Download as pdf or txt

You might also like

- Agreement of Sale Cum General Power of Attorney: (With Possession)Document7 pagesAgreement of Sale Cum General Power of Attorney: (With Possession)DrSyed ShujauddinNo ratings yet

- Cost Benefit AnalysisDocument2 pagesCost Benefit AnalysisAriel Peralta AdvientoNo ratings yet

- Guidelines and Instructions For BIR FORM No. 2118-EA Estate Tax Amnesty ReturnDocument1 pageGuidelines and Instructions For BIR FORM No. 2118-EA Estate Tax Amnesty ReturnChaNo ratings yet

- BIR Ruling No. 340-11 - E-BooksDocument5 pagesBIR Ruling No. 340-11 - E-BooksCkey ArNo ratings yet

- Special Power of Attorney For IncorporationDocument2 pagesSpecial Power of Attorney For IncorporationALEXANDRIA RABANESNo ratings yet

- Real Property TaxationDocument125 pagesReal Property TaxationLaw_Portal100% (5)

- The Role of Government Assessors Appraisers in Valuing PropertiesDocument154 pagesThe Role of Government Assessors Appraisers in Valuing PropertiesVinz Molina100% (1)

- PD 1812 - Amended Provision of PD 464 (Real Prop Tax Code)Document2 pagesPD 1812 - Amended Provision of PD 464 (Real Prop Tax Code)Rocky MarcianoNo ratings yet

- Real Propert Y: TaxationDocument41 pagesReal Propert Y: TaxationFreeza Masculino FabrigasNo ratings yet

- Dof Do 37-09 Ivs AdoptionDocument2 pagesDof Do 37-09 Ivs Adoptionrubydelacruz100% (1)

- 2021 REA Licensure Examination AM With Revised AnswerDocument76 pages2021 REA Licensure Examination AM With Revised AnswerVincent De CardoNo ratings yet

- APRSL2021 Vergonville - May18Document10 pagesAPRSL2021 Vergonville - May18Maureen ban-egNo ratings yet

- REAL PROPERTY TAXATION - PresentationDocument71 pagesREAL PROPERTY TAXATION - PresentationMarcial Militante100% (1)

- PHILIPPINE VALUATION STANDARDS NotesDocument15 pagesPHILIPPINE VALUATION STANDARDS NotesPrince EG DltgNo ratings yet

- LTD Lecture 07192023Document9 pagesLTD Lecture 07192023Emmanuel FernandezNo ratings yet

- Resa and Irr - Cres 2014Document23 pagesResa and Irr - Cres 2014Ariel MartinezNo ratings yet

- 3 REB Practice QuestionsDocument27 pages3 REB Practice QuestionsPrince EG DltgNo ratings yet

- Fundamentals of Real Estate Management Real Estate Management ProfessionDocument56 pagesFundamentals of Real Estate Management Real Estate Management Professionleanzyjenel domiginaNo ratings yet

- Real Estate Service Act REM1Document29 pagesReal Estate Service Act REM1Francis L100% (1)

- Part II. Chapter 2 Imposition of Real Property TaxDocument30 pagesPart II. Chapter 2 Imposition of Real Property TaxRuiz, CherryjaneNo ratings yet

- Ra 4276Document8 pagesRa 4276Monique Allen LoriaNo ratings yet

- Real Estate Appraisal ReviewerDocument1 pageReal Estate Appraisal ReviewerventuristaNo ratings yet

- Fundamentals of Real PropertyDocument74 pagesFundamentals of Real PropertyFrancis L100% (1)

- PD 464Document36 pagesPD 464Nath VillenaNo ratings yet

- When To Reject Loan Collateral OffersDocument6 pagesWhen To Reject Loan Collateral OffersLuningning CariosNo ratings yet

- Guillarte Angelita Cost Approach AppraisalDocument14 pagesGuillarte Angelita Cost Approach AppraisalZara Kanielle GuillarteNo ratings yet

- UntitledDocument21 pagesUntitledBRENDA BRADECINANo ratings yet

- Dealings in PropertyDocument30 pagesDealings in PropertyPrie DitucalanNo ratings yet

- Real Estate Service Act of The Philippines PDFDocument15 pagesReal Estate Service Act of The Philippines PDFVener Angelo MargalloNo ratings yet

- PRBRES ResolutionsDocument1 pagePRBRES ResolutionsDexterNo ratings yet

- Definition of EncumbranceDocument3 pagesDefinition of EncumbranceamvronaNo ratings yet

