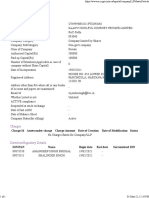

CRA Investment Accounting Theory

CRA Investment Accounting Theory

You might also like

- Question - Chapter 2Document17 pagesQuestion - Chapter 2Mạnh Đỗ ĐứcNo ratings yet

- Accounting For Ijarah and Ijarah MuntahiaDocument12 pagesAccounting For Ijarah and Ijarah Muntahiatheintelligentgirl100% (1)

- Class 12 Accounts Notes Chapter 9 Studyguide360Document19 pagesClass 12 Accounts Notes Chapter 9 Studyguide360Ali ssNo ratings yet

- CA Final FR A MTP 1 May 2024 Castudynotes ComDocument12 pagesCA Final FR A MTP 1 May 2024 Castudynotes Compabitrarijal1227No ratings yet

- P1_FR_May24_MTP1_Solution @CA_Final_LegendDocument16 pagesP1_FR_May24_MTP1_Solution @CA_Final_Legendcontact.hemaamudhaNo ratings yet

- MTP 1 PAPER 1 Answe KeyDocument12 pagesMTP 1 PAPER 1 Answe Keyhitesh YadavNo ratings yet

- C9 Receivable Financing Discounting of Notes ReceivableDocument24 pagesC9 Receivable Financing Discounting of Notes ReceivableAngelie LaxaNo ratings yet

- Topic 3 Issuance, Redemption and Conversion of Loan Instruments Mfrs 7, Mfrs 9, Mfrs 132 (MFRS 17-Effective 1.1.2020)Document86 pagesTopic 3 Issuance, Redemption and Conversion of Loan Instruments Mfrs 7, Mfrs 9, Mfrs 132 (MFRS 17-Effective 1.1.2020)Ainshafiyyah AinshafiyyahNo ratings yet

- Adjusting EntriesDocument10 pagesAdjusting EntriesJezmar John B. GulmaticoNo ratings yet

- Chapter-8 Issue of Debentures: Debenture: The Word Debenture' Has Been Derived From A Latin Word Debere' WhichDocument8 pagesChapter-8 Issue of Debentures: Debenture: The Word Debenture' Has Been Derived From A Latin Word Debere' Whichramandeep kaurNo ratings yet

- Issue of DebenturesDocument23 pagesIssue of Debenturesramandeep kaurNo ratings yet

- LECTURE 7 Accounting For Merchandising Activities Periodic and Perpetual BSAFDocument40 pagesLECTURE 7 Accounting For Merchandising Activities Periodic and Perpetual BSAFShahzad C7No ratings yet

- FR - AnswerDocument12 pagesFR - Answer6dzk78g2vyNo ratings yet

- 8 Cash Flow StatementDocument10 pages8 Cash Flow StatementBAZINGANo ratings yet

- Revenue PrintingDocument19 pagesRevenue Printingayushmaharaj68No ratings yet

- Session 7 - Financial InstrumentsDocument31 pagesSession 7 - Financial InstrumentsMa. Bernadette MontianoNo ratings yet

- Trial Balance: Credit Balances of All Accounts in The Ledger With A View To Test Arithmetical Accuracy of The BooksDocument5 pagesTrial Balance: Credit Balances of All Accounts in The Ledger With A View To Test Arithmetical Accuracy of The BooksPriyanka SharmaNo ratings yet

- Loans ReceivableDocument3 pagesLoans ReceivableDonna ValentinNo ratings yet

- Board Paper-2022-XIDocument8 pagesBoard Paper-2022-XIRn GuptaNo ratings yet

- Amalgamation: 5) (BasicallyDocument11 pagesAmalgamation: 5) (Basicallymadhu peeralaNo ratings yet

- Adobe Scan 13 Oct 2022Document13 pagesAdobe Scan 13 Oct 2022Abhishek SinghNo ratings yet

- Advanced Financial Reporting: Module 4: Final Accounts of Insurance CompaniesDocument23 pagesAdvanced Financial Reporting: Module 4: Final Accounts of Insurance CompaniesBijosh ThomasNo ratings yet

