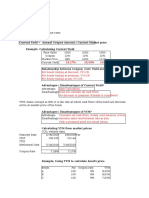

Session 1 and 2

Session 1 and 2

You might also like

- Solution Manual For Fundamentals of Corporate Finance 7th Canadian Edition Richard A BrealeyDocument22 pagesSolution Manual For Fundamentals of Corporate Finance 7th Canadian Edition Richard A BrealeyKarinaMasonprdbc100% (50)

- Im AnswersDocument6 pagesIm Answersromal_talwarNo ratings yet

- Quantitative Problems Chapter 3Document5 pagesQuantitative Problems Chapter 3Khadija ShabbirNo ratings yet

- Suggested Solutions Assignment 02: Operational Risk ManagementDocument5 pagesSuggested Solutions Assignment 02: Operational Risk ManagementDigong Smaz50% (2)

- Problem Set 1 - Bonds and Time Value of MoneyDocument4 pagesProblem Set 1 - Bonds and Time Value of Moneymattgodftey1No ratings yet

- Convexity and DurationDocument20 pagesConvexity and DurationNikka CasyaoNo ratings yet

- Lecture 10 502 1ppDocument12 pagesLecture 10 502 1ppJohn SmithNo ratings yet

- Lec 12Document5 pagesLec 12Ryan GroffNo ratings yet

- Bodie10ce SM CH15Document13 pagesBodie10ce SM CH15William GrignonNo ratings yet

- Present ValueDocument38 pagesPresent Valuemarjannaseri77100% (1)

- Chapter 12 Bond Prices and YieldsDocument15 pagesChapter 12 Bond Prices and YieldsSharoz SheikhNo ratings yet

- Unit 5 Bonds and Stock Valuation and Cost of CapitalDocument14 pagesUnit 5 Bonds and Stock Valuation and Cost of CapitalGizaw BelayNo ratings yet

- Interest Rates Chapter 4 (Part1) : Geng NiuDocument49 pagesInterest Rates Chapter 4 (Part1) : Geng NiuegaNo ratings yet

- 1.02 The Time Value of Money in Finance - AnswersDocument4 pages1.02 The Time Value of Money in Finance - AnswersThe SpectreNo ratings yet

- Activity Sheet In: Business FinanceDocument8 pagesActivity Sheet In: Business FinanceCatherine Larce100% (1)

- Bond Return Valuatio DurationDocument63 pagesBond Return Valuatio DurationSambi Reddy Gari NeelimaNo ratings yet

- 7 Additional Solved Problems 6Document14 pages7 Additional Solved Problems 6Pranoy SarkarNo ratings yet

- Quiz 10 - CH 16Document4 pagesQuiz 10 - CH 16JamNo ratings yet

- Interest Rates Chapter 4 (Part1) : Geng NiuDocument52 pagesInterest Rates Chapter 4 (Part1) : Geng NiuegaNo ratings yet

- Interest Rates and Exchange RatesDocument5 pagesInterest Rates and Exchange RatesPutriNo ratings yet

- Excel TVM Functions PDFDocument8 pagesExcel TVM Functions PDFVishal GoelNo ratings yet

- BKM9e Answers Chap015 PDFDocument11 pagesBKM9e Answers Chap015 PDFLê Chấn PhongNo ratings yet

- BMA 12e SM CH 25 Final PDFDocument16 pagesBMA 12e SM CH 25 Final PDFNikhil ChadhaNo ratings yet

- Fixed Income Class Examples ADocument9 pagesFixed Income Class Examples ADebashis MallickNo ratings yet

- Quantitative Problems Chapter 3Document5 pagesQuantitative Problems Chapter 3Shahzain RafiqNo ratings yet

- SFE Interest Futures PricingDocument9 pagesSFE Interest Futures Pricingron22No ratings yet

- Term Structure TutorialDocument6 pagesTerm Structure TutorialShivam PathakNo ratings yet

- Part II - Chapter4 Time and Resource Allocation, Chapter 4 - Allocating Resources Over TimeDocument27 pagesPart II - Chapter4 Time and Resource Allocation, Chapter 4 - Allocating Resources Over TimeDuy TânNo ratings yet