- 2016 Module 1 ExamDocument17 pages2016 Module 1 ExamTacloban RebsNo ratings yet

- 1.4 Real-Estate-Taxation With Problems and Answers - REBDocument82 pages1.4 Real-Estate-Taxation With Problems and Answers - REBgore.soliven100% (1)

- 2WK1 - Objectives and Purposes of Property ManagementDocument9 pages2WK1 - Objectives and Purposes of Property ManagementAnna SalinoNo ratings yet

- Ordinary V CapitalDocument26 pagesOrdinary V CapitalerwinNo ratings yet

- Real Estate Board Exam Question On Maceda Law, RA 6552Document1 pageReal Estate Board Exam Question On Maceda Law, RA 6552Tenshi FukuiNo ratings yet

- As Amended by DO No. 22, S. of 1987, DAO No. 2, S. of 1988 and DAO No. 6, S. of 1994Document12 pagesAs Amended by DO No. 22, S. of 1987, DAO No. 2, S. of 1988 and DAO No. 6, S. of 1994Richard Villaverde100% (1)

- Philippine Valuation StandardsDocument45 pagesPhilippine Valuation StandardsAl MarzolNo ratings yet

- BIR RR 07-2003Document8 pagesBIR RR 07-2003Brian BaldwinNo ratings yet

- Code of Ethic and Responsibilities - Philippine Real Estate Broker ReviewerDocument16 pagesCode of Ethic and Responsibilities - Philippine Real Estate Broker ReviewerRhea SunshineNo ratings yet

- Valuation of Expropriated PropertiesDocument10 pagesValuation of Expropriated PropertiesLuningning CariosNo ratings yet

- Batas Pambansa 185Document56 pagesBatas Pambansa 185heartiee1018No ratings yet

- Appraisal and Assessment in The Government Sector PrelimDocument6 pagesAppraisal and Assessment in The Government Sector PrelimMichelle EsperalNo ratings yet

- Broker Reviewer 2022Document8 pagesBroker Reviewer 2022Janzel SantillanNo ratings yet

- Real Estate Taxation - Transfer of PropertyDocument9 pagesReal Estate Taxation - Transfer of PropertyJuan FrivaldoNo ratings yet

- Taxation QuestionsDocument63 pagesTaxation QuestionsPrince EG DltgNo ratings yet

- 3.1n Theories & Principles - UnlockedDocument11 pages3.1n Theories & Principles - Unlockedccc100% (1)

- Regalian DoctrineDocument4 pagesRegalian DoctrineJacinto HyacinthNo ratings yet

- Notes On Fundamentals of Property OwnershipDocument17 pagesNotes On Fundamentals of Property OwnershipJoshua ArmestoNo ratings yet

- PARA SeminarDocument2 pagesPARA SeminarShielaMarie MalanoNo ratings yet

- FINANCE Time Value PvoaDocument24 pagesFINANCE Time Value PvoaJanzel SantillanNo ratings yet

- Resa Irr. Ra 9646Document17 pagesResa Irr. Ra 9646Israeli Tagalog-Brondial100% (1)

- IVSC Effective 31 Jan 2022 Red-LineDocument141 pagesIVSC Effective 31 Jan 2022 Red-LineCesar MedinaNo ratings yet

- RA 9700: Comprehensive Agrarian Reform Law/CARPER (Approved August 7, 2009)Document3 pagesRA 9700: Comprehensive Agrarian Reform Law/CARPER (Approved August 7, 2009)Marcial MilitanteNo ratings yet

- Appraisal of Machinery and EquipmentDocument3 pagesAppraisal of Machinery and EquipmentJen ManriqueNo ratings yet

- RAMO 1-20 Updated Handbook On Audit Procedures and TECHNIQUEDocument96 pagesRAMO 1-20 Updated Handbook On Audit Procedures and TECHNIQUEDante JulianNo ratings yet

- 02.07.14am Fundamentals of Real Property Ownership - Part 1 DoneDocument6 pages02.07.14am Fundamentals of Real Property Ownership - Part 1 DoneZillah GallardoNo ratings yet

- Real Estate TaxationDocument6 pagesReal Estate TaxationShine Revilla - MontefalconNo ratings yet

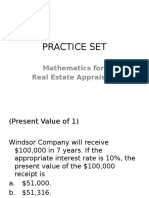

- Practice SetDocument39 pagesPractice SetDionico O. Payo Jr.No ratings yet

- Part I. Chapter 9 Civil Remedies by The LGU For Collection of RevenuesDocument36 pagesPart I. Chapter 9 Civil Remedies by The LGU For Collection of RevenuesFunyoungNo ratings yet

