Download as pdf or txt

You might also like

- Accenture Solutions PVT LTDDocument6 pagesAccenture Solutions PVT LTDChethan ChinnuNo ratings yet

- 1 TRN Tawa 100326845300003Document1 page1 TRN Tawa 100326845300003Roopesh ReddyNo ratings yet

- Tax Deduction at SourceDocument62 pagesTax Deduction at SourcePallavisweet100% (1)

- BSBFIM502 - Student Assessment v1.1Document19 pagesBSBFIM502 - Student Assessment v1.1Niomi Golrai100% (1)

- TDS 3Document16 pagesTDS 3payal AgrawalNo ratings yet

- Tds - Tax Deducted at Source: FCA Vishal PoddarDocument22 pagesTds - Tax Deducted at Source: FCA Vishal PoddarPalak PunjabiNo ratings yet

- Lecture Notes - Study Module 9 - TDSDocument32 pagesLecture Notes - Study Module 9 - TDSdata.mvgNo ratings yet

- 30851ipcc May Nov14 It Vol1 CP 9.unlockedDocument43 pages30851ipcc May Nov14 It Vol1 CP 9.unlockedavesatanas13No ratings yet

- Tds ProvisionsDocument38 pagesTds Provisionsglobalfreedom4No ratings yet

- 19771ipcc It Vol1 Cp9Document40 pages19771ipcc It Vol1 Cp9Joseph SalidoNo ratings yet

- TDS - TCSDocument55 pagesTDS - TCSBeing HumaneNo ratings yet

- The Rigours of TDS - An OverviewDocument31 pagesThe Rigours of TDS - An OverviewShaleenPatniNo ratings yet

- All About Tax Deducted at Source (TDS) - Taxguru - inDocument11 pagesAll About Tax Deducted at Source (TDS) - Taxguru - inwaqtkeebaatein12No ratings yet

- CA-Ashok-Mehta - PPT - Income TaxDocument88 pagesCA-Ashok-Mehta - PPT - Income TaxAbinash DasNo ratings yet

- TDS ElaboratedDocument80 pagesTDS ElaboratedAncyNo ratings yet

- Chapter 12 Tds & TcsDocument28 pagesChapter 12 Tds & TcsRajNo ratings yet

- Introduction To TDS:-: Tax Deducted at SourceDocument3 pagesIntroduction To TDS:-: Tax Deducted at Sourcepadmanabha14No ratings yet

- TDS Rates and ReturnsDocument3 pagesTDS Rates and ReturnsKashishKumarNo ratings yet

- 31188sm DTL Finalnew-May-Nov14 Cp28Document66 pages31188sm DTL Finalnew-May-Nov14 Cp28gvcNo ratings yet

- Tds Law and Practice: Under Income Tax Act, 1961Document84 pagesTds Law and Practice: Under Income Tax Act, 1961Vaibhav ChauhanNo ratings yet

- Section 192 Relatin Gto TDS On Salary - Section 192 Says That Every Person Who Is Responsible For Paying Any Income Chargeable Under The HeadDocument46 pagesSection 192 Relatin Gto TDS On Salary - Section 192 Says That Every Person Who Is Responsible For Paying Any Income Chargeable Under The HeadAtul SharmaNo ratings yet

- Tax Deducted at Source IMPORTANT POINTSDocument2 pagesTax Deducted at Source IMPORTANT POINTSnABSAMNNo ratings yet

- Bhubaneswar 08112015 Session I PDFDocument42 pagesBhubaneswar 08112015 Session I PDFsachin NegiNo ratings yet

- Tax - Questio AnswersDocument7 pagesTax - Questio AnswersAnamika VatsaNo ratings yet

- Tax Deducted at SourceDocument20 pagesTax Deducted at Sourceaditisrivastava0511No ratings yet

- Tax Deducted at Source - I: KPPM & AssociatesDocument63 pagesTax Deducted at Source - I: KPPM & AssociatesSaksham JoshiNo ratings yet

- TDS Rate Financial Year 13-14Document10 pagesTDS Rate Financial Year 13-14Heena AgreNo ratings yet

- Overview of TDS: by C.A. Manish JathliyaDocument21 pagesOverview of TDS: by C.A. Manish JathliyaHasan Babu KothaNo ratings yet

- Deduction, Collection & Recovery of TaxesDocument143 pagesDeduction, Collection & Recovery of TaxesjyotiNo ratings yet

- Income Tax 2017 Edazdb1013Document50 pagesIncome Tax 2017 Edazdb1013Pradeep PatilNo ratings yet

