Download as pdf or txt

You might also like

- Cash and Cash Equivalent AuditingDocument8 pagesCash and Cash Equivalent Auditing수지No ratings yet

- 3.cash and Cash EquivalentsDocument44 pages3.cash and Cash EquivalentsAaron JusayanNo ratings yet

- Ia1 ReviewerDocument10 pagesIa1 ReviewerVeronica SarmientoNo ratings yet

- Compiled Lessons - Far 1Document23 pagesCompiled Lessons - Far 1Gwyn OliverNo ratings yet

- Cash and Cash EquivalentsDocument34 pagesCash and Cash EquivalentsJennalyn S. GanalonNo ratings yet

- Sta Clara - Summary Part 1Document49 pagesSta Clara - Summary Part 1Carms St ClaireNo ratings yet

- If Silent As To Date of Acquisition, Assume As Current: Cash and Cash Equivalents 1. CashDocument3 pagesIf Silent As To Date of Acquisition, Assume As Current: Cash and Cash Equivalents 1. CashKent Raysil PamaongNo ratings yet

- Far.03 Cash and Cash EquivalentsDocument8 pagesFar.03 Cash and Cash EquivalentsRhea Royce CabuhatNo ratings yet

- Cfas - Cash and Cash EquivalentsDocument5 pagesCfas - Cash and Cash EquivalentsYna SarrondoNo ratings yet

- Cash and Cash EquivalentsDocument3 pagesCash and Cash EquivalentsKent Raysil PamaongNo ratings yet

- Accounting For Cash and Cash EquivalentsDocument2 pagesAccounting For Cash and Cash EquivalentsMaybelle BernalNo ratings yet

- Cash & Cash Equivalent: If The Problem Is Silent, Daily, They Are Part of Cash and Cash EquivalentsDocument30 pagesCash & Cash Equivalent: If The Problem Is Silent, Daily, They Are Part of Cash and Cash EquivalentsKim Audrey JalalainNo ratings yet

- Cash and Cash Equivalents and Bank Reconciliation 1Document16 pagesCash and Cash Equivalents and Bank Reconciliation 1Jenny Claire CrusperoNo ratings yet

- Cash and Account ReceivableDocument27 pagesCash and Account Receivableletkristal shineNo ratings yet

- Cash and Cash EquivalentDocument3 pagesCash and Cash EquivalentKimberly Laggui PonayoNo ratings yet

- Chapter 1 Cash and Cash EquivalentsDocument28 pagesChapter 1 Cash and Cash Equivalents2021315379No ratings yet

- Intacc Cash and Cash EquivalentsDocument2 pagesIntacc Cash and Cash EquivalentsKristalen ArmandoNo ratings yet

- Cash and Cash EquivalentsDocument5 pagesCash and Cash Equivalentsforuse insitesNo ratings yet

- Accounting For CashDocument2 pagesAccounting For CashAlexis Jeremie100% (1)

- Accounting For CASH AND CASH EQUIVALENTS PDFDocument2 pagesAccounting For CASH AND CASH EQUIVALENTS PDFCj BarrettoNo ratings yet

- Cash and Cash EquivalentsDocument7 pagesCash and Cash EquivalentsHunNo ratings yet

- Chapter 1Document5 pagesChapter 1Soria Sophia AnnNo ratings yet

- Cash and Cash EquivalentsDocument43 pagesCash and Cash EquivalentsJohn Anjelo MoraldeNo ratings yet

- Cash and Cash EquivalentsDocument2 pagesCash and Cash Equivalentsyes it's kaiNo ratings yet

- RetentionDocument4 pagesRetentionPrince PierreNo ratings yet

- Intacc ReviewerDocument20 pagesIntacc ReviewerAvos NnNo ratings yet

- 01 Cash and Cash EquivalentDocument3 pages01 Cash and Cash EquivalentJetro JuantaNo ratings yet

- Cash and Cash Equivalents (Chapter 1)Document171 pagesCash and Cash Equivalents (Chapter 1)chingNo ratings yet

- PPT2.1-1 Cash and Cash Equivalents (2020)Document42 pagesPPT2.1-1 Cash and Cash Equivalents (2020)Avery Paul MateoNo ratings yet

- Notes (Audit Prob)Document6 pagesNotes (Audit Prob)kodzuken.teyNo ratings yet

- Cash and Cash EquivalentsDocument16 pagesCash and Cash Equivalentsspur iousNo ratings yet

- Cash Cash Equivalents - Part 1Document35 pagesCash Cash Equivalents - Part 1Lily of the ValleyNo ratings yet

- Module 5 - Substantive Test of CashDocument6 pagesModule 5 - Substantive Test of CashJesievelle Villafuerte NapaoNo ratings yet