- 1 Intro To LiabilitiesDocument13 pages1 Intro To LiabilitiesPioloNo ratings yet

- IFRS 2 Share Based PaymentDocument19 pagesIFRS 2 Share Based PaymentVikky BehNo ratings yet

- Chapter Three The Balance Sheet and Financial DisclosuresDocument33 pagesChapter Three The Balance Sheet and Financial Disclosuressan marcoNo ratings yet

- Futures Contracts Market: Romanian Commodities ExchangeDocument28 pagesFutures Contracts Market: Romanian Commodities Exchangegriguta99No ratings yet

- Ilovepdf MergedDocument17 pagesIlovepdf Mergednsm2zmvnbbNo ratings yet

- Dr. M. D. Chase Long Beach State University Accounting 500 4A Balance SheetDocument9 pagesDr. M. D. Chase Long Beach State University Accounting 500 4A Balance SheetArtur JastNo ratings yet

- Assets MeasurementsDocument11 pagesAssets MeasurementslllllnubhbhgNo ratings yet

- Issue of DebenturesDocument12 pagesIssue of Debenturessiva883100% (1)

- Week 05 2022 Topic 5 Lecture Leases Part ADocument20 pagesWeek 05 2022 Topic 5 Lecture Leases Part AErnest LeongNo ratings yet

- MATERIALDocument8 pagesMATERIALVatsal ParmarNo ratings yet

- Chapter-5 - FI-BDocument20 pagesChapter-5 - FI-BKhanh LinhNo ratings yet

- Topic: Accounting Cycle of A Service BusinessDocument5 pagesTopic: Accounting Cycle of A Service BusinessJohn Rey BusimeNo ratings yet

- Receivable Financing: 3. Factoring of Accounts Receivable 4. Discounting of Notes ReceivableDocument2 pagesReceivable Financing: 3. Factoring of Accounts Receivable 4. Discounting of Notes ReceivableJonathan NavalloNo ratings yet

- IFA Lesson 3 Slides (Financial Liabilities & Equity)Document53 pagesIFA Lesson 3 Slides (Financial Liabilities & Equity)zengruiqi20000302No ratings yet

- 13 Financial Asset at Amortized CostDocument5 pages13 Financial Asset at Amortized CostLara Jane Dela CruzNo ratings yet

- EA EA1 SU2 OutlineDocument23 pagesEA EA1 SU2 OutlineAashu AntilNo ratings yet

- Part-A Answer To The Question No.1: 1.quick Ratio 1.21 TimesDocument7 pagesPart-A Answer To The Question No.1: 1.quick Ratio 1.21 TimesThe JesterNo ratings yet

- IA1-Continuation PPEDocument13 pagesIA1-Continuation PPEJhunnie LoriaNo ratings yet

- Accounting For Bonds PayableDocument31 pagesAccounting For Bonds PayableJon Christian Miranda100% (2)

- Fundamentals of AccountingDocument27 pagesFundamentals of AccountingMajariya Sahar SabladNo ratings yet

- Module 1 Notes and Loans Receivable PDFDocument43 pagesModule 1 Notes and Loans Receivable PDFALEXA GENMARY GULFAN0% (1)

- P7 - Investment in Debt Securities & Other Non-Current Financial AssetsDocument46 pagesP7 - Investment in Debt Securities & Other Non-Current Financial AssetsNashiel AnneNo ratings yet

- Security Valuation 2 RevisionDocument14 pagesSecurity Valuation 2 RevisionParth joshiNo ratings yet

- Edexcel IGCSE Accounting Student S Book Answers PDFDocument92 pagesEdexcel IGCSE Accounting Student S Book Answers PDFArshad Bashir100% (1)

- Qucik RFR On CL (Sec 123 To 148)Document10 pagesQucik RFR On CL (Sec 123 To 148)visshelp100% (1)

- Chapter 2 Rules of Debit and Credit and General LedgerDocument3 pagesChapter 2 Rules of Debit and Credit and General LedgerDaniel Tan KtNo ratings yet