- Part II. Chapter 5 Collection of Real Property TaxDocument39 pagesPart II. Chapter 5 Collection of Real Property TaxRuiz, CherryjaneNo ratings yet

- 2012 08 NIRC Remedies TablesDocument8 pages2012 08 NIRC Remedies TablesJaime Dadbod NolascoNo ratings yet

- 96 Calendar ActivitiesDocument2 pages96 Calendar ActivitiesRuiz, CherryjaneNo ratings yet

- Chapter 3-8Document2 pagesChapter 3-8Ruiz, CherryjaneNo ratings yet

- HISTORYDocument3 pagesHISTORYRuiz, CherryjaneNo ratings yet

- CH 19 Acctg For Foreign Currency TransacDocument35 pagesCH 19 Acctg For Foreign Currency TransacRuiz, CherryjaneNo ratings yet

- Proposal HearingDocument1 pageProposal HearingRuiz, CherryjaneNo ratings yet

- PFRS 5 Discontinued OperationsDocument11 pagesPFRS 5 Discontinued OperationsRuiz, CherryjaneNo ratings yet

- Wells Fargo-A Case-Study On Corporate GovernanceDocument4 pagesWells Fargo-A Case-Study On Corporate GovernanceRuiz, CherryjaneNo ratings yet

- Kinds of ObligationsDocument1 pageKinds of ObligationsRuiz, CherryjaneNo ratings yet

- Chapter 3 Exercise 1 Group Activity PDFDocument2 pagesChapter 3 Exercise 1 Group Activity PDFRuiz, CherryjaneNo ratings yet

- Chapter 1 MasDocument18 pagesChapter 1 MasRuiz, CherryjaneNo ratings yet

- Chapter 4 Sec CodeDocument19 pagesChapter 4 Sec CodeRuiz, CherryjaneNo ratings yet

- Chapter 2Document10 pagesChapter 2Ruiz, CherryjaneNo ratings yet

- Midterm ForumDocument5 pagesMidterm ForumRuiz, CherryjaneNo ratings yet

- Financial Management Chapter 1Document11 pagesFinancial Management Chapter 1Ruiz, CherryjaneNo ratings yet

- Quiz 2Document2 pagesQuiz 2Ruiz, CherryjaneNo ratings yet

- Wells Fargo Scandal Alternative SolutionDocument1 pageWells Fargo Scandal Alternative SolutionRuiz, CherryjaneNo ratings yet

- Solution Part Wells FargoDocument1 pageSolution Part Wells FargoRuiz, CherryjaneNo ratings yet

- Financial Management Cabrera CH 1 - 5Document72 pagesFinancial Management Cabrera CH 1 - 5Ruiz, CherryjaneNo ratings yet

- Acctg 324 Seatwork 1Document1 pageAcctg 324 Seatwork 1Ruiz, CherryjaneNo ratings yet

- Chapter 1: Introduction To Business AnalyticsDocument5 pagesChapter 1: Introduction To Business AnalyticsRuiz, CherryjaneNo ratings yet

- Activity2-Answer Key1Document9 pagesActivity2-Answer Key1Ruiz, CherryjaneNo ratings yet

- c1 - LiabilitiesDocument44 pagesc1 - LiabilitiesRuiz, CherryjaneNo ratings yet

- Part II. Chapter 3 Exemption From Real Property TaxesDocument30 pagesPart II. Chapter 3 Exemption From Real Property TaxesRuiz, CherryjaneNo ratings yet

- IA 2 - NotesDocument3 pagesIA 2 - NotesRuiz, CherryjaneNo ratings yet

- Part II. Chapter 5 Collection of Real Property TaxDocument39 pagesPart II. Chapter 5 Collection of Real Property TaxRuiz, CherryjaneNo ratings yet

- Bonds PayableDocument39 pagesBonds PayableRuiz, CherryjaneNo ratings yet

- Other TopicsDocument42 pagesOther TopicsRuiz, CherryjaneNo ratings yet

- Chapter 5 Bonds PayableDocument3 pagesChapter 5 Bonds PayableRuiz, CherryjaneNo ratings yet

- Part II. Chapter 1 Real Property Taxation in GeneralDocument20 pagesPart II. Chapter 1 Real Property Taxation in GeneralRuiz, CherryjaneNo ratings yet

