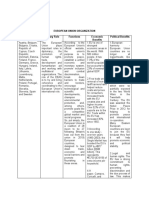

Chapter 2 Demand and Supply

Chapter 2 Demand and Supply

You might also like

- ECON: Practice Quizes 1-5Document37 pagesECON: Practice Quizes 1-5Audrey JacksonNo ratings yet

- Mid-Term Exam (With Answers)Document12 pagesMid-Term Exam (With Answers)Wallace HungNo ratings yet

- Exam#1 (1) SolutionDocument6 pagesExam#1 (1) SolutionaininhusninaNo ratings yet

- Macroeconomics Midterm 2013Document19 pagesMacroeconomics Midterm 2013Daniel Welch100% (1)

- Elasticity Graphs Use The Graph Below To Answer Questions 1 &2Document6 pagesElasticity Graphs Use The Graph Below To Answer Questions 1 &2SaadNo ratings yet

- Lesson Plan Summative-5Document3 pagesLesson Plan Summative-5api-241351663No ratings yet

- Micro Quiz 6Document8 pagesMicro Quiz 6Gia Han TranNo ratings yet

- Econ Q and ADocument93 pagesEcon Q and AGel Mi Amor100% (1)

- Mock Quiz 14A Chap24Document16 pagesMock Quiz 14A Chap24trudis trudisNo ratings yet

- Quiz On MacroDocument4 pagesQuiz On MacroAlexandria EvangelistaNo ratings yet

- Macroeconomics 2001 - Assignments - Jamal HaiderDocument104 pagesMacroeconomics 2001 - Assignments - Jamal Haidermaged famNo ratings yet

- Economics AssignmentDocument6 pagesEconomics Assignmentsolo_sudhanNo ratings yet

- Chap 03Document16 pagesChap 03Syed Hamdan100% (1)

- Demand and SupplyDocument53 pagesDemand and SupplydascXCNo ratings yet

- Eco - Contributed by Dr. Monica Gupta & Prof. Swati AgDocument90 pagesEco - Contributed by Dr. Monica Gupta & Prof. Swati AgManjusree SaamavedamNo ratings yet

- Principles of Economics Question PaperDocument130 pagesPrinciples of Economics Question PaperEmmanuel Kwame Ocloo50% (2)

- 3.1 Firms and Households: The Basic Decision Making Units: Chapter 3 Demand, Supply, and Market EquilibriumDocument51 pages3.1 Firms and Households: The Basic Decision Making Units: Chapter 3 Demand, Supply, and Market EquilibriumNoor Mohammad100% (1)

- Managerial Economics: Quiz 1Document4 pagesManagerial Economics: Quiz 1MarkNo ratings yet

- Demand NumericalsDocument2 pagesDemand Numericalsmahesh kumar0% (1)

- Econ 0-Mudule 3 (2022-2023)Document11 pagesEcon 0-Mudule 3 (2022-2023)Bai NiloNo ratings yet

- Chapter 1: Economics For Managers (Question Bank & Answers)Document13 pagesChapter 1: Economics For Managers (Question Bank & Answers)tk_atiqah100% (1)

- Chapter 08Document30 pagesChapter 08MaxNo ratings yet

- ECON 410 Midterm ExamDocument3 pagesECON 410 Midterm ExamDeVryHelp100% (1)

- Microeconomics QuizDocument5 pagesMicroeconomics QuizFaisal FarooquiNo ratings yet

- Law On Supply and Demand ExamDocument6 pagesLaw On Supply and Demand ExamSharah Del T. TudeNo ratings yet

- Chapter 9 - Market Structures WorksheetDocument2 pagesChapter 9 - Market Structures WorksheetTerry CueNo ratings yet

- Costing Prob FinalsDocument52 pagesCosting Prob FinalsSiddhesh Khade100% (1)

- Midterm Exam 1Document3 pagesMidterm Exam 1dinh_dang_18No ratings yet

- Econ Ch. 5Document22 pagesEcon Ch. 5Demi ToNo ratings yet

- Econ 211 Chapter 3 Test BankDocument55 pagesEcon 211 Chapter 3 Test Bankanthony gebrayelNo ratings yet

