The Keynesian Theory Vs Classical Theory

The Keynesian Theory Vs Classical Theory

You might also like

- United Republic of Tanzania: Ministry of Health, Community Development, Gender, Elderly and ChildrenDocument50 pagesUnited Republic of Tanzania: Ministry of Health, Community Development, Gender, Elderly and ChildrenHAMIS MASOUDNo ratings yet

- Notes ch2 Discrete and Continuous DistributionsDocument48 pagesNotes ch2 Discrete and Continuous DistributionsErkin DNo ratings yet

- Itime Wearfit 2 Smart Bracelet ManualDocument5 pagesItime Wearfit 2 Smart Bracelet ManualOrestes CaminhaNo ratings yet

- Type-I and Type-II Errors in StatisticsDocument3 pagesType-I and Type-II Errors in StatisticsImtiyaz AhmadNo ratings yet

- Notes For Econ 8453Document51 pagesNotes For Econ 8453zaheer khanNo ratings yet

- Chapter 30 Money Growth and InflationDocument42 pagesChapter 30 Money Growth and InflationKING RAMBONo ratings yet

- Paper - 3Document9 pagesPaper - 3Mamatha ShettyNo ratings yet

- Econometrics Chapter 1& 2Document35 pagesEconometrics Chapter 1& 2Dagi AdanewNo ratings yet

- Pearson Correlation - SPSS Tutorials - LibGuides at Kent State UniversityDocument13 pagesPearson Correlation - SPSS Tutorials - LibGuides at Kent State Universityjohn gabrielNo ratings yet

- Chapter-I: Derivatives (Futures & Options)Document18 pagesChapter-I: Derivatives (Futures & Options)burranareshNo ratings yet

- Econ HWDocument3 pagesEcon HWmiggawee880% (1)

- Neyman Pearson LemmaDocument2 pagesNeyman Pearson Lemmaamiba45No ratings yet

- Elasticity of Demand.Document20 pagesElasticity of Demand.Gamaya EmmanuelNo ratings yet

- Stock Market Time Series AnalysisDocument12 pagesStock Market Time Series AnalysisTanay JainNo ratings yet

- MCA4020-Model Question PaperDocument18 pagesMCA4020-Model Question PaperAppTest PINo ratings yet

- Econ MIdterm 2 PractiseDocument11 pagesEcon MIdterm 2 PractiseConnorNo ratings yet

- Development EconomicsI ModuleI-1Document106 pagesDevelopment EconomicsI ModuleI-1Terefe Bergene bussaNo ratings yet

- Assignment 2: Name: Saif Ali Momin Erp Id: 08003 Course: Business Finance IIDocument39 pagesAssignment 2: Name: Saif Ali Momin Erp Id: 08003 Course: Business Finance IISaif Ali MominNo ratings yet

- Inflation Instruments OpenGammaDocument4 pagesInflation Instruments OpenGammadondan123No ratings yet

- The Sargent & Wallace Policy Ineffectiveness Proposition, Lucas CritiqueDocument8 pagesThe Sargent & Wallace Policy Ineffectiveness Proposition, Lucas CritiquehishamsaukNo ratings yet

- RA-Chambers-Time SlotsDocument152 pagesRA-Chambers-Time Slotsaryanmalik3333333333No ratings yet

- Karl Pearson's Coefficient of Correlation: FormulaDocument2 pagesKarl Pearson's Coefficient of Correlation: FormulaAnupriyaNo ratings yet

- TheoryDocument128 pagesTheorykrishna45No ratings yet

- Lecture 3Document11 pagesLecture 3Huthaifah Salman100% (1)

- SAS Dumps For Base SAS 9 ExamDocument15 pagesSAS Dumps For Base SAS 9 Examvikrants13060% (1)

- CH Ii Business StatDocument27 pagesCH Ii Business StatWudneh AmareNo ratings yet

- 1.1 Sunpharma and Pfizer 1 2 3 4Document7 pages1.1 Sunpharma and Pfizer 1 2 3 4AnanthkrishnanNo ratings yet