- Financial TheoryDocument173 pagesFinancial TheoryDaniele NaddeoNo ratings yet

- Notes Receivable.docxDocument4 pagesNotes Receivable.docxCenelyn PajarillaNo ratings yet

- CH 2 Problem HandoutDocument2 pagesCH 2 Problem HandoutAbdullah alhamaadNo ratings yet

- Introduction of Investment Accounting 2023-2024Document6 pagesIntroduction of Investment Accounting 2023-20247013 Arpit DubeyNo ratings yet

- K-W-L Chart: (Financial Accounts) Bba - Semester 1Document9 pagesK-W-L Chart: (Financial Accounts) Bba - Semester 1Rabeeka SiddiquiNo ratings yet

- Company Acc Unit 3Document39 pagesCompany Acc Unit 3Megha DevanpalliNo ratings yet

- Module 1 AccDocument6 pagesModule 1 Acc21-035 Dhanjit RoymedhiNo ratings yet

- F7 - C7 RevenueDocument76 pagesF7 - C7 RevenueNgô Thành DanhNo ratings yet

- Free Cash Flow ComputationDocument2 pagesFree Cash Flow ComputationDebapratim SenguptaNo ratings yet

- Chapter 5 Accounting PrincipleDocument5 pagesChapter 5 Accounting PrincipleTrinh Nguyễn ThảoNo ratings yet

- Investment Pricing Methods: A Guide for Accounting and Financial ProfessionalsFrom EverandInvestment Pricing Methods: A Guide for Accounting and Financial ProfessionalsNo ratings yet

- Financial Analysis 101: An Introduction to Analyzing Financial Statements for beginnersFrom EverandFinancial Analysis 101: An Introduction to Analyzing Financial Statements for beginnersNo ratings yet

- EC2 Economics Chapter 21 - Oligopoly 155-162Document21 pagesEC2 Economics Chapter 21 - Oligopoly 155-162bardak twoNo ratings yet

- Lakkapää Import - ICPO - Kingfa 10 M - 20210421Document2 pagesLakkapää Import - ICPO - Kingfa 10 M - 20210421Alex SalaNo ratings yet

- MR - Jacob O Pang ConfirmationDocument1 pageMR - Jacob O Pang ConfirmationJoshua DreamcatcherNo ratings yet

- Gipe BGG 1894 11 01 PVDocument61 pagesGipe BGG 1894 11 01 PVAamir MugheriNo ratings yet

- Jasperson Et Al. - 2010 - Comparison of Micro-Pin-Fin and Microchannel HeatDocument13 pagesJasperson Et Al. - 2010 - Comparison of Micro-Pin-Fin and Microchannel Heatmosab.backkupNo ratings yet

- Soal PAS 9 2022Document6 pagesSoal PAS 9 2022PKBM Darul Ulum BuluNo ratings yet

- Assist. Mirela-Oana Pintea PH.D Student: Provided by Research Papers in EconomicsDocument12 pagesAssist. Mirela-Oana Pintea PH.D Student: Provided by Research Papers in EconomicsRabia SabirNo ratings yet

- E StatementpdfDocument3 pagesE StatementpdfgarrettloehrNo ratings yet

- 06 - Class 06 - Trade SetupsDocument12 pages06 - Class 06 - Trade SetupsChandler BingNo ratings yet

- FİTTİNGSDocument11 pagesFİTTİNGSHalil KocNo ratings yet

- 4.33 - La Paz South District - Las - Q2 - Tle - He 6 - Week 1Document4 pages4.33 - La Paz South District - Las - Q2 - Tle - He 6 - Week 1VALERIE Y. DIZON0% (1)

- Weighted Index Numbers Are Also of Two TypesDocument4 pagesWeighted Index Numbers Are Also of Two TypesSumit BainNo ratings yet

- Sujet de Dissertation Sur Les Finances PubliquesDocument8 pagesSujet de Dissertation Sur Les Finances PubliquesWriteMyPaperForMeCheapSingapore100% (1)

- Secured PayoutDocument2 pagesSecured PayoutVishal BawaneNo ratings yet

- Memo - Office of The Municipal AccountantDocument4 pagesMemo - Office of The Municipal AccountantJanJan BoragayNo ratings yet

