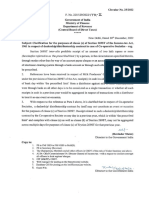

Circular 14 2022

Circular 14 2022

You might also like

- HSBC - de - PGL - Bank Endorsed - DraftDocument10 pagesHSBC - de - PGL - Bank Endorsed - Draftzagog100% (1)

- Assignment No 1 IMPEXDocument3 pagesAssignment No 1 IMPEXMUHAMMAD -No ratings yet

- URSBDocument1 pageURSBJudeNo ratings yet

- AMNPR3273M - Issue Letter - 1054531107 (1) - 23072023Document3 pagesAMNPR3273M - Issue Letter - 1054531107 (1) - 23072023prakash reddyNo ratings yet

- Aino Communique 110th Dec EditionDocument12 pagesAino Communique 110th Dec EditionSwathi JainNo ratings yet

- Itr Deadline Extended ITR Filing, Tax Audit Report Deadlines For FY 2020-21 Extended by CBDT - The Economic TimesDocument1 pageItr Deadline Extended ITR Filing, Tax Audit Report Deadlines For FY 2020-21 Extended by CBDT - The Economic TimesVittal TalwarNo ratings yet

- Aino Communique 100th Edition - Feb 2022 PDFDocument22 pagesAino Communique 100th Edition - Feb 2022 PDFSwathi JainNo ratings yet

- PWC News Alert 30 September 2020 Taxation and Other Laws Relaxation and Amendment of Certain Provisions Act 2020 NotifiedDocument9 pagesPWC News Alert 30 September 2020 Taxation and Other Laws Relaxation and Amendment of Certain Provisions Act 2020 Notifiedsujit guptaNo ratings yet

- Circular No 18 2022Document6 pagesCircular No 18 2022Manish KumarNo ratings yet

- Memo No 1304Document8 pagesMemo No 1304chandra shekharNo ratings yet

- GST Circular PDFDocument11 pagesGST Circular PDFNavnera divisionNo ratings yet

- Refund in GSTDocument6 pagesRefund in GSTNilesh SoniNo ratings yet

- Incometax 29 09 2022Document3 pagesIncometax 29 09 2022nitishbhaskaran4No ratings yet

- Circulars/Notifications: Legal UpdateDocument6 pagesCirculars/Notifications: Legal UpdateAnupam BaliNo ratings yet

- Compliance Calendar NovDocument23 pagesCompliance Calendar NovDsp VarmaNo ratings yet

- Tax Laws - Direct TaxDocument45 pagesTax Laws - Direct TaxAnubha PriyaNo ratings yet

- Aino Communique-109EditionDocument12 pagesAino Communique-109EditionSwathi JainNo ratings yet

- TDS in GSTDocument3 pagesTDS in GSTacm001No ratings yet

- GSTDocument40 pagesGSTsangkhawmaNo ratings yet

- Decoding Indian Union Budget Finance Bil PDFDocument7 pagesDecoding Indian Union Budget Finance Bil PDFkumarNo ratings yet

- Aino Communique 108th EditionDocument12 pagesAino Communique 108th EditionSwathi JainNo ratings yet

- Taxguru - In-Extended Due Dates of Income Tax Return Tax Audit TP AuditDocument5 pagesTaxguru - In-Extended Due Dates of Income Tax Return Tax Audit TP AuditJessica NulphNo ratings yet

- AINO Communique 105th Edition - July 2022Document13 pagesAINO Communique 105th Edition - July 2022Swathi JainNo ratings yet

- Address: of The of The Employee 2021-2022Document3 pagesAddress: of The of The Employee 2021-2022Dipak PArmarNo ratings yet

- Inpu T Tax CRE Dit!: Week 6Document39 pagesInpu T Tax CRE Dit!: Week 6himeesha dhiliwalNo ratings yet

- Latest Updates in GSTDocument6 pagesLatest Updates in GSTprathNo ratings yet

- Circular No.: Government India Department Revenue Board Direct Division)Document2 pagesCircular No.: Government India Department Revenue Board Direct Division)ashim1No ratings yet

- FAQsonTDS 230221 120909Document8 pagesFAQsonTDS 230221 120909Bharath UGNo ratings yet

- 66522bos53752 cp9Document39 pages66522bos53752 cp9Chandan ganapathi HcNo ratings yet