- Kaplan-Meier Estimator: Association. The Journal Editor, John Tukey, Convinced Them To Combine TheirDocument7 pagesKaplan-Meier Estimator: Association. The Journal Editor, John Tukey, Convinced Them To Combine TheirRafles SimbolonNo ratings yet

- Global Vehicle Sales PGM Demand Hydrogen Aug 2020Document13 pagesGlobal Vehicle Sales PGM Demand Hydrogen Aug 2020ResearchtimeNo ratings yet

- Assessment - 1 - Pfizer & Sunpharma - Group 09Document4 pagesAssessment - 1 - Pfizer & Sunpharma - Group 09AnanthkrishnanNo ratings yet

- Research Methodology For Mobile Phone OperatorsDocument50 pagesResearch Methodology For Mobile Phone Operatorsanandita28100% (2)

- 8 - Portfolio AnalysisDocument24 pages8 - Portfolio AnalysisJosh AckmanNo ratings yet

- Thimmaiah B C - Asst Registrar - PatentDocument12 pagesThimmaiah B C - Asst Registrar - PatentTHIMMAIAH B CNo ratings yet

- Basic BiostatisticsDocument319 pagesBasic BiostatisticsgirumNo ratings yet

- Correlation and Chi-Square Test - LDR 280Document71 pagesCorrelation and Chi-Square Test - LDR 280RohanPuthalath100% (1)

- 3122-Article Text-6458-1-10-20210709Document23 pages3122-Article Text-6458-1-10-20210709epiphaneNo ratings yet

- Data Analysis Final AssignmentDocument14 pagesData Analysis Final AssignmentAnamitra SenNo ratings yet

- 14 Principles of Management by Henri Fayol AMPAROBODOSODocument60 pages14 Principles of Management by Henri Fayol AMPAROBODOSORonalyn Gaor VillegasNo ratings yet

- Answer 2 Consumption FunctionDocument4 pagesAnswer 2 Consumption FunctionNave2n adventurism & art works.No ratings yet

- Assessing The Impact of Fuel Subsidy Removal in NigeriaDocument5 pagesAssessing The Impact of Fuel Subsidy Removal in NigeriamuhammadNo ratings yet

- Unit 3 and 4Document62 pagesUnit 3 and 4Piyush SinglaNo ratings yet

- Analysis of Myntra's App Only Move - Project ProposalDocument3 pagesAnalysis of Myntra's App Only Move - Project ProposalChetanDVNo ratings yet

- Marginal Productivity Theory of DistributionDocument8 pagesMarginal Productivity Theory of DistributionsamNo ratings yet

- Topics To Be Covered: Introduction Single Item - Deterministic Models - Purchase Inventory Models WithDocument13 pagesTopics To Be Covered: Introduction Single Item - Deterministic Models - Purchase Inventory Models WithRama RajuNo ratings yet

- Bibliometric Survey For Adoption of Building Information Modeling (BIM) in Construction IndustryDocument16 pagesBibliometric Survey For Adoption of Building Information Modeling (BIM) in Construction IndustryMateo RamirezNo ratings yet

- Productivity, Output, and EmploymentDocument49 pagesProductivity, Output, and EmploymentAditi RustagiNo ratings yet

- 2 BanksDocument8 pages2 BanksRajni KumariNo ratings yet

- Time Series Econometrics For MSC 20212022Document268 pagesTime Series Econometrics For MSC 20212022Tise TegyNo ratings yet

- The Roles of StatisticsDocument56 pagesThe Roles of StatisticsVinh HuỳnhNo ratings yet

- Index NumbersDocument16 pagesIndex NumbersMuhammad Faisal QureshiNo ratings yet

- Application of The SAW Method in Support Systems Decisions On Providing Assistance To Market TradersDocument10 pagesApplication of The SAW Method in Support Systems Decisions On Providing Assistance To Market TradersMas ZNo ratings yet

- Classical Economics Vs Keynesian Economics Part 1Document5 pagesClassical Economics Vs Keynesian Economics Part 1Aahil AliNo ratings yet

- Week 12Document13 pagesWeek 12nsnnsNo ratings yet

- Longer Term Investments - en - 1474497Document23 pagesLonger Term Investments - en - 1474497Vincent ChanNo ratings yet

