Download as pdf or txt

You might also like

- Case Assignment 2 Cutting Through The Fog Finding A Future With Fintech PDFDocument13 pagesCase Assignment 2 Cutting Through The Fog Finding A Future With Fintech PDFIndira Alfonso100% (2)

- Business Proposal For Using Fintech in Banking ArenaDocument4 pagesBusiness Proposal For Using Fintech in Banking ArenawoosanNo ratings yet

- Fintech in India - FinalDocument11 pagesFintech in India - FinalSRISHTI NARANG100% (1)

- Tybaf - Dhruvil Jain - 038Document5 pagesTybaf - Dhruvil Jain - 038DhruviNo ratings yet

- Nikunj Sharma CTIF Assignment 1Document14 pagesNikunj Sharma CTIF Assignment 1nikunj sharmaNo ratings yet

- MBA Global Trends Lecture 1 - Intro To Financial TechnologyDocument20 pagesMBA Global Trends Lecture 1 - Intro To Financial Technologyemanz21No ratings yet

- Fin TechDocument7 pagesFin TechHarsh ChaudharyNo ratings yet

- FinTech Report 2024Document82 pagesFinTech Report 2024darshanNo ratings yet

- Fintech ProjectDocument11 pagesFintech ProjectJaveria Umar100% (1)

- Fin Tech 1 To 30Document428 pagesFin Tech 1 To 30Harshil MehtaNo ratings yet

- S 1 - Overview of The Fintech IndustryDocument29 pagesS 1 - Overview of The Fintech IndustryPPNo ratings yet

- Management of Banks & Financial ServicesDocument22 pagesManagement of Banks & Financial ServicesSnehalNo ratings yet

- Fintech 400 PDFDocument410 pagesFintech 400 PDFHarshil MehtaNo ratings yet

- Southeast Asia Coming of The Digital Challenger BanksDocument21 pagesSoutheast Asia Coming of The Digital Challenger BanksSubhro SenguptaNo ratings yet

- Notes For The ClassDocument25 pagesNotes For The ClassgopiNo ratings yet

- Impact of Technology in Banking Industry FINAL PAPERDocument8 pagesImpact of Technology in Banking Industry FINAL PAPERSam MumoNo ratings yet

- Fint TechDocument13 pagesFint TechLaxmi SadhukhanNo ratings yet

- FinTechDocument9 pagesFinTecholabayoabdulbasitNo ratings yet

- Fintech v1Document22 pagesFintech v1anisaNo ratings yet

- Fintech Business ModelDocument30 pagesFintech Business ModeldantieNo ratings yet

- 3rd Sem Fintech Presentation by r20bc565Document12 pages3rd Sem Fintech Presentation by r20bc565Prithvi RajNo ratings yet

- Fintech Case StudyDocument5 pagesFintech Case StudyAMIT KUMAR CHAUHAN100% (1)

- Financial Technology (Fintech) - Its Uses and Impact On Our LivesDocument10 pagesFinancial Technology (Fintech) - Its Uses and Impact On Our Livessharafernando2No ratings yet

- Mape Fintech 2016 PDFDocument53 pagesMape Fintech 2016 PDFNarent ShekhawatNo ratings yet

- Fintech Wave in IndiaDocument7 pagesFintech Wave in IndiaT ForsythNo ratings yet

- Establishing and Managing Partnership With Fintechs Final 1Document81 pagesEstablishing and Managing Partnership With Fintechs Final 1mebreaNo ratings yet

- S 1 - Overview of The Fintech IndustryDocument28 pagesS 1 - Overview of The Fintech IndustryAninda DuttaNo ratings yet

- Importance of FintechDocument2 pagesImportance of Fintechneha1No ratings yet

- FinTech Paper - RevisedDocument11 pagesFinTech Paper - Revisedsrinivasa rao arigelaNo ratings yet

- The Future of FinanceDocument30 pagesThe Future of FinanceRenuka SharmaNo ratings yet

- Introduction To FinTechDocument34 pagesIntroduction To FinTechvarun022084100% (4)