- Margin UpdatedDocument35 pagesMargin Updatedparinita raviNo ratings yet

- Yield Curve: DR HK Pradhan XLRI JamshedpurDocument38 pagesYield Curve: DR HK Pradhan XLRI JamshedpurzerocoolrklNo ratings yet

- Soln CH 14 Bond PricesDocument12 pagesSoln CH 14 Bond PricesSilviu TrebuianNo ratings yet

- Derivatives ActivitiesDocument9 pagesDerivatives Activitiesjoong wanNo ratings yet

- Accounting-Hire Purchase and Installment Sale Transactions-1653399056860714Document48 pagesAccounting-Hire Purchase and Installment Sale Transactions-1653399056860714Badhrinath ShanmugamNo ratings yet

- Premium Calculation: Juhi Sharma Rajat Gupta Deepak SinghDocument23 pagesPremium Calculation: Juhi Sharma Rajat Gupta Deepak SinghDeepak SinghNo ratings yet

- Financial MnagementDocument16 pagesFinancial MnagementbirhanuNo ratings yet

- Que 5 - Bond MathematicsDocument25 pagesQue 5 - Bond MathematicsPushkaraj SaveNo ratings yet

- Bond Valuation SolutionsDocument7 pagesBond Valuation SolutionsShubham AggarwalNo ratings yet

- Bond Project - Luka RadosevicDocument17 pagesBond Project - Luka RadosevicKate RuzevichNo ratings yet

- Module 1 - Time Value of Money Handout For LMS 2020Document8 pagesModule 1 - Time Value of Money Handout For LMS 2020sandeshNo ratings yet

- Security Analysis & Portfolio Management: Name Muqaddas ZubairDocument7 pagesSecurity Analysis & Portfolio Management: Name Muqaddas ZubairMahlab RajpootNo ratings yet

- Solution Manual For Financial Institutions Markets and Money Kidwell Blackwell Whidbee Sias 11th EditionDocument8 pagesSolution Manual For Financial Institutions Markets and Money Kidwell Blackwell Whidbee Sias 11th EditionAmandaMartinxdwj100% (40)

- F9 Financial Management ACCADocument4 pagesF9 Financial Management ACCAFaheem AhmadNo ratings yet

- Quantitative Problem Chapter 3: Solution: PVDocument5 pagesQuantitative Problem Chapter 3: Solution: PVAni SubelianiNo ratings yet

- CF 4 2016Document43 pagesCF 4 2016Siddhartha PatraNo ratings yet

- FINA 4400: Financial Markets and Institutions: Help TopicsDocument17 pagesFINA 4400: Financial Markets and Institutions: Help TopicsMr. Copernicus0% (1)

- Compute Clean Price, Total Price and Modified DurationDocument20 pagesCompute Clean Price, Total Price and Modified Durationparv salechaNo ratings yet

- Mmo Most Important Question SolutionDocument4 pagesMmo Most Important Question SolutionAshish GoelNo ratings yet

- The Time Value of MoneyDocument29 pagesThe Time Value of Moneymasandvishal50% (2)

- CH 5 SNDocument17 pagesCH 5 SNSam TnNo ratings yet

- Assignment No 6 - FM Actual Summer 2020 Furqan Farooq-18292Document37 pagesAssignment No 6 - FM Actual Summer 2020 Furqan Farooq-18292Furqan Farooq Vadharia100% (1)

- Economics Final Exam SolutionsDocument4 pagesEconomics Final Exam SolutionsPower GirlsNo ratings yet

- Ca Final SFM Super 100 Class 6 To 10 1Document32 pagesCa Final SFM Super 100 Class 6 To 10 1Deepsikha maitiNo ratings yet

- CH 4Document22 pagesCH 4Asif Abdullah KhanNo ratings yet

- Topic 3 Interest RatesDocument6 pagesTopic 3 Interest RatesRamsha ShafeelNo ratings yet

- Module 5 Exercises - JFCDocument7 pagesModule 5 Exercises - JFCJARED DARREN ONGNo ratings yet

- Bond Practice Solutions PDFDocument3 pagesBond Practice Solutions PDFRob GordonNo ratings yet

- GF520 Unit2 Assignment CorrectionsDocument7 pagesGF520 Unit2 Assignment CorrectionsPriscilla Morales86% (7)

- SFM-Ans - Unit 2 Fixed Income Securities EduDocument14 pagesSFM-Ans - Unit 2 Fixed Income Securities EduJenneey D RajaniNo ratings yet