- Part I: Statutory Update: © The Institute of Chartered Accountants of IndiaDocument41 pagesPart I: Statutory Update: © The Institute of Chartered Accountants of IndiaApeksha ChilwalNo ratings yet

- Bos 32722 P 4Document37 pagesBos 32722 P 4CmaChanduNo ratings yet

- Nov 2021-97th EditionDocument13 pagesNov 2021-97th EditionSwathi JainNo ratings yet

- Suggested Answer On Tax Planning and Compliance Nov-Dec, 2023Document18 pagesSuggested Answer On Tax Planning and Compliance Nov-Dec, 2023Erfan KhanNo ratings yet

- Circular 25 2022Document1 pageCircular 25 2022NESL WebsiteNo ratings yet

- Cir 187 19 2022 CGSTDocument3 pagesCir 187 19 2022 CGSTAtanu Kumar SenNo ratings yet

- Circular-No-10-2022 Income Tax ActDocument4 pagesCircular-No-10-2022 Income Tax Actsaurabh14014No ratings yet

- Do You Know GST I March 2021 I Ranjan MehtaDocument15 pagesDo You Know GST I March 2021 I Ranjan MehtaCA Ranjan MehtaNo ratings yet

- Aino Communique PDFDocument14 pagesAino Communique PDFSwathi JainNo ratings yet

- Executive Programme (New Syllabus) Supplement FOR Tax LawsDocument14 pagesExecutive Programme (New Syllabus) Supplement FOR Tax Lawsgopika mundraNo ratings yet

- Lavanya Tax InternalDocument12 pagesLavanya Tax InternalYouTube PremiumNo ratings yet

- News 11 20Document26 pagesNews 11 20gst samvaadNo ratings yet

- E InvoiceDocument23 pagesE Invoicenallarahul86No ratings yet

- Tax Memorandum On The Finance Act 2023Document26 pagesTax Memorandum On The Finance Act 2023Random videosNo ratings yet

- Shuttlers Metropolitan ReportDocument7 pagesShuttlers Metropolitan ReportAkinyemi SilasNo ratings yet

- Budget 2022 BBDocument30 pagesBudget 2022 BBCA SRD & CONo ratings yet

- 30.07.2020 - CGST Rules, 2017 - (Part-A - Rules)Document164 pages30.07.2020 - CGST Rules, 2017 - (Part-A - Rules)Dost BhawanaNo ratings yet

- GST Changes Effective From January 01, 2022Document9 pagesGST Changes Effective From January 01, 2022p.kunduNo ratings yet

- Circular No 10 2022Document4 pagesCircular No 10 2022Shobhit ShuklaNo ratings yet

- Ramesh GPFDocument2 pagesRamesh GPFSHARANUNo ratings yet

- Volume 1 - 75 PagesDocument75 pagesVolume 1 - 75 PagesMarsNo ratings yet

- Computation of Income Tax For The Financial Year 2021-2022 Corresponding To The Assessment Year 2022-2023Document3 pagesComputation of Income Tax For The Financial Year 2021-2022 Corresponding To The Assessment Year 2022-2023maityutsabNo ratings yet

- Circular 1 2023Document1 pageCircular 1 2023KunalKumarNo ratings yet

- Corporate Compliance Calendar August 2023Document23 pagesCorporate Compliance Calendar August 2023Sreenivasan KorappathNo ratings yet

- GST Updates-45th Council MeetingDocument5 pagesGST Updates-45th Council Meetinghimesh amibrokerNo ratings yet

- 51198bos40905 cp4 PDFDocument41 pages51198bos40905 cp4 PDFShubham VyasNo ratings yet

- Central Goods and Services Tax (CGST) Rules, 2017 Part - A (Rules)Document163 pagesCentral Goods and Services Tax (CGST) Rules, 2017 Part - A (Rules)Rakshit AgarwalNo ratings yet

- Tax HDocument15 pagesTax HDeepesh SinghNo ratings yet

- ShowfileDocument4 pagesShowfileMkNo ratings yet

- Latest Circulars, Notifications and Press Releases: 2. This Notification Shall Come Into Force From The 1Document0 pagesLatest Circulars, Notifications and Press Releases: 2. This Notification Shall Come Into Force From The 1Ketan ThakkarNo ratings yet