- Part II. Chapter 2 Imposition of Real Property TaxDocument30 pagesPart II. Chapter 2 Imposition of Real Property TaxRuiz, CherryjaneNo ratings yet

- Contract of Lease 2019-2020 - Abdukahal, Arbi (Tigbongabong, Tungawan, Zamboanga Sibugay)Document3 pagesContract of Lease 2019-2020 - Abdukahal, Arbi (Tigbongabong, Tungawan, Zamboanga Sibugay)Enrryson SebastianNo ratings yet

- Section 1. The System of Registration Under The Spanish Mortgage Law Is DiscontinuedDocument6 pagesSection 1. The System of Registration Under The Spanish Mortgage Law Is DiscontinuedVicente Alberm Cruz-AmNo ratings yet

- Home Mortgage Interest Deduction: Publication 936Document18 pagesHome Mortgage Interest Deduction: Publication 936Zack BurichNo ratings yet

- 5 Look Before You LeapDocument4 pages5 Look Before You LeapUzair MNNo ratings yet

- Land Sale AgreementDocument3 pagesLand Sale Agreementtkvimal100% (1)

- Consideration, Contract LawDocument7 pagesConsideration, Contract LawManasvi SainiNo ratings yet

- SAR Notes Semester TestDocument100 pagesSAR Notes Semester Testry9w4mqjs6No ratings yet

- 7 Rabaja Ranch Development VsDocument4 pages7 Rabaja Ranch Development VsColee StiflerNo ratings yet

- Contract Act 1872 Past-PapersDocument5 pagesContract Act 1872 Past-Papersbasitalee81No ratings yet

- DOAS Flaviano Lim To Aeleene Jill Rosselle C. Ramos-Braga & Allenby Jiro C. Ramos Shell Tower C Unit 1122Document2 pagesDOAS Flaviano Lim To Aeleene Jill Rosselle C. Ramos-Braga & Allenby Jiro C. Ramos Shell Tower C Unit 1122billyjoe.smdcNo ratings yet

- TP 2Document36 pagesTP 2Dolly Singh OberoiNo ratings yet

- Respondent'S Position Paper: Facts of The CaseDocument8 pagesRespondent'S Position Paper: Facts of The CaseRothea SimonNo ratings yet

- Partners RightsDocument16 pagesPartners RightsManali JainNo ratings yet

- 03 DKC Holdings Corp V CADocument2 pages03 DKC Holdings Corp V CADanielle LimNo ratings yet

- Env of Bus 2010 NotesDocument91 pagesEnv of Bus 2010 NotesErnest Kwame Brawua0% (1)

- SuccessionDocument25 pagesSuccessionDennis EvoraNo ratings yet

- Schedule A LeaseDocument3 pagesSchedule A Leasealvinliu725No ratings yet

- Introduction To Property LawDocument6 pagesIntroduction To Property LawGPNo ratings yet

- Multi Tenant NNN LeaseDocument25 pagesMulti Tenant NNN LeaseTheoNo ratings yet

- OHCHR: Discriminatory Laws and Practices and Acts of Violence Against Individuals Based On Their Sexual Orientation and Gender IdentityDocument25 pagesOHCHR: Discriminatory Laws and Practices and Acts of Violence Against Individuals Based On Their Sexual Orientation and Gender IdentityLGBT Asylum NewsNo ratings yet

- Geographical IndicationDocument4 pagesGeographical IndicationMegha RanjanNo ratings yet

- DBP v. GuarinaDocument2 pagesDBP v. GuarinaMichael Vincent BautistaNo ratings yet

- Discussions On Chapter 1 Part 2 Discussions On Chapter 1 Part 2Document5 pagesDiscussions On Chapter 1 Part 2 Discussions On Chapter 1 Part 2Hybe RetweetsNo ratings yet

- Doctrine of MarshallingDocument4 pagesDoctrine of MarshallingchitraNo ratings yet

- Cash For Keys AgreementDocument3 pagesCash For Keys AgreementpolmidasNo ratings yet

- E-Commerce: Business. Technology. SocietyDocument22 pagesE-Commerce: Business. Technology. Societymona911No ratings yet

- Agra MCQDocument4 pagesAgra MCQDiane UyNo ratings yet

- Guaranty and Suretyship: Kuenzle & Streiff vs. Jose Tan Sunco, Et AlDocument3 pagesGuaranty and Suretyship: Kuenzle & Streiff vs. Jose Tan Sunco, Et AlLara DelleNo ratings yet