Download as doc, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5823)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Practical Accounting 1Document6 pagesPractical Accounting 1glrosaaa c100% (1)

- Latihan Soal PGDocument12 pagesLatihan Soal PGshafirasrjNo ratings yet

- A. Universal PartnershipDocument3 pagesA. Universal Partnershipglrosaaa cNo ratings yet

- Overview of Strategic MarketingDocument5 pagesOverview of Strategic Marketingglrosaaa cNo ratings yet

- A. Business B. Mutual Benefit C. Credit D. None of The AboveDocument3 pagesA. Business B. Mutual Benefit C. Credit D. None of The Aboveglrosaaa cNo ratings yet

- 12correction of Errors - ExerciseDocument3 pages12correction of Errors - Exerciseglrosaaa cNo ratings yet

- Notes Payable and Debt RestructuringDocument14 pagesNotes Payable and Debt Restructuringglrosaaa cNo ratings yet

- ACC 211 Group Discussion - Bonds PayableDocument2 pagesACC 211 Group Discussion - Bonds Payableglrosaaa cNo ratings yet

- ACC 211 Bonds Payable - AKDocument4 pagesACC 211 Bonds Payable - AKglrosaaa cNo ratings yet

- JouDocument15 pagesJouglrosaaa cNo ratings yet

- Accounting For Income TaxDocument12 pagesAccounting For Income Taxglrosaaa cNo ratings yet

- Types of Financial InstitutionsDocument32 pagesTypes of Financial Institutionsglrosaaa cNo ratings yet

- CBM 112 ReviewerDocument1 pageCBM 112 Reviewerglrosaaa cNo ratings yet

- ACC 211 Review AssignmentDocument5 pagesACC 211 Review Assignmentglrosaaa cNo ratings yet

- Receive and Process Reservations in Hotel and Travel IndustriesDocument68 pagesReceive and Process Reservations in Hotel and Travel IndustriesChin DhoNo ratings yet

- Steps 4 Opening A.CDocument20 pagesSteps 4 Opening A.CBipinNo ratings yet

- ImpairmentDocument45 pagesImpairmentnati100% (1)

- Managing in A Global Environment: Learning ObjectivesDocument27 pagesManaging in A Global Environment: Learning ObjectivesaroojNo ratings yet

- Planning Reports and Proposals: 12/28/20 Chapter 11-1Document27 pagesPlanning Reports and Proposals: 12/28/20 Chapter 11-1H. U. KonainNo ratings yet

- Fundamentals of HRM ch01Document17 pagesFundamentals of HRM ch01korpseeNo ratings yet

- Case Study 1 (Suggested Answer)Document3 pagesCase Study 1 (Suggested Answer)NurnazihaNo ratings yet

- Documentary Credit Application UKDocument3 pagesDocumentary Credit Application UKtamer abdelhadyNo ratings yet

- Douglas County School District Board of Trustees Agenda: Sept. 9Document9 pagesDouglas County School District Board of Trustees Agenda: Sept. 9cvalleytimesNo ratings yet

- Amortization TableDocument3 pagesAmortization TableIop A MopNo ratings yet

- The Pavilion II - Investment NoteDocument37 pagesThe Pavilion II - Investment NoteRamkumar KNo ratings yet

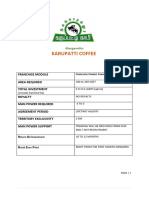

- Akc Franchise PDFDocument4 pagesAkc Franchise PDFVky SpeaksNo ratings yet

- Black White Minimalist CV ResumeDocument1 pageBlack White Minimalist CV ResumeeyitayoolusayoNo ratings yet

- Data WarehousingDocument61 pagesData WarehousingSANJANA GHOSE 20MID0039No ratings yet

- This Online Bba Is Your Career Gamechanger! This Online Bba Is Your Career Gamechanger!Document4 pagesThis Online Bba Is Your Career Gamechanger! This Online Bba Is Your Career Gamechanger!spNo ratings yet

- TBEMDocument4 pagesTBEMSubhamay DebNo ratings yet

- T&F Proposal of EMP - Subhan FoodDocument18 pagesT&F Proposal of EMP - Subhan FoodJahangeer AsadNo ratings yet

- CHAPTER 3 Market ResearchDocument37 pagesCHAPTER 3 Market ResearchJojobaby51714No ratings yet

- Trencor IAR 2016Document96 pagesTrencor IAR 2016dmm tgctpNo ratings yet

- Business Whitepaper: Chia Network IncDocument31 pagesBusiness Whitepaper: Chia Network Incwiki.raoNo ratings yet

- Please See The Lectures in Sequence They Are Given: by CA Darshan D. Khare Recorded Jan 2019Document4 pagesPlease See The Lectures in Sequence They Are Given: by CA Darshan D. Khare Recorded Jan 2019vipinsingla1No ratings yet

- Small Business Loan Application Form For Individual - Sole - BDODocument2 pagesSmall Business Loan Application Form For Individual - Sole - BDOjunco111222No ratings yet

- Letter Pran RFLDocument6 pagesLetter Pran RFLHasan AtikNo ratings yet

- Literature Review: Effects of Employee Relation On OrganizationDocument5 pagesLiterature Review: Effects of Employee Relation On OrganizationHameeda ShoukatNo ratings yet

- SM MCQ 2Document20 pagesSM MCQ 2Anusha BhatiaNo ratings yet

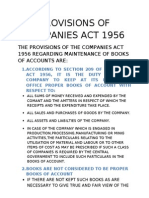

- Provisions of Companies Act 1956 FinalDocument9 pagesProvisions of Companies Act 1956 FinalDiwahar Sunder100% (1)

- Eng Abdalla Jamal C.V. - 1Document6 pagesEng Abdalla Jamal C.V. - 1broo jooNo ratings yet

- Ch4 of Org Behavior by JonesDocument47 pagesCh4 of Org Behavior by JonesGurpreet SeehraNo ratings yet