- Circular 9 2021Document3 pagesCircular 9 2021Camp Asst. to ADGP AdministrationNo ratings yet

- Invoicing Under GSTDocument53 pagesInvoicing Under GSTkomal tanwaniNo ratings yet

- Aino Communique 111th Edition Jan 2023 PDFDocument14 pagesAino Communique 111th Edition Jan 2023 PDFSwathi JainNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- 0cover I & IVDocument1 page0cover I & IVshantXNo ratings yet

- Circular No 12 2022Document7 pagesCircular No 12 2022shantXNo ratings yet

- Rates of Income Tax A.Y.2013-14: (A) Individuals, Non-Specified Hufs and AopsDocument3 pagesRates of Income Tax A.Y.2013-14: (A) Individuals, Non-Specified Hufs and AopsshantXNo ratings yet

- Accountancy: Financial AccountingDocument10 pagesAccountancy: Financial AccountingshantXNo ratings yet

- Financial Statements - II: 360 AccountancyDocument65 pagesFinancial Statements - II: 360 AccountancyshantX100% (1)

- Appendix Description of Commonly Used Functions in Access: Sales Sales Sales SalesDocument5 pagesAppendix Description of Commonly Used Functions in Access: Sales Sales Sales SalesshantXNo ratings yet

- In The Income Tax Appellate Tribunal "B" Bench, Ahmedabad Before Shri Pradip Kumar Kedia, Accountant Member & Shri Mahavir Prasad, Judicial MemebrDocument47 pagesIn The Income Tax Appellate Tribunal "B" Bench, Ahmedabad Before Shri Pradip Kumar Kedia, Accountant Member & Shri Mahavir Prasad, Judicial MemebrshantXNo ratings yet

- 56 II VIIIDocument2 pages56 II VIIIshantXNo ratings yet

- RegulationsDocument3 pagesRegulationsshantXNo ratings yet

- M/S.Ashok Leyland LTD Vs The Assistant Commissioner of On 10 February, 2016Document2 pagesM/S.Ashok Leyland LTD Vs The Assistant Commissioner of On 10 February, 2016shantXNo ratings yet

- Corporation Tax Direct TaxesDocument30 pagesCorporation Tax Direct TaxesshantXNo ratings yet

- EY Tax Alert: Mumbai Tribunal Upholds The Deductibility of Sales Promotion Expenditure Incurred by A Pharma CompanyDocument4 pagesEY Tax Alert: Mumbai Tribunal Upholds The Deductibility of Sales Promotion Expenditure Incurred by A Pharma CompanyshantXNo ratings yet

- Export of ServicesDocument9 pagesExport of ServicesshantX100% (1)

- Maxopp Investment LTD Vs CitDocument17 pagesMaxopp Investment LTD Vs CitshantXNo ratings yet

- ISSAI 1000 E Endorsement VersionDocument40 pagesISSAI 1000 E Endorsement VersionshantX100% (1)

- Indicative Deposit Profit Rates: PKR Savings AccountsDocument3 pagesIndicative Deposit Profit Rates: PKR Savings AccountsEjaz AhmadNo ratings yet

- Myrna Keith - Employer Package PDFDocument24 pagesMyrna Keith - Employer Package PDFJoey KeithNo ratings yet

- Business MathUSlem Q2week3Document10 pagesBusiness MathUSlem Q2week3Rex MagdaluyoNo ratings yet

- Confirmation For Booking ID # 849524949Document1 pageConfirmation For Booking ID # 849524949Saibal SenNo ratings yet

- Income Taxation Case DigestDocument22 pagesIncome Taxation Case DigestCoyzz de Guzman100% (1)

- CE Interim ReportingDocument2 pagesCE Interim ReportingalyssaNo ratings yet

- ST SupO 3069 2022 23 193255Document1 pageST SupO 3069 2022 23 193255Rajat SharmaNo ratings yet

- Base Files Maintenance ManualDocument1,012 pagesBase Files Maintenance ManualAdminNo ratings yet

- Bill 10859611Document1 pageBill 10859611Vikas SoniNo ratings yet

- CIR V Toledo (2015)Document2 pagesCIR V Toledo (2015)Anonymous bOncqbp8yiNo ratings yet

- Report Monthly 2023 OctDocument6 pagesReport Monthly 2023 Octcaretravels11No ratings yet

