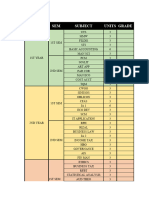

Ch03 Percentage Tax Rates Table

Ch03 Percentage Tax Rates Table

You might also like

- Customer Satisfaction Towards After Sales Service of Maruti SuzukiDocument83 pagesCustomer Satisfaction Towards After Sales Service of Maruti SuzukiSHUBHAM GURUNG90% (10)

- SCM Streamlining Period End Un Invoiced Receipt Accruals in Receipt Accounting PDFDocument23 pagesSCM Streamlining Period End Un Invoiced Receipt Accruals in Receipt Accounting PDFSaritha VittaNo ratings yet

- CHAPTER 5 - Percentage TaxDocument2 pagesCHAPTER 5 - Percentage Taxnewlymade641No ratings yet

- Percentage Tax ItemsDocument3 pagesPercentage Tax ItemsKristine CamposNo ratings yet

- Quarterly Percentage Tax Rates TableDocument2 pagesQuarterly Percentage Tax Rates TableJoseph MangahasNo ratings yet

- Other Perceentage TaxesDocument9 pagesOther Perceentage TaxesBrian Martin AnupolNo ratings yet

- Other Percentage Tax Summary of Other Percentage Tax Rates: Coverage Taxable Base Tax RateDocument18 pagesOther Percentage Tax Summary of Other Percentage Tax Rates: Coverage Taxable Base Tax RateZaaavnn VannnnnNo ratings yet

- Percentage Tax Description: Under Sections 116 To 126 of The Tax Code, As AmendedDocument4 pagesPercentage Tax Description: Under Sections 116 To 126 of The Tax Code, As AmendedAndrea TanNo ratings yet

- Other Percentage Tax DraftDocument9 pagesOther Percentage Tax Draftbeadineros8No ratings yet

- Tax Rates: Coverage Basis Tax RateDocument3 pagesTax Rates: Coverage Basis Tax RateDymphna Ann CalumpianoNo ratings yet

- Taxation Reviewer - Percentage TaxDocument3 pagesTaxation Reviewer - Percentage TaxDaphne BarceNo ratings yet

- Quarterly Percentage Tax Rates Table: Taxable Base Tax RateDocument4 pagesQuarterly Percentage Tax Rates Table: Taxable Base Tax RateKathrine CruzNo ratings yet

- Bullet Notes 9 - Other Percentage TaxDocument4 pagesBullet Notes 9 - Other Percentage TaxFlores Renato Jr. S.No ratings yet

- Tax Quiz BeeDocument10 pagesTax Quiz BeeMitchelle DumlaoNo ratings yet

- Other Percentage TaxDocument3 pagesOther Percentage Taxmira limNo ratings yet

- Excise Percentage TaxDocument9 pagesExcise Percentage TaxPines MacapagalNo ratings yet

- Percentage TaxDocument28 pagesPercentage TaxkemboseNo ratings yet

- Business TaxationDocument41 pagesBusiness TaxationKim AranasNo ratings yet

- Other Percentage Taxes Transaction/Entity Tax Rate Tax BaseDocument4 pagesOther Percentage Taxes Transaction/Entity Tax Rate Tax BaseClarissa de VeraNo ratings yet

- TAX 401 Percentage Tax Part 1Document7 pagesTAX 401 Percentage Tax Part 1Juan Miguel UngsodNo ratings yet

- Lecture 7 - Other Percentage TaxDocument3 pagesLecture 7 - Other Percentage TaxJeffrey BionaNo ratings yet

- TAX-401: Percentage TAX (P 1) : - T R S ADocument6 pagesTAX-401: Percentage TAX (P 1) : - T R S AEira ShaneNo ratings yet

- Infographics - TaxDocument12 pagesInfographics - TaxPablo InocencioNo ratings yet

- BIR Form 2551Q: Quarterly Percentage TaxDocument8 pagesBIR Form 2551Q: Quarterly Percentage TaxAngelyn SamandeNo ratings yet

- Withholding Taxes 2023Document23 pagesWithholding Taxes 2023Antonette Frilles GibagaNo ratings yet

