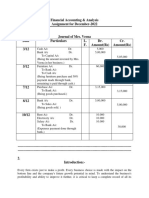

Financial Accounting Analysis Dec 2022 Rfaxjt

Financial Accounting Analysis Dec 2022 Rfaxjt

You might also like

- Recording Transactions: Using The Method of Journal EntriesDocument50 pagesRecording Transactions: Using The Method of Journal EntriesHasanAbdullah100% (1)

- Financial Accounting Analysis z1xzdfDocument11 pagesFinancial Accounting Analysis z1xzdfJerrin JoseNo ratings yet

- Financial Accounting Analysis PLGXQCDocument11 pagesFinancial Accounting Analysis PLGXQCSagar KothawadeNo ratings yet

- Financial Accounting & Analysis - V - STDocument10 pagesFinancial Accounting & Analysis - V - STJeff Syn DeepNo ratings yet

- Financial Accounting & AnalysisDocument9 pagesFinancial Accounting & Analysisshriyansh jainNo ratings yet

- Vipin FinanceDocument10 pagesVipin Financeshivansh tiwariNo ratings yet

- Financial-Accounting-Analysis-Dec 2022Document10 pagesFinancial-Accounting-Analysis-Dec 2022Rameshwar BhatiNo ratings yet

- Financial Accounting and AnalysisDocument13 pagesFinancial Accounting and AnalysisAditya Raj DuttaNo ratings yet

- Financial AccountingDocument10 pagesFinancial Accountingsakshi khadiyaNo ratings yet

- Financial-Accounting-Analysis-Dec 2022Document12 pagesFinancial-Accounting-Analysis-Dec 2022Rameshwar BhatiNo ratings yet

- Financial Accounting and AnalysisDocument9 pagesFinancial Accounting and AnalysisvasanthNo ratings yet

- FinanceDocument12 pagesFinanceshivansh tiwariNo ratings yet

- Financial AccountingDocument11 pagesFinancial AccountingVinay RawatNo ratings yet

- Financial Accounting Analysis 4cm 238Document12 pagesFinancial Accounting Analysis 4cm 238Yatharth NarangNo ratings yet

- Financial AccountingDocument10 pagesFinancial AccountingTeesha jainNo ratings yet

- Financial Accounting AnalysisDocument11 pagesFinancial Accounting Analysisharminder kaurNo ratings yet

- Hemant Assignment - FaDocument8 pagesHemant Assignment - Fahemant gaurkarNo ratings yet

- Financial AccountingDocument14 pagesFinancial AccountingUmesh SonawaneNo ratings yet

- Financial Accounting Analysis WelabyDocument9 pagesFinancial Accounting Analysis WelabyPubg loverNo ratings yet

- Financial AccountingDocument3 pagesFinancial Accountingjayprakash singhNo ratings yet

- Assignment Answers AccountingDocument8 pagesAssignment Answers AccountingAnkitNo ratings yet

- Financial Accounting and AnalysisDocument8 pagesFinancial Accounting and Analysisdisha.pcm22103No ratings yet

- Financial-Accounting-Analysis. Dec22Document11 pagesFinancial-Accounting-Analysis. Dec22Harish KumarNo ratings yet

- Financial Accounting and Finance Assignment Sem 1Document12 pagesFinancial Accounting and Finance Assignment Sem 1missmanju4uNo ratings yet

- Financial AccountingDocument5 pagesFinancial AccountingSanskar KhowalNo ratings yet

- Financial Accounting & Analysis AssignmentDocument9 pagesFinancial Accounting & Analysis AssignmentKhushboo BhojwaniNo ratings yet

- Financial Accounting and AnalysisDocument9 pagesFinancial Accounting and AnalysisYT MotivationNo ratings yet

- Financial Accounting & Analysis-1Document10 pagesFinancial Accounting & Analysis-1Abhishek JhaNo ratings yet

- AccountsDocument7 pagesAccountsAmit BadgujarNo ratings yet

- Financial Accounting and AnalysisDocument8 pagesFinancial Accounting and AnalysisRajesh BathulaNo ratings yet

- Financial AccountingDocument6 pagesFinancial Accountingprachi kewalramaniNo ratings yet

