Download as pdf or txt

You might also like

- Economic Indicators by Philip MohrDocument255 pagesEconomic Indicators by Philip MohrZanele Dlamini100% (2)

- Principles of Economics 10Th Edition Case Test Bank Full Chapter PDFDocument52 pagesPrinciples of Economics 10Th Edition Case Test Bank Full Chapter PDFmirabeltuyenwzp6f100% (11)

- EC1002 Commentary 2017Document40 pagesEC1002 Commentary 2017Sophia Garner100% (1)

- Lewis Model of Rural Urban InteractionDocument14 pagesLewis Model of Rural Urban InteractionAbhimanyu Singh0% (1)

- Unit Three Money - Forms and FunctionsDocument6 pagesUnit Three Money - Forms and FunctionsMihai TudorNo ratings yet

- The Keynesian ModelDocument37 pagesThe Keynesian ModelmahamNo ratings yet

- TM.10 Uang Dan BankDocument23 pagesTM.10 Uang Dan BankEgi MadiunNo ratings yet

- Session 6-Supply of MoneyDocument28 pagesSession 6-Supply of MoneyeshanNo ratings yet

- Econjn 0060 Study Guide, Exam 3 Fall17Document18 pagesEconjn 0060 Study Guide, Exam 3 Fall17Lauren SerafiniNo ratings yet

- Inisiasi 7Document23 pagesInisiasi 7Devi AkatsukiNo ratings yet

- 4 - The Asset MarketDocument52 pages4 - The Asset MarketJiayin LeeNo ratings yet

- Money Demand and Money Suppy Process: Session 09-10Document28 pagesMoney Demand and Money Suppy Process: Session 09-10Raj PatelNo ratings yet

- The Asset Market Money and PriceDocument12 pagesThe Asset Market Money and PriceRaja Sikanadar - 92023/TCHR/BSBNo ratings yet

- Quantity Theories of Money - From Fisher To FriedmanDocument4 pagesQuantity Theories of Money - From Fisher To FriedmansahadudheenNo ratings yet

- Money and Monetary Policy: Md. Shawkat Ali Professor Department of EconomicsDocument23 pagesMoney and Monetary Policy: Md. Shawkat Ali Professor Department of EconomicsEverything What U WantNo ratings yet

- Session 9 Reading 1. This Set of Slides 2. From The Text Material Chapter - 5Document33 pagesSession 9 Reading 1. This Set of Slides 2. From The Text Material Chapter - 5AkshitSoniNo ratings yet

- MacroC4 The Money MarketDocument50 pagesMacroC4 The Money MarketNguyễn Khắc Quý HươngNo ratings yet

- NotesDocument2 pagesNotesbousry.meryemNo ratings yet

- Money, Prices & Inflation in The LR: MGEB06Document31 pagesMoney, Prices & Inflation in The LR: MGEB06Zheng JaydenNo ratings yet

- Monetary Policy: Based On "Macroeconomics" by Dornbusch and Fischer and "Elements of Economics" by TullaoDocument12 pagesMonetary Policy: Based On "Macroeconomics" by Dornbusch and Fischer and "Elements of Economics" by TullaoDiane UyNo ratings yet

- Module 2 - PPT - 1 - The Classical Macroeconomic Model - Part I PDFDocument15 pagesModule 2 - PPT - 1 - The Classical Macroeconomic Model - Part I PDFChristian Cedrick OlmonNo ratings yet

- Lecture 7Document23 pagesLecture 7CHUA WEI JINNo ratings yet

- Lecture 2Document26 pagesLecture 2PratyushGarewalNo ratings yet

- Unit 2Document33 pagesUnit 2Shivam RajNo ratings yet

- Chapter 3Document49 pagesChapter 3Trang ĐoànNo ratings yet

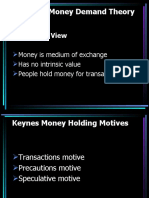

- Keynesian Money Demand Theory: Traditional ViewDocument52 pagesKeynesian Money Demand Theory: Traditional ViewALINo ratings yet

- III. Demand For MoneyDocument25 pagesIII. Demand For MoneyTanishq VijayNo ratings yet

- CLass 4 Monetary PolicyDocument13 pagesCLass 4 Monetary PolicyMd. Faysal HossainNo ratings yet

- Lecture 03 Notes - Spring 2009 PDFDocument8 pagesLecture 03 Notes - Spring 2009 PDF6doitNo ratings yet

- Introduction To Money, Concepts, Definitions, Central Bank, Theories of Money Supply, EtcDocument28 pagesIntroduction To Money, Concepts, Definitions, Central Bank, Theories of Money Supply, Etcyousuf anwarNo ratings yet

