan Efek Merged 13012018 PDFVinco EvertNo ratings yet

- GTM TradingExpensesDocument19 pagesGTM TradingExpensesDmitry PopovNo ratings yet

- Cfa TopicsDocument1 pageCfa Topicshanzenda2511No ratings yet

- Problems On Profit Prior To IncorporationDocument18 pagesProblems On Profit Prior To Incorporationcsneha0803No ratings yet

- YL Digital Banking OverviewDocument11 pagesYL Digital Banking OverviewAbdul SyedNo ratings yet

- Financial Forecast: Nelson Mandela Bay StadiumDocument7 pagesFinancial Forecast: Nelson Mandela Bay StadiumFooyNo ratings yet

- Optimizing Manufacturing Operations Using Big Data and AnalyticsDocument39 pagesOptimizing Manufacturing Operations Using Big Data and AnalyticsWisnu AjiNo ratings yet

- Finance Modeling Handbook (00000002)Document1 pageFinance Modeling Handbook (00000002)baronfgfNo ratings yet

- Trade Receivables Discounting System - M1 ExchangeDocument14 pagesTrade Receivables Discounting System - M1 ExchangeM1 ExchangeNo ratings yet

- Investment Banking: Summers PreparationDocument31 pagesInvestment Banking: Summers PreparationManu JanardananNo ratings yet

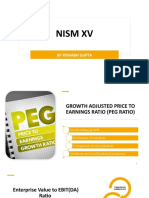

- Nism XV - RG (191-197)Document7 pagesNism XV - RG (191-197)Rishabh R. GuptaNo ratings yet

- TUM Forum SustainabilityDocument126 pagesTUM Forum SustainabilityJesús CastellanosNo ratings yet

- 7 2022 - Gas Grid Training (Part 1) FluxysDocument41 pages7 2022 - Gas Grid Training (Part 1) FluxysJesús CastellanosNo ratings yet

- 6 Energy Aggregators As New Market Players 2022-03-30 - KU Leuven (Flexcity:Veolia)Document62 pages6 Energy Aggregators As New Market Players 2022-03-30 - KU Leuven (Flexcity:Veolia)Jesús CastellanosNo ratings yet

- 5 Evolution of Electricity Market Regulation - March2022 LMeeus (VBS)Document63 pages5 Evolution of Electricity Market Regulation - March2022 LMeeus (VBS)Jesús CastellanosNo ratings yet

- 4 20220309 - KULeuven - The DSO in The Energy Market (Fluvius)Document64 pages4 20220309 - KULeuven - The DSO in The Energy Market (Fluvius)Jesús CastellanosNo ratings yet

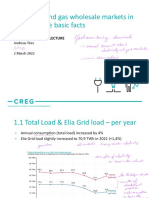

- 3 220302 KULeuven Gastles FBMC - ATI AMA (CREG)Document50 pages3 220302 KULeuven Gastles FBMC - ATI AMA (CREG)Jesús CastellanosNo ratings yet

- 1 Electricity and Gas Markets 2022 - v2 (Delarue)Document29 pages1 Electricity and Gas Markets 2022 - v2 (Delarue)Jesús CastellanosNo ratings yet

- 3 220302 E&G Flash Monitoring 2021 - KULeuven - ATI (CREG)Document18 pages3 220302 E&G Flash Monitoring 2021 - KULeuven - ATI (CREG)Jesús CastellanosNo ratings yet

- ABB Patent TRAVELING WAVE BASED FAULT LOCATION USING UNSYNCHRONIZED MEASUREMENTS FOR TRANSMISSION LINES US11204382Document15 pagesABB Patent TRAVELING WAVE BASED FAULT LOCATION USING UNSYNCHRONIZED MEASUREMENTS FOR TRANSMISSION LINES US11204382Jesús CastellanosNo ratings yet