- Tds Rate Chart Fy 2014-15 Ay 2015-16Document26 pagesTds Rate Chart Fy 2014-15 Ay 2015-16shivashankari86No ratings yet

- TDS On Salaries - Income Tax Department, INDIADocument112 pagesTDS On Salaries - Income Tax Department, INDIAArnav MendirattaNo ratings yet

- For Tds On SalaryDocument40 pagesFor Tds On SalarykshitijsaxenaNo ratings yet

- Tax Deduction at SourceDocument4 pagesTax Deduction at SourcevishalsidankarNo ratings yet

- Complete TDSNotesDocument40 pagesComplete TDSNotesRohan NagvekarNo ratings yet

- TDS, TCS & Advance TaxDocument32 pagesTDS, TCS & Advance TaxBablu KumarNo ratings yet

- Tax Final Notes. 1Document25 pagesTax Final Notes. 1Hannah MeranoNo ratings yet

- 51 GST Flyer - Chapter 47 - TDS On GSTDocument5 pages51 GST Flyer - Chapter 47 - TDS On GSTRanjanNo ratings yet

- OL 4 - BLT Study Text Suppliment 2021 - On New Tax AmmendmentsDocument28 pagesOL 4 - BLT Study Text Suppliment 2021 - On New Tax Ammendmentshte19031No ratings yet

- BasicsDocument5 pagesBasicsnazriya nasarNo ratings yet

- AX Educted at Ource - I: KPPM & AssociatesDocument67 pagesAX Educted at Ource - I: KPPM & AssociatesSaksham JoshiNo ratings yet

- GST Amdts Part 2Document5 pagesGST Amdts Part 2amankhurana0910No ratings yet

- Tax Deducted at Source TDSDocument55 pagesTax Deducted at Source TDSDhruv SetiaNo ratings yet

- Tax Deducted at SourceDocument29 pagesTax Deducted at SourceAmbar Pratik MishraNo ratings yet

- Ch-9 Advance Tax, TDS, TCSDocument122 pagesCh-9 Advance Tax, TDS, TCSrinkal jethiNo ratings yet

- TDS NotesDocument6 pagesTDS NotesRustam SalamNo ratings yet

- Presentation+ +Manish+ShahDocument106 pagesPresentation+ +Manish+ShahAtul PatelNo ratings yet

- What Is Tax Deducted at SourceDocument6 pagesWhat Is Tax Deducted at SourcejdonNo ratings yet

- IMP All About Due Date For TDS TCS Payment and TDS TCSDocument32 pagesIMP All About Due Date For TDS TCS Payment and TDS TCSsukantabera215No ratings yet

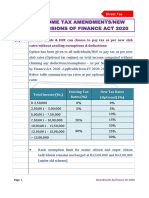

- Income Tax Amendments/New Provisions of Finance Act 2020Document46 pagesIncome Tax Amendments/New Provisions of Finance Act 2020shubhamworkNo ratings yet

- CP 9 Advanced Tax, Tax Deduction at Source and Introduction of Tax Collection at SourceDocument108 pagesCP 9 Advanced Tax, Tax Deduction at Source and Introduction of Tax Collection at Sourcesaravana pandianNo ratings yet

- 74802bos60498-Cp7 (1) - UnlockedDocument136 pages74802bos60498-Cp7 (1) - Unlockedsinghalrachit27No ratings yet

- Section 194C: TDS On ContractDocument5 pagesSection 194C: TDS On ContractwaghuleNo ratings yet

- For Assessment Year - 2011 - 12 TDS Rates Chart Rates of TDS For Major Nature of Payments For The Financial Year 2010-11Document6 pagesFor Assessment Year - 2011 - 12 TDS Rates Chart Rates of TDS For Major Nature of Payments For The Financial Year 2010-11Savoir PenNo ratings yet

- Tenant Advisory: 20 Day of The Month Following The Close of The Taxable QuarterDocument1 pageTenant Advisory: 20 Day of The Month Following The Close of The Taxable QuarterJanetNo ratings yet

- 1.7.7.1. Entertainment Allowance (U/s 16 (Ii) ) : 1.7.7. Deduction Out of Gross Salary (Section 16)Document5 pages1.7.7.1. Entertainment Allowance (U/s 16 (Ii) ) : 1.7.7. Deduction Out of Gross Salary (Section 16)Vinod PillaiNo ratings yet

- Tax Deduction at SourceDocument5 pagesTax Deduction at SourceSarayu BhardwajNo ratings yet