- MNGT 604 Day2 Problem Set Solutions-2Document7 pagesMNGT 604 Day2 Problem Set Solutions-2harini muthuNo ratings yet

- Chapter 12 Bond Portfolio MGMTDocument41 pagesChapter 12 Bond Portfolio MGMTsharktale2828No ratings yet

- CPA Review Notes 2019 - BEC (Business Environment Concepts)From EverandCPA Review Notes 2019 - BEC (Business Environment Concepts)Rating: 4 out of 5 stars4/5 (9)

- Sumeet Prajapati - ResumeDocument3 pagesSumeet Prajapati - ResumeChandru JeyaramNo ratings yet

- Study of Mutual Models in Insurance - Report - 03 OctDocument53 pagesStudy of Mutual Models in Insurance - Report - 03 OctChandru JeyaramNo ratings yet

- Fee Structure and Schedule 2021-23Document2 pagesFee Structure and Schedule 2021-23Chandru JeyaramNo ratings yet

- Session 2 IllustrationDocument5 pagesSession 2 IllustrationChandru JeyaramNo ratings yet

- The Contents 1 Cyber Hull 2 Cyber Hull InventoryDocument28 pagesThe Contents 1 Cyber Hull 2 Cyber Hull InventoryChandru JeyaramNo ratings yet

- Becg - L1Document66 pagesBecg - L1Chandru JeyaramNo ratings yet

- Sessions 3 and 4Document7 pagesSessions 3 and 4Chandru JeyaramNo ratings yet

- ERM-Group 6 - AckoDocument11 pagesERM-Group 6 - AckoChandru JeyaramNo ratings yet

- UMW Toyota Motor SDN BHD (60576-K) Price List For Labuan Effective From 15 December 2020Document1 pageUMW Toyota Motor SDN BHD (60576-K) Price List For Labuan Effective From 15 December 2020ProAutoNo ratings yet

- Cert 2307V2018 Global MirakelDocument2 pagesCert 2307V2018 Global MirakelLeo BagtasNo ratings yet

- Manonmaniam Sundaranar University: Insurance and Risk ManagementDocument190 pagesManonmaniam Sundaranar University: Insurance and Risk ManagementDevanshu JulkaNo ratings yet

- Ironman AgreementDocument6 pagesIronman AgreementColin MerryNo ratings yet

- Pearsons Federal Taxation 2019 Comprehensive 32nd Edition Rupert Solutions ManualDocument15 pagesPearsons Federal Taxation 2019 Comprehensive 32nd Edition Rupert Solutions Manualbannerolglycide41uud100% (25)

- Module 8 Financial Literacy Pasiapasumbal 1Document16 pagesModule 8 Financial Literacy Pasiapasumbal 1Khristel Alcayde83% (6)

- Exide Life Guaranteed Wealth Plus BrochureDocument13 pagesExide Life Guaranteed Wealth Plus BrochureRajesh ExperisNo ratings yet

- Swimming For Autistic Children by Cerebral Palsy Alliance: Presenting by Pawandeep Kaur STUDENT ID 1067235Document17 pagesSwimming For Autistic Children by Cerebral Palsy Alliance: Presenting by Pawandeep Kaur STUDENT ID 1067235Pawan JohalNo ratings yet

- Midcap FundDocument1 pageMidcap FundAnurag NahataNo ratings yet

- Principles of InsuranceDocument4 pagesPrinciples of InsuranceVandita KhudiaNo ratings yet

- Cash Surrender Request FormDocument2 pagesCash Surrender Request Formkatrina gobNo ratings yet

- "Promotional Strategy in Life Insurance CompaniesDocument19 pages"Promotional Strategy in Life Insurance CompaniesChintan PatelNo ratings yet

- Basic Finance Assignment Bsa 1Document4 pagesBasic Finance Assignment Bsa 1Albert PetranNo ratings yet

- InsuranceDocument2 pagesInsuranceJanelle TabuzoNo ratings yet

- Bonifacio Brothers v. Mora, 20 SCRA 261Document2 pagesBonifacio Brothers v. Mora, 20 SCRA 261Sopongco ColeenNo ratings yet