- Transaction StatementDocument10 pagesTransaction StatementVenki GajaNo ratings yet

- VAT Act 1997Document105 pagesVAT Act 1997JesseNderingoNo ratings yet

- Sprepl - Comparitive Statement For Supply of "SKF" Make Spherical Roller BearingDocument4 pagesSprepl - Comparitive Statement For Supply of "SKF" Make Spherical Roller BearingSuresh KumarNo ratings yet

- Service Tax On Works ContractDocument4 pagesService Tax On Works Contractrajs27No ratings yet

- Payment ProcessingDocument58 pagesPayment Processingsubash_dotNo ratings yet

- SA300622Document1 pageSA300622JEFF WONNo ratings yet

- Banking 05Document34 pagesBanking 05kannan sunilNo ratings yet

- Circular 1 Switching Fee AePS EKYC Card 0 0Document2 pagesCircular 1 Switching Fee AePS EKYC Card 0 0Sharanya KunduNo ratings yet

- University of Management and Technology Quotation Master Paints 01-08-2023Document2 pagesUniversity of Management and Technology Quotation Master Paints 01-08-2023usman khanNo ratings yet

- Tax-03-01-Basic-Principles of Taxation - EncryptedDocument11 pagesTax-03-01-Basic-Principles of Taxation - Encryptedgean eszekeilNo ratings yet

- CTA EB Case No. 250 and 255Document25 pagesCTA EB Case No. 250 and 255trina tsai100% (1)

- Allotment OrderDocument2 pagesAllotment Orderbchandu112No ratings yet

- Audit PlanDocument9 pagesAudit Planananda_joshi5178No ratings yet

- Solved Shannon Signs A 100 000 Contract To Develop A Plan ForDocument1 pageSolved Shannon Signs A 100 000 Contract To Develop A Plan ForAnbu jaromiaNo ratings yet

- ITC-Profit-Loss 2017 PDFDocument1 pageITC-Profit-Loss 2017 PDFShristi GutgutiaNo ratings yet

- Book Bill - BarnenduDocument2 pagesBook Bill - Barnendubarnendu.sarkarNo ratings yet

Download as pdf or txt

You might also like

- HSBC - de - PGL - Bank Endorsed - DraftDocument10 pagesHSBC - de - PGL - Bank Endorsed - Draftzagog100% (1)

- Assignment No 1 IMPEXDocument3 pagesAssignment No 1 IMPEXMUHAMMAD -No ratings yet

- URSBDocument1 pageURSBJudeNo ratings yet

- AMNPR3273M - Issue Letter - 1054531107 (1) - 23072023Document3 pagesAMNPR3273M - Issue Letter - 1054531107 (1) - 23072023prakash reddyNo ratings yet

- Aino Communique 110th Dec EditionDocument12 pagesAino Communique 110th Dec EditionSwathi JainNo ratings yet

- Itr Deadline Extended ITR Filing, Tax Audit Report Deadlines For FY 2020-21 Extended by CBDT - The Economic TimesDocument1 pageItr Deadline Extended ITR Filing, Tax Audit Report Deadlines For FY 2020-21 Extended by CBDT - The Economic TimesVittal TalwarNo ratings yet

- Aino Communique 100th Edition - Feb 2022 PDFDocument22 pagesAino Communique 100th Edition - Feb 2022 PDFSwathi JainNo ratings yet

- PWC News Alert 30 September 2020 Taxation and Other Laws Relaxation and Amendment of Certain Provisions Act 2020 NotifiedDocument9 pagesPWC News Alert 30 September 2020 Taxation and Other Laws Relaxation and Amendment of Certain Provisions Act 2020 Notifiedsujit guptaNo ratings yet

- Circular No 18 2022Document6 pagesCircular No 18 2022Manish KumarNo ratings yet

- Memo No 1304Document8 pagesMemo No 1304chandra shekharNo ratings yet

- GST Circular PDFDocument11 pagesGST Circular PDFNavnera divisionNo ratings yet

- Refund in GSTDocument6 pagesRefund in GSTNilesh SoniNo ratings yet

- Incometax 29 09 2022Document3 pagesIncometax 29 09 2022nitishbhaskaran4No ratings yet