- Tax UpdatesDocument79 pagesTax UpdatesFreijiah SonNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- 1040 Exam Prep: Module II - Basic Tax ConceptsFrom Everand1040 Exam Prep: Module II - Basic Tax ConceptsRating: 1.5 out of 5 stars1.5/5 (2)

- 1040 Exam Prep: Module I: The Form 1040 FormulaFrom Everand1040 Exam Prep: Module I: The Form 1040 FormulaRating: 1 out of 5 stars1/5 (3)

- 71147bos57143 cp9Document147 pages71147bos57143 cp9shivani singhNo ratings yet

- A Study On Merger in DetailDocument101 pagesA Study On Merger in Detailshivani singhNo ratings yet

- Intro of TdsDocument6 pagesIntro of Tdsshivani singhNo ratings yet

- All HTML Codes2 Assignment-2Document12 pagesAll HTML Codes2 Assignment-2shivani singhNo ratings yet

- Tax Deduction at SourceDocument10 pagesTax Deduction at Sourceshivani singhNo ratings yet

- Uk Payslip PDFDocument3 pagesUk Payslip PDFJhonel PauloNo ratings yet

- UKPayslipDocument2 pagesUKPayslipjoasebr08No ratings yet

- Ias 12Document21 pagesIas 12david_thapaNo ratings yet

- Vinay Sagar BillDocument1 pageVinay Sagar BillVinaysagar KakkurlaNo ratings yet

- Invoice 7272206376Document5 pagesInvoice 7272206376Bhagawant KamatNo ratings yet

- DocxDocument4 pagesDocxnicole bancoro100% (1)

- RR No. 8 2018Document35 pagesRR No. 8 2018zul fanNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)ANANT MISHRANo ratings yet

- Archana Ashok Raut GST Impact On Consumer DurablesDocument64 pagesArchana Ashok Raut GST Impact On Consumer DurablesArun Singh100% (1)

- Effective Tax RateDocument55 pagesEffective Tax RateArturas GumuliauskasNo ratings yet

- Direct and Indirect TaxesDocument14 pagesDirect and Indirect Taxeskratika singhNo ratings yet

- 82202BIR Form 1702-MXDocument9 pages82202BIR Form 1702-MXRen A EleponioNo ratings yet

- Cir vs. Seagate TechnologyDocument1 pageCir vs. Seagate Technologygeorge almedaNo ratings yet

- PEZA REPORTORIAL REQUIREMENTS As of Feb 2023Document2 pagesPEZA REPORTORIAL REQUIREMENTS As of Feb 2023MarkNo ratings yet

- Income Tax BotswanaDocument15 pagesIncome Tax BotswanaFrancisNo ratings yet

- MCQ Reviewer in TaxationDocument40 pagesMCQ Reviewer in TaxationRock LeeNo ratings yet

- Bir Ruling No 477-2013Document1 pageBir Ruling No 477-2013Jaz SumalinogNo ratings yet

- Special Liabilities San Carlos CollegeDocument23 pagesSpecial Liabilities San Carlos CollegeRowbby Gwyn100% (1)

- (Office Copy. Please Attach With The Application) : Page 1/1Document1 page(Office Copy. Please Attach With The Application) : Page 1/1Sujith Raj SNo ratings yet

- 2C00445Document6 pages2C00445Anurag KhadeNo ratings yet

- N. B A - C.I.T. JT 2003 (1) SC 363: Agavathy Mmal VDocument6 pagesN. B A - C.I.T. JT 2003 (1) SC 363: Agavathy Mmal VarmsarivuNo ratings yet

- Maharashtra National Law University, Aurangabad: Law of Taxation-GST ProjectDocument13 pagesMaharashtra National Law University, Aurangabad: Law of Taxation-GST ProjectSoumiki GhoshNo ratings yet

- STM1 FormDocument2 pagesSTM1 Formmeimeicui14No ratings yet

- Book in VoiceDocument1 pageBook in VoiceSanjeet RaizadaNo ratings yet

- Thomson 123.2cm 49 Inch Ultra HD 4K LED Smart Android TV With In-Built Soundbar & NetflixDocument2 pagesThomson 123.2cm 49 Inch Ultra HD 4K LED Smart Android TV With In-Built Soundbar & NetflixSandipan MNo ratings yet

- Fasb 109Document116 pagesFasb 109Gopal Krishna OzaNo ratings yet

- Accounting For VAT in Th... Accounting Center, Inc.Document4 pagesAccounting For VAT in Th... Accounting Center, Inc.Martin EspinosaNo ratings yet