- Bookkeeping Periodic PerpetualDocument12 pagesBookkeeping Periodic PerpetualLou Anthony A. CaliboNo ratings yet

- Tourism Traning Centre Politeknik Negeri Bali (TTC-PNB) : Executive SummaryDocument8 pagesTourism Traning Centre Politeknik Negeri Bali (TTC-PNB) : Executive SummaryBowoNo ratings yet

- What Is Retention MoneyDocument3 pagesWhat Is Retention MoneyAbdul Rahman Sabra100% (1)

- Analisa Struktur Kos Tri SuyaDocument32 pagesAnalisa Struktur Kos Tri SuyafaisalNo ratings yet

- Beta Saham 20171229 enDocument12 pagesBeta Saham 20171229 enAgung AryaNo ratings yet

- Aklan State Univeristy School of Management SchoolDocument4 pagesAklan State Univeristy School of Management SchoolKenneth Christian WilburNo ratings yet

- Toy World CaseDocument9 pagesToy World Casesaurabhsaurs100% (1)

- FOLKE Sweater PatternDocument8 pagesFOLKE Sweater Patternlukeberlin76No ratings yet

- Saanvi Soulful Journey Company DetailsDocument1 pageSaanvi Soulful Journey Company Detailssarthak kumarNo ratings yet

- BZF79D591 ChuangchidDocument9 pagesBZF79D591 Chuangchidwill bNo ratings yet

- Chapter 1 - IntroductionDocument11 pagesChapter 1 - IntroductionChelsea Anne VidalloNo ratings yet

- In - Selfx India Fashinza Event d2cDocument1 pageIn - Selfx India Fashinza Event d2camanpatniNo ratings yet

- Indian Sugar Industry IntroductionDocument2 pagesIndian Sugar Industry Introductionjayeshvk100% (7)

- ELT Cowhorn DatasheetDocument1 pageELT Cowhorn Datasheettienhm_pve1553No ratings yet

- Autumn Waves PonchoDocument9 pagesAutumn Waves PonchoMelinda MunkaiNo ratings yet

Download as pdf or txt

You might also like

- Question - Chapter 2Document17 pagesQuestion - Chapter 2Mạnh Đỗ ĐứcNo ratings yet

- Accounting For Ijarah and Ijarah MuntahiaDocument12 pagesAccounting For Ijarah and Ijarah Muntahiatheintelligentgirl100% (1)

- Class 12 Accounts Notes Chapter 9 Studyguide360Document19 pagesClass 12 Accounts Notes Chapter 9 Studyguide360Ali ssNo ratings yet

- CA Final FR A MTP 1 May 2024 Castudynotes ComDocument12 pagesCA Final FR A MTP 1 May 2024 Castudynotes Compabitrarijal1227No ratings yet

- P1_FR_May24_MTP1_Solution @CA_Final_LegendDocument16 pagesP1_FR_May24_MTP1_Solution @CA_Final_Legendcontact.hemaamudhaNo ratings yet

- MTP 1 PAPER 1 Answe KeyDocument12 pagesMTP 1 PAPER 1 Answe Keyhitesh YadavNo ratings yet

- C9 Receivable Financing Discounting of Notes ReceivableDocument24 pagesC9 Receivable Financing Discounting of Notes ReceivableAngelie LaxaNo ratings yet

- Topic 3 Issuance, Redemption and Conversion of Loan Instruments Mfrs 7, Mfrs 9, Mfrs 132 (MFRS 17-Effective 1.1.2020)Document86 pagesTopic 3 Issuance, Redemption and Conversion of Loan Instruments Mfrs 7, Mfrs 9, Mfrs 132 (MFRS 17-Effective 1.1.2020)Ainshafiyyah AinshafiyyahNo ratings yet

- Adjusting EntriesDocument10 pagesAdjusting EntriesJezmar John B. GulmaticoNo ratings yet