- SEL Patent TIME-DOMAIN DIRECTIONAL LINE PROTECTION OF ELECTRIC POWER DELIVERY SYSTEMS US20170082675A1Document29 pagesSEL Patent TIME-DOMAIN DIRECTIONAL LINE PROTECTION OF ELECTRIC POWER DELIVERY SYSTEMS US20170082675A1Jesús CastellanosNo ratings yet

- HN4Unit 2 Vocab ADocument3 pagesHN4Unit 2 Vocab AAnna NowakowskaNo ratings yet

- Notes ICSEClass 10 Chemistry Organic ChemistryDocument5 pagesNotes ICSEClass 10 Chemistry Organic Chemistryvenuspoliston123No ratings yet

- Us4207124 PDFDocument3 pagesUs4207124 PDFchecolonoskiNo ratings yet

- Lecture - 5 ExamplesDocument26 pagesLecture - 5 ExamplesDimas Angga100% (7)

- Conservation of EnergyDocument8 pagesConservation of EnergySasankBabuNo ratings yet

- Cosmos Carl SaganDocument18 pagesCosmos Carl SaganRabia AbdullahNo ratings yet

- Smectites 1212335219716023 8Document30 pagesSmectites 1212335219716023 8mantillawilliamNo ratings yet

- Importance of TreesDocument1 pageImportance of Treesvision2010jobNo ratings yet

- Physical Science Week 3Document9 pagesPhysical Science Week 3Rona Grace MartinezNo ratings yet

- PDF Book 3 Connection TRBDocument109 pagesPDF Book 3 Connection TRBsinansec.schoolNo ratings yet

- Explorer 3-Natural Disasters Vocab Sheet PDFDocument4 pagesExplorer 3-Natural Disasters Vocab Sheet PDFLucy100% (1)

- Cape Chemistry Unit 1 Paper 2 - May 2011Document9 pagesCape Chemistry Unit 1 Paper 2 - May 2011asjawolverine100% (8)

- ENVI SCI SAS Day 8.Document7 pagesENVI SCI SAS Day 8.jl sanchezNo ratings yet

- Biology Lesson Note For Grade 11Document3 pagesBiology Lesson Note For Grade 11Milkias BerhanuNo ratings yet

- Travel Through SpainDocument491 pagesTravel Through SpainFrancisco Javier SpínolaNo ratings yet

- Natural ResourcsDocument20 pagesNatural Resourcsdinesh rokkaNo ratings yet

- Project Report On Effect of LEACHATE On The Engineering Properties of The SoilDocument91 pagesProject Report On Effect of LEACHATE On The Engineering Properties of The SoilShashank Singh100% (6)

- X-Ray Crystallography X-RayDocument10 pagesX-Ray Crystallography X-RayJoriel SolenonNo ratings yet

- Science JHS 1 - 1Document5 pagesScience JHS 1 - 1stanleyaklikaNo ratings yet

- Wind Turbine Tower Collapse Cases - A Historical OverviewDocument9 pagesWind Turbine Tower Collapse Cases - A Historical OverviewJoaquim TchamoNo ratings yet

- Nano Ice CreamDocument5 pagesNano Ice Creamapi-288531740No ratings yet

- Economics of Power GenerationDocument18 pagesEconomics of Power Generationaymanabboouds100% (1)

- Energy Conservation Building Code (ECBC) Compliance and Beyond A Pilot StudyDocument48 pagesEnergy Conservation Building Code (ECBC) Compliance and Beyond A Pilot Studyemraan KhanNo ratings yet

- 4AV.3.24 PaperDocument4 pages4AV.3.24 Papermohammed umarNo ratings yet

- As Test 04Document6 pagesAs Test 04LearnchemNo ratings yet

- Literature Review On Solar Irrigation SystemDocument5 pagesLiterature Review On Solar Irrigation Systemc5sx83ws100% (1)

- Wossen MillionDocument187 pagesWossen MillionRebi HamzaNo ratings yet

- ElectrostaticDocument3 pagesElectrostaticPrincess Roan RobertoNo ratings yet