- Circulars/Notifications: Legal UpdateDocument6 pagesCirculars/Notifications: Legal UpdateAnupam BaliNo ratings yet

- Compliance Calendar NovDocument23 pagesCompliance Calendar NovDsp VarmaNo ratings yet

- Tax Laws - Direct TaxDocument45 pagesTax Laws - Direct TaxAnubha PriyaNo ratings yet

- Aino Communique-109EditionDocument12 pagesAino Communique-109EditionSwathi JainNo ratings yet

- TDS in GSTDocument3 pagesTDS in GSTacm001No ratings yet

- GSTDocument40 pagesGSTsangkhawmaNo ratings yet

- Decoding Indian Union Budget Finance Bil PDFDocument7 pagesDecoding Indian Union Budget Finance Bil PDFkumarNo ratings yet

- Aino Communique 108th EditionDocument12 pagesAino Communique 108th EditionSwathi JainNo ratings yet

- Taxguru - In-Extended Due Dates of Income Tax Return Tax Audit TP AuditDocument5 pagesTaxguru - In-Extended Due Dates of Income Tax Return Tax Audit TP AuditJessica NulphNo ratings yet

- AINO Communique 105th Edition - July 2022Document13 pagesAINO Communique 105th Edition - July 2022Swathi JainNo ratings yet

- Address: of The of The Employee 2021-2022Document3 pagesAddress: of The of The Employee 2021-2022Dipak PArmarNo ratings yet

- Inpu T Tax CRE Dit!: Week 6Document39 pagesInpu T Tax CRE Dit!: Week 6himeesha dhiliwalNo ratings yet

- Latest Updates in GSTDocument6 pagesLatest Updates in GSTprathNo ratings yet

- Circular No.: Government India Department Revenue Board Direct Division)Document2 pagesCircular No.: Government India Department Revenue Board Direct Division)ashim1No ratings yet

- FAQsonTDS 230221 120909Document8 pagesFAQsonTDS 230221 120909Bharath UGNo ratings yet

- 66522bos53752 cp9Document39 pages66522bos53752 cp9Chandan ganapathi HcNo ratings yet

- Part I: Statutory Update: © The Institute of Chartered Accountants of IndiaDocument41 pagesPart I: Statutory Update: © The Institute of Chartered Accountants of IndiaApeksha ChilwalNo ratings yet

- Bos 32722 P 4Document37 pagesBos 32722 P 4CmaChanduNo ratings yet

- Nov 2021-97th EditionDocument13 pagesNov 2021-97th EditionSwathi JainNo ratings yet

- Suggested Answer On Tax Planning and Compliance Nov-Dec, 2023Document18 pagesSuggested Answer On Tax Planning and Compliance Nov-Dec, 2023Erfan KhanNo ratings yet

- Circular 25 2022Document1 pageCircular 25 2022NESL WebsiteNo ratings yet

- Cir 187 19 2022 CGSTDocument3 pagesCir 187 19 2022 CGSTAtanu Kumar SenNo ratings yet

- Circular-No-10-2022 Income Tax ActDocument4 pagesCircular-No-10-2022 Income Tax Actsaurabh14014No ratings yet

- Do You Know GST I March 2021 I Ranjan MehtaDocument15 pagesDo You Know GST I March 2021 I Ranjan MehtaCA Ranjan MehtaNo ratings yet

- Aino Communique PDFDocument14 pagesAino Communique PDFSwathi JainNo ratings yet

- Executive Programme (New Syllabus) Supplement FOR Tax LawsDocument14 pagesExecutive Programme (New Syllabus) Supplement FOR Tax Lawsgopika mundraNo ratings yet

- Lavanya Tax InternalDocument12 pagesLavanya Tax InternalYouTube PremiumNo ratings yet

- News 11 20Document26 pagesNews 11 20gst samvaadNo ratings yet

- E InvoiceDocument23 pagesE Invoicenallarahul86No ratings yet

- Tax Memorandum On The Finance Act 2023Document26 pagesTax Memorandum On The Finance Act 2023Random videosNo ratings yet

- Shuttlers Metropolitan ReportDocument7 pagesShuttlers Metropolitan ReportAkinyemi SilasNo ratings yet

- Budget 2022 BBDocument30 pagesBudget 2022 BBCA SRD & CONo ratings yet

- 30.07.2020 - CGST Rules, 2017 - (Part-A - Rules)Document164 pages30.07.2020 - CGST Rules, 2017 - (Part-A - Rules)Dost BhawanaNo ratings yet