- Chapter-8 Issue of Debentures: Debenture: The Word Debenture' Has Been Derived From A Latin Word Debere' WhichDocument8 pagesChapter-8 Issue of Debentures: Debenture: The Word Debenture' Has Been Derived From A Latin Word Debere' Whichramandeep kaurNo ratings yet

- Issue of DebenturesDocument23 pagesIssue of Debenturesramandeep kaurNo ratings yet

- LECTURE 7 Accounting For Merchandising Activities Periodic and Perpetual BSAFDocument40 pagesLECTURE 7 Accounting For Merchandising Activities Periodic and Perpetual BSAFShahzad C7No ratings yet

- FR - AnswerDocument12 pagesFR - Answer6dzk78g2vyNo ratings yet

- 8 Cash Flow StatementDocument10 pages8 Cash Flow StatementBAZINGANo ratings yet

- Revenue PrintingDocument19 pagesRevenue Printingayushmaharaj68No ratings yet

- Session 7 - Financial InstrumentsDocument31 pagesSession 7 - Financial InstrumentsMa. Bernadette MontianoNo ratings yet

- Trial Balance: Credit Balances of All Accounts in The Ledger With A View To Test Arithmetical Accuracy of The BooksDocument5 pagesTrial Balance: Credit Balances of All Accounts in The Ledger With A View To Test Arithmetical Accuracy of The BooksPriyanka SharmaNo ratings yet

- Loans ReceivableDocument3 pagesLoans ReceivableDonna ValentinNo ratings yet

- Board Paper-2022-XIDocument8 pagesBoard Paper-2022-XIRn GuptaNo ratings yet

- Amalgamation: 5) (BasicallyDocument11 pagesAmalgamation: 5) (Basicallymadhu peeralaNo ratings yet

- Adobe Scan 13 Oct 2022Document13 pagesAdobe Scan 13 Oct 2022Abhishek SinghNo ratings yet

- Advanced Financial Reporting: Module 4: Final Accounts of Insurance CompaniesDocument23 pagesAdvanced Financial Reporting: Module 4: Final Accounts of Insurance CompaniesBijosh ThomasNo ratings yet

- 1 Intro To LiabilitiesDocument13 pages1 Intro To LiabilitiesPioloNo ratings yet

- IFRS 2 Share Based PaymentDocument19 pagesIFRS 2 Share Based PaymentVikky BehNo ratings yet

- Chapter Three The Balance Sheet and Financial DisclosuresDocument33 pagesChapter Three The Balance Sheet and Financial Disclosuressan marcoNo ratings yet

- Futures Contracts Market: Romanian Commodities ExchangeDocument28 pagesFutures Contracts Market: Romanian Commodities Exchangegriguta99No ratings yet

- Ilovepdf MergedDocument17 pagesIlovepdf Mergednsm2zmvnbbNo ratings yet

- Dr. M. D. Chase Long Beach State University Accounting 500 4A Balance SheetDocument9 pagesDr. M. D. Chase Long Beach State University Accounting 500 4A Balance SheetArtur JastNo ratings yet

- Assets MeasurementsDocument11 pagesAssets MeasurementslllllnubhbhgNo ratings yet

- Issue of DebenturesDocument12 pagesIssue of Debenturessiva883100% (1)

- Week 05 2022 Topic 5 Lecture Leases Part ADocument20 pagesWeek 05 2022 Topic 5 Lecture Leases Part AErnest LeongNo ratings yet

- MATERIALDocument8 pagesMATERIALVatsal ParmarNo ratings yet

- Chapter-5 - FI-BDocument20 pagesChapter-5 - FI-BKhanh LinhNo ratings yet

- Topic: Accounting Cycle of A Service BusinessDocument5 pagesTopic: Accounting Cycle of A Service BusinessJohn Rey BusimeNo ratings yet

- Receivable Financing: 3. Factoring of Accounts Receivable 4. Discounting of Notes ReceivableDocument2 pagesReceivable Financing: 3. Factoring of Accounts Receivable 4. Discounting of Notes ReceivableJonathan NavalloNo ratings yet

- IFA Lesson 3 Slides (Financial Liabilities & Equity)Document53 pagesIFA Lesson 3 Slides (Financial Liabilities & Equity)zengruiqi20000302No ratings yet