- Cash and Cash EquivalentsDocument5 pagesCash and Cash EquivalentsCamille Joyce Corpuz Dela CruzNo ratings yet

- Cash and Cash EquivalentDocument22 pagesCash and Cash EquivalentCamille MaterumNo ratings yet

- Intacc 1a Reviewer Conceptual Framework and Accounting StandardsDocument32 pagesIntacc 1a Reviewer Conceptual Framework and Accounting StandardsKrizahMarieCaballeroNo ratings yet

- 01 CashandCashEquivalentsNotesDocument7 pages01 CashandCashEquivalentsNotesVeroNo ratings yet

- Cash and Cash Equivalents SummaryDocument2 pagesCash and Cash Equivalents SummaryJulienne UntalascoNo ratings yet

- C and CE NotesDocument4 pagesC and CE NotesFrancine PimentelNo ratings yet

- FAR LectureDocument6 pagesFAR Lecturewingsenigma 00No ratings yet

- INACCT1Document4 pagesINACCT1RhaegneNo ratings yet

- and Highly Liquid Investment Readily Convertible Into CashDocument3 pagesand Highly Liquid Investment Readily Convertible Into CashGirl Lang AkoNo ratings yet

- Intermediate Accounting - ReviewerDocument29 pagesIntermediate Accounting - ReviewerEthelyn Cailly R. ChenNo ratings yet

- Cash and Cash EquivalentsDocument46 pagesCash and Cash Equivalentsncaacademics.nfjpia2324No ratings yet

- Cash and Cash EquivalentsDocument2 pagesCash and Cash EquivalentsMeluNo ratings yet

- Intacc 1 Cash and Cash Equivalents-1Document10 pagesIntacc 1 Cash and Cash Equivalents-1randel10caneteNo ratings yet

- Cash and Cash EquivalentsDocument31 pagesCash and Cash EquivalentsMark LouieNo ratings yet

- Intermediate Accounting NotesDocument7 pagesIntermediate Accounting NotesKyle Angela IlanNo ratings yet

- Cash and Cash EquivalentsDocument2 pagesCash and Cash EquivalentsMary Jullianne Caile SalcedoNo ratings yet

- CPALE REVIEWER by RDEDocument6 pagesCPALE REVIEWER by RDERachelle Dane EspañolaNo ratings yet

- Module Audit of Cash and Cash EquivalentsDocument6 pagesModule Audit of Cash and Cash EquivalentsIvy ObligadoNo ratings yet

- Topic 1 - Audit of Cash Transactions and BalancesDocument6 pagesTopic 1 - Audit of Cash Transactions and BalancesChelsea PagcaliwaganNo ratings yet

- CFAS Chapter 4 - Cash and Cash EquivalentsDocument3 pagesCFAS Chapter 4 - Cash and Cash EquivalentsAngelaMariePeñarandaNo ratings yet

- Intacc 1a Reviewer Conceptual Framework and Accounting StandardsDocument32 pagesIntacc 1a Reviewer Conceptual Framework and Accounting StandardsKatherine Cabading InocandoNo ratings yet

- NOTESmidtermDocument6 pagesNOTESmidtermAlexis Jhan MagoNo ratings yet

- C7 Lecture NotesDocument3 pagesC7 Lecture NotesJonathan NavalloNo ratings yet

- Unit 1 - CASH AND CASH EQUIVALENTS PDFDocument9 pagesUnit 1 - CASH AND CASH EQUIVALENTS PDFJeric Lagyaban Astrologio100% (1)

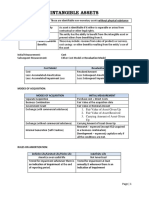

- FAR 007 Summary Notes - Intangible AssetsDocument5 pagesFAR 007 Summary Notes - Intangible AssetsMarynelle Labrador SevillaNo ratings yet

- UNIT 1 Discussion ProblemsDocument13 pagesUNIT 1 Discussion ProblemsMarynelle Labrador SevillaNo ratings yet

- Cost AcctgDocument6 pagesCost AcctgMarynelle Labrador SevillaNo ratings yet

- FAR 006 Summary Notes - Property, Plant & EquipmentDocument9 pagesFAR 006 Summary Notes - Property, Plant & EquipmentMarynelle Labrador SevillaNo ratings yet

- 1 Partnership AccountingDocument10 pages1 Partnership AccountingMarynelle Labrador SevillaNo ratings yet

- PurcomDocument2 pagesPurcomMarynelle Labrador SevillaNo ratings yet

- Unit 6 AUDIT OF INTANGIBLE ASSETS Lecture Notes 2020Document11 pagesUnit 6 AUDIT OF INTANGIBLE ASSETS Lecture Notes 2020Marynelle Labrador Sevilla100% (1)