Download as pdf or txt

You might also like

- Hyundai Excavators Manuals and Parts Catalogs Sitemap 8bdfeDocument6 pagesHyundai Excavators Manuals and Parts Catalogs Sitemap 8bdfeJhoncyto BorysNo ratings yet

- List of Cement Companies in IndiaDocument6 pagesList of Cement Companies in Indiaygadiya50% (8)

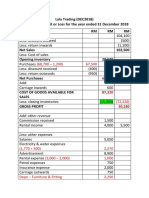

- Lala Trading DEC2018 - SOPL & SOFP DEC2018 AFTER ADJUSTMENTDocument3 pagesLala Trading DEC2018 - SOPL & SOFP DEC2018 AFTER ADJUSTMENTAFIQ RAFIQIN RAHMADNo ratings yet

- Marine CV Captain Template Modern Seafarer Application FormDocument1 pageMarine CV Captain Template Modern Seafarer Application FormMarine CVNo ratings yet

- The Baptist FaithDocument3 pagesThe Baptist FaithJeanelle Denosta100% (1)

- Pajuyo Vs CA DigestDocument1 pagePajuyo Vs CA DigestAngel Urbano100% (3)

- Solution Tax667 - Dec 2016Document7 pagesSolution Tax667 - Dec 2016Zahiratul QamarinaNo ratings yet

- UntitledDocument2 pagesUntitledNur AsnadirahNo ratings yet

- Answer Exercise 1Document2 pagesAnswer Exercise 1MUHAMMAD SYAZWAN MAZLANNo ratings yet

- Quiz 3: Profit Before Taxation - s4 (A) 67,069Document5 pagesQuiz 3: Profit Before Taxation - s4 (A) 67,069fujinlim98No ratings yet

- Suggested Answers TAX667 - DEC 2016Document7 pagesSuggested Answers TAX667 - DEC 2016diysNo ratings yet

- SOLUTION JUN 2018Document8 pagesSOLUTION JUN 2018faiqahn602No ratings yet

- SS Mar22 PDFDocument8 pagesSS Mar22 PDFuser mrmysteryNo ratings yet

- Solution June 2019Document8 pagesSolution June 2019faiqahn602No ratings yet

- Mark Scheme - AccountingDocument23 pagesMark Scheme - AccountingDanielNo ratings yet

- Solution Test 1Document3 pagesSolution Test 1anis izzatiNo ratings yet

- Solutions IhcDocument19 pagesSolutions IhcWahida AmalinNo ratings yet

- TUTO_SS_PYQJULY 2023Document2 pagesTUTO_SS_PYQJULY 20232022871354No ratings yet

- SCI Gerry LTD - Co. SolutionDocument1 pageSCI Gerry LTD - Co. SolutionSamira JahinNo ratings yet

- Company Tax SS Sept 2021 (Rate 2021) .For StudentsDocument3 pagesCompany Tax SS Sept 2021 (Rate 2021) .For StudentsizzahNo ratings yet

- Chapter 8 - Answer TutorialDocument3 pagesChapter 8 - Answer TutorialNUR ALEEYA MAISARAH BINTI MOHD NASIR (AS)No ratings yet

- Mark Scheme (Results) January 2016: Pearson Edexcel IAL in Accounting (WAC01) Paper 01Document21 pagesMark Scheme (Results) January 2016: Pearson Edexcel IAL in Accounting (WAC01) Paper 01hisakofelixNo ratings yet

- Less: Cost of Goods Sold: Capital ExpenditureDocument3 pagesLess: Cost of Goods Sold: Capital Expenditurefahim tusarNo ratings yet

- Solution NIngDocument3 pagesSolution NIngfahim tusarNo ratings yet

- Solution Far510 - Jun 2015Document8 pagesSolution Far510 - Jun 2015azila aliasNo ratings yet

- 2007 Jan U1 U2 PDFDocument31 pages2007 Jan U1 U2 PDFTharakaaNo ratings yet

- IT AY 2022-23 Probs On PGBPDocument15 pagesIT AY 2022-23 Probs On PGBPmojesnandas9935No ratings yet

- FAR Revision Answer Scheme Jul 2017Document8 pagesFAR Revision Answer Scheme Jul 2017Nurul Farahdatul Ashikin RamlanNo ratings yet

- Cost SheetDocument12 pagesCost SheetBharat ki BaatNo ratings yet

- Taxation Solution 2017 SeptemberDocument11 pagesTaxation Solution 2017 Septemberzezu zazaNo ratings yet

- Post-Closing Trial BalanceDocument8 pagesPost-Closing Trial BalanceNicole Andrea TuazonNo ratings yet