- Module 3 Percentage TaxDocument10 pagesModule 3 Percentage TaxDay DreamNo ratings yet

- Notes Other Tax PercentageDocument7 pagesNotes Other Tax PercentageJohn RellonNo ratings yet

- Percentage TaxesDocument8 pagesPercentage TaxesTokha YatsurugiNo ratings yet

- Income Tax For CorporationsDocument2 pagesIncome Tax For CorporationskjabbugaoNo ratings yet

- Module No 3 - INCOME TAXATION PART1ADocument6 pagesModule No 3 - INCOME TAXATION PART1APrinces S. RoqueNo ratings yet

- Business and Transfer TaxationDocument5 pagesBusiness and Transfer TaxationElizabeth OlaNo ratings yet

- Business Tax SummaryDocument10 pagesBusiness Tax SummaryJohn Raymond MarzanNo ratings yet

- Notes in Percentage TaxDocument8 pagesNotes in Percentage TaxESTRADA, Angelica T.No ratings yet

- Lecture 7 - Other Percentage TaxDocument3 pagesLecture 7 - Other Percentage TaxJohn Felix Morelos DoldolNo ratings yet

- Tax 05 Percentage Tax LectureDocument12 pagesTax 05 Percentage Tax LectureAllan Jay CabreraNo ratings yet

- (Bustax) ReviewerDocument4 pages(Bustax) Reviewerphia triesNo ratings yet

- Percentage TAX: Prepared By: Mrs. Nelia I. Tomas, Cpa, LPTDocument37 pagesPercentage TAX: Prepared By: Mrs. Nelia I. Tomas, Cpa, LPTTokis SabaNo ratings yet

- Percentage TaxDocument17 pagesPercentage TaxPrincess Jay NacorNo ratings yet

- Other Percentage Tax SUMMARYDocument1 pageOther Percentage Tax SUMMARYMarionne GNo ratings yet

- Tax RateDocument8 pagesTax RateJames Domini Lopez LabianoNo ratings yet

- Tax RateDocument8 pagesTax RateJames Domini Lopez LabianoNo ratings yet

- Tax Rate A. For Individuals Earning Purely Compensation Income and Individuals Engaged in Business and Practice of ProfessionDocument4 pagesTax Rate A. For Individuals Earning Purely Compensation Income and Individuals Engaged in Business and Practice of Professioniona4andalNo ratings yet

- OPT, Excise, DST, Tax RemediesDocument11 pagesOPT, Excise, DST, Tax RemediesLou Brad Nazareno IgnacioNo ratings yet

- Income Tax Chart - Individual TaxpayersDocument2 pagesIncome Tax Chart - Individual TaxpayersAlthia Joy AlisingNo ratings yet

- Other Percentage Taxes Focus Notes (Group 1)Document7 pagesOther Percentage Taxes Focus Notes (Group 1)LeonilaEnriquez100% (1)

- Withholding of Percentage TaxesDocument17 pagesWithholding of Percentage TaxesNilda Sahibul BaclayanNo ratings yet

- Source Final Tax: Interest Income or Yield From Local Currency Bank Deposits or Deposit SubstitutesDocument3 pagesSource Final Tax: Interest Income or Yield From Local Currency Bank Deposits or Deposit SubstitutesJhon Ariel JulatonNo ratings yet

- HumRes TaxDocument3 pagesHumRes TaxJob Noel BernardoNo ratings yet

- Other Percentage Tax and Zero RatedDocument6 pagesOther Percentage Tax and Zero RatedRenalyn Ps MewagNo ratings yet

- W14 Module 12withholding TaxesDocument7 pagesW14 Module 12withholding Taxescamille ducutNo ratings yet

- Bsa1202 Ss2324e Individuals 08a AddendumDocument2 pagesBsa1202 Ss2324e Individuals 08a Addendumninarissi.05No ratings yet

- Withholding Taxes Learning ObjectivesDocument8 pagesWithholding Taxes Learning ObjectivesAce AlquinNo ratings yet