- M1520 Rev A Optilab and MicroOptilab Users GuideDocument117 pagesM1520 Rev A Optilab and MicroOptilab Users GuideChEAF AdminNo ratings yet

- Tests of Significance and Measures of AssociationDocument21 pagesTests of Significance and Measures of Associationanandan777supmNo ratings yet

- Kenys TheoryDocument4 pagesKenys TheoryClaire Montaño LincunaNo ratings yet

- 6c7d5keynesian TheoryDocument5 pages6c7d5keynesian TheoryShubhamNo ratings yet

- Keynesian TheoryDocument7 pagesKeynesian TheoryAbhishek Malhotra100% (1)

- Keynesian ApproachDocument20 pagesKeynesian ApproachDeepikaNo ratings yet

- Gender & LGBTQ IntegrationDocument85 pagesGender & LGBTQ Integrationkilon miniNo ratings yet

- Ambisyon Natin 2040 & Updated PDP 2017-2022Document15 pagesAmbisyon Natin 2040 & Updated PDP 2017-2022kilon miniNo ratings yet

- Is There A Philippine Public GovernmentDocument2 pagesIs There A Philippine Public Governmentkilon miniNo ratings yet

- Summary of Contributions of People in The Field of ManagementDocument2 pagesSummary of Contributions of People in The Field of Managementkilon miniNo ratings yet

- 2020 Overseas Filipino WorkersDocument6 pages2020 Overseas Filipino Workerskilon miniNo ratings yet

- Public ExpenditureDocument8 pagesPublic Expenditurekilon miniNo ratings yet

- Main Characteristics of Capitalist EconomiesDocument3 pagesMain Characteristics of Capitalist Economieskilon miniNo ratings yet

- Global Operations & Supply Chain ManagementDocument37 pagesGlobal Operations & Supply Chain ManagementAnonymousNo ratings yet

- Guide To The Markets: Market InsightsDocument71 pagesGuide To The Markets: Market Insightssofia goicocheaNo ratings yet

- Quantity Discounts For The Eoq ModelDocument13 pagesQuantity Discounts For The Eoq Modelnatalie clyde mates100% (1)

- Pakarinen Tea PDFDocument170 pagesPakarinen Tea PDFNAMRATA SHARMANo ratings yet

- QMT AssignmentDocument95 pagesQMT AssignmentZeeshan BakaliNo ratings yet

- Microeconomics For Managers: Biresh Sahoo, PH.DDocument57 pagesMicroeconomics For Managers: Biresh Sahoo, PH.DpratmamboNo ratings yet

- Financial Sectors-Deepika Bhati FIMTDocument21 pagesFinancial Sectors-Deepika Bhati FIMTNITISH BHATINo ratings yet

- Full Credit Report - EXAMPLEDocument1 pageFull Credit Report - EXAMPLEChris PearsonNo ratings yet

- Economics IB - Real World Examples of Economic TopicsDocument3 pagesEconomics IB - Real World Examples of Economic TopicsRishika KothariNo ratings yet

- ACCOUNTINGDocument10 pagesACCOUNTINGAyaw Ko NaNo ratings yet

- Juakali Section 3 Access RoadDocument34 pagesJuakali Section 3 Access RoadKISUJA MADUHUNo ratings yet

- Commercial Transactions Law 2015: DR Andrew HutchisonDocument47 pagesCommercial Transactions Law 2015: DR Andrew HutchisonNomvelo_JuiceNo ratings yet

- The Atlas of Economic Indicators PDFDocument123 pagesThe Atlas of Economic Indicators PDFswinki383% (6)

- NALCODocument1 pageNALCOMladen GomilanovicNo ratings yet

- 5 Years Anna University GE2022 Total Quality ManagemntDocument19 pages5 Years Anna University GE2022 Total Quality ManagemntManimegalaiNo ratings yet

- Exam Summary PUB Comp Graduate July 2020Document24 pagesExam Summary PUB Comp Graduate July 2020ajrevillaNo ratings yet

- Internship Report Saqlain ArifDocument65 pagesInternship Report Saqlain ArifSaqlain KhanNo ratings yet