- Financial Accounting and Analysis - Assignment Dec 2022Document4 pagesFinancial Accounting and Analysis - Assignment Dec 2022shane.voronenkoNo ratings yet

- Financial Accounting and AnalysisDocument7 pagesFinancial Accounting and AnalysisKush BafnaNo ratings yet

- Account FinancingDocument7 pagesAccount FinancingSirnabeelNo ratings yet

- Financial Accounting and AnalysisDocument4 pagesFinancial Accounting and Analysispooja mandalNo ratings yet

- Jay ProjectDocument41 pagesJay Projecthenillakhani72No ratings yet

- Unit 7 PDFDocument22 pagesUnit 7 PDFSatti NagendrareddyNo ratings yet

- Financial Accounting and Analysis AssignmentDocument10 pagesFinancial Accounting and Analysis AssignmentRahul RJNo ratings yet

- Assignment Dec 2022 Financial AccountingDocument7 pagesAssignment Dec 2022 Financial Accountingkashishsidana64No ratings yet

- Class 11 Accountancy Chapter-3 Revision NotesDocument11 pagesClass 11 Accountancy Chapter-3 Revision NotesMohd. Khushmeen KhanNo ratings yet

- Accounting and Tally BookDocument10 pagesAccounting and Tally BookCA PASSNo ratings yet

- Financial Accounting & AnalysisDocument6 pagesFinancial Accounting & AnalysisDeepanshu SinghalNo ratings yet

- Financial Accounting and AnalysisDocument7 pagesFinancial Accounting and AnalysisShubh JainNo ratings yet

- Financial Accounting AssignmentDocument5 pagesFinancial Accounting Assignmentmohsink841No ratings yet

- FINANCIAL ACCOUNTING AND ANALYSING Sem 1Document4 pagesFINANCIAL ACCOUNTING AND ANALYSING Sem 1Maitry VasaNo ratings yet

- Tally Accounting Book by Ca MD ImranDocument6 pagesTally Accounting Book by Ca MD ImranMd ImranNo ratings yet

- Financial Accounting and AnalysisDocument3 pagesFinancial Accounting and AnalysisIsha TilokaniNo ratings yet

- Basics of Accounting: Chanakya Introduced The Accounting Concepts in His Book Arthashastra. in His Book, HeDocument15 pagesBasics of Accounting: Chanakya Introduced The Accounting Concepts in His Book Arthashastra. in His Book, HeShams100% (1)

- Financial Accounting & Analysis - N (1A)Document10 pagesFinancial Accounting & Analysis - N (1A)Tajinder MatharuNo ratings yet

- Analysis of Transactions-Recording Process-Journal EntriesDocument30 pagesAnalysis of Transactions-Recording Process-Journal Entrieshammad buttNo ratings yet

- What Is Accounting???Document15 pagesWhat Is Accounting???Modassar NazarNo ratings yet

- Financial-Accounting-Analysis Sem 1Document9 pagesFinancial-Accounting-Analysis Sem 1himanshujoshi335No ratings yet

- Financial Accounting and Analysis PDFDocument18 pagesFinancial Accounting and Analysis PDFDirghayu MaliNo ratings yet

- Sole Traders Final Account-QuestionsDocument11 pagesSole Traders Final Account-QuestionsHarsh VoraNo ratings yet

- Module 2 - Merchandising Concern-Completing The Accounting CycleDocument26 pagesModule 2 - Merchandising Concern-Completing The Accounting Cycledimolangalam5No ratings yet

- Finance NewDocument3 pagesFinance Newamanda divechaNo ratings yet

- Financial Accounting (Najeeb)Document8 pagesFinancial Accounting (Najeeb)Najeeb Khan0% (1)

- 110-Chapter 3 - Books of Original Entry-Journal - WMDocument21 pages110-Chapter 3 - Books of Original Entry-Journal - WMaaditya kumar jhaNo ratings yet

- Financial Accounting & Analysis 1Document7 pagesFinancial Accounting & Analysis 1Yogesh BhapkarNo ratings yet