- What Is Percentage TaxDocument4 pagesWhat Is Percentage Taxmy miNo ratings yet

- TAX Chapter 5 Reviewer - Summary Principles of Business Taxation TAX Chapter 5 Reviewer - Summary Principles of Business TaxationDocument5 pagesTAX Chapter 5 Reviewer - Summary Principles of Business Taxation TAX Chapter 5 Reviewer - Summary Principles of Business TaxationMakoy BixenmanNo ratings yet

- OPTDocument4 pagesOPTMarie MAy MagtibayNo ratings yet

- Opt HandoutDocument4 pagesOpt HandoutjulsNo ratings yet

- Tax NotesDocument6 pagesTax NotesDeloria DelsaNo ratings yet

- OPT NotesDocument1 pageOPT NotesRonalyn SantosNo ratings yet

- TAXATION 2 Chapter 8 Percentage Tax PDFDocument4 pagesTAXATION 2 Chapter 8 Percentage Tax PDFKim Cristian MaañoNo ratings yet

- Other Percentage Taxes: Prof. Jeanefer Reyes CPA, MPADocument29 pagesOther Percentage Taxes: Prof. Jeanefer Reyes CPA, MPAmark anthony espirituNo ratings yet

- Summary of Grades Gwa CalculatorDocument4 pagesSummary of Grades Gwa CalculatorRenelyn FiloteoNo ratings yet

- Individual Activity No.Document3 pagesIndividual Activity No.Renelyn FiloteoNo ratings yet

- Lesson 3 Basic Skills in Volleyball Pe-04Document24 pagesLesson 3 Basic Skills in Volleyball Pe-04Renelyn FiloteoNo ratings yet

- Ch05 Documentary Stamp TaxDocument9 pagesCh05 Documentary Stamp TaxRenelyn FiloteoNo ratings yet

- Activity - Filoteo, Renelyn A.Document1 pageActivity - Filoteo, Renelyn A.Renelyn FiloteoNo ratings yet

- Module 3Document7 pagesModule 3Renelyn FiloteoNo ratings yet

- BSA Internship Manual ReportsDocument20 pagesBSA Internship Manual ReportsRenelyn FiloteoNo ratings yet

- Auditing and Assurance Speclized Industries - 18 Sep 2023Document29 pagesAuditing and Assurance Speclized Industries - 18 Sep 2023Renelyn FiloteoNo ratings yet

- 2022.08.10 Aud TheoDocument17 pages2022.08.10 Aud TheoRenelyn FiloteoNo ratings yet

- Ch06 Introduction To Transfer TaxesDocument9 pagesCh06 Introduction To Transfer TaxesRenelyn FiloteoNo ratings yet

- AUD02 - 10 - Audit of Other Assests - Illustrative ProblemsDocument3 pagesAUD02 - 10 - Audit of Other Assests - Illustrative ProblemsRenelyn FiloteoNo ratings yet

- Smartbooks Advance Guide To Database SetupDocument7 pagesSmartbooks Advance Guide To Database SetupRenelyn FiloteoNo ratings yet

- Ch10 Donor's TaxDocument9 pagesCh10 Donor's TaxRenelyn FiloteoNo ratings yet

- Ch09 Net Taxable EstateDocument11 pagesCh09 Net Taxable EstateRenelyn FiloteoNo ratings yet

- CH07 Gross EstateDocument9 pagesCH07 Gross EstateRenelyn FiloteoNo ratings yet

- Ch03 Percentage TaxesDocument8 pagesCh03 Percentage TaxesRenelyn FiloteoNo ratings yet

- Labor Standards ComputationDocument8 pagesLabor Standards ComputationRenelyn FiloteoNo ratings yet

- DocxDocument7 pagesDocxRenelyn FiloteoNo ratings yet

- Ch01 Introduction To Business TaxesDocument6 pagesCh01 Introduction To Business TaxesRenelyn FiloteoNo ratings yet

- Ch07 Gross EstateDocument8 pagesCh07 Gross EstateRenelyn FiloteoNo ratings yet

- Ch02 Value-Added TaxDocument22 pagesCh02 Value-Added TaxRenelyn FiloteoNo ratings yet