- Annual Report 2017-2018Document140 pagesAnnual Report 2017-2018Pema DorjiNo ratings yet

- MICRO-5-Competitive Market - HDocument34 pagesMICRO-5-Competitive Market - HLỘC LÊ QUÝNo ratings yet

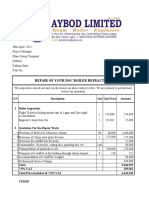

- Repair of Doc Boiler RefractoryDocument2 pagesRepair of Doc Boiler RefractoryIshola TaiwoNo ratings yet

- AfCFTA E-Tariff Book - Draft User Guide V0.4Document14 pagesAfCFTA E-Tariff Book - Draft User Guide V0.4Fuaad DodooNo ratings yet

- Contemporary Issues in Fashion and TextilesDocument5 pagesContemporary Issues in Fashion and TextilesPrasad KumbhareNo ratings yet

- Mumbai To Shirdi Vande Bharat PDFDocument21 pagesMumbai To Shirdi Vande Bharat PDFvivek patilNo ratings yet

- ASIANDocument8 pagesASIANubaida haqueNo ratings yet

- Admission of A Partner WorksheetDocument4 pagesAdmission of A Partner Worksheetneeraj sharmaNo ratings yet

- Ds 3 ZJG PFA8 VV 0 Uhb Itzm K2 ARl EGBc 82 SQB 9 ZHC 4 PDocument1 pageDs 3 ZJG PFA8 VV 0 Uhb Itzm K2 ARl EGBc 82 SQB 9 ZHC 4 PprabindraNo ratings yet

- Financial Risk Management Notes II Year III Sem Updated.Document95 pagesFinancial Risk Management Notes II Year III Sem Updated.afeefa siddiquaNo ratings yet

- Pure CompetitionDocument7 pagesPure CompetitionEricka TorresNo ratings yet

- Chapter 6 - Effective Interest MethodDocument62 pagesChapter 6 - Effective Interest MethodCeline Therese BuNo ratings yet

- Statements 9261Document6 pagesStatements 9261Jaun Tew Theory PhuorrNo ratings yet

Download as docx, pdf, or txt

You might also like

- United Republic of Tanzania: Ministry of Health, Community Development, Gender, Elderly and ChildrenDocument50 pagesUnited Republic of Tanzania: Ministry of Health, Community Development, Gender, Elderly and ChildrenHAMIS MASOUDNo ratings yet

- Notes ch2 Discrete and Continuous DistributionsDocument48 pagesNotes ch2 Discrete and Continuous DistributionsErkin DNo ratings yet

- Itime Wearfit 2 Smart Bracelet ManualDocument5 pagesItime Wearfit 2 Smart Bracelet ManualOrestes CaminhaNo ratings yet

- Type-I and Type-II Errors in StatisticsDocument3 pagesType-I and Type-II Errors in StatisticsImtiyaz AhmadNo ratings yet

- Notes For Econ 8453Document51 pagesNotes For Econ 8453zaheer khanNo ratings yet

- Chapter 30 Money Growth and InflationDocument42 pagesChapter 30 Money Growth and InflationKING RAMBONo ratings yet

- Paper - 3Document9 pagesPaper - 3Mamatha ShettyNo ratings yet

- Econometrics Chapter 1& 2Document35 pagesEconometrics Chapter 1& 2Dagi AdanewNo ratings yet

- Pearson Correlation - SPSS Tutorials - LibGuides at Kent State UniversityDocument13 pagesPearson Correlation - SPSS Tutorials - LibGuides at Kent State Universityjohn gabrielNo ratings yet

- Chapter-I: Derivatives (Futures & Options)Document18 pagesChapter-I: Derivatives (Futures & Options)burranareshNo ratings yet

- Econ HWDocument3 pagesEcon HWmiggawee880% (1)

- Neyman Pearson LemmaDocument2 pagesNeyman Pearson Lemmaamiba45No ratings yet

- Elasticity of Demand.Document20 pagesElasticity of Demand.Gamaya EmmanuelNo ratings yet