- Econ 100.1 Exercise Set No. 1Document2 pagesEcon 100.1 Exercise Set No. 1Charmaine Bernados BrucalNo ratings yet

- QuizDocument36 pagesQuizStormy88No ratings yet

- Topic 2 Demand and Supply (Student)Document4 pagesTopic 2 Demand and Supply (Student)RubbanNo ratings yet

- EC101 Revision Questions - Graphical Analysis - SolutionsDocument10 pagesEC101 Revision Questions - Graphical Analysis - SolutionsZaffia AliNo ratings yet

- Production FunctionDocument17 pagesProduction FunctionharlloveNo ratings yet

- Strategic Management - Midterm Quiz 1Document6 pagesStrategic Management - Midterm Quiz 1Uy SamuelNo ratings yet

- Price Discrimination Under Monopoly: Types, Degrees and Other DetailsDocument18 pagesPrice Discrimination Under Monopoly: Types, Degrees and Other DetailsSanchit BabbarNo ratings yet

- Microeconomics Lecture 1Document12 pagesMicroeconomics Lecture 1Xero CNo ratings yet

- Measuring A Nation'S Income: Questions For ReviewDocument4 pagesMeasuring A Nation'S Income: Questions For ReviewNoman MustafaNo ratings yet

- Elasticity of Demand WorksheetDocument3 pagesElasticity of Demand WorksheetVijay KumarNo ratings yet

- EC1301 Midterm Test: You Have CompletedDocument21 pagesEC1301 Midterm Test: You Have CompletedBrandon boo100% (1)

- 2 - Inventory ControlDocument60 pages2 - Inventory ControlNada BadawiNo ratings yet

- Microeconomics Quiz 1 Study GuideDocument8 pagesMicroeconomics Quiz 1 Study GuideeinsteinspyNo ratings yet

- Managerial Economics Ch3Document67 pagesManagerial Economics Ch3Ashe BalchaNo ratings yet

- Managerial Economics (Quiz) Subject Code: 12MCEC01 MBA-Trimester - IDocument4 pagesManagerial Economics (Quiz) Subject Code: 12MCEC01 MBA-Trimester - IShivani PandeyNo ratings yet

- Microeconomics Test 1Document14 pagesMicroeconomics Test 1Hunter Brown100% (1)

- 10e 12 Chap Student WorkbookDocument23 pages10e 12 Chap Student WorkbookkartikartikaaNo ratings yet

- Chapter 5 Consumer BehaviourDocument5 pagesChapter 5 Consumer BehaviourZyroneGlennJeraoSayanaNo ratings yet

- Economics - Markets With Asymmetric InformationDocument21 pagesEconomics - Markets With Asymmetric Informationragneshr100% (1)

- EconomicsDocument19 pagesEconomicsnekkmatt100% (1)

- The University of Manila Final Exam in MicroeconomicsDocument3 pagesThe University of Manila Final Exam in MicroeconomicsLeon Dela Torre100% (2)

- Consumer Surplus Indifference CurvesDocument7 pagesConsumer Surplus Indifference CurvesDivya AroraNo ratings yet

- MA Applied Economics Syllabus.Document65 pagesMA Applied Economics Syllabus.Vishnu VenugopalNo ratings yet

- Financial Management Week 1 HomeworkDocument6 pagesFinancial Management Week 1 HomeworkF4ARNo ratings yet

- Inferior Goods-A Product That's Demand Is Inversely Related To Consumer Income. in Other WordsDocument5 pagesInferior Goods-A Product That's Demand Is Inversely Related To Consumer Income. in Other WordsJasmine AlucimanNo ratings yet

- Managerial Economics: Ii: Demand and SupplyDocument74 pagesManagerial Economics: Ii: Demand and Supplykewani negashNo ratings yet

- Law of Supply and DemandDocument49 pagesLaw of Supply and DemandArvi Kyle Grospe PunzalanNo ratings yet

- Seminar 2 - Demand and Supply - ADocument12 pagesSeminar 2 - Demand and Supply - Avivekrabadia0077No ratings yet

