Download as pdf or txt

You might also like

- Cash and Cash Equivalents - ProblemsDocument47 pagesCash and Cash Equivalents - Problemscommissioned homeworkNo ratings yet

- Google's Project Oxygen Google's Project OxygenDocument4 pagesGoogle's Project Oxygen Google's Project OxygenDeep NagNo ratings yet

- Chapter 2 Cash and Cash Equivalents Exercises T3AY2021Document7 pagesChapter 2 Cash and Cash Equivalents Exercises T3AY2021Carl Vincent BarituaNo ratings yet

- Intermediate Accounting 1Document12 pagesIntermediate Accounting 1Walter Peralta100% (1)

- Practice Problems Account ReceivableDocument14 pagesPractice Problems Account ReceivableDonna Zandueta-TumalaNo ratings yet

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- SAP Brazil GRC NFE OverviewDocument29 pagesSAP Brazil GRC NFE OverviewdhanahbalNo ratings yet

- Chapter 1 Cash and Cash Equivalent-01 PDFDocument7 pagesChapter 1 Cash and Cash Equivalent-01 PDFleng g50% (2)

- Cash To InventoryDocument6 pagesCash To InventoryEdmar HalogNo ratings yet

- Peer Mentoring PostTestDocument7 pagesPeer Mentoring PostTestronnelNo ratings yet

- Audit ReviewDocument9 pagesAudit ReviewephraimNo ratings yet

- Securities: Date Acquired Maturity Date AmountDocument5 pagesSecurities: Date Acquired Maturity Date AmountThe Chuffed Shop PHNo ratings yet

- HANDOUT - CASH AND CASH EQUIVALENTS - Inclusions and ExclusionsDocument4 pagesHANDOUT - CASH AND CASH EQUIVALENTS - Inclusions and ExclusionsKAYLA SHANE GONZALESNo ratings yet

- Far: Mock Qualifying Quiz 2 (Cash and Cash Equivalents & Loans and Receivables)Document8 pagesFar: Mock Qualifying Quiz 2 (Cash and Cash Equivalents & Loans and Receivables)RodelLaborNo ratings yet

- HW On Receivables CDocument5 pagesHW On Receivables CAmjad Rian MangondatoNo ratings yet

- Midterm Examination Suggested AnswersDocument9 pagesMidterm Examination Suggested AnswersJoshua CaraldeNo ratings yet

- HW On ReceivablesDocument20 pagesHW On Receivablesdenvermanapo2000No ratings yet

- Practice Porblems CashDocument8 pagesPractice Porblems CashDonna Zandueta-TumalaNo ratings yet

- Questions - Level 1Document2 pagesQuestions - Level 1didiaenNo ratings yet

- Audit of Cash and Cash EquivalentsDocument3 pagesAudit of Cash and Cash EquivalentsRandy ManzanoNo ratings yet

- IA1 - 1st Mock Quiz (With Suggested Answers)Document6 pagesIA1 - 1st Mock Quiz (With Suggested Answers)Rogienel ReyesNo ratings yet

- PAULA GOZUN - Activity 2 Accounting For Cash-receivables-InventoriesDocument9 pagesPAULA GOZUN - Activity 2 Accounting For Cash-receivables-InventoriesPaupauNo ratings yet

- Cash and Cash EquivalentDocument6 pagesCash and Cash EquivalentNicole RC Del RosarioNo ratings yet

- Audit of Accounts ReceivablesDocument5 pagesAudit of Accounts ReceivablesIzza Mae Rivera KarimNo ratings yet

- 6870 - FAR First PreboardDocument14 pages6870 - FAR First PreboardZiee00No ratings yet

- Cash and Cash Equivalents Problem SetDocument3 pagesCash and Cash Equivalents Problem Setmarinel pioquidNo ratings yet

- Cash and Cash Equivalent QuizDocument3 pagesCash and Cash Equivalent QuizApril Rose Sobrevilla DimpoNo ratings yet

- CE On Receivables T2 AY2021Document4 pagesCE On Receivables T2 AY2021Gian Carlo RamonesNo ratings yet

- Template - Assignment - Audit of ReceivablesDocument6 pagesTemplate - Assignment - Audit of ReceivablesEdemson NavalesNo ratings yet

- Quizbee Practice IntaccDocument21 pagesQuizbee Practice IntaccCharles Kevin MinaNo ratings yet

- Problems CCEDocument10 pagesProblems CCERafael Renz DayaoNo ratings yet

- Audit Ar With SolutionsDocument14 pagesAudit Ar With Solutionsbobo kaNo ratings yet

- Acccob2 Quiz1 Set A With AnswersDocument5 pagesAcccob2 Quiz1 Set A With AnswersshirardadivisoNo ratings yet

- Review Material ACC PRINTDocument11 pagesReview Material ACC PRINTtjcute125No ratings yet