- Non-Performing Assets in Indian Banking Sector: An Analytical and Comparative Study Between Public and Private Sector BanksDocument7 pagesNon-Performing Assets in Indian Banking Sector: An Analytical and Comparative Study Between Public and Private Sector BanksRajni KumariNo ratings yet

- An Analytical Study On Non-Performing Assets of Punjab National BankDocument4 pagesAn Analytical Study On Non-Performing Assets of Punjab National BankRajni KumariNo ratings yet

- Chapter 3 MCQs on Classification of IncomeDocument4 pagesChapter 3 MCQs on Classification of IncomeRajni KumariNo ratings yet

- An Analysis of Non Performing Assets (NPA) On Punjab National BankDocument14 pagesAn Analysis of Non Performing Assets (NPA) On Punjab National BankRajni KumariNo ratings yet

- Projec Guidelines - 111Document3 pagesProjec Guidelines - 111Rajni KumariNo ratings yet

- Vol2I1 Paper6Document9 pagesVol2I1 Paper6Rajni KumariNo ratings yet

- Vishal R. Bhimani and Ramesh B. LakhanaDocument11 pagesVishal R. Bhimani and Ramesh B. LakhanaRajni KumariNo ratings yet

- Customer Buying Behaviour and Reasons of Customer Attrition in Online Shopping of Fruits and Vegetables in Surat CityDocument7 pagesCustomer Buying Behaviour and Reasons of Customer Attrition in Online Shopping of Fruits and Vegetables in Surat CityRajni KumariNo ratings yet

- Project Proposal TemplateDocument4 pagesProject Proposal TemplateRajni KumariNo ratings yet

- Sample Guidelines - 1-6Document6 pagesSample Guidelines - 1-6Rajni KumariNo ratings yet

- GPH Assignement LIST 2023-24Document23 pagesGPH Assignement LIST 2023-24Rajni KumariNo ratings yet

- MCS 42Document46 pagesMCS 42Rajni KumariNo ratings yet

- 202 eDocument8 pages202 eRajni KumariNo ratings yet

- Bphe-104 Phe-4Document16 pagesBphe-104 Phe-4Rajni KumariNo ratings yet

- MPY 02 English December 2023 June 2024Document16 pagesMPY 02 English December 2023 June 2024Rajni KumariNo ratings yet

- Blie 228Document6 pagesBlie 228Rajni KumariNo ratings yet

- MPYE 13 English December 2023 June 2024Document16 pagesMPYE 13 English December 2023 June 2024Rajni KumariNo ratings yet

- SIP, Project Work, Industry Internship Guidelines 2023 of MBA, BBA andDocument3 pagesSIP, Project Work, Industry Internship Guidelines 2023 of MBA, BBA andRajni KumariNo ratings yet

- TS 05 English January 2023 July 2023Document22 pagesTS 05 English January 2023 July 2023Rajni KumariNo ratings yet

- MPYE 11 English December 2023 June 2024Document14 pagesMPYE 11 English December 2023 June 2024Rajni KumariNo ratings yet

- MMPC 4 em 2023 24Document22 pagesMMPC 4 em 2023 24Rajni KumariNo ratings yet

- MPYE 09 English December 2023 June 2024Document16 pagesMPYE 09 English December 2023 June 2024Rajni KumariNo ratings yet

- MPYE 05 English December 2023 June 2024Document16 pagesMPYE 05 English December 2023 June 2024Rajni KumariNo ratings yet

- MPYE 15 English December 2023 June 2024Document14 pagesMPYE 15 English December 2023 June 2024Rajni KumariNo ratings yet

- MPYE 12 English July 2023 January 2024Document12 pagesMPYE 12 English July 2023 January 2024Rajni KumariNo ratings yet

- Fepw 103Document4 pagesFepw 103Rajni KumariNo ratings yet

- MPYE 04 English December 2023 June 2024Document14 pagesMPYE 04 English December 2023 June 2024Rajni Kumari0% (1)

- MPY 01 English December 2023 June 2024Document18 pagesMPY 01 English December 2023 June 2024Rajni KumariNo ratings yet

- MPYE 10 English December 2023 June 2024Document14 pagesMPYE 10 English December 2023 June 2024Rajni KumariNo ratings yet