- Building A Flexible Supply Chain in Low Volume High Mix IndustrialsDocument9 pagesBuilding A Flexible Supply Chain in Low Volume High Mix IndustrialsThanhquy NguyenNo ratings yet

- Globalization Visual Sources CH 23Document6 pagesGlobalization Visual Sources CH 23api-230184052No ratings yet

- PDF San Beda College of Law MEMORY AID I PDFDocument106 pagesPDF San Beda College of Law MEMORY AID I PDFGladys ManaliliNo ratings yet

- Citizenscharter2020 PDFDocument650 pagesCitizenscharter2020 PDFLeulaDianneCantosNo ratings yet

- Adb Brief 127 Industrial Park Rating System IndiaDocument8 pagesAdb Brief 127 Industrial Park Rating System IndiaSiddhartha ShekharNo ratings yet

- Organizational Management: Submitted ToDocument5 pagesOrganizational Management: Submitted ToSehar WaleedNo ratings yet

- Abm 1-W6.M2.T1.L2Document5 pagesAbm 1-W6.M2.T1.L2mbiloloNo ratings yet

- GST Issues For Works Contract CA Yashwant Kasar - 31st July 2021Document73 pagesGST Issues For Works Contract CA Yashwant Kasar - 31st July 2021fintech ConsultancyNo ratings yet

- Swot Analysis Krispy KremeDocument30 pagesSwot Analysis Krispy KremeAnonymous nj3pIshNo ratings yet

- MKC Case Study FinalDocument39 pagesMKC Case Study FinalxyzNo ratings yet

- Interest On Loan 80eDocument2 pagesInterest On Loan 80ePaymaster ServicesNo ratings yet

- BBA Syllabus Sem-6 (Finance)Document10 pagesBBA Syllabus Sem-6 (Finance)Mukesh GiriNo ratings yet

- AmazonDocument3 pagesAmazonDominicNo ratings yet

- InvoiceDocument1 pageInvoiceshiv kumarNo ratings yet

- Impacts That Matter - Product Sustainability Overview - 54959 - PDFDocument4 pagesImpacts That Matter - Product Sustainability Overview - 54959 - PDFOptima StoreNo ratings yet

- Slavery in The Roman Empire: Alex Grigoriou 2ADocument5 pagesSlavery in The Roman Empire: Alex Grigoriou 2AAlex GrigoriouNo ratings yet

- Sourcing Strategies of Fahion Retailers PDFDocument10 pagesSourcing Strategies of Fahion Retailers PDFVinay VashisthNo ratings yet

- FL MasDocument7 pagesFL Masedrick LouiseNo ratings yet

- Marketing NotesDocument4 pagesMarketing NotesChristineNo ratings yet

- 1.4 StakeholdersDocument20 pages1.4 StakeholdersRODRIGO GUTIERREZ HUAMANINo ratings yet

- Princess Julienne Y. Yu 2GphDocument4 pagesPrincess Julienne Y. Yu 2GphPRINCESS JULIENNE YUNo ratings yet

- Test Bank For Essentials of Marketing Management 1st Edition MarshallDocument92 pagesTest Bank For Essentials of Marketing Management 1st Edition MarshallXolani MpilaNo ratings yet

- Course Detail 7th Sem Mkm. BBADocument8 pagesCourse Detail 7th Sem Mkm. BBAHari AdhikariNo ratings yet

- Dell Computer: Refining and Extending The Business Model With ITDocument18 pagesDell Computer: Refining and Extending The Business Model With ITTathagataNo ratings yet

- 1st Module AssessmentfmDocument6 pages1st Module AssessmentfmMansi GuptaNo ratings yet

- RDocument671 pagesRlinhtruong.31221024012No ratings yet

- Annual Work Accident - Illness Exposure Data ReportDocument1 pageAnnual Work Accident - Illness Exposure Data ReportJon Allan Buenaobra100% (1)

- Pcpar Backflush Costing and JitDocument2 pagesPcpar Backflush Costing and Jitdoora keysNo ratings yet

- 03 - Mental Accounting - HANDOUTDocument8 pages03 - Mental Accounting - HANDOUTtkkt1015No ratings yet