- MACN-A018 - Universal Affidavit of Termination of All CORPORATE CONTRACTS-Inola Enapay Bey Ex Relatione ANNETTA JAMES BROWN 8+30+22Document5 pagesMACN-A018 - Universal Affidavit of Termination of All CORPORATE CONTRACTS-Inola Enapay Bey Ex Relatione ANNETTA JAMES BROWN 8+30+22stonsomeNo ratings yet

- Neetu Vasudev SynopsisDocument4 pagesNeetu Vasudev Synopsis11naqviNo ratings yet

- TIRTHAN-JIBHI-JALORI ITINERARY-minDocument13 pagesTIRTHAN-JIBHI-JALORI ITINERARY-minAshish KansalNo ratings yet

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Document4 pagesForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961ElvisPresliiNo ratings yet

- Aon Risk Services Australia Limited: Ian JonesDocument29 pagesAon Risk Services Australia Limited: Ian JonesGarry HouseNo ratings yet

- Insurance Intermediaries: Agents IC 223: Fundamentals of InsuranceDocument10 pagesInsurance Intermediaries: Agents IC 223: Fundamentals of InsuranceMerupranta SaikiaNo ratings yet

- Unit 12 - MCQs BBN AnswersDocument50 pagesUnit 12 - MCQs BBN Answersايهاب العنبوسيNo ratings yet

- CarriersDocument90 pagesCarriersabdel amarillasNo ratings yet

- Annuities and Sinking FundsDocument34 pagesAnnuities and Sinking FundsAnnie VNo ratings yet

- (Kotak) Insurance, February 02, 2023Document11 pages(Kotak) Insurance, February 02, 2023Deepak KhatwaniNo ratings yet

- Gpa Proposal FormatDocument3 pagesGpa Proposal FormatMargaret Quiachon ChiuNo ratings yet

- Vfis A&s RenewalDocument6 pagesVfis A&s RenewalmarNo ratings yet

- 1996 September - David Hall - Privatisation in Health Services in Central and Eastern EuropeDocument11 pages1996 September - David Hall - Privatisation in Health Services in Central and Eastern EuropeSusanne Namer-WaldenstromNo ratings yet

- Malayan Insurance Vs CA March 20,1997Document2 pagesMalayan Insurance Vs CA March 20,1997Alvin-Evelyn GuloyNo ratings yet

Download as xlsx, pdf, or txt

You might also like

- Solution Manual For Fundamentals of Corporate Finance 7th Canadian Edition Richard A BrealeyDocument22 pagesSolution Manual For Fundamentals of Corporate Finance 7th Canadian Edition Richard A BrealeyKarinaMasonprdbc100% (50)

- Im AnswersDocument6 pagesIm Answersromal_talwarNo ratings yet

- Quantitative Problems Chapter 3Document5 pagesQuantitative Problems Chapter 3Khadija ShabbirNo ratings yet

- Suggested Solutions Assignment 02: Operational Risk ManagementDocument5 pagesSuggested Solutions Assignment 02: Operational Risk ManagementDigong Smaz50% (2)

- Problem Set 1 - Bonds and Time Value of MoneyDocument4 pagesProblem Set 1 - Bonds and Time Value of Moneymattgodftey1No ratings yet

- Convexity and DurationDocument20 pagesConvexity and DurationNikka CasyaoNo ratings yet

- Lecture 10 502 1ppDocument12 pagesLecture 10 502 1ppJohn SmithNo ratings yet

- Lec 12Document5 pagesLec 12Ryan GroffNo ratings yet

- Bodie10ce SM CH15Document13 pagesBodie10ce SM CH15William GrignonNo ratings yet

- Present ValueDocument38 pagesPresent Valuemarjannaseri77100% (1)

- Chapter 12 Bond Prices and YieldsDocument15 pagesChapter 12 Bond Prices and YieldsSharoz SheikhNo ratings yet

- Unit 5 Bonds and Stock Valuation and Cost of CapitalDocument14 pagesUnit 5 Bonds and Stock Valuation and Cost of CapitalGizaw BelayNo ratings yet

- Interest Rates Chapter 4 (Part1) : Geng NiuDocument49 pagesInterest Rates Chapter 4 (Part1) : Geng NiuegaNo ratings yet

- 1.02 The Time Value of Money in Finance - AnswersDocument4 pages1.02 The Time Value of Money in Finance - AnswersThe SpectreNo ratings yet