- MPYE 03 English December 2023 June 2024Document14 pagesMPYE 03 English December 2023 June 2024Rajni KumariNo ratings yet

Download as docx, pdf, or txt

You might also like

- Recording Transactions: Using The Method of Journal EntriesDocument50 pagesRecording Transactions: Using The Method of Journal EntriesHasanAbdullah100% (1)

- Financial Accounting Analysis z1xzdfDocument11 pagesFinancial Accounting Analysis z1xzdfJerrin JoseNo ratings yet

- Financial Accounting Analysis PLGXQCDocument11 pagesFinancial Accounting Analysis PLGXQCSagar KothawadeNo ratings yet

- Financial Accounting & Analysis - V - STDocument10 pagesFinancial Accounting & Analysis - V - STJeff Syn DeepNo ratings yet

- Financial Accounting & AnalysisDocument9 pagesFinancial Accounting & Analysisshriyansh jainNo ratings yet

- Vipin FinanceDocument10 pagesVipin Financeshivansh tiwariNo ratings yet

- Financial-Accounting-Analysis-Dec 2022Document10 pagesFinancial-Accounting-Analysis-Dec 2022Rameshwar BhatiNo ratings yet

- Financial Accounting and AnalysisDocument13 pagesFinancial Accounting and AnalysisAditya Raj DuttaNo ratings yet

- Financial AccountingDocument10 pagesFinancial Accountingsakshi khadiyaNo ratings yet

- Financial-Accounting-Analysis-Dec 2022Document12 pagesFinancial-Accounting-Analysis-Dec 2022Rameshwar BhatiNo ratings yet

- Financial Accounting and AnalysisDocument9 pagesFinancial Accounting and AnalysisvasanthNo ratings yet

- FinanceDocument12 pagesFinanceshivansh tiwariNo ratings yet

- Financial AccountingDocument11 pagesFinancial AccountingVinay RawatNo ratings yet

- Financial Accounting Analysis 4cm 238Document12 pagesFinancial Accounting Analysis 4cm 238Yatharth NarangNo ratings yet

- Financial AccountingDocument10 pagesFinancial AccountingTeesha jainNo ratings yet

- Financial Accounting AnalysisDocument11 pagesFinancial Accounting Analysisharminder kaurNo ratings yet

- Hemant Assignment - FaDocument8 pagesHemant Assignment - Fahemant gaurkarNo ratings yet

- Financial AccountingDocument14 pagesFinancial AccountingUmesh SonawaneNo ratings yet

- Financial Accounting Analysis WelabyDocument9 pagesFinancial Accounting Analysis WelabyPubg loverNo ratings yet

- Financial AccountingDocument3 pagesFinancial Accountingjayprakash singhNo ratings yet

- Assignment Answers AccountingDocument8 pagesAssignment Answers AccountingAnkitNo ratings yet

- Financial Accounting and AnalysisDocument8 pagesFinancial Accounting and Analysisdisha.pcm22103No ratings yet

- Financial-Accounting-Analysis. Dec22Document11 pagesFinancial-Accounting-Analysis. Dec22Harish KumarNo ratings yet

- Financial Accounting and Finance Assignment Sem 1Document12 pagesFinancial Accounting and Finance Assignment Sem 1missmanju4uNo ratings yet

- Financial AccountingDocument5 pagesFinancial AccountingSanskar KhowalNo ratings yet

- Financial Accounting & Analysis AssignmentDocument9 pagesFinancial Accounting & Analysis AssignmentKhushboo BhojwaniNo ratings yet

- Financial Accounting and AnalysisDocument9 pagesFinancial Accounting and AnalysisYT MotivationNo ratings yet

- Financial Accounting & Analysis-1Document10 pagesFinancial Accounting & Analysis-1Abhishek JhaNo ratings yet

- AccountsDocument7 pagesAccountsAmit BadgujarNo ratings yet

- Financial Accounting and AnalysisDocument8 pagesFinancial Accounting and AnalysisRajesh BathulaNo ratings yet

- Financial AccountingDocument6 pagesFinancial Accountingprachi kewalramaniNo ratings yet