- Sample Productivity ProblemsDocument5 pagesSample Productivity ProblemsCassia MontiNo ratings yet

Download as docx, pdf, or txt

You might also like

- ECON: Practice Quizes 1-5Document37 pagesECON: Practice Quizes 1-5Audrey JacksonNo ratings yet

- Mid-Term Exam (With Answers)Document12 pagesMid-Term Exam (With Answers)Wallace HungNo ratings yet

- Exam#1 (1) SolutionDocument6 pagesExam#1 (1) SolutionaininhusninaNo ratings yet

- Macroeconomics Midterm 2013Document19 pagesMacroeconomics Midterm 2013Daniel Welch100% (1)

- Elasticity Graphs Use The Graph Below To Answer Questions 1 &2Document6 pagesElasticity Graphs Use The Graph Below To Answer Questions 1 &2SaadNo ratings yet

- Lesson Plan Summative-5Document3 pagesLesson Plan Summative-5api-241351663No ratings yet

- Micro Quiz 6Document8 pagesMicro Quiz 6Gia Han TranNo ratings yet

- Econ Q and ADocument93 pagesEcon Q and AGel Mi Amor100% (1)

- Mock Quiz 14A Chap24Document16 pagesMock Quiz 14A Chap24trudis trudisNo ratings yet

- Quiz On MacroDocument4 pagesQuiz On MacroAlexandria EvangelistaNo ratings yet

- Macroeconomics 2001 - Assignments - Jamal HaiderDocument104 pagesMacroeconomics 2001 - Assignments - Jamal Haidermaged famNo ratings yet

- Economics AssignmentDocument6 pagesEconomics Assignmentsolo_sudhanNo ratings yet

- Chap 03Document16 pagesChap 03Syed Hamdan100% (1)

- Demand and SupplyDocument53 pagesDemand and SupplydascXCNo ratings yet

- Eco - Contributed by Dr. Monica Gupta & Prof. Swati AgDocument90 pagesEco - Contributed by Dr. Monica Gupta & Prof. Swati AgManjusree SaamavedamNo ratings yet

- Principles of Economics Question PaperDocument130 pagesPrinciples of Economics Question PaperEmmanuel Kwame Ocloo50% (2)

- 3.1 Firms and Households: The Basic Decision Making Units: Chapter 3 Demand, Supply, and Market EquilibriumDocument51 pages3.1 Firms and Households: The Basic Decision Making Units: Chapter 3 Demand, Supply, and Market EquilibriumNoor Mohammad100% (1)

- Managerial Economics: Quiz 1Document4 pagesManagerial Economics: Quiz 1MarkNo ratings yet

- Demand NumericalsDocument2 pagesDemand Numericalsmahesh kumar0% (1)

- Econ 0-Mudule 3 (2022-2023)Document11 pagesEcon 0-Mudule 3 (2022-2023)Bai NiloNo ratings yet

- Chapter 1: Economics For Managers (Question Bank & Answers)Document13 pagesChapter 1: Economics For Managers (Question Bank & Answers)tk_atiqah100% (1)

- Chapter 08Document30 pagesChapter 08MaxNo ratings yet

- ECON 410 Midterm ExamDocument3 pagesECON 410 Midterm ExamDeVryHelp100% (1)

- Microeconomics QuizDocument5 pagesMicroeconomics QuizFaisal FarooquiNo ratings yet

- Law On Supply and Demand ExamDocument6 pagesLaw On Supply and Demand ExamSharah Del T. TudeNo ratings yet

- Chapter 9 - Market Structures WorksheetDocument2 pagesChapter 9 - Market Structures WorksheetTerry CueNo ratings yet

- Costing Prob FinalsDocument52 pagesCosting Prob FinalsSiddhesh Khade100% (1)

- Midterm Exam 1Document3 pagesMidterm Exam 1dinh_dang_18No ratings yet

- Econ Ch. 5Document22 pagesEcon Ch. 5Demi ToNo ratings yet

- Econ 211 Chapter 3 Test BankDocument55 pagesEcon 211 Chapter 3 Test Bankanthony gebrayelNo ratings yet