- Practice Problems AR and NotesDocument7 pagesPractice Problems AR and NotesDonna Zandueta-TumalaNo ratings yet

- Au Ia1 Midterm ExamDocument4 pagesAu Ia1 Midterm ExamCherrylane EdicaNo ratings yet

- ICARE Preweek APDocument15 pagesICARE Preweek APjohn paulNo ratings yet

- Answer in Act. 2 For Cash-receivables-InventoriesDocument10 pagesAnswer in Act. 2 For Cash-receivables-InventoriesPaupauNo ratings yet

- Compre 2 - Far1Document5 pagesCompre 2 - Far1Mary Alyssa Claire Capate IINo ratings yet

- Audit of LiabilitiesDocument4 pagesAudit of LiabilitiesJhaybie San BuenaventuraNo ratings yet

- Pamantasan NG Lungsod NG Marikina Auditing and Assurance Concepts & Applications On-Line Learning Mr. Nilo N. Iglesias, CPA, MBA, REA Activities For Week 1 and Week 2Document4 pagesPamantasan NG Lungsod NG Marikina Auditing and Assurance Concepts & Applications On-Line Learning Mr. Nilo N. Iglesias, CPA, MBA, REA Activities For Week 1 and Week 2suruth242No ratings yet

- Let Check AACC124 PDFDocument13 pagesLet Check AACC124 PDFFatima Medriza DuranNo ratings yet

- Financial LiabilitiesDocument4 pagesFinancial LiabilitiesNicah AcojonNo ratings yet

- Far 103 - Accounting For Receivables and Notes ReceivableDocument4 pagesFar 103 - Accounting For Receivables and Notes ReceivablePatrishaNo ratings yet

- ACCTG102 MidtermQ1.5 Cash Make Up ExamDocument6 pagesACCTG102 MidtermQ1.5 Cash Make Up ExamBarrylou Manayan100% (1)

- Q2 FAR0 - 1st Sem 2019 20Document2 pagesQ2 FAR0 - 1st Sem 2019 20Ceejay Cruz TusiNo ratings yet

- Cash and Cash EquivalentDocument3 pagesCash and Cash EquivalentDanica ConcepcionNo ratings yet

- Mocule1 Quiz 202Document4 pagesMocule1 Quiz 202yowatdafrickNo ratings yet

- Mock Departmental Part 1Document7 pagesMock Departmental Part 1Mikee RizonNo ratings yet

- ACCT 1Document15 pagesACCT 1Joyce OcarizaNo ratings yet

- Liability SeatworkDocument8 pagesLiability SeatworkMary Ann B. GabucanNo ratings yet

- LiabilityDocument8 pagesLiabilityAce DesabilleNo ratings yet

- Lesson 2-ACCOUNTS RECEIVABLES-2021NADocument5 pagesLesson 2-ACCOUNTS RECEIVABLES-2021NAandreaNo ratings yet

- ACCO30053-AACA1 Final-Examination 1st-Semester AY2021-2022 QUESTIONNAIREDocument12 pagesACCO30053-AACA1 Final-Examination 1st-Semester AY2021-2022 QUESTIONNAIREKabalaNo ratings yet

- Sample QuestionsDocument9 pagesSample QuestionsLorena DeofilesNo ratings yet

- HO 2 Receivables PDFDocument4 pagesHO 2 Receivables PDFIzzy BNo ratings yet

- Midterm Answer KeyDocument9 pagesMidterm Answer Keylil mixNo ratings yet

- Audit of Receivable PDFDocument7 pagesAudit of Receivable PDFRyan Prado Andaya100% (1)

- 8 Audit of LiabilitiesDocument4 pages8 Audit of LiabilitiesCarieza CardenasNo ratings yet

- The Barrington Guide to Property Management Accounting: The Definitive Guide for Property Owners, Managers, Accountants, and Bookkeepers to ThriveFrom EverandThe Barrington Guide to Property Management Accounting: The Definitive Guide for Property Owners, Managers, Accountants, and Bookkeepers to ThriveNo ratings yet

- Make Money With Dividends Investing, With Less Risk And Higher ReturnsFrom EverandMake Money With Dividends Investing, With Less Risk And Higher ReturnsNo ratings yet

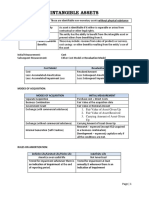

- FAR 007 Summary Notes - Intangible AssetsDocument5 pagesFAR 007 Summary Notes - Intangible AssetsMarynelle Labrador SevillaNo ratings yet

- FAR 002 Summary Notes - Cash & Proof of CashDocument8 pagesFAR 002 Summary Notes - Cash & Proof of CashMarynelle Labrador SevillaNo ratings yet

- FAR 006 Summary Notes - Property, Plant & EquipmentDocument9 pagesFAR 006 Summary Notes - Property, Plant & EquipmentMarynelle Labrador SevillaNo ratings yet