- Activity Sheet In: Business FinanceDocument8 pagesActivity Sheet In: Business FinanceCatherine Larce100% (1)

- Bond Return Valuatio DurationDocument63 pagesBond Return Valuatio DurationSambi Reddy Gari NeelimaNo ratings yet

- 7 Additional Solved Problems 6Document14 pages7 Additional Solved Problems 6Pranoy SarkarNo ratings yet

- Quiz 10 - CH 16Document4 pagesQuiz 10 - CH 16JamNo ratings yet

- Interest Rates Chapter 4 (Part1) : Geng NiuDocument52 pagesInterest Rates Chapter 4 (Part1) : Geng NiuegaNo ratings yet

- Interest Rates and Exchange RatesDocument5 pagesInterest Rates and Exchange RatesPutriNo ratings yet

- Excel TVM Functions PDFDocument8 pagesExcel TVM Functions PDFVishal GoelNo ratings yet

- BKM9e Answers Chap015 PDFDocument11 pagesBKM9e Answers Chap015 PDFLê Chấn PhongNo ratings yet

- BMA 12e SM CH 25 Final PDFDocument16 pagesBMA 12e SM CH 25 Final PDFNikhil ChadhaNo ratings yet

- Fixed Income Class Examples ADocument9 pagesFixed Income Class Examples ADebashis MallickNo ratings yet

- Quantitative Problems Chapter 3Document5 pagesQuantitative Problems Chapter 3Shahzain RafiqNo ratings yet

- SFE Interest Futures PricingDocument9 pagesSFE Interest Futures Pricingron22No ratings yet

- Term Structure TutorialDocument6 pagesTerm Structure TutorialShivam PathakNo ratings yet

- Part II - Chapter4 Time and Resource Allocation, Chapter 4 - Allocating Resources Over TimeDocument27 pagesPart II - Chapter4 Time and Resource Allocation, Chapter 4 - Allocating Resources Over TimeDuy TânNo ratings yet

- Margin UpdatedDocument35 pagesMargin Updatedparinita raviNo ratings yet

- Yield Curve: DR HK Pradhan XLRI JamshedpurDocument38 pagesYield Curve: DR HK Pradhan XLRI JamshedpurzerocoolrklNo ratings yet

- Soln CH 14 Bond PricesDocument12 pagesSoln CH 14 Bond PricesSilviu TrebuianNo ratings yet

- Derivatives ActivitiesDocument9 pagesDerivatives Activitiesjoong wanNo ratings yet

- Accounting-Hire Purchase and Installment Sale Transactions-1653399056860714Document48 pagesAccounting-Hire Purchase and Installment Sale Transactions-1653399056860714Badhrinath ShanmugamNo ratings yet

- Premium Calculation: Juhi Sharma Rajat Gupta Deepak SinghDocument23 pagesPremium Calculation: Juhi Sharma Rajat Gupta Deepak SinghDeepak SinghNo ratings yet

- Financial MnagementDocument16 pagesFinancial MnagementbirhanuNo ratings yet

- Que 5 - Bond MathematicsDocument25 pagesQue 5 - Bond MathematicsPushkaraj SaveNo ratings yet

- Bond Valuation SolutionsDocument7 pagesBond Valuation SolutionsShubham AggarwalNo ratings yet

- Bond Project - Luka RadosevicDocument17 pagesBond Project - Luka RadosevicKate RuzevichNo ratings yet

- Module 1 - Time Value of Money Handout For LMS 2020Document8 pagesModule 1 - Time Value of Money Handout For LMS 2020sandeshNo ratings yet

- Security Analysis & Portfolio Management: Name Muqaddas ZubairDocument7 pagesSecurity Analysis & Portfolio Management: Name Muqaddas ZubairMahlab RajpootNo ratings yet

- Solution Manual For Financial Institutions Markets and Money Kidwell Blackwell Whidbee Sias 11th EditionDocument8 pagesSolution Manual For Financial Institutions Markets and Money Kidwell Blackwell Whidbee Sias 11th EditionAmandaMartinxdwj100% (40)

- F9 Financial Management ACCADocument4 pagesF9 Financial Management ACCAFaheem AhmadNo ratings yet

- Quantitative Problem Chapter 3: Solution: PVDocument5 pagesQuantitative Problem Chapter 3: Solution: PVAni SubelianiNo ratings yet