- Econ 100.1 Exercise Set No. 1Document2 pagesEcon 100.1 Exercise Set No. 1Charmaine Bernados BrucalNo ratings yet

- QuizDocument36 pagesQuizStormy88No ratings yet

- Topic 2 Demand and Supply (Student)Document4 pagesTopic 2 Demand and Supply (Student)RubbanNo ratings yet

- EC101 Revision Questions - Graphical Analysis - SolutionsDocument10 pagesEC101 Revision Questions - Graphical Analysis - SolutionsZaffia AliNo ratings yet

- Production FunctionDocument17 pagesProduction FunctionharlloveNo ratings yet

- Strategic Management - Midterm Quiz 1Document6 pagesStrategic Management - Midterm Quiz 1Uy SamuelNo ratings yet

- Price Discrimination Under Monopoly: Types, Degrees and Other DetailsDocument18 pagesPrice Discrimination Under Monopoly: Types, Degrees and Other DetailsSanchit BabbarNo ratings yet

- Microeconomics Lecture 1Document12 pagesMicroeconomics Lecture 1Xero CNo ratings yet

- Measuring A Nation'S Income: Questions For ReviewDocument4 pagesMeasuring A Nation'S Income: Questions For ReviewNoman MustafaNo ratings yet

- Elasticity of Demand WorksheetDocument3 pagesElasticity of Demand WorksheetVijay KumarNo ratings yet

- EC1301 Midterm Test: You Have CompletedDocument21 pagesEC1301 Midterm Test: You Have CompletedBrandon boo100% (1)

- 2 - Inventory ControlDocument60 pages2 - Inventory ControlNada BadawiNo ratings yet

- Microeconomics Quiz 1 Study GuideDocument8 pagesMicroeconomics Quiz 1 Study GuideeinsteinspyNo ratings yet

- Managerial Economics Ch3Document67 pagesManagerial Economics Ch3Ashe BalchaNo ratings yet

- Managerial Economics (Quiz) Subject Code: 12MCEC01 MBA-Trimester - IDocument4 pagesManagerial Economics (Quiz) Subject Code: 12MCEC01 MBA-Trimester - IShivani PandeyNo ratings yet

- Microeconomics Test 1Document14 pagesMicroeconomics Test 1Hunter Brown100% (1)

- 10e 12 Chap Student WorkbookDocument23 pages10e 12 Chap Student WorkbookkartikartikaaNo ratings yet

- Chapter 5 Consumer BehaviourDocument5 pagesChapter 5 Consumer BehaviourZyroneGlennJeraoSayanaNo ratings yet

- Economics - Markets With Asymmetric InformationDocument21 pagesEconomics - Markets With Asymmetric Informationragneshr100% (1)

- EconomicsDocument19 pagesEconomicsnekkmatt100% (1)

- The University of Manila Final Exam in MicroeconomicsDocument3 pagesThe University of Manila Final Exam in MicroeconomicsLeon Dela Torre100% (2)

- Consumer Surplus Indifference CurvesDocument7 pagesConsumer Surplus Indifference CurvesDivya AroraNo ratings yet

- MA Applied Economics Syllabus.Document65 pagesMA Applied Economics Syllabus.Vishnu VenugopalNo ratings yet

- Financial Management Week 1 HomeworkDocument6 pagesFinancial Management Week 1 HomeworkF4ARNo ratings yet

- Inferior Goods-A Product That's Demand Is Inversely Related To Consumer Income. in Other WordsDocument5 pagesInferior Goods-A Product That's Demand Is Inversely Related To Consumer Income. in Other WordsJasmine AlucimanNo ratings yet

- Managerial Economics: Ii: Demand and SupplyDocument74 pagesManagerial Economics: Ii: Demand and Supplykewani negashNo ratings yet

- Law of Supply and DemandDocument49 pagesLaw of Supply and DemandArvi Kyle Grospe PunzalanNo ratings yet

- Seminar 2 - Demand and Supply - ADocument12 pagesSeminar 2 - Demand and Supply - Avivekrabadia0077No ratings yet

- Building A Flexible Supply Chain in Low Volume High Mix IndustrialsDocument9 pagesBuilding A Flexible Supply Chain in Low Volume High Mix IndustrialsThanhquy NguyenNo ratings yet