- GST Changes Effective From January 01, 2022Document9 pagesGST Changes Effective From January 01, 2022p.kunduNo ratings yet

- Circular No 10 2022Document4 pagesCircular No 10 2022Shobhit ShuklaNo ratings yet

- Ramesh GPFDocument2 pagesRamesh GPFSHARANUNo ratings yet

- Volume 1 - 75 PagesDocument75 pagesVolume 1 - 75 PagesMarsNo ratings yet

- Computation of Income Tax For The Financial Year 2021-2022 Corresponding To The Assessment Year 2022-2023Document3 pagesComputation of Income Tax For The Financial Year 2021-2022 Corresponding To The Assessment Year 2022-2023maityutsabNo ratings yet

- Circular 1 2023Document1 pageCircular 1 2023KunalKumarNo ratings yet

- Corporate Compliance Calendar August 2023Document23 pagesCorporate Compliance Calendar August 2023Sreenivasan KorappathNo ratings yet

- GST Updates-45th Council MeetingDocument5 pagesGST Updates-45th Council Meetinghimesh amibrokerNo ratings yet

- 51198bos40905 cp4 PDFDocument41 pages51198bos40905 cp4 PDFShubham VyasNo ratings yet

- Central Goods and Services Tax (CGST) Rules, 2017 Part - A (Rules)Document163 pagesCentral Goods and Services Tax (CGST) Rules, 2017 Part - A (Rules)Rakshit AgarwalNo ratings yet

- Tax HDocument15 pagesTax HDeepesh SinghNo ratings yet

- ShowfileDocument4 pagesShowfileMkNo ratings yet

- Latest Circulars, Notifications and Press Releases: 2. This Notification Shall Come Into Force From The 1Document0 pagesLatest Circulars, Notifications and Press Releases: 2. This Notification Shall Come Into Force From The 1Ketan ThakkarNo ratings yet

- Circular 9 2021Document3 pagesCircular 9 2021Camp Asst. to ADGP AdministrationNo ratings yet

- Invoicing Under GSTDocument53 pagesInvoicing Under GSTkomal tanwaniNo ratings yet

- Aino Communique 111th Edition Jan 2023 PDFDocument14 pagesAino Communique 111th Edition Jan 2023 PDFSwathi JainNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- 0cover I & IVDocument1 page0cover I & IVshantXNo ratings yet

- Circular No 12 2022Document7 pagesCircular No 12 2022shantXNo ratings yet

- Rates of Income Tax A.Y.2013-14: (A) Individuals, Non-Specified Hufs and AopsDocument3 pagesRates of Income Tax A.Y.2013-14: (A) Individuals, Non-Specified Hufs and AopsshantXNo ratings yet

- Accountancy: Financial AccountingDocument10 pagesAccountancy: Financial AccountingshantXNo ratings yet

- Financial Statements - II: 360 AccountancyDocument65 pagesFinancial Statements - II: 360 AccountancyshantX100% (1)

- Appendix Description of Commonly Used Functions in Access: Sales Sales Sales SalesDocument5 pagesAppendix Description of Commonly Used Functions in Access: Sales Sales Sales SalesshantXNo ratings yet

- In The Income Tax Appellate Tribunal "B" Bench, Ahmedabad Before Shri Pradip Kumar Kedia, Accountant Member & Shri Mahavir Prasad, Judicial MemebrDocument47 pagesIn The Income Tax Appellate Tribunal "B" Bench, Ahmedabad Before Shri Pradip Kumar Kedia, Accountant Member & Shri Mahavir Prasad, Judicial MemebrshantXNo ratings yet

- 56 II VIIIDocument2 pages56 II VIIIshantXNo ratings yet

- RegulationsDocument3 pagesRegulationsshantXNo ratings yet

- M/S.Ashok Leyland LTD Vs The Assistant Commissioner of On 10 February, 2016Document2 pagesM/S.Ashok Leyland LTD Vs The Assistant Commissioner of On 10 February, 2016shantXNo ratings yet

- Corporation Tax Direct TaxesDocument30 pagesCorporation Tax Direct TaxesshantXNo ratings yet