- Exam 2 Input Sheet-FinalDocument24 pagesExam 2 Input Sheet-Finalさくら樱花No ratings yet

- Happyjacline Robert Njako Acc128 BHRM 2Document8 pagesHappyjacline Robert Njako Acc128 BHRM 2jupiter stationeryNo ratings yet

- PGBP Part 2 SolutionDocument14 pagesPGBP Part 2 SolutionDhruv SetiaNo ratings yet

- Profit and Gains of Business or Profession (PGBP) : Dr. Sonam Topgay BhutiaDocument8 pagesProfit and Gains of Business or Profession (PGBP) : Dr. Sonam Topgay BhutiaUmesh SharmaNo ratings yet

- Assignment 2Document6 pagesAssignment 2TAWHID ARMANNo ratings yet

- Taxation Solution 2018 SeptemberDocument9 pagesTaxation Solution 2018 SeptemberIffah NasuhaaNo ratings yet

- Solution To Q1 Summer 2022Document2 pagesSolution To Q1 Summer 2022dgornik021No ratings yet

- SS Project January 2023Document2 pagesSS Project January 2023NUR AFFIDAH LEENo ratings yet

- Business Income Template (Ain)Document9 pagesBusiness Income Template (Ain)Imran FarhanNo ratings yet

- Chapter7 - Unadjusted Principles - of - Accounts - For - Caribbean - StudentsDocument11 pagesChapter7 - Unadjusted Principles - of - Accounts - For - Caribbean - StudentsZahra BaptisteNo ratings yet

- Rise School of Accountancy: Suggested Solution Test 08Document2 pagesRise School of Accountancy: Suggested Solution Test 08iamneonkingNo ratings yet

- Solution To Compiled QuestionsDocument7 pagesSolution To Compiled Questionslovia mensahNo ratings yet

- Solution Test 2 (1) June 19Document5 pagesSolution Test 2 (1) June 19Nur Dina AbsbNo ratings yet

- Individual AssignmentDocument22 pagesIndividual AssignmentEda LimNo ratings yet

- SolutionDocument4 pagesSolutionIGO SAUCENo ratings yet

- Assets.: (Vi) Due To Lack of Information, Depreciation Has Not Been Provided On FixedDocument6 pagesAssets.: (Vi) Due To Lack of Information, Depreciation Has Not Been Provided On FixedMehul Gupta100% (1)

- Gwapa Ko Chapter 3 Tax 1Document10 pagesGwapa Ko Chapter 3 Tax 1adarose romaresNo ratings yet

- Solution Lecture 4 Part 2: Financial Statement With Adjustments Question 1 (A) AdjustmentsDocument7 pagesSolution Lecture 4 Part 2: Financial Statement With Adjustments Question 1 (A) AdjustmentsIsyraf Hatim Mohd TamizamNo ratings yet

- Tax267 Ex3Document5 pagesTax267 Ex3SITI NUR DIANA SELAMATNo ratings yet

- Fac1601 Exam Pack 2018Document98 pagesFac1601 Exam Pack 2018OlebogengPNo ratings yet

- 4 A TUTORIAL 4 AnswerDocument6 pages4 A TUTORIAL 4 AnswerLee HansNo ratings yet

- TAX317 SS JUN2019. (Rate 2021.for Students)Document10 pagesTAX317 SS JUN2019. (Rate 2021.for Students)izzahNo ratings yet

- Unrealized Gain On Sale of Equipment: Cost ModelDocument25 pagesUnrealized Gain On Sale of Equipment: Cost ModelLove FreddyNo ratings yet

- Problem 12 Preparing The Financial Statements 4Document1 pageProblem 12 Preparing The Financial Statements 4Chunne LinqueNo ratings yet

- Exam 14 October 2012, Answers Exam 14 October 2012, AnswersDocument9 pagesExam 14 October 2012, Answers Exam 14 October 2012, AnswerscandiceNo ratings yet

- The Statement of Cash Flows Problems 5-1. (Currency Company)Document7 pagesThe Statement of Cash Flows Problems 5-1. (Currency Company)Marcos DmitriNo ratings yet

- Tugas 20.445cs4Document8 pagesTugas 20.445cs4ina aktNo ratings yet

- Example 2Document4 pagesExample 2Raudhatun Nisa'No ratings yet

- Fac2601-2013-6 - Answers PDFDocument9 pagesFac2601-2013-6 - Answers PDFcandiceNo ratings yet

- AFS SolutionsDocument19 pagesAFS SolutionsRolivhuwaNo ratings yet

- ABFT2020 Tutorial 12 Busines ExpenseDocument6 pagesABFT2020 Tutorial 12 Busines ExpensePUI TUNG CHONGNo ratings yet