- Globalization Visual Sources CH 23Document6 pagesGlobalization Visual Sources CH 23api-230184052No ratings yet

- PDF San Beda College of Law MEMORY AID I PDFDocument106 pagesPDF San Beda College of Law MEMORY AID I PDFGladys ManaliliNo ratings yet

- Citizenscharter2020 PDFDocument650 pagesCitizenscharter2020 PDFLeulaDianneCantosNo ratings yet

- Adb Brief 127 Industrial Park Rating System IndiaDocument8 pagesAdb Brief 127 Industrial Park Rating System IndiaSiddhartha ShekharNo ratings yet

- Organizational Management: Submitted ToDocument5 pagesOrganizational Management: Submitted ToSehar WaleedNo ratings yet

- Abm 1-W6.M2.T1.L2Document5 pagesAbm 1-W6.M2.T1.L2mbiloloNo ratings yet

- GST Issues For Works Contract CA Yashwant Kasar - 31st July 2021Document73 pagesGST Issues For Works Contract CA Yashwant Kasar - 31st July 2021fintech ConsultancyNo ratings yet

- Swot Analysis Krispy KremeDocument30 pagesSwot Analysis Krispy KremeAnonymous nj3pIshNo ratings yet

- MKC Case Study FinalDocument39 pagesMKC Case Study FinalxyzNo ratings yet

- Interest On Loan 80eDocument2 pagesInterest On Loan 80ePaymaster ServicesNo ratings yet

- BBA Syllabus Sem-6 (Finance)Document10 pagesBBA Syllabus Sem-6 (Finance)Mukesh GiriNo ratings yet

- AmazonDocument3 pagesAmazonDominicNo ratings yet

- InvoiceDocument1 pageInvoiceshiv kumarNo ratings yet

- Impacts That Matter - Product Sustainability Overview - 54959 - PDFDocument4 pagesImpacts That Matter - Product Sustainability Overview - 54959 - PDFOptima StoreNo ratings yet

- Slavery in The Roman Empire: Alex Grigoriou 2ADocument5 pagesSlavery in The Roman Empire: Alex Grigoriou 2AAlex GrigoriouNo ratings yet

- Sourcing Strategies of Fahion Retailers PDFDocument10 pagesSourcing Strategies of Fahion Retailers PDFVinay VashisthNo ratings yet

- FL MasDocument7 pagesFL Masedrick LouiseNo ratings yet

- Marketing NotesDocument4 pagesMarketing NotesChristineNo ratings yet

- 1.4 StakeholdersDocument20 pages1.4 StakeholdersRODRIGO GUTIERREZ HUAMANINo ratings yet

- Princess Julienne Y. Yu 2GphDocument4 pagesPrincess Julienne Y. Yu 2GphPRINCESS JULIENNE YUNo ratings yet

- Test Bank For Essentials of Marketing Management 1st Edition MarshallDocument92 pagesTest Bank For Essentials of Marketing Management 1st Edition MarshallXolani MpilaNo ratings yet

- Course Detail 7th Sem Mkm. BBADocument8 pagesCourse Detail 7th Sem Mkm. BBAHari AdhikariNo ratings yet

- Dell Computer: Refining and Extending The Business Model With ITDocument18 pagesDell Computer: Refining and Extending The Business Model With ITTathagataNo ratings yet

- 1st Module AssessmentfmDocument6 pages1st Module AssessmentfmMansi GuptaNo ratings yet

- RDocument671 pagesRlinhtruong.31221024012No ratings yet

- Annual Work Accident - Illness Exposure Data ReportDocument1 pageAnnual Work Accident - Illness Exposure Data ReportJon Allan Buenaobra100% (1)

- Pcpar Backflush Costing and JitDocument2 pagesPcpar Backflush Costing and Jitdoora keysNo ratings yet

- 03 - Mental Accounting - HANDOUTDocument8 pages03 - Mental Accounting - HANDOUTtkkt1015No ratings yet

- Sample Productivity ProblemsDocument5 pagesSample Productivity ProblemsCassia MontiNo ratings yet