- Ch06 Introduction To Transfer TaxesDocument9 pagesCh06 Introduction To Transfer TaxesRenelyn FiloteoNo ratings yet

- Ch01 Introduction To Cost AccountingDocument5 pagesCh01 Introduction To Cost AccountingRenelyn FiloteoNo ratings yet

- Case - Network SolutionsDocument3 pagesCase - Network SolutionsSameera AroraNo ratings yet

- Acct 555 Audit Week 4 MidtermDocument6 pagesAcct 555 Audit Week 4 MidtermNatasha DeclanNo ratings yet

- 2019 - ACA Exam Dates and Deadlines - WebDocument2 pages2019 - ACA Exam Dates and Deadlines - WebSree Mathi SuntheriNo ratings yet

- BSBINN301 - Promote Innovation in A Team Environment Learner Guide V3-1Document100 pagesBSBINN301 - Promote Innovation in A Team Environment Learner Guide V3-1Luiz50% (2)

- Effect of Brand Image On Customer Satisfaction & Loyalty Intention and The Role of Customer..Document13 pagesEffect of Brand Image On Customer Satisfaction & Loyalty Intention and The Role of Customer..Ali HafeezNo ratings yet

- TBChap 010Document23 pagesTBChap 010alaamabood6No ratings yet

- WEB GST Template1oldDocument1,025 pagesWEB GST Template1oldkarthikeyanwebtelNo ratings yet

- Reviewers: Project Transition ChecklistDocument6 pagesReviewers: Project Transition Checklistnsadnan100% (2)

- Chapter 03Document9 pagesChapter 03Gonzales JhayVeeNo ratings yet

- DepreciationDocument24 pagesDepreciationKRISHNA KANT GUPTANo ratings yet

- Mergers: Principles of Corporate FinanceDocument35 pagesMergers: Principles of Corporate FinancechooisinNo ratings yet

- Company Profile EmperorDocument11 pagesCompany Profile EmperorBekal SurgaNo ratings yet

- Answers To Questions For Chapter 14: (Questions Are in Bold Print Followed by Answers.)Document17 pagesAnswers To Questions For Chapter 14: (Questions Are in Bold Print Followed by Answers.)Yew KeanNo ratings yet

- TQM Supplier SelectionDocument13 pagesTQM Supplier SelectionmanagolgappaNo ratings yet

- 2 Erp SapDocument10 pages2 Erp SapShipra SharmaNo ratings yet

- Dessler 17Document14 pagesDessler 17Victoria EyelashesNo ratings yet

- Optional Standard Deductions ExampleDocument7 pagesOptional Standard Deductions ExampleSandia EspejoNo ratings yet

- Chapter 9Document15 pagesChapter 9Leah Rose Feldman0% (1)

- Ssentamu Derrick CVDocument4 pagesSsentamu Derrick CVJay MenonNo ratings yet

- Annexure II CP 14-13-14 PDFDocument381 pagesAnnexure II CP 14-13-14 PDFவேணிNo ratings yet

- Encl.: As Above. Copy For Kind Perusal To:: SMEC International Pty. LTDDocument8 pagesEncl.: As Above. Copy For Kind Perusal To:: SMEC International Pty. LTDMohd UmarNo ratings yet

- Oracle Freight Payment, Billing, and Claims CloudDocument3 pagesOracle Freight Payment, Billing, and Claims CloudALLIA LOPEZNo ratings yet

- PT - Mbi 2020Document65 pagesPT - Mbi 2020caesar putraNo ratings yet

- Management and Cost AccountingDocument13 pagesManagement and Cost AccountingRashedNo ratings yet

- For Quiz - Product CostingDocument3 pagesFor Quiz - Product CostingBetchang AquinoNo ratings yet

- Ce LawsDocument37 pagesCe LawsIvyJoama Batin-Barnachea PrioloNo ratings yet

- Micro Insurance in IndiaDocument127 pagesMicro Insurance in IndiaVineet SukumarNo ratings yet

- In The United States Bankruptcy Court Eastern District of Michigan Southern DivisionDocument15 pagesIn The United States Bankruptcy Court Eastern District of Michigan Southern DivisionChapter 11 DocketsNo ratings yet