- 13 Financial Asset at Amortized CostDocument5 pages13 Financial Asset at Amortized CostLara Jane Dela CruzNo ratings yet

- EA EA1 SU2 OutlineDocument23 pagesEA EA1 SU2 OutlineAashu AntilNo ratings yet

- Part-A Answer To The Question No.1: 1.quick Ratio 1.21 TimesDocument7 pagesPart-A Answer To The Question No.1: 1.quick Ratio 1.21 TimesThe JesterNo ratings yet

- IA1-Continuation PPEDocument13 pagesIA1-Continuation PPEJhunnie LoriaNo ratings yet

- Accounting For Bonds PayableDocument31 pagesAccounting For Bonds PayableJon Christian Miranda100% (2)

- Fundamentals of AccountingDocument27 pagesFundamentals of AccountingMajariya Sahar SabladNo ratings yet

- Module 1 Notes and Loans Receivable PDFDocument43 pagesModule 1 Notes and Loans Receivable PDFALEXA GENMARY GULFAN0% (1)

- P7 - Investment in Debt Securities & Other Non-Current Financial AssetsDocument46 pagesP7 - Investment in Debt Securities & Other Non-Current Financial AssetsNashiel AnneNo ratings yet

- Security Valuation 2 RevisionDocument14 pagesSecurity Valuation 2 RevisionParth joshiNo ratings yet

- Edexcel IGCSE Accounting Student S Book Answers PDFDocument92 pagesEdexcel IGCSE Accounting Student S Book Answers PDFArshad Bashir100% (1)

- Qucik RFR On CL (Sec 123 To 148)Document10 pagesQucik RFR On CL (Sec 123 To 148)visshelp100% (1)

- Chapter 2 Rules of Debit and Credit and General LedgerDocument3 pagesChapter 2 Rules of Debit and Credit and General LedgerDaniel Tan KtNo ratings yet

- Financial TheoryDocument173 pagesFinancial TheoryDaniele NaddeoNo ratings yet

- Notes Receivable.docxDocument4 pagesNotes Receivable.docxCenelyn PajarillaNo ratings yet

- CH 2 Problem HandoutDocument2 pagesCH 2 Problem HandoutAbdullah alhamaadNo ratings yet

- Introduction of Investment Accounting 2023-2024Document6 pagesIntroduction of Investment Accounting 2023-20247013 Arpit DubeyNo ratings yet

- K-W-L Chart: (Financial Accounts) Bba - Semester 1Document9 pagesK-W-L Chart: (Financial Accounts) Bba - Semester 1Rabeeka SiddiquiNo ratings yet

- Company Acc Unit 3Document39 pagesCompany Acc Unit 3Megha DevanpalliNo ratings yet

- Module 1 AccDocument6 pagesModule 1 Acc21-035 Dhanjit RoymedhiNo ratings yet

- F7 - C7 RevenueDocument76 pagesF7 - C7 RevenueNgô Thành DanhNo ratings yet

- Free Cash Flow ComputationDocument2 pagesFree Cash Flow ComputationDebapratim SenguptaNo ratings yet

- Chapter 5 Accounting PrincipleDocument5 pagesChapter 5 Accounting PrincipleTrinh Nguyễn ThảoNo ratings yet

- Investment Pricing Methods: A Guide for Accounting and Financial ProfessionalsFrom EverandInvestment Pricing Methods: A Guide for Accounting and Financial ProfessionalsNo ratings yet

- Financial Analysis 101: An Introduction to Analyzing Financial Statements for beginnersFrom EverandFinancial Analysis 101: An Introduction to Analyzing Financial Statements for beginnersNo ratings yet

- EC2 Economics Chapter 21 - Oligopoly 155-162Document21 pagesEC2 Economics Chapter 21 - Oligopoly 155-162bardak twoNo ratings yet

- Lakkapää Import - ICPO - Kingfa 10 M - 20210421Document2 pagesLakkapää Import - ICPO - Kingfa 10 M - 20210421Alex SalaNo ratings yet