- Cost AcctgDocument6 pagesCost AcctgMarynelle Labrador SevillaNo ratings yet

- 1 Partnership AccountingDocument10 pages1 Partnership AccountingMarynelle Labrador SevillaNo ratings yet

- Unit 6 AUDIT OF INTANGIBLE ASSETS Lecture Notes 2020Document11 pagesUnit 6 AUDIT OF INTANGIBLE ASSETS Lecture Notes 2020Marynelle Labrador Sevilla100% (1)

- PurcomDocument2 pagesPurcomMarynelle Labrador SevillaNo ratings yet

- Sustainable Marketing SyllabusDocument17 pagesSustainable Marketing Syllabusnanda1101No ratings yet

- Bursa de ValoriDocument46 pagesBursa de ValoriDana DanielaNo ratings yet

- MAN 326 Chapter 4-Product PlanningDocument17 pagesMAN 326 Chapter 4-Product PlanningBakir SkenderovicNo ratings yet

- Liber8 Your BusinessDocument7 pagesLiber8 Your BusinessLaura HumphreysNo ratings yet

- 04 130 Feasibility Cost Estimation SheetDocument2 pages04 130 Feasibility Cost Estimation SheetGeorge JaneNo ratings yet

- Asia Amalgamated Holdings Corporation Financials - RobotDoughDocument6 pagesAsia Amalgamated Holdings Corporation Financials - RobotDoughKeith LameraNo ratings yet

- Corporate Governance and SustainabilityDocument8 pagesCorporate Governance and SustainabilitysailendrNo ratings yet

- CNCS Organization Assessment Tool Final 082517 508 0Document29 pagesCNCS Organization Assessment Tool Final 082517 508 0Nicole TaylorNo ratings yet

- Kế toán quản trịDocument88 pagesKế toán quản trịHà Mai VõNo ratings yet

- BPCL Digital TenderDocument99 pagesBPCL Digital TenderKANADARPARNo ratings yet

- Balaji Annual Report 2014 15 PDFDocument280 pagesBalaji Annual Report 2014 15 PDFRahul AgrawalNo ratings yet

- BEGIM Perfume Product LaunchDocument37 pagesBEGIM Perfume Product LaunchMuhammad Yoosuf ShahNo ratings yet

- Stevenson 13e Chapter 13Document40 pagesStevenson 13e Chapter 13Jerwin MarasiganNo ratings yet

- FLAg Checklist of Requirement2Document1 pageFLAg Checklist of Requirement2elton jay amilaNo ratings yet

- Prosecutors Evidence Smith Ouzman LTD Others Trial Opening Final Draft 07-11-14 2Document65 pagesProsecutors Evidence Smith Ouzman LTD Others Trial Opening Final Draft 07-11-14 2Cyprian NyakundiNo ratings yet

- Research FinalDocument18 pagesResearch FinalErwin Carl MendozaNo ratings yet

- Test Series: June, 2022 Mock Test Paper 2 Foundation Course Paper 4: Business Economics and Business and Commercial Knowledge Part-I: Business Economics QuestionsDocument15 pagesTest Series: June, 2022 Mock Test Paper 2 Foundation Course Paper 4: Business Economics and Business and Commercial Knowledge Part-I: Business Economics QuestionsShrwan SinghNo ratings yet

- Project Scope StatementDocument4 pagesProject Scope StatementAlan FirminoNo ratings yet

- Priority Work Try To Find The PersonDocument47 pagesPriority Work Try To Find The PersonThủy Tiên NguyễnNo ratings yet

- Dominos ProjectDocument59 pagesDominos ProjectLakhan Singh RajputNo ratings yet

- SALN Form BlankDocument3 pagesSALN Form BlankIrish GarciaNo ratings yet

- Pushpanjali Case StudyDocument2 pagesPushpanjali Case StudyMohamed Mohamed AdelNo ratings yet

- Basic Information About Business Environment:: Environment Analysis, and Strategy FormulationDocument29 pagesBasic Information About Business Environment:: Environment Analysis, and Strategy Formulationdyah_dewi_1No ratings yet

- Share Price Movements and Its DeterminantsDocument2 pagesShare Price Movements and Its DeterminantsTalha AquilNo ratings yet

- IFI Tut 4Document14 pagesIFI Tut 4Nguyễn Thị Hường 3TC-20ACNNo ratings yet

- Options Summary Notes by CA Gaurav Jain SirDocument14 pagesOptions Summary Notes by CA Gaurav Jain Sirqamaraleem1_25038318No ratings yet

- Assignment No 1Document2 pagesAssignment No 1bakhtawar soniaNo ratings yet

- 5 12th Accountancy Important 23 Mark Questions English MediumDocument6 pages5 12th Accountancy Important 23 Mark Questions English Mediumqueensmiling495No ratings yet