Download as pdf or txt

You might also like

- Customer Satisfaction Towards After Sales Service of Maruti SuzukiDocument83 pagesCustomer Satisfaction Towards After Sales Service of Maruti SuzukiSHUBHAM GURUNG90% (10)

- SCM Streamlining Period End Un Invoiced Receipt Accruals in Receipt Accounting PDFDocument23 pagesSCM Streamlining Period End Un Invoiced Receipt Accruals in Receipt Accounting PDFSaritha VittaNo ratings yet

- CHAPTER 5 - Percentage TaxDocument2 pagesCHAPTER 5 - Percentage Taxnewlymade641No ratings yet

- Percentage Tax ItemsDocument3 pagesPercentage Tax ItemsKristine CamposNo ratings yet

- Quarterly Percentage Tax Rates TableDocument2 pagesQuarterly Percentage Tax Rates TableJoseph MangahasNo ratings yet

- Other Perceentage TaxesDocument9 pagesOther Perceentage TaxesBrian Martin AnupolNo ratings yet

- Other Percentage Tax Summary of Other Percentage Tax Rates: Coverage Taxable Base Tax RateDocument18 pagesOther Percentage Tax Summary of Other Percentage Tax Rates: Coverage Taxable Base Tax RateZaaavnn VannnnnNo ratings yet

- Percentage Tax Description: Under Sections 116 To 126 of The Tax Code, As AmendedDocument4 pagesPercentage Tax Description: Under Sections 116 To 126 of The Tax Code, As AmendedAndrea TanNo ratings yet

- Other Percentage Tax DraftDocument9 pagesOther Percentage Tax Draftbeadineros8No ratings yet

- Tax Rates: Coverage Basis Tax RateDocument3 pagesTax Rates: Coverage Basis Tax RateDymphna Ann CalumpianoNo ratings yet

- Taxation Reviewer - Percentage TaxDocument3 pagesTaxation Reviewer - Percentage TaxDaphne BarceNo ratings yet

- Quarterly Percentage Tax Rates Table: Taxable Base Tax RateDocument4 pagesQuarterly Percentage Tax Rates Table: Taxable Base Tax RateKathrine CruzNo ratings yet

- Bullet Notes 9 - Other Percentage TaxDocument4 pagesBullet Notes 9 - Other Percentage TaxFlores Renato Jr. S.No ratings yet

- Tax Quiz BeeDocument10 pagesTax Quiz BeeMitchelle DumlaoNo ratings yet

- Other Percentage TaxDocument3 pagesOther Percentage Taxmira limNo ratings yet

- Excise Percentage TaxDocument9 pagesExcise Percentage TaxPines MacapagalNo ratings yet

- Percentage TaxDocument28 pagesPercentage TaxkemboseNo ratings yet

- Business TaxationDocument41 pagesBusiness TaxationKim AranasNo ratings yet

- Other Percentage Taxes Transaction/Entity Tax Rate Tax BaseDocument4 pagesOther Percentage Taxes Transaction/Entity Tax Rate Tax BaseClarissa de VeraNo ratings yet

- TAX 401 Percentage Tax Part 1Document7 pagesTAX 401 Percentage Tax Part 1Juan Miguel UngsodNo ratings yet

- Lecture 7 - Other Percentage TaxDocument3 pagesLecture 7 - Other Percentage TaxJeffrey BionaNo ratings yet

- TAX-401: Percentage TAX (P 1) : - T R S ADocument6 pagesTAX-401: Percentage TAX (P 1) : - T R S AEira ShaneNo ratings yet

- Infographics - TaxDocument12 pagesInfographics - TaxPablo InocencioNo ratings yet

- BIR Form 2551Q: Quarterly Percentage TaxDocument8 pagesBIR Form 2551Q: Quarterly Percentage TaxAngelyn SamandeNo ratings yet

- Withholding Taxes 2023Document23 pagesWithholding Taxes 2023Antonette Frilles GibagaNo ratings yet