- MR - Jacob O Pang ConfirmationDocument1 pageMR - Jacob O Pang ConfirmationJoshua DreamcatcherNo ratings yet

- Gipe BGG 1894 11 01 PVDocument61 pagesGipe BGG 1894 11 01 PVAamir MugheriNo ratings yet

- Jasperson Et Al. - 2010 - Comparison of Micro-Pin-Fin and Microchannel HeatDocument13 pagesJasperson Et Al. - 2010 - Comparison of Micro-Pin-Fin and Microchannel Heatmosab.backkupNo ratings yet

- Soal PAS 9 2022Document6 pagesSoal PAS 9 2022PKBM Darul Ulum BuluNo ratings yet

- Assist. Mirela-Oana Pintea PH.D Student: Provided by Research Papers in EconomicsDocument12 pagesAssist. Mirela-Oana Pintea PH.D Student: Provided by Research Papers in EconomicsRabia SabirNo ratings yet

- E StatementpdfDocument3 pagesE StatementpdfgarrettloehrNo ratings yet

- 06 - Class 06 - Trade SetupsDocument12 pages06 - Class 06 - Trade SetupsChandler BingNo ratings yet

- FİTTİNGSDocument11 pagesFİTTİNGSHalil KocNo ratings yet

- 4.33 - La Paz South District - Las - Q2 - Tle - He 6 - Week 1Document4 pages4.33 - La Paz South District - Las - Q2 - Tle - He 6 - Week 1VALERIE Y. DIZON0% (1)

- Weighted Index Numbers Are Also of Two TypesDocument4 pagesWeighted Index Numbers Are Also of Two TypesSumit BainNo ratings yet

- Sujet de Dissertation Sur Les Finances PubliquesDocument8 pagesSujet de Dissertation Sur Les Finances PubliquesWriteMyPaperForMeCheapSingapore100% (1)

- Secured PayoutDocument2 pagesSecured PayoutVishal BawaneNo ratings yet

- Memo - Office of The Municipal AccountantDocument4 pagesMemo - Office of The Municipal AccountantJanJan BoragayNo ratings yet

- Bookkeeping Periodic PerpetualDocument12 pagesBookkeeping Periodic PerpetualLou Anthony A. CaliboNo ratings yet

- Tourism Traning Centre Politeknik Negeri Bali (TTC-PNB) : Executive SummaryDocument8 pagesTourism Traning Centre Politeknik Negeri Bali (TTC-PNB) : Executive SummaryBowoNo ratings yet

- What Is Retention MoneyDocument3 pagesWhat Is Retention MoneyAbdul Rahman Sabra100% (1)

- Analisa Struktur Kos Tri SuyaDocument32 pagesAnalisa Struktur Kos Tri SuyafaisalNo ratings yet

- Beta Saham 20171229 enDocument12 pagesBeta Saham 20171229 enAgung AryaNo ratings yet

- Aklan State Univeristy School of Management SchoolDocument4 pagesAklan State Univeristy School of Management SchoolKenneth Christian WilburNo ratings yet

- Toy World CaseDocument9 pagesToy World Casesaurabhsaurs100% (1)

- FOLKE Sweater PatternDocument8 pagesFOLKE Sweater Patternlukeberlin76No ratings yet

- Saanvi Soulful Journey Company DetailsDocument1 pageSaanvi Soulful Journey Company Detailssarthak kumarNo ratings yet

- BZF79D591 ChuangchidDocument9 pagesBZF79D591 Chuangchidwill bNo ratings yet

- Chapter 1 - IntroductionDocument11 pagesChapter 1 - IntroductionChelsea Anne VidalloNo ratings yet

- In - Selfx India Fashinza Event d2cDocument1 pageIn - Selfx India Fashinza Event d2camanpatniNo ratings yet

- Indian Sugar Industry IntroductionDocument2 pagesIndian Sugar Industry Introductionjayeshvk100% (7)

- ELT Cowhorn DatasheetDocument1 pageELT Cowhorn Datasheettienhm_pve1553No ratings yet

- Autumn Waves PonchoDocument9 pagesAutumn Waves PonchoMelinda MunkaiNo ratings yet