- Stock Market Time Series AnalysisDocument12 pagesStock Market Time Series AnalysisTanay JainNo ratings yet

- MCA4020-Model Question PaperDocument18 pagesMCA4020-Model Question PaperAppTest PINo ratings yet

- Econ MIdterm 2 PractiseDocument11 pagesEcon MIdterm 2 PractiseConnorNo ratings yet

- Development EconomicsI ModuleI-1Document106 pagesDevelopment EconomicsI ModuleI-1Terefe Bergene bussaNo ratings yet

- Assignment 2: Name: Saif Ali Momin Erp Id: 08003 Course: Business Finance IIDocument39 pagesAssignment 2: Name: Saif Ali Momin Erp Id: 08003 Course: Business Finance IISaif Ali MominNo ratings yet

- Inflation Instruments OpenGammaDocument4 pagesInflation Instruments OpenGammadondan123No ratings yet

- The Sargent & Wallace Policy Ineffectiveness Proposition, Lucas CritiqueDocument8 pagesThe Sargent & Wallace Policy Ineffectiveness Proposition, Lucas CritiquehishamsaukNo ratings yet

- RA-Chambers-Time SlotsDocument152 pagesRA-Chambers-Time Slotsaryanmalik3333333333No ratings yet

- Karl Pearson's Coefficient of Correlation: FormulaDocument2 pagesKarl Pearson's Coefficient of Correlation: FormulaAnupriyaNo ratings yet

- TheoryDocument128 pagesTheorykrishna45No ratings yet

- Lecture 3Document11 pagesLecture 3Huthaifah Salman100% (1)

- SAS Dumps For Base SAS 9 ExamDocument15 pagesSAS Dumps For Base SAS 9 Examvikrants13060% (1)

- CH Ii Business StatDocument27 pagesCH Ii Business StatWudneh AmareNo ratings yet

- 1.1 Sunpharma and Pfizer 1 2 3 4Document7 pages1.1 Sunpharma and Pfizer 1 2 3 4AnanthkrishnanNo ratings yet

- Kaplan-Meier Estimator: Association. The Journal Editor, John Tukey, Convinced Them To Combine TheirDocument7 pagesKaplan-Meier Estimator: Association. The Journal Editor, John Tukey, Convinced Them To Combine TheirRafles SimbolonNo ratings yet

- Global Vehicle Sales PGM Demand Hydrogen Aug 2020Document13 pagesGlobal Vehicle Sales PGM Demand Hydrogen Aug 2020ResearchtimeNo ratings yet

- Assessment - 1 - Pfizer & Sunpharma - Group 09Document4 pagesAssessment - 1 - Pfizer & Sunpharma - Group 09AnanthkrishnanNo ratings yet

- Research Methodology For Mobile Phone OperatorsDocument50 pagesResearch Methodology For Mobile Phone Operatorsanandita28100% (2)

- 8 - Portfolio AnalysisDocument24 pages8 - Portfolio AnalysisJosh AckmanNo ratings yet

- Thimmaiah B C - Asst Registrar - PatentDocument12 pagesThimmaiah B C - Asst Registrar - PatentTHIMMAIAH B CNo ratings yet

- Basic BiostatisticsDocument319 pagesBasic BiostatisticsgirumNo ratings yet

- Correlation and Chi-Square Test - LDR 280Document71 pagesCorrelation and Chi-Square Test - LDR 280RohanPuthalath100% (1)

- 3122-Article Text-6458-1-10-20210709Document23 pages3122-Article Text-6458-1-10-20210709epiphaneNo ratings yet

- Data Analysis Final AssignmentDocument14 pagesData Analysis Final AssignmentAnamitra SenNo ratings yet

- 14 Principles of Management by Henri Fayol AMPAROBODOSODocument60 pages14 Principles of Management by Henri Fayol AMPAROBODOSORonalyn Gaor VillegasNo ratings yet

- Answer 2 Consumption FunctionDocument4 pagesAnswer 2 Consumption FunctionNave2n adventurism & art works.No ratings yet

- Assessing The Impact of Fuel Subsidy Removal in NigeriaDocument5 pagesAssessing The Impact of Fuel Subsidy Removal in NigeriamuhammadNo ratings yet