- Module 3 Percentage TaxDocument10 pagesModule 3 Percentage TaxDay DreamNo ratings yet

- Notes Other Tax PercentageDocument7 pagesNotes Other Tax PercentageJohn RellonNo ratings yet

- Percentage TaxesDocument8 pagesPercentage TaxesTokha YatsurugiNo ratings yet

- Income Tax For CorporationsDocument2 pagesIncome Tax For CorporationskjabbugaoNo ratings yet

- Module No 3 - INCOME TAXATION PART1ADocument6 pagesModule No 3 - INCOME TAXATION PART1APrinces S. RoqueNo ratings yet

- Business and Transfer TaxationDocument5 pagesBusiness and Transfer TaxationElizabeth OlaNo ratings yet

- Business Tax SummaryDocument10 pagesBusiness Tax SummaryJohn Raymond MarzanNo ratings yet

- Notes in Percentage TaxDocument8 pagesNotes in Percentage TaxESTRADA, Angelica T.No ratings yet

- Lecture 7 - Other Percentage TaxDocument3 pagesLecture 7 - Other Percentage TaxJohn Felix Morelos DoldolNo ratings yet

- Tax 05 Percentage Tax LectureDocument12 pagesTax 05 Percentage Tax LectureAllan Jay CabreraNo ratings yet

- (Bustax) ReviewerDocument4 pages(Bustax) Reviewerphia triesNo ratings yet

- Percentage TAX: Prepared By: Mrs. Nelia I. Tomas, Cpa, LPTDocument37 pagesPercentage TAX: Prepared By: Mrs. Nelia I. Tomas, Cpa, LPTTokis SabaNo ratings yet

- Percentage TaxDocument17 pagesPercentage TaxPrincess Jay NacorNo ratings yet

- Other Percentage Tax SUMMARYDocument1 pageOther Percentage Tax SUMMARYMarionne GNo ratings yet

- Tax RateDocument8 pagesTax RateJames Domini Lopez LabianoNo ratings yet

- Tax RateDocument8 pagesTax RateJames Domini Lopez LabianoNo ratings yet

- Tax Rate A. For Individuals Earning Purely Compensation Income and Individuals Engaged in Business and Practice of ProfessionDocument4 pagesTax Rate A. For Individuals Earning Purely Compensation Income and Individuals Engaged in Business and Practice of Professioniona4andalNo ratings yet

- OPT, Excise, DST, Tax RemediesDocument11 pagesOPT, Excise, DST, Tax RemediesLou Brad Nazareno IgnacioNo ratings yet

- Income Tax Chart - Individual TaxpayersDocument2 pagesIncome Tax Chart - Individual TaxpayersAlthia Joy AlisingNo ratings yet

- Other Percentage Taxes Focus Notes (Group 1)Document7 pagesOther Percentage Taxes Focus Notes (Group 1)LeonilaEnriquez100% (1)

- Withholding of Percentage TaxesDocument17 pagesWithholding of Percentage TaxesNilda Sahibul BaclayanNo ratings yet

- Source Final Tax: Interest Income or Yield From Local Currency Bank Deposits or Deposit SubstitutesDocument3 pagesSource Final Tax: Interest Income or Yield From Local Currency Bank Deposits or Deposit SubstitutesJhon Ariel JulatonNo ratings yet

- HumRes TaxDocument3 pagesHumRes TaxJob Noel BernardoNo ratings yet

- Other Percentage Tax and Zero RatedDocument6 pagesOther Percentage Tax and Zero RatedRenalyn Ps MewagNo ratings yet

- W14 Module 12withholding TaxesDocument7 pagesW14 Module 12withholding Taxescamille ducutNo ratings yet

- Bsa1202 Ss2324e Individuals 08a AddendumDocument2 pagesBsa1202 Ss2324e Individuals 08a Addendumninarissi.05No ratings yet

- Withholding Taxes Learning ObjectivesDocument8 pagesWithholding Taxes Learning ObjectivesAce AlquinNo ratings yet

