Download as pdf or txt

You might also like

- Managerial Accounting Course OutlineDocument4 pagesManagerial Accounting Course OutlineASMARA HABIB100% (1)

- Price Action Diver Power - Manual EngDocument5 pagesPrice Action Diver Power - Manual EngAdnan Wasim0% (1)

- 1.2 Financial and Management AccountingDocument55 pages1.2 Financial and Management Accountingteshome100% (2)

- ACCA F2 Course NotesDocument494 pagesACCA F2 Course NotesТурал Мансумов100% (4)

- Cost Concepts-09-05-2022Document87 pagesCost Concepts-09-05-2022chandanNo ratings yet

- Cost and Management AccouningDocument25 pagesCost and Management AccouningNahidul Islam IUNo ratings yet

- Chapter 1 Answer Cost Accounting PDFDocument5 pagesChapter 1 Answer Cost Accounting PDFCris VillarNo ratings yet

- Chapter 1 AnswerDocument4 pagesChapter 1 AnswerJanine NazNo ratings yet

- Cost Accounting-Task No. 1Document11 pagesCost Accounting-Task No. 1Aguilar Desirie P.No ratings yet

- F2.1 Notes & PPDocument220 pagesF2.1 Notes & PPjbah saimon baptiste100% (2)

- Fin Man Finals CoverageDocument5 pagesFin Man Finals Coverageaculify321No ratings yet

- Project, Appraisal, Planning & ControlDocument23 pagesProject, Appraisal, Planning & ControlAnantha NagNo ratings yet

- Definition of Cost and CostingDocument6 pagesDefinition of Cost and CostingNahidul Islam IUNo ratings yet

- CH 5Document45 pagesCH 5reader100% (1)

- The Nature and Purpose of Management Accounting: 1.1 Acca Syllabus Guide Outcome 1Document366 pagesThe Nature and Purpose of Management Accounting: 1.1 Acca Syllabus Guide Outcome 1Şâh Šůmiť100% (1)

- Strategy CostDocument4 pagesStrategy Costseungwan sonNo ratings yet

- Acowtancy F2 PDFDocument369 pagesAcowtancy F2 PDFŞâh ŠůmiťNo ratings yet

- CH 01Document6 pagesCH 01Kanbiro OrkaidoNo ratings yet

- Capital Budgeting Financial ManagementDocument18 pagesCapital Budgeting Financial ManagementAmoghavarsha BMNo ratings yet

- MA CH 1Document18 pagesMA CH 1prasad guthiNo ratings yet

- Cost AccountingDocument52 pagesCost Accountingd. CNo ratings yet

- Cost Accounting II YearDocument52 pagesCost Accounting II YearAnkit ThakurNo ratings yet

- Accounting For Managerial Decisions NotesDocument481 pagesAccounting For Managerial Decisions NotesVinoth D100% (1)

- Cost SheetDocument14 pagesCost Sheettanbir singhNo ratings yet

- 1.1 Intro To SCM and Management AccountingDocument6 pages1.1 Intro To SCM and Management AccountingXyril MañagoNo ratings yet

- Management Accounting Basic ConceptsDocument5 pagesManagement Accounting Basic ConceptsAlexandra Nicole IsaacNo ratings yet

- Cost Best Theory NoteDocument84 pagesCost Best Theory NotebinuNo ratings yet

- Usl MS 01Document6 pagesUsl MS 01myrnabalisi8No ratings yet

- Cost AccountingDocument117 pagesCost AccountingSIKANDARR GAMING YTNo ratings yet

- Standards and The Conceptual Framework Underlying Financial AccountingDocument26 pagesStandards and The Conceptual Framework Underlying Financial AccountingLodovicus LasdiNo ratings yet

- Cost Analysis and Control - HeroDocument23 pagesCost Analysis and Control - HeroshivaniNo ratings yet

- CPSM Exam 1 Financial Analysis Worksheet 2020Document9 pagesCPSM Exam 1 Financial Analysis Worksheet 2020DanitaNo ratings yet

- Cma - Chapter OneDocument19 pagesCma - Chapter OneKiya AbdiNo ratings yet

- 1 Basics of CMADocument39 pages1 Basics of CMAkhushi shahNo ratings yet

- Simon Chap. 5Document33 pagesSimon Chap. 5harum77No ratings yet

- MA Week 1Document61 pagesMA Week 1Lam BiNo ratings yet

- Management Advisory Services Objectives, Role & Scope of Management AccountingDocument8 pagesManagement Advisory Services Objectives, Role & Scope of Management AccountingNhicoleChoiNo ratings yet