- Fintech Session 1-10Document37 pagesFintech Session 1-10Taksh DhamiNo ratings yet

- Fin TechDocument6 pagesFin TechgopiNo ratings yet

- Digital Economy and Role of FintechDocument3 pagesDigital Economy and Role of FintechArun KumarNo ratings yet

- MCQ BankingDocument37 pagesMCQ BankingKripa Vijay100% (1)

- The Role of Regulation in Fintech Regtech in IndiaDocument24 pagesThe Role of Regulation in Fintech Regtech in Indiaintextu585No ratings yet

- FinTech and The Younger GeneraDocument19 pagesFinTech and The Younger GeneraĐinh HạnhNo ratings yet

- Financial Technology (Fintech) Is Used To Describe New Tech That Seeks To Improve and Automate TheDocument4 pagesFinancial Technology (Fintech) Is Used To Describe New Tech That Seeks To Improve and Automate ThePreah GulatiNo ratings yet

- Fintech - Banking Trends Technologies - Jan2024 McKinseyDocument8 pagesFintech - Banking Trends Technologies - Jan2024 McKinseyvinod.dumblekarNo ratings yet

- Fintech Sessions 11 - 20Document24 pagesFintech Sessions 11 - 20Taksh DhamiNo ratings yet

- Fintech Vs BankingDocument13 pagesFintech Vs BankingPHANEENDRA REDDY75% (4)

- Notes Fintech W 1 Lyst2346Document21 pagesNotes Fintech W 1 Lyst2346Ayush SrivastavaNo ratings yet

- Financial Technology Themes Meeting # 07-08: Course: Z0919 - ERP For Financial and Controlling Year: 2017Document17 pagesFinancial Technology Themes Meeting # 07-08: Course: Z0919 - ERP For Financial and Controlling Year: 2017Stella BenitaNo ratings yet

- Impact of Financial Technology On Payment and Lending in AsiaDocument19 pagesImpact of Financial Technology On Payment and Lending in AsiaADBI EventsNo ratings yet

- Financial TechnologyDocument8 pagesFinancial TechnologyGanesh FakatkarNo ratings yet

- 10th CRM Panayiotou PresentationDocument22 pages10th CRM Panayiotou PresentationKpessou GuihonNo ratings yet

- Fintech (Financial Technology)Document24 pagesFintech (Financial Technology)Jyotirmaya MaharanaNo ratings yet

- FinTech-transforming-finance ACCA November 2016Document16 pagesFinTech-transforming-finance ACCA November 2016CrowdfundInsider100% (2)

- IntroductionDocument3 pagesIntroduction3037 Vishva RNo ratings yet

- The Digital Fifth Fintech Annual Report 2022Document88 pagesThe Digital Fifth Fintech Annual Report 2022Shantanu YadavNo ratings yet

- Indian Financial System CIA-1bDocument21 pagesIndian Financial System CIA-1bprince chaudharyNo ratings yet

- Fintech InnovationDocument20 pagesFintech InnovationGiorgioNo ratings yet

- UNSGSA Report 2019 Final-CompressedDocument76 pagesUNSGSA Report 2019 Final-Compressedsaad.ahmadNo ratings yet

- Ayan Kumar Mazumder Jitendriya Sarkar Sayantan BhaduryDocument10 pagesAyan Kumar Mazumder Jitendriya Sarkar Sayantan BhaduryAyan KumarNo ratings yet

- Fin TechDocument32 pagesFin Techkritigupta.may1999No ratings yet

- FinTech - Friends or FoesDocument27 pagesFinTech - Friends or FoesRupak ThapaNo ratings yet

- Surge of Startups and Their SuccessesDocument17 pagesSurge of Startups and Their SuccessesAbhishek Kumar LalNo ratings yet

- Fintech-Banking SectorDocument17 pagesFintech-Banking Sectorhimanshu bhattNo ratings yet

- CP PLUS Certified IP Training Programme (CSE Level-I) : Participant Registration Form (CSE - 011/CHENNAI)Document1 pageCP PLUS Certified IP Training Programme (CSE Level-I) : Participant Registration Form (CSE - 011/CHENNAI)giri xdaNo ratings yet