- What Is Percentage TaxDocument4 pagesWhat Is Percentage Taxmy miNo ratings yet

- TAX Chapter 5 Reviewer - Summary Principles of Business Taxation TAX Chapter 5 Reviewer - Summary Principles of Business TaxationDocument5 pagesTAX Chapter 5 Reviewer - Summary Principles of Business Taxation TAX Chapter 5 Reviewer - Summary Principles of Business TaxationMakoy BixenmanNo ratings yet

- OPTDocument4 pagesOPTMarie MAy MagtibayNo ratings yet

- Opt HandoutDocument4 pagesOpt HandoutjulsNo ratings yet

- Tax NotesDocument6 pagesTax NotesDeloria DelsaNo ratings yet

- OPT NotesDocument1 pageOPT NotesRonalyn SantosNo ratings yet

- TAXATION 2 Chapter 8 Percentage Tax PDFDocument4 pagesTAXATION 2 Chapter 8 Percentage Tax PDFKim Cristian MaañoNo ratings yet

- Other Percentage Taxes: Prof. Jeanefer Reyes CPA, MPADocument29 pagesOther Percentage Taxes: Prof. Jeanefer Reyes CPA, MPAmark anthony espirituNo ratings yet

- Summary of Grades Gwa CalculatorDocument4 pagesSummary of Grades Gwa CalculatorRenelyn FiloteoNo ratings yet

- Individual Activity No.Document3 pagesIndividual Activity No.Renelyn FiloteoNo ratings yet

- Lesson 3 Basic Skills in Volleyball Pe-04Document24 pagesLesson 3 Basic Skills in Volleyball Pe-04Renelyn FiloteoNo ratings yet

- Ch05 Documentary Stamp TaxDocument9 pagesCh05 Documentary Stamp TaxRenelyn FiloteoNo ratings yet

- Activity - Filoteo, Renelyn A.Document1 pageActivity - Filoteo, Renelyn A.Renelyn FiloteoNo ratings yet

- Module 3Document7 pagesModule 3Renelyn FiloteoNo ratings yet

- BSA Internship Manual ReportsDocument20 pagesBSA Internship Manual ReportsRenelyn FiloteoNo ratings yet

- Auditing and Assurance Speclized Industries - 18 Sep 2023Document29 pagesAuditing and Assurance Speclized Industries - 18 Sep 2023Renelyn FiloteoNo ratings yet

- 2022.08.10 Aud TheoDocument17 pages2022.08.10 Aud TheoRenelyn FiloteoNo ratings yet

- Ch06 Introduction To Transfer TaxesDocument9 pagesCh06 Introduction To Transfer TaxesRenelyn FiloteoNo ratings yet

- AUD02 - 10 - Audit of Other Assests - Illustrative ProblemsDocument3 pagesAUD02 - 10 - Audit of Other Assests - Illustrative ProblemsRenelyn FiloteoNo ratings yet

- Smartbooks Advance Guide To Database SetupDocument7 pagesSmartbooks Advance Guide To Database SetupRenelyn FiloteoNo ratings yet

- Ch10 Donor's TaxDocument9 pagesCh10 Donor's TaxRenelyn FiloteoNo ratings yet

- Ch09 Net Taxable EstateDocument11 pagesCh09 Net Taxable EstateRenelyn FiloteoNo ratings yet

- CH07 Gross EstateDocument9 pagesCH07 Gross EstateRenelyn FiloteoNo ratings yet

- Ch03 Percentage TaxesDocument8 pagesCh03 Percentage TaxesRenelyn FiloteoNo ratings yet

- Labor Standards ComputationDocument8 pagesLabor Standards ComputationRenelyn FiloteoNo ratings yet

- DocxDocument7 pagesDocxRenelyn FiloteoNo ratings yet

- Ch01 Introduction To Business TaxesDocument6 pagesCh01 Introduction To Business TaxesRenelyn FiloteoNo ratings yet

- Ch07 Gross EstateDocument8 pagesCh07 Gross EstateRenelyn FiloteoNo ratings yet

- Ch02 Value-Added TaxDocument22 pagesCh02 Value-Added TaxRenelyn FiloteoNo ratings yet

- Ch06 Introduction To Transfer TaxesDocument9 pagesCh06 Introduction To Transfer TaxesRenelyn FiloteoNo ratings yet