- Unit 3 and 4Document62 pagesUnit 3 and 4Piyush SinglaNo ratings yet

- Analysis of Myntra's App Only Move - Project ProposalDocument3 pagesAnalysis of Myntra's App Only Move - Project ProposalChetanDVNo ratings yet

- Marginal Productivity Theory of DistributionDocument8 pagesMarginal Productivity Theory of DistributionsamNo ratings yet

- Topics To Be Covered: Introduction Single Item - Deterministic Models - Purchase Inventory Models WithDocument13 pagesTopics To Be Covered: Introduction Single Item - Deterministic Models - Purchase Inventory Models WithRama RajuNo ratings yet

- Bibliometric Survey For Adoption of Building Information Modeling (BIM) in Construction IndustryDocument16 pagesBibliometric Survey For Adoption of Building Information Modeling (BIM) in Construction IndustryMateo RamirezNo ratings yet

- Productivity, Output, and EmploymentDocument49 pagesProductivity, Output, and EmploymentAditi RustagiNo ratings yet

- 2 BanksDocument8 pages2 BanksRajni KumariNo ratings yet

- Time Series Econometrics For MSC 20212022Document268 pagesTime Series Econometrics For MSC 20212022Tise TegyNo ratings yet

- The Roles of StatisticsDocument56 pagesThe Roles of StatisticsVinh HuỳnhNo ratings yet

- Index NumbersDocument16 pagesIndex NumbersMuhammad Faisal QureshiNo ratings yet

- Application of The SAW Method in Support Systems Decisions On Providing Assistance To Market TradersDocument10 pagesApplication of The SAW Method in Support Systems Decisions On Providing Assistance To Market TradersMas ZNo ratings yet

- Classical Economics Vs Keynesian Economics Part 1Document5 pagesClassical Economics Vs Keynesian Economics Part 1Aahil AliNo ratings yet

- Week 12Document13 pagesWeek 12nsnnsNo ratings yet

- Longer Term Investments - en - 1474497Document23 pagesLonger Term Investments - en - 1474497Vincent ChanNo ratings yet

- M1520 Rev A Optilab and MicroOptilab Users GuideDocument117 pagesM1520 Rev A Optilab and MicroOptilab Users GuideChEAF AdminNo ratings yet

- Tests of Significance and Measures of AssociationDocument21 pagesTests of Significance and Measures of Associationanandan777supmNo ratings yet

- Kenys TheoryDocument4 pagesKenys TheoryClaire Montaño LincunaNo ratings yet

- 6c7d5keynesian TheoryDocument5 pages6c7d5keynesian TheoryShubhamNo ratings yet

- Keynesian TheoryDocument7 pagesKeynesian TheoryAbhishek Malhotra100% (1)

- Keynesian ApproachDocument20 pagesKeynesian ApproachDeepikaNo ratings yet

- Gender & LGBTQ IntegrationDocument85 pagesGender & LGBTQ Integrationkilon miniNo ratings yet

- Ambisyon Natin 2040 & Updated PDP 2017-2022Document15 pagesAmbisyon Natin 2040 & Updated PDP 2017-2022kilon miniNo ratings yet

- Is There A Philippine Public GovernmentDocument2 pagesIs There A Philippine Public Governmentkilon miniNo ratings yet

- Summary of Contributions of People in The Field of ManagementDocument2 pagesSummary of Contributions of People in The Field of Managementkilon miniNo ratings yet

- 2020 Overseas Filipino WorkersDocument6 pages2020 Overseas Filipino Workerskilon miniNo ratings yet

- Public ExpenditureDocument8 pagesPublic Expenditurekilon miniNo ratings yet

- Main Characteristics of Capitalist EconomiesDocument3 pagesMain Characteristics of Capitalist Economieskilon miniNo ratings yet

- Global Operations & Supply Chain ManagementDocument37 pagesGlobal Operations & Supply Chain ManagementAnonymousNo ratings yet

- Guide To The Markets: Market InsightsDocument71 pagesGuide To The Markets: Market Insightssofia goicocheaNo ratings yet