- Demand For MoneyDocument24 pagesDemand For MoneyNIKHILESHNo ratings yet

- For TeachingMoneyDocument32 pagesFor TeachingMoneySubrat PatroNo ratings yet

- Chapter 4: Money and InflationDocument37 pagesChapter 4: Money and InflationMinh HangNo ratings yet

- Macroeconomics 4Document37 pagesMacroeconomics 4Quần hoaNo ratings yet

- Chap 8Document24 pagesChap 8nbh167705No ratings yet

- Macroeconomics - Chapter 6Document24 pagesMacroeconomics - Chapter 6tomshave28No ratings yet

- Uang Dan Bank: Pertemuan Ke-13Document23 pagesUang Dan Bank: Pertemuan Ke-13Yudha Rachman WinartoNo ratings yet

- The Demand For Money: Theories and EvidenceDocument14 pagesThe Demand For Money: Theories and EvidenceAchal LalwaniNo ratings yet

- Intermediate Macroeconomics (Ecn 2215) : Money and Inflation Lecture Notes by Charles M. Banda Notes Extracted From MankiwDocument25 pagesIntermediate Macroeconomics (Ecn 2215) : Money and Inflation Lecture Notes by Charles M. Banda Notes Extracted From MankiwYande ZuluNo ratings yet

- Lecture 7 - Money Growth and InflationDocument35 pagesLecture 7 - Money Growth and InflationY Nguyen Ngoc Nhu QTKD-1TC-18No ratings yet

- Liquidity Preference TheoryDocument34 pagesLiquidity Preference Theorygoldenguy90100% (2)

- Money PresentationDocument14 pagesMoney PresentationChristina C ChNo ratings yet

- Money Demand and SupplyDocument18 pagesMoney Demand and SupplyChristopher John MwakipesileNo ratings yet

- Me 6Document21 pagesMe 6Panchami Padmasana Sarangi PGP 2022-24 BatchNo ratings yet

- Lecture Notes 3Document15 pagesLecture Notes 3Eris HotiNo ratings yet

- Topic 7 - Money and The Money MarketDocument21 pagesTopic 7 - Money and The Money Marketpreetirajasegar08No ratings yet

- Classical Theory Demand For Money NallDocument15 pagesClassical Theory Demand For Money NallAchmad TriantoNo ratings yet

- Ch3 (Demand For Money)Document71 pagesCh3 (Demand For Money)Rezuanul RafiNo ratings yet

- Unit5 MoneyDocument34 pagesUnit5 Moneytempacc9322No ratings yet

- Chapter+3+ +blaauw+ +class+2023Document103 pagesChapter+3+ +blaauw+ +class+2023Msa MsaNo ratings yet

- Demand of Money: A Presentation by Sahil MirDocument14 pagesDemand of Money: A Presentation by Sahil MirSahil MirNo ratings yet

- Money and Money Market: Unit 1: Demand of MoneyDocument24 pagesMoney and Money Market: Unit 1: Demand of MoneyJoseph PrabhuNo ratings yet

- (KTVM) Kinh Te VI Mo - Pham Xuan Truong - Chap 8 Money and Monetary PolicyDocument22 pages(KTVM) Kinh Te VI Mo - Pham Xuan Truong - Chap 8 Money and Monetary PolicyTHANH TẤN TRẦNNo ratings yet

- Session 8 & 9 - IsLMDocument30 pagesSession 8 & 9 - IsLMAyusha MakenNo ratings yet

- MACRO 5.2 LecDocument5 pagesMACRO 5.2 LecАдамNo ratings yet

- Chapter 25Document7 pagesChapter 25Tasnim SghairNo ratings yet

- Liquidity Preference TheoryDocument10 pagesLiquidity Preference TheoryRajshree MundraNo ratings yet

- 27 Jan Lecture HandoutsDocument37 pages27 Jan Lecture HandoutsJun Rui ChngNo ratings yet

- Group 6 Money Growth & InflationDocument27 pagesGroup 6 Money Growth & Inflationlarasetiari123No ratings yet

- 2 - Money Demand TheoriesDocument8 pages2 - Money Demand Theoriesmajmmallikarachchi.mallikarachchiNo ratings yet

- Friedman Quantity Theory of MoneyDocument12 pagesFriedman Quantity Theory of MoneyAnisha ChoudharyNo ratings yet

- Macroeconomic Analysis I Topic 6: The Asset Market, Money and Prices (Abel, Bernanke & Croushore: Chapter 7)Document40 pagesMacroeconomic Analysis I Topic 6: The Asset Market, Money and Prices (Abel, Bernanke & Croushore: Chapter 7)Enigmatic ElstonNo ratings yet