- Ch01 Introduction To Cost AccountingDocument5 pagesCh01 Introduction To Cost AccountingRenelyn FiloteoNo ratings yet

- Case - Network SolutionsDocument3 pagesCase - Network SolutionsSameera AroraNo ratings yet

- Acct 555 Audit Week 4 MidtermDocument6 pagesAcct 555 Audit Week 4 MidtermNatasha DeclanNo ratings yet

- 2019 - ACA Exam Dates and Deadlines - WebDocument2 pages2019 - ACA Exam Dates and Deadlines - WebSree Mathi SuntheriNo ratings yet

- BSBINN301 - Promote Innovation in A Team Environment Learner Guide V3-1Document100 pagesBSBINN301 - Promote Innovation in A Team Environment Learner Guide V3-1Luiz50% (2)

- Effect of Brand Image On Customer Satisfaction & Loyalty Intention and The Role of Customer..Document13 pagesEffect of Brand Image On Customer Satisfaction & Loyalty Intention and The Role of Customer..Ali HafeezNo ratings yet

- TBChap 010Document23 pagesTBChap 010alaamabood6No ratings yet

- WEB GST Template1oldDocument1,025 pagesWEB GST Template1oldkarthikeyanwebtelNo ratings yet

- Reviewers: Project Transition ChecklistDocument6 pagesReviewers: Project Transition Checklistnsadnan100% (2)

- Chapter 03Document9 pagesChapter 03Gonzales JhayVeeNo ratings yet

- DepreciationDocument24 pagesDepreciationKRISHNA KANT GUPTANo ratings yet

- Mergers: Principles of Corporate FinanceDocument35 pagesMergers: Principles of Corporate FinancechooisinNo ratings yet

- Company Profile EmperorDocument11 pagesCompany Profile EmperorBekal SurgaNo ratings yet

- Answers To Questions For Chapter 14: (Questions Are in Bold Print Followed by Answers.)Document17 pagesAnswers To Questions For Chapter 14: (Questions Are in Bold Print Followed by Answers.)Yew KeanNo ratings yet

- TQM Supplier SelectionDocument13 pagesTQM Supplier SelectionmanagolgappaNo ratings yet

- 2 Erp SapDocument10 pages2 Erp SapShipra SharmaNo ratings yet

- Dessler 17Document14 pagesDessler 17Victoria EyelashesNo ratings yet

- Optional Standard Deductions ExampleDocument7 pagesOptional Standard Deductions ExampleSandia EspejoNo ratings yet

- Chapter 9Document15 pagesChapter 9Leah Rose Feldman0% (1)

- Ssentamu Derrick CVDocument4 pagesSsentamu Derrick CVJay MenonNo ratings yet

- Annexure II CP 14-13-14 PDFDocument381 pagesAnnexure II CP 14-13-14 PDFவேணிNo ratings yet

- Encl.: As Above. Copy For Kind Perusal To:: SMEC International Pty. LTDDocument8 pagesEncl.: As Above. Copy For Kind Perusal To:: SMEC International Pty. LTDMohd UmarNo ratings yet

- Oracle Freight Payment, Billing, and Claims CloudDocument3 pagesOracle Freight Payment, Billing, and Claims CloudALLIA LOPEZNo ratings yet

- PT - Mbi 2020Document65 pagesPT - Mbi 2020caesar putraNo ratings yet

- Management and Cost AccountingDocument13 pagesManagement and Cost AccountingRashedNo ratings yet

- For Quiz - Product CostingDocument3 pagesFor Quiz - Product CostingBetchang AquinoNo ratings yet

- Ce LawsDocument37 pagesCe LawsIvyJoama Batin-Barnachea PrioloNo ratings yet

- Micro Insurance in IndiaDocument127 pagesMicro Insurance in IndiaVineet SukumarNo ratings yet

- In The United States Bankruptcy Court Eastern District of Michigan Southern DivisionDocument15 pagesIn The United States Bankruptcy Court Eastern District of Michigan Southern DivisionChapter 11 DocketsNo ratings yet