- Financial Accounting and Analysis - Assignment Dec 2022Document4 pagesFinancial Accounting and Analysis - Assignment Dec 2022shane.voronenkoNo ratings yet

- Financial Accounting and AnalysisDocument7 pagesFinancial Accounting and AnalysisKush BafnaNo ratings yet

- Account FinancingDocument7 pagesAccount FinancingSirnabeelNo ratings yet

- Financial Accounting and AnalysisDocument4 pagesFinancial Accounting and Analysispooja mandalNo ratings yet

- Jay ProjectDocument41 pagesJay Projecthenillakhani72No ratings yet

- Unit 7 PDFDocument22 pagesUnit 7 PDFSatti NagendrareddyNo ratings yet

- Financial Accounting and Analysis AssignmentDocument10 pagesFinancial Accounting and Analysis AssignmentRahul RJNo ratings yet

- Assignment Dec 2022 Financial AccountingDocument7 pagesAssignment Dec 2022 Financial Accountingkashishsidana64No ratings yet

- Class 11 Accountancy Chapter-3 Revision NotesDocument11 pagesClass 11 Accountancy Chapter-3 Revision NotesMohd. Khushmeen KhanNo ratings yet

- Accounting and Tally BookDocument10 pagesAccounting and Tally BookCA PASSNo ratings yet

- Financial Accounting & AnalysisDocument6 pagesFinancial Accounting & AnalysisDeepanshu SinghalNo ratings yet

- Financial Accounting and AnalysisDocument7 pagesFinancial Accounting and AnalysisShubh JainNo ratings yet

- Financial Accounting AssignmentDocument5 pagesFinancial Accounting Assignmentmohsink841No ratings yet

- FINANCIAL ACCOUNTING AND ANALYSING Sem 1Document4 pagesFINANCIAL ACCOUNTING AND ANALYSING Sem 1Maitry VasaNo ratings yet

- Tally Accounting Book by Ca MD ImranDocument6 pagesTally Accounting Book by Ca MD ImranMd ImranNo ratings yet

- Financial Accounting and AnalysisDocument3 pagesFinancial Accounting and AnalysisIsha TilokaniNo ratings yet

- Basics of Accounting: Chanakya Introduced The Accounting Concepts in His Book Arthashastra. in His Book, HeDocument15 pagesBasics of Accounting: Chanakya Introduced The Accounting Concepts in His Book Arthashastra. in His Book, HeShams100% (1)

- Financial Accounting & Analysis - N (1A)Document10 pagesFinancial Accounting & Analysis - N (1A)Tajinder MatharuNo ratings yet

- Analysis of Transactions-Recording Process-Journal EntriesDocument30 pagesAnalysis of Transactions-Recording Process-Journal Entrieshammad buttNo ratings yet

- What Is Accounting???Document15 pagesWhat Is Accounting???Modassar NazarNo ratings yet

- Financial-Accounting-Analysis Sem 1Document9 pagesFinancial-Accounting-Analysis Sem 1himanshujoshi335No ratings yet

- Financial Accounting and Analysis PDFDocument18 pagesFinancial Accounting and Analysis PDFDirghayu MaliNo ratings yet

- Sole Traders Final Account-QuestionsDocument11 pagesSole Traders Final Account-QuestionsHarsh VoraNo ratings yet

- Module 2 - Merchandising Concern-Completing The Accounting CycleDocument26 pagesModule 2 - Merchandising Concern-Completing The Accounting Cycledimolangalam5No ratings yet

- Finance NewDocument3 pagesFinance Newamanda divechaNo ratings yet

- Financial Accounting (Najeeb)Document8 pagesFinancial Accounting (Najeeb)Najeeb Khan0% (1)

- 110-Chapter 3 - Books of Original Entry-Journal - WMDocument21 pages110-Chapter 3 - Books of Original Entry-Journal - WMaaditya kumar jhaNo ratings yet

- Financial Accounting & Analysis 1Document7 pagesFinancial Accounting & Analysis 1Yogesh BhapkarNo ratings yet

- Non-Performing Assets in Indian Banking Sector: An Analytical and Comparative Study Between Public and Private Sector BanksDocument7 pagesNon-Performing Assets in Indian Banking Sector: An Analytical and Comparative Study Between Public and Private Sector BanksRajni KumariNo ratings yet