- CF 4 2016Document43 pagesCF 4 2016Siddhartha PatraNo ratings yet

- FINA 4400: Financial Markets and Institutions: Help TopicsDocument17 pagesFINA 4400: Financial Markets and Institutions: Help TopicsMr. Copernicus0% (1)

- Compute Clean Price, Total Price and Modified DurationDocument20 pagesCompute Clean Price, Total Price and Modified Durationparv salechaNo ratings yet

- Mmo Most Important Question SolutionDocument4 pagesMmo Most Important Question SolutionAshish GoelNo ratings yet

- The Time Value of MoneyDocument29 pagesThe Time Value of Moneymasandvishal50% (2)

- CH 5 SNDocument17 pagesCH 5 SNSam TnNo ratings yet

- Assignment No 6 - FM Actual Summer 2020 Furqan Farooq-18292Document37 pagesAssignment No 6 - FM Actual Summer 2020 Furqan Farooq-18292Furqan Farooq Vadharia100% (1)

- Economics Final Exam SolutionsDocument4 pagesEconomics Final Exam SolutionsPower GirlsNo ratings yet

- Ca Final SFM Super 100 Class 6 To 10 1Document32 pagesCa Final SFM Super 100 Class 6 To 10 1Deepsikha maitiNo ratings yet

- CH 4Document22 pagesCH 4Asif Abdullah KhanNo ratings yet

- Topic 3 Interest RatesDocument6 pagesTopic 3 Interest RatesRamsha ShafeelNo ratings yet

- Module 5 Exercises - JFCDocument7 pagesModule 5 Exercises - JFCJARED DARREN ONGNo ratings yet

- Bond Practice Solutions PDFDocument3 pagesBond Practice Solutions PDFRob GordonNo ratings yet

- GF520 Unit2 Assignment CorrectionsDocument7 pagesGF520 Unit2 Assignment CorrectionsPriscilla Morales86% (7)

- SFM-Ans - Unit 2 Fixed Income Securities EduDocument14 pagesSFM-Ans - Unit 2 Fixed Income Securities EduJenneey D RajaniNo ratings yet

- MNGT 604 Day2 Problem Set Solutions-2Document7 pagesMNGT 604 Day2 Problem Set Solutions-2harini muthuNo ratings yet

- Chapter 12 Bond Portfolio MGMTDocument41 pagesChapter 12 Bond Portfolio MGMTsharktale2828No ratings yet

- CPA Review Notes 2019 - BEC (Business Environment Concepts)From EverandCPA Review Notes 2019 - BEC (Business Environment Concepts)Rating: 4 out of 5 stars4/5 (9)

- Sumeet Prajapati - ResumeDocument3 pagesSumeet Prajapati - ResumeChandru JeyaramNo ratings yet

- Study of Mutual Models in Insurance - Report - 03 OctDocument53 pagesStudy of Mutual Models in Insurance - Report - 03 OctChandru JeyaramNo ratings yet

- Fee Structure and Schedule 2021-23Document2 pagesFee Structure and Schedule 2021-23Chandru JeyaramNo ratings yet

- Session 2 IllustrationDocument5 pagesSession 2 IllustrationChandru JeyaramNo ratings yet

- The Contents 1 Cyber Hull 2 Cyber Hull InventoryDocument28 pagesThe Contents 1 Cyber Hull 2 Cyber Hull InventoryChandru JeyaramNo ratings yet

- Becg - L1Document66 pagesBecg - L1Chandru JeyaramNo ratings yet

- Sessions 3 and 4Document7 pagesSessions 3 and 4Chandru JeyaramNo ratings yet

- ERM-Group 6 - AckoDocument11 pagesERM-Group 6 - AckoChandru JeyaramNo ratings yet

- UMW Toyota Motor SDN BHD (60576-K) Price List For Labuan Effective From 15 December 2020Document1 pageUMW Toyota Motor SDN BHD (60576-K) Price List For Labuan Effective From 15 December 2020ProAutoNo ratings yet

- Cert 2307V2018 Global MirakelDocument2 pagesCert 2307V2018 Global MirakelLeo BagtasNo ratings yet

- Manonmaniam Sundaranar University: Insurance and Risk ManagementDocument190 pagesManonmaniam Sundaranar University: Insurance and Risk ManagementDevanshu JulkaNo ratings yet