- Fintech January2021Document110 pagesFintech January2021Edward Khoo100% (2)

- Wells Fargo Opportunity CheckingDocument4 pagesWells Fargo Opportunity Checkingson tungNo ratings yet

- VisaDocument338 pagesVisaRichu MehraNo ratings yet

- Weekly Report FormatDocument2 pagesWeekly Report FormatAbhishek ChoudharyNo ratings yet

- PSD2-AFP Online-The New Generation of Third-Party ProvidersDocument15 pagesPSD2-AFP Online-The New Generation of Third-Party Providersanshul2503No ratings yet

- Mitc Gold RCPDocument6 pagesMitc Gold RCPu4rishiNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument7 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balanceavnish sharmaNo ratings yet

- FAQ MDB Digital Savings AccountDocument4 pagesFAQ MDB Digital Savings AccountKamrul islam ShohagNo ratings yet

- Ecommerce Tracking in GA4 Via GTMDocument7 pagesEcommerce Tracking in GA4 Via GTMMehedi HassanNo ratings yet

- Articles Related To Fintech and Financial InclusionDocument4 pagesArticles Related To Fintech and Financial InclusionHabiba KausarNo ratings yet

- Case Study On AI in Finance SectorDocument4 pagesCase Study On AI in Finance Sectortejas pawarNo ratings yet

- Account Statement From 30 Jan 2019 To 8 Feb 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 30 Jan 2019 To 8 Feb 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balanceajaykumar soddalaNo ratings yet

- PRR 10748 WM Franchise Fee July 16 2007 To July 15 2015 PDFDocument98 pagesPRR 10748 WM Franchise Fee July 16 2007 To July 15 2015 PDFRecordTrac - City of OaklandNo ratings yet

- Sbi 8Document11 pagesSbi 8Logesh Waran KmlNo ratings yet

- MGV Form (FORM ABC)Document32 pagesMGV Form (FORM ABC)Muhammad MujibNo ratings yet

- Statement202003002999 PDFDocument2 pagesStatement202003002999 PDFAmir IjazNo ratings yet

- Myhomem 2 UcommondashboardcasaDocument1 pageMyhomem 2 UcommondashboardcasaMuhammad DanialNo ratings yet

- Nov-22 110058Document9 pagesNov-22 110058Shyam KumarNo ratings yet

- UOB Phone Banking GuideDocument2 pagesUOB Phone Banking GuideAldrin LapitanNo ratings yet

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument35 pagesDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalancevaraprasadNo ratings yet

- CFPB Sample Revocation Letter To Your Bank or Credit UnionDocument2 pagesCFPB Sample Revocation Letter To Your Bank or Credit UnionkongbengNo ratings yet

- Statement - PDF - Debit Card - Credit CardDocument3 pagesStatement - PDF - Debit Card - Credit Cardannawiewiora79No ratings yet

- I 1 ZCK 8 OKh 71 CC 7 CPDocument2 pagesI 1 ZCK 8 OKh 71 CC 7 CPAvinash SomannaNo ratings yet

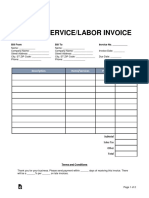

- Service Labor Invoice TemplateDocument2 pagesService Labor Invoice TemplateDavidNo ratings yet

- Cricket Bill Pay Methods - Cricket WirelessDocument6 pagesCricket Bill Pay Methods - Cricket WirelessJohn Michael Antonio100% (1)

- Easypaisa Account Transaction Show: 20/06/2021 To 09/09/2021Document1 pageEasypaisa Account Transaction Show: 20/06/2021 To 09/09/2021Shahzad AliNo ratings yet

- Account Statement PDFDocument12 pagesAccount Statement PDFBiswajeet Kumar RouthNo ratings yet

- Avalanche Bank Statement 26.02.2021Document2 pagesAvalanche Bank Statement 26.02.2021HerbertNo ratings yet