- Rethinking Food SufficiencyDocument4 pagesRethinking Food SufficiencysanjeeNo ratings yet

- Dying To Be Green (PP 27-31 ONLY)Document73 pagesDying To Be Green (PP 27-31 ONLY)sanjeeNo ratings yet

- Accessible HousingDocument1 pageAccessible HousingsanjeeNo ratings yet

- Brenda Yeoh-CosmopolitanismDocument16 pagesBrenda Yeoh-CosmopolitanismsanjeeNo ratings yet

- History of Economic Thought 2nd Exam - Take HomeDocument5 pagesHistory of Economic Thought 2nd Exam - Take HomeUDecon100% (1)

- Class 12 Macro Economics Chapter 3 - Revision NotesDocument4 pagesClass 12 Macro Economics Chapter 3 - Revision NotesPappu BhatiyaNo ratings yet

- Chapter 4 Aggregate Demand and Aggregate SupplyDocument22 pagesChapter 4 Aggregate Demand and Aggregate SupplyThuy Dung NguyenNo ratings yet

- Relationship Between A Components of Money Demand Function and General Index of A Stock MarketDocument2 pagesRelationship Between A Components of Money Demand Function and General Index of A Stock MarketNabeel Mahdi AljanabiNo ratings yet

- Bank: UNITED BANK LIMITED - Analysis of Financial Statements Financial Year 2004 - Financial Year 2009Document5 pagesBank: UNITED BANK LIMITED - Analysis of Financial Statements Financial Year 2004 - Financial Year 2009Muhammad MuzammalNo ratings yet

- Tiburon Systemic Risk PresentationDocument12 pagesTiburon Systemic Risk PresentationDistressedDebtInvestNo ratings yet

- Use The Data and Your Economic Knowledge To Assess The View That Living Standards in The UK Are Likely To Benefit From Sustained Economic Growth in The Economies of AfricaDocument2 pagesUse The Data and Your Economic Knowledge To Assess The View That Living Standards in The UK Are Likely To Benefit From Sustained Economic Growth in The Economies of AfricaDan Bowen100% (1)

- Literature Review On Unemployment in NigeriaDocument6 pagesLiterature Review On Unemployment in Nigeriaafmzveozwsprug100% (1)

- Central BankDocument65 pagesCentral BankFarazNaseer100% (1)

- External Reserves and Economic Growth in NigeriaDocument11 pagesExternal Reserves and Economic Growth in NigeriaEditor IJTSRDNo ratings yet

- Malaysian Property Bubble: Lecturer'S Name: en Mohd Hafiz Bin Mohd Saberi Group MembersDocument15 pagesMalaysian Property Bubble: Lecturer'S Name: en Mohd Hafiz Bin Mohd Saberi Group MembersZahin SamsudinNo ratings yet

- Nature of EconomicsDocument12 pagesNature of EconomicsHealthyYOU100% (8)

- Measuring Macroeconomic Activity: © 2014 Pearson Education, IncDocument22 pagesMeasuring Macroeconomic Activity: © 2014 Pearson Education, IncchooisinNo ratings yet

- Gross Domestic ProductDocument5 pagesGross Domestic ProductEgege Clinton IkechiNo ratings yet

- Exchange Rate Determination and PolicyDocument33 pagesExchange Rate Determination and PolicyJunius Markov OlivierNo ratings yet

- 2017-01 IFR - Take Comfort in Asian CreditDocument1 page2017-01 IFR - Take Comfort in Asian CreditdildildildilNo ratings yet

- Chapter 13 AnswerDocument19 pagesChapter 13 AnswerKathy WongNo ratings yet

- Cambridge Assessment International Education: Economics 2281/21 May/June 2019Document18 pagesCambridge Assessment International Education: Economics 2281/21 May/June 2019Nivesh BangarigaduNo ratings yet

- Macro Practice Test#2Document10 pagesMacro Practice Test#2Chinmay PanhaleNo ratings yet

- Chapter 1Document23 pagesChapter 1Husnain HaiderNo ratings yet

- Econ310 - Test 2Document7 pagesEcon310 - Test 2Jimmy TengNo ratings yet

- Rbi Report On DemonetisationDocument2 pagesRbi Report On DemonetisationshaktiNo ratings yet

- GDP: A Measure of Total Production and IncomeDocument27 pagesGDP: A Measure of Total Production and IncomeRider TorqueNo ratings yet

- ECO6201 - Chapter 5 - Production and Cost Analysis in The Short Run (Amended)Document36 pagesECO6201 - Chapter 5 - Production and Cost Analysis in The Short Run (Amended)Thomas WuNo ratings yet

- Exercise Sheet - Week 3Document6 pagesExercise Sheet - Week 3Precious MarksNo ratings yet