- Quantity Discounts For The Eoq ModelDocument13 pagesQuantity Discounts For The Eoq Modelnatalie clyde mates100% (1)

- Pakarinen Tea PDFDocument170 pagesPakarinen Tea PDFNAMRATA SHARMANo ratings yet

- QMT AssignmentDocument95 pagesQMT AssignmentZeeshan BakaliNo ratings yet

- Microeconomics For Managers: Biresh Sahoo, PH.DDocument57 pagesMicroeconomics For Managers: Biresh Sahoo, PH.DpratmamboNo ratings yet

- Financial Sectors-Deepika Bhati FIMTDocument21 pagesFinancial Sectors-Deepika Bhati FIMTNITISH BHATINo ratings yet

- Full Credit Report - EXAMPLEDocument1 pageFull Credit Report - EXAMPLEChris PearsonNo ratings yet

- Economics IB - Real World Examples of Economic TopicsDocument3 pagesEconomics IB - Real World Examples of Economic TopicsRishika KothariNo ratings yet

- ACCOUNTINGDocument10 pagesACCOUNTINGAyaw Ko NaNo ratings yet

- Juakali Section 3 Access RoadDocument34 pagesJuakali Section 3 Access RoadKISUJA MADUHUNo ratings yet

- Commercial Transactions Law 2015: DR Andrew HutchisonDocument47 pagesCommercial Transactions Law 2015: DR Andrew HutchisonNomvelo_JuiceNo ratings yet

- The Atlas of Economic Indicators PDFDocument123 pagesThe Atlas of Economic Indicators PDFswinki383% (6)

- NALCODocument1 pageNALCOMladen GomilanovicNo ratings yet

- 5 Years Anna University GE2022 Total Quality ManagemntDocument19 pages5 Years Anna University GE2022 Total Quality ManagemntManimegalaiNo ratings yet

- Exam Summary PUB Comp Graduate July 2020Document24 pagesExam Summary PUB Comp Graduate July 2020ajrevillaNo ratings yet

- Internship Report Saqlain ArifDocument65 pagesInternship Report Saqlain ArifSaqlain KhanNo ratings yet

- Annual Report 2017-2018Document140 pagesAnnual Report 2017-2018Pema DorjiNo ratings yet

- MICRO-5-Competitive Market - HDocument34 pagesMICRO-5-Competitive Market - HLỘC LÊ QUÝNo ratings yet

- Repair of Doc Boiler RefractoryDocument2 pagesRepair of Doc Boiler RefractoryIshola TaiwoNo ratings yet

- AfCFTA E-Tariff Book - Draft User Guide V0.4Document14 pagesAfCFTA E-Tariff Book - Draft User Guide V0.4Fuaad DodooNo ratings yet

- Contemporary Issues in Fashion and TextilesDocument5 pagesContemporary Issues in Fashion and TextilesPrasad KumbhareNo ratings yet

- Mumbai To Shirdi Vande Bharat PDFDocument21 pagesMumbai To Shirdi Vande Bharat PDFvivek patilNo ratings yet

- ASIANDocument8 pagesASIANubaida haqueNo ratings yet

- Admission of A Partner WorksheetDocument4 pagesAdmission of A Partner Worksheetneeraj sharmaNo ratings yet

- Ds 3 ZJG PFA8 VV 0 Uhb Itzm K2 ARl EGBc 82 SQB 9 ZHC 4 PDocument1 pageDs 3 ZJG PFA8 VV 0 Uhb Itzm K2 ARl EGBc 82 SQB 9 ZHC 4 PprabindraNo ratings yet

- Financial Risk Management Notes II Year III Sem Updated.Document95 pagesFinancial Risk Management Notes II Year III Sem Updated.afeefa siddiquaNo ratings yet

- Pure CompetitionDocument7 pagesPure CompetitionEricka TorresNo ratings yet

- Chapter 6 - Effective Interest MethodDocument62 pagesChapter 6 - Effective Interest MethodCeline Therese BuNo ratings yet

- Statements 9261Document6 pagesStatements 9261Jaun Tew Theory PhuorrNo ratings yet