- EY Tax Alert: Mumbai Tribunal Upholds The Deductibility of Sales Promotion Expenditure Incurred by A Pharma CompanyDocument4 pagesEY Tax Alert: Mumbai Tribunal Upholds The Deductibility of Sales Promotion Expenditure Incurred by A Pharma CompanyshantXNo ratings yet

- Export of ServicesDocument9 pagesExport of ServicesshantX100% (1)

- Maxopp Investment LTD Vs CitDocument17 pagesMaxopp Investment LTD Vs CitshantXNo ratings yet

- ISSAI 1000 E Endorsement VersionDocument40 pagesISSAI 1000 E Endorsement VersionshantX100% (1)

- Indicative Deposit Profit Rates: PKR Savings AccountsDocument3 pagesIndicative Deposit Profit Rates: PKR Savings AccountsEjaz AhmadNo ratings yet

- Myrna Keith - Employer Package PDFDocument24 pagesMyrna Keith - Employer Package PDFJoey KeithNo ratings yet

- Business MathUSlem Q2week3Document10 pagesBusiness MathUSlem Q2week3Rex MagdaluyoNo ratings yet

- Confirmation For Booking ID # 849524949Document1 pageConfirmation For Booking ID # 849524949Saibal SenNo ratings yet

- Income Taxation Case DigestDocument22 pagesIncome Taxation Case DigestCoyzz de Guzman100% (1)

- CE Interim ReportingDocument2 pagesCE Interim ReportingalyssaNo ratings yet

- ST SupO 3069 2022 23 193255Document1 pageST SupO 3069 2022 23 193255Rajat SharmaNo ratings yet

- Base Files Maintenance ManualDocument1,012 pagesBase Files Maintenance ManualAdminNo ratings yet

- Bill 10859611Document1 pageBill 10859611Vikas SoniNo ratings yet

- CIR V Toledo (2015)Document2 pagesCIR V Toledo (2015)Anonymous bOncqbp8yiNo ratings yet

- Report Monthly 2023 OctDocument6 pagesReport Monthly 2023 Octcaretravels11No ratings yet

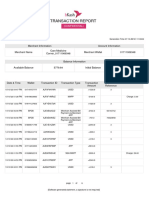

- Transaction StatementDocument10 pagesTransaction StatementVenki GajaNo ratings yet

- VAT Act 1997Document105 pagesVAT Act 1997JesseNderingoNo ratings yet

- Sprepl - Comparitive Statement For Supply of "SKF" Make Spherical Roller BearingDocument4 pagesSprepl - Comparitive Statement For Supply of "SKF" Make Spherical Roller BearingSuresh KumarNo ratings yet

- Service Tax On Works ContractDocument4 pagesService Tax On Works Contractrajs27No ratings yet

- Payment ProcessingDocument58 pagesPayment Processingsubash_dotNo ratings yet

- SA300622Document1 pageSA300622JEFF WONNo ratings yet

- Banking 05Document34 pagesBanking 05kannan sunilNo ratings yet

- Circular 1 Switching Fee AePS EKYC Card 0 0Document2 pagesCircular 1 Switching Fee AePS EKYC Card 0 0Sharanya KunduNo ratings yet

- University of Management and Technology Quotation Master Paints 01-08-2023Document2 pagesUniversity of Management and Technology Quotation Master Paints 01-08-2023usman khanNo ratings yet

- Tax-03-01-Basic-Principles of Taxation - EncryptedDocument11 pagesTax-03-01-Basic-Principles of Taxation - Encryptedgean eszekeilNo ratings yet

- CTA EB Case No. 250 and 255Document25 pagesCTA EB Case No. 250 and 255trina tsai100% (1)

- Allotment OrderDocument2 pagesAllotment Orderbchandu112No ratings yet

- Audit PlanDocument9 pagesAudit Planananda_joshi5178No ratings yet

- Solved Shannon Signs A 100 000 Contract To Develop A Plan ForDocument1 pageSolved Shannon Signs A 100 000 Contract To Develop A Plan ForAnbu jaromiaNo ratings yet

- ITC-Profit-Loss 2017 PDFDocument1 pageITC-Profit-Loss 2017 PDFShristi GutgutiaNo ratings yet

- Book Bill - BarnenduDocument2 pagesBook Bill - Barnendubarnendu.sarkarNo ratings yet