- An Analytical Study On Non-Performing Assets of Punjab National BankDocument4 pagesAn Analytical Study On Non-Performing Assets of Punjab National BankRajni KumariNo ratings yet

- Chapter 3 MCQs on Classification of IncomeDocument4 pagesChapter 3 MCQs on Classification of IncomeRajni KumariNo ratings yet

- An Analysis of Non Performing Assets (NPA) On Punjab National BankDocument14 pagesAn Analysis of Non Performing Assets (NPA) On Punjab National BankRajni KumariNo ratings yet

- Projec Guidelines - 111Document3 pagesProjec Guidelines - 111Rajni KumariNo ratings yet

- Vol2I1 Paper6Document9 pagesVol2I1 Paper6Rajni KumariNo ratings yet

- Vishal R. Bhimani and Ramesh B. LakhanaDocument11 pagesVishal R. Bhimani and Ramesh B. LakhanaRajni KumariNo ratings yet

- Customer Buying Behaviour and Reasons of Customer Attrition in Online Shopping of Fruits and Vegetables in Surat CityDocument7 pagesCustomer Buying Behaviour and Reasons of Customer Attrition in Online Shopping of Fruits and Vegetables in Surat CityRajni KumariNo ratings yet

- Project Proposal TemplateDocument4 pagesProject Proposal TemplateRajni KumariNo ratings yet

- Sample Guidelines - 1-6Document6 pagesSample Guidelines - 1-6Rajni KumariNo ratings yet

- GPH Assignement LIST 2023-24Document23 pagesGPH Assignement LIST 2023-24Rajni KumariNo ratings yet

- MCS 42Document46 pagesMCS 42Rajni KumariNo ratings yet

- 202 eDocument8 pages202 eRajni KumariNo ratings yet

- Bphe-104 Phe-4Document16 pagesBphe-104 Phe-4Rajni KumariNo ratings yet

- MPY 02 English December 2023 June 2024Document16 pagesMPY 02 English December 2023 June 2024Rajni KumariNo ratings yet

- Blie 228Document6 pagesBlie 228Rajni KumariNo ratings yet

- MPYE 13 English December 2023 June 2024Document16 pagesMPYE 13 English December 2023 June 2024Rajni KumariNo ratings yet

- SIP, Project Work, Industry Internship Guidelines 2023 of MBA, BBA andDocument3 pagesSIP, Project Work, Industry Internship Guidelines 2023 of MBA, BBA andRajni KumariNo ratings yet

- TS 05 English January 2023 July 2023Document22 pagesTS 05 English January 2023 July 2023Rajni KumariNo ratings yet

- MPYE 11 English December 2023 June 2024Document14 pagesMPYE 11 English December 2023 June 2024Rajni KumariNo ratings yet

- MMPC 4 em 2023 24Document22 pagesMMPC 4 em 2023 24Rajni KumariNo ratings yet

- MPYE 09 English December 2023 June 2024Document16 pagesMPYE 09 English December 2023 June 2024Rajni KumariNo ratings yet

- MPYE 05 English December 2023 June 2024Document16 pagesMPYE 05 English December 2023 June 2024Rajni KumariNo ratings yet

- MPYE 15 English December 2023 June 2024Document14 pagesMPYE 15 English December 2023 June 2024Rajni KumariNo ratings yet

- MPYE 12 English July 2023 January 2024Document12 pagesMPYE 12 English July 2023 January 2024Rajni KumariNo ratings yet

- Fepw 103Document4 pagesFepw 103Rajni KumariNo ratings yet

- MPYE 04 English December 2023 June 2024Document14 pagesMPYE 04 English December 2023 June 2024Rajni Kumari0% (1)

- MPY 01 English December 2023 June 2024Document18 pagesMPY 01 English December 2023 June 2024Rajni KumariNo ratings yet

- MPYE 10 English December 2023 June 2024Document14 pagesMPYE 10 English December 2023 June 2024Rajni KumariNo ratings yet

- MPYE 03 English December 2023 June 2024Document14 pagesMPYE 03 English December 2023 June 2024Rajni KumariNo ratings yet