- Week 8 - Overcoming Myopia & Balance ScorecardDocument6 pagesWeek 8 - Overcoming Myopia & Balance ScorecardMERINANo ratings yet

- Strategic BSC Budget Concepts Methodolog ForcastDocument187 pagesStrategic BSC Budget Concepts Methodolog ForcastSardan AbdullahNo ratings yet

- Project Chapter 1 EditedDocument18 pagesProject Chapter 1 Editedsamuel debebeNo ratings yet

- Cost Accounting: Adolph Matz Milton F. UsryDocument18 pagesCost Accounting: Adolph Matz Milton F. UsrySaifNazirNo ratings yet

- 3overview of Management Accounting & Cost ConceptsDocument13 pages3overview of Management Accounting & Cost Conceptsshubhamkumar.bhagat.23mbNo ratings yet

- BFC 5175 Management Accounting NotesDocument94 pagesBFC 5175 Management Accounting NotescyrusNo ratings yet

- Management Accounting Unit-1Document6 pagesManagement Accounting Unit-1prof.hpk18No ratings yet

- FM Course Outline & Materials-Thappar UnivDocument74 pagesFM Course Outline & Materials-Thappar Univharsimranjitsidhu661No ratings yet

- Budgeting Chapter. SixDocument22 pagesBudgeting Chapter. SixTatasha Takaye KasitoNo ratings yet

- Chapter 4 (Edited)Document30 pagesChapter 4 (Edited)Hoang Thi Thanh TamNo ratings yet

- Resa MAS-01: Management Accounting - Financial Management: - T R S ADocument4 pagesResa MAS-01: Management Accounting - Financial Management: - T R S AKenneth Pimentel100% (1)

- ch01 CostAccDocument18 pagesch01 CostAccqueneemaeaustriaNo ratings yet

- Chapter 1 - Introduction To Cost & Management AccountingDocument30 pagesChapter 1 - Introduction To Cost & Management AccountingJiajia MoxNo ratings yet

- AccountingDocument5 pagesAccountingDaniella Mae Basas OlanoNo ratings yet

- Cost Accounting PDFDocument35 pagesCost Accounting PDFSanta-ana Jerald JuanoNo ratings yet

- Chapter 1: Introduction To Managerial AccountingDocument3 pagesChapter 1: Introduction To Managerial AccountingRohanne Garcia AbrigoNo ratings yet

- P1 Course NotesDocument213 pagesP1 Course NotesJohn Sue Han100% (2)

- CostcoDocument3 pagesCostcoDERYL GALVENo ratings yet

- 3.FINA211 Financial ManagementDocument5 pages3.FINA211 Financial ManagementIqtidar Khan0% (1)

- Dmgt202 Cost and Management AccountingDocument269 pagesDmgt202 Cost and Management AccountingRoaster 2100% (2)

- Lesson 2 - Cost Accounting Cycle Part 1Document39 pagesLesson 2 - Cost Accounting Cycle Part 1Mama MiyaNo ratings yet

- Module 6: Internal Analysis of The Company 6.1. Opportunity CostDocument7 pagesModule 6: Internal Analysis of The Company 6.1. Opportunity CostSanjayNo ratings yet

- Management Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesFrom EverandManagement Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesNo ratings yet

- Slides Sessions 7-10Document58 pagesSlides Sessions 7-10020Abhisek KhadangaNo ratings yet

- RV SCM Session 1 To 6Document108 pagesRV SCM Session 1 To 6020Abhisek KhadangaNo ratings yet

- Session Slides - 3Document34 pagesSession Slides - 3020Abhisek KhadangaNo ratings yet

- Session-3-Material Cost and ControlDocument42 pagesSession-3-Material Cost and Control020Abhisek KhadangaNo ratings yet

- Costing System - Absorption vs. Variable CostingDocument29 pagesCosting System - Absorption vs. Variable Costing020Abhisek KhadangaNo ratings yet

- Session Slides - 1Document21 pagesSession Slides - 1020Abhisek KhadangaNo ratings yet

- Normal Vs Actual CapacityDocument8 pagesNormal Vs Actual Capacity020Abhisek KhadangaNo ratings yet

- 18-10-2022-Activity Based BudgetingDocument32 pages18-10-2022-Activity Based Budgeting020Abhisek KhadangaNo ratings yet

- Sampling Distributions - 1Document19 pagesSampling Distributions - 1020Abhisek KhadangaNo ratings yet