- Ironman AgreementDocument6 pagesIronman AgreementColin MerryNo ratings yet

- Pearsons Federal Taxation 2019 Comprehensive 32nd Edition Rupert Solutions ManualDocument15 pagesPearsons Federal Taxation 2019 Comprehensive 32nd Edition Rupert Solutions Manualbannerolglycide41uud100% (25)

- Module 8 Financial Literacy Pasiapasumbal 1Document16 pagesModule 8 Financial Literacy Pasiapasumbal 1Khristel Alcayde83% (6)

- Exide Life Guaranteed Wealth Plus BrochureDocument13 pagesExide Life Guaranteed Wealth Plus BrochureRajesh ExperisNo ratings yet

- Swimming For Autistic Children by Cerebral Palsy Alliance: Presenting by Pawandeep Kaur STUDENT ID 1067235Document17 pagesSwimming For Autistic Children by Cerebral Palsy Alliance: Presenting by Pawandeep Kaur STUDENT ID 1067235Pawan JohalNo ratings yet

- Midcap FundDocument1 pageMidcap FundAnurag NahataNo ratings yet

- Principles of InsuranceDocument4 pagesPrinciples of InsuranceVandita KhudiaNo ratings yet

- Cash Surrender Request FormDocument2 pagesCash Surrender Request Formkatrina gobNo ratings yet

- "Promotional Strategy in Life Insurance CompaniesDocument19 pages"Promotional Strategy in Life Insurance CompaniesChintan PatelNo ratings yet

- Basic Finance Assignment Bsa 1Document4 pagesBasic Finance Assignment Bsa 1Albert PetranNo ratings yet

- InsuranceDocument2 pagesInsuranceJanelle TabuzoNo ratings yet

- Bonifacio Brothers v. Mora, 20 SCRA 261Document2 pagesBonifacio Brothers v. Mora, 20 SCRA 261Sopongco ColeenNo ratings yet

- MACN-A018 - Universal Affidavit of Termination of All CORPORATE CONTRACTS-Inola Enapay Bey Ex Relatione ANNETTA JAMES BROWN 8+30+22Document5 pagesMACN-A018 - Universal Affidavit of Termination of All CORPORATE CONTRACTS-Inola Enapay Bey Ex Relatione ANNETTA JAMES BROWN 8+30+22stonsomeNo ratings yet

- Neetu Vasudev SynopsisDocument4 pagesNeetu Vasudev Synopsis11naqviNo ratings yet

- TIRTHAN-JIBHI-JALORI ITINERARY-minDocument13 pagesTIRTHAN-JIBHI-JALORI ITINERARY-minAshish KansalNo ratings yet

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Document4 pagesForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961ElvisPresliiNo ratings yet

- Aon Risk Services Australia Limited: Ian JonesDocument29 pagesAon Risk Services Australia Limited: Ian JonesGarry HouseNo ratings yet

- Insurance Intermediaries: Agents IC 223: Fundamentals of InsuranceDocument10 pagesInsurance Intermediaries: Agents IC 223: Fundamentals of InsuranceMerupranta SaikiaNo ratings yet

- Unit 12 - MCQs BBN AnswersDocument50 pagesUnit 12 - MCQs BBN Answersايهاب العنبوسيNo ratings yet

- CarriersDocument90 pagesCarriersabdel amarillasNo ratings yet

- Annuities and Sinking FundsDocument34 pagesAnnuities and Sinking FundsAnnie VNo ratings yet

- (Kotak) Insurance, February 02, 2023Document11 pages(Kotak) Insurance, February 02, 2023Deepak KhatwaniNo ratings yet

- Gpa Proposal FormatDocument3 pagesGpa Proposal FormatMargaret Quiachon ChiuNo ratings yet

- Vfis A&s RenewalDocument6 pagesVfis A&s RenewalmarNo ratings yet

- 1996 September - David Hall - Privatisation in Health Services in Central and Eastern EuropeDocument11 pages1996 September - David Hall - Privatisation in Health Services in Central and Eastern EuropeSusanne Namer-WaldenstromNo ratings yet

- Malayan Insurance Vs CA March 20,1997Document2 pagesMalayan Insurance Vs CA March 20,1997Alvin-Evelyn GuloyNo ratings yet