- Wac01 w15 Ms 01Document21 pagesWac01 w15 Ms 01mohamedyanaal2020No ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- J.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineNo ratings yet

- Weekly Lessonplan - Oct2022Document3 pagesWeekly Lessonplan - Oct2022HANIS IZYAN MAT ISANo ratings yet

- Topic 6 TutorialDocument16 pagesTopic 6 TutorialHANIS IZYAN MAT ISANo ratings yet

- Topic 2 Residence Status For IndividualDocument23 pagesTopic 2 Residence Status For IndividualHANIS IZYAN MAT ISANo ratings yet

- Topic 1 Basis of Malaysian TaxationDocument15 pagesTopic 1 Basis of Malaysian TaxationHANIS IZYAN MAT ISANo ratings yet

- Oceanic Wireless Network, Inc. V. Cir G.R. NO. 148380 December 9, 2005 FactsDocument2 pagesOceanic Wireless Network, Inc. V. Cir G.R. NO. 148380 December 9, 2005 FactsGyelamagne EstradaNo ratings yet

- Case Study Parole JetherDocument6 pagesCase Study Parole JetherBryan ChuNo ratings yet

- Exercício Do Mês: October 2012 Wish / If OnlyDocument0 pagesExercício Do Mês: October 2012 Wish / If OnlyDudu LauraNo ratings yet

- GR 113213 - Wright V Court of AppealsDocument1 pageGR 113213 - Wright V Court of AppealsApple Gee Libo-on100% (1)

- Adiabatic and Isothermal ProcessesDocument2 pagesAdiabatic and Isothermal ProcessesphydotsiNo ratings yet

- Hand Out#: Far 01 Topic: Accounting Process Classification: TheoriesDocument3 pagesHand Out#: Far 01 Topic: Accounting Process Classification: TheoriesJolaica DiocolanoNo ratings yet

- Chordu Guitar Chords Ensamble Tejedora Manabita Expresarte Música Chordsheet Id GiY7U7AjCaYDocument3 pagesChordu Guitar Chords Ensamble Tejedora Manabita Expresarte Música Chordsheet Id GiY7U7AjCaYAngelita;3 Neko:3No ratings yet

- International Arbitration Conference - MNLU Mumbai - 6 December PDFDocument4 pagesInternational Arbitration Conference - MNLU Mumbai - 6 December PDFRCR 75No ratings yet

- A00-02 - Grid Setout PlanDocument1 pageA00-02 - Grid Setout PlanazikNo ratings yet

- Leaflet - HDFC Balanced Advantage Fund - June 2024Document3 pagesLeaflet - HDFC Balanced Advantage Fund - June 2024DeepakNo ratings yet

- CA San BernardinoDocument6 pagesCA San BernardinotressanavaltaNo ratings yet

- CA1 NewDocument39 pagesCA1 NewGarcia Rowell S.100% (1)

- Appointment Letter FormatDocument9 pagesAppointment Letter FormatNiraliNo ratings yet

- United States Court of Appeals, Eleventh CircuitDocument5 pagesUnited States Court of Appeals, Eleventh CircuitScribd Government DocsNo ratings yet

- Tata Technologies Limited: Corporate Identity Number: U72200PN1994PLC013313Document436 pagesTata Technologies Limited: Corporate Identity Number: U72200PN1994PLC013313RoshanNo ratings yet

- Contracts - Case Briefs - PriyanshDocument87 pagesContracts - Case Briefs - PriyanshManju Nadger100% (1)

- Sex HD MOBILE Pics Ann Angel XXX Ann Angel Ideal Booty Playmate 5Document1 pageSex HD MOBILE Pics Ann Angel XXX Ann Angel Ideal Booty Playmate 5mariawalker47kNo ratings yet

- 620 MessagesDocument518 pages620 MessagesMan YauNo ratings yet

- How To Block Storage Location - SCNDocument4 pagesHow To Block Storage Location - SCNSushil KanuNo ratings yet

- Audit of Investment - 2Document4 pagesAudit of Investment - 2Juvy Dimaano0% (1)

- Appeal Section 374 CRPCDocument11 pagesAppeal Section 374 CRPCHet DoshiNo ratings yet

- Aritcle of Incorporation CodedDocument8 pagesAritcle of Incorporation CodedmmmnnyskrtNo ratings yet

- But The Fruit of The Spirit Is LoveDocument1 pageBut The Fruit of The Spirit Is LovextneNo ratings yet

- Health Law Report CompleteDocument46 pagesHealth Law Report CompleteMeenakshiNo ratings yet

- Vault-Best-Practice-IPJ & Vault StructureDocument14 pagesVault-Best-Practice-IPJ & Vault StructuretKc1234No ratings yet