- Session-16-17-18-CVP AnalysisDocument78 pagesSession-16-17-18-CVP Analysis020Abhisek KhadangaNo ratings yet

- Hypothesis Testing - 1Document32 pagesHypothesis Testing - 1020Abhisek KhadangaNo ratings yet

- Amity Law SchoolDocument6 pagesAmity Law SchoolsimranNo ratings yet

- Application FormDocument5 pagesApplication FormNikhil KumarNo ratings yet

- Accenture Breaking Bad Habits Infographic PDFDocument1 pageAccenture Breaking Bad Habits Infographic PDFAmine AïdiNo ratings yet

- Specific Borrowing, P2, Number 5, Page 295Document2 pagesSpecific Borrowing, P2, Number 5, Page 295Jxrriz Cyrxl EhxllaNo ratings yet

- Realme Narzo 20 Pro (Black Ninja, 128 GB) : Grand Total 16999.00Document2 pagesRealme Narzo 20 Pro (Black Ninja, 128 GB) : Grand Total 16999.00CSE Muthu Vignesh RNo ratings yet

- Nomos Meaning Management Household: Choices. - Means That Our ChoicesDocument3 pagesNomos Meaning Management Household: Choices. - Means That Our ChoicesnicNo ratings yet

- Multiple Choice Questions 1 If A Company Uses The Direct Write OffDocument1 pageMultiple Choice Questions 1 If A Company Uses The Direct Write OffHassan JanNo ratings yet

- Nygard ResponseDocument80 pagesNygard ResponseDaniel FisherNo ratings yet

- Invoice Number Seller's Name and Address GSTIN Number: 19AAICB2268A1ZWDocument1 pageInvoice Number Seller's Name and Address GSTIN Number: 19AAICB2268A1ZWarvindyadavNo ratings yet

- Al FarisDocument1 pageAl FarisctrlaltdestroyNo ratings yet

- Final (PPT) A Study On Investors Perception Towards MutualDocument12 pagesFinal (PPT) A Study On Investors Perception Towards MutualAvantika JindalNo ratings yet

- Key ProjectDocument2 pagesKey ProjectNasirNo ratings yet

- Fundamentals of ABMDocument4 pagesFundamentals of ABMMadriñan Wency M.No ratings yet

- Module 3Document32 pagesModule 3Manuel ErmitaNo ratings yet

- Dheo's TeamDocument1 pageDheo's TeamDheo AlviansyahNo ratings yet

- ACS - HondaDocument3 pagesACS - HondaRiya3No ratings yet

- How To Easily Make Quality Juggling TorchesDocument4 pagesHow To Easily Make Quality Juggling TorchesPrimaria AvrigNo ratings yet

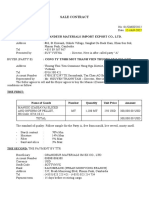

- Sale Contract:: Cong Ty TNHH Mot Thanh Vien Thuong Mai Gia LocDocument2 pagesSale Contract:: Cong Ty TNHH Mot Thanh Vien Thuong Mai Gia LocNiron CompanyNo ratings yet

- Marico BSDocument2 pagesMarico BSAbhay Kumar SinghNo ratings yet

- BERDocument8 pagesBERacealloysllp.accNo ratings yet

- Caltex V COA DigestDocument3 pagesCaltex V COA DigestCarlito HilvanoNo ratings yet

- Mercury Athletic Footwear: Ashutosh DashDocument49 pagesMercury Athletic Footwear: Ashutosh DashSaurabh ChhabraNo ratings yet

- The Time Value of MoneyDocument98 pagesThe Time Value of MoneyNathaniel YbanezNo ratings yet

- Assignment 1 - Digital CurrencyDocument10 pagesAssignment 1 - Digital CurrencyAina SaffiyahNo ratings yet

- The Global Interstate System Pt. 3Document4 pagesThe Global Interstate System Pt. 3Mia AstilloNo ratings yet

- Tax Invoice: Excitel Broadband Pvt. LTDDocument1 pageTax Invoice: Excitel Broadband Pvt. LTDMittal GalaxyNo ratings yet

- Gold Account 06 December 2021 To 06 June 2022Document1 pageGold Account 06 December 2021 To 06 June 2022mohamed elmakhzniNo ratings yet

- FTU - Financial Reporting QualityDocument22 pagesFTU - Financial Reporting Qualityk60.2113343020No ratings yet

- Foreign Exchange: The Structure and Operation of The FX MarketDocument44 pagesForeign Exchange: The Structure and Operation of The FX MarketThu NguyenNo ratings yet