PWC India Report

PWC India Report

You might also like

- AML KYC Mock Test - Practice TestsDocument16 pagesAML KYC Mock Test - Practice Testsdev100% (1)

- APES 310 Audit ProgramDocument13 pagesAPES 310 Audit ProgramShamir Gupta100% (1)

- 104 2022 218 BdoDocument29 pages104 2022 218 BdoJason BramwellNo ratings yet

- Revenue and Receivables Audit ProgramsDocument26 pagesRevenue and Receivables Audit ProgramsRhea SimoneNo ratings yet

- Power Query - Solution Book PDFDocument113 pagesPower Query - Solution Book PDFGermán Darío León Cardona100% (3)

- Risk of Material Misstatement Worksheet - Overview General InstructionsDocument35 pagesRisk of Material Misstatement Worksheet - Overview General InstructionswellawalalasithNo ratings yet

- Bata Annual Report 2020 MergedDocument248 pagesBata Annual Report 2020 Mergedshree nathNo ratings yet

- Imvula Health Logistics Brochure SingleDocument8 pagesImvula Health Logistics Brochure SingleAndile NtuliNo ratings yet

- Module 1 - What Is RiskDocument19 pagesModule 1 - What Is RiskKim Anh NguyenNo ratings yet

- SOX Deficiencies TraiingDocument49 pagesSOX Deficiencies TraiingSridhair IyengarNo ratings yet

- Office of The Superintendent of Financial Institutions Internal Audit Report On Finance - RevenueDocument19 pagesOffice of The Superintendent of Financial Institutions Internal Audit Report On Finance - RevenueCharu Panchal Bedi100% (1)

- Guidance On Journal Entries - KAM 3.2.20 (Ver01.20)Document9 pagesGuidance On Journal Entries - KAM 3.2.20 (Ver01.20)Aries BautistaNo ratings yet

- Appendix IV - RoMM Control Objectives and Control ActivitiesDocument133 pagesAppendix IV - RoMM Control Objectives and Control ActivitiesNitin goyalNo ratings yet

- AT 06-06 Transaction Cycles Part 1Document9 pagesAT 06-06 Transaction Cycles Part 1Eeuh100% (1)

- PDF PPR 15 FiccaDocument44 pagesPDF PPR 15 FiccaPankaj GoyalNo ratings yet

- SCCPSS Management Action Plan - School Nutrition AuditDocument1 pageSCCPSS Management Action Plan - School Nutrition Auditsavannahnow.comNo ratings yet

- ICSI Internal Controls and Risk Management System 07082022Document56 pagesICSI Internal Controls and Risk Management System 07082022monika vermaNo ratings yet

- Internal Financial Controls-IfCORDocument47 pagesInternal Financial Controls-IfCORGovind PaliwalNo ratings yet

- Risk Analysis MemoDocument7 pagesRisk Analysis MemoAnonymous in4fhbdwkNo ratings yet

- Form 18 Sdi 2 - Loans - Risk of Material Misstatement (Romm) WorksheetDocument27 pagesForm 18 Sdi 2 - Loans - Risk of Material Misstatement (Romm) WorksheetwellawalalasithNo ratings yet

- Commission On Higher Education - Regional Office - Student Services Monitoring InstrumentDocument64 pagesCommission On Higher Education - Regional Office - Student Services Monitoring InstrumentdreaNo ratings yet

- Integration Workplan For Core FunctionsDocument51 pagesIntegration Workplan For Core Functionsthe_playerNo ratings yet

- Risk of Material Misstatement Worksheet - Overview General InstructionsDocument26 pagesRisk of Material Misstatement Worksheet - Overview General InstructionswellawalalasithNo ratings yet

- BSSOXPurchasing&Payables Control MatrixDocument2 pagesBSSOXPurchasing&Payables Control MatrixDivine GraceNo ratings yet

- Form 18 Sdi 4 - Recourse Liabilities - Risk of Material Misstatement (Romm) WorksheetDocument17 pagesForm 18 Sdi 4 - Recourse Liabilities - Risk of Material Misstatement (Romm) WorksheetwellawalalasithNo ratings yet

- Fraud Awareness Training: Detection and PreventionDocument20 pagesFraud Awareness Training: Detection and PreventionDataMis EliosHealthCareNo ratings yet

- NYC Comptroller Audit of DOT Bridge WorkDocument38 pagesNYC Comptroller Audit of DOT Bridge WorkGersh KuntzmanNo ratings yet

- Scope of Concurrent AuditDocument17 pagesScope of Concurrent AuditAnandNo ratings yet

- ISA 240 - Auditor's Responsibilities Relating To Fraud: Akash Mukesh Kumar, ACADocument20 pagesISA 240 - Auditor's Responsibilities Relating To Fraud: Akash Mukesh Kumar, ACAJ. EDUNo ratings yet

- Inventory Inventory IDR Control NoDocument23 pagesInventory Inventory IDR Control NoCA Rahul GuptaNo ratings yet

- INTERNAL CONTROLS - Section 3 Example of Documentation: FlowchartDocument8 pagesINTERNAL CONTROLS - Section 3 Example of Documentation: Flowchartحسين عبدالرحمنNo ratings yet

- Treasury RCM 2022-2023Document1 pageTreasury RCM 2022-2023Aman ParchaniNo ratings yet

- SUM - Summary of Uncorrected MisstatementsDocument1 pageSUM - Summary of Uncorrected MisstatementsCharielle Esthelin BacuganNo ratings yet

- Ombudsman Victoria Complaint Handling Good Practice Guide1Document58 pagesOmbudsman Victoria Complaint Handling Good Practice Guide1Rhea SimoneNo ratings yet

- Form 1840sdi-2 - Substantive Procedures Guide - Banking and Finance - LoansDocument17 pagesForm 1840sdi-2 - Substantive Procedures Guide - Banking and Finance - LoanswellawalalasithNo ratings yet

- Risk Assesment by Program AreaDocument7 pagesRisk Assesment by Program AreaJoanne PerandoNo ratings yet

- Consideration of Management Override of ControlsDocument2 pagesConsideration of Management Override of ControlsCaterina De LucaNo ratings yet

- Combatting Financial Crime in The UAEDocument11 pagesCombatting Financial Crime in The UAEBellaNo ratings yet

- SWOT Analysis: Organizational Context and Interested Parties Need & ExpectationDocument43 pagesSWOT Analysis: Organizational Context and Interested Parties Need & Expectationamril alrizaNo ratings yet

- Sunera Best Practices For Remediating SoDsDocument7 pagesSunera Best Practices For Remediating SoDssura anil reddyNo ratings yet

- Risk Assessment BackfilligDocument5 pagesRisk Assessment Backfilligmolobe mkhondoNo ratings yet

- Debt Interest Expense Substantive AnalyticalDocument2 pagesDebt Interest Expense Substantive AnalyticalErik RodriguesNo ratings yet

- Risk Management ManualDocument78 pagesRisk Management ManualSaudi MindNo ratings yet

- 2014 PricewaterhouseCoopers LLPDocument56 pages2014 PricewaterhouseCoopers LLPJahidur Rahman FcaNo ratings yet

- Understanding Transaction Monitoring V 1.0Document51 pagesUnderstanding Transaction Monitoring V 1.0Michael O'hare100% (1)

- Related Parties PT 2Document8 pagesRelated Parties PT 2Caterina De LucaNo ratings yet

- 104 2022 221 GTDocument25 pages104 2022 221 GTJason BramwellNo ratings yet

- Credit Monitoring and Early Warning SignalsDocument10 pagesCredit Monitoring and Early Warning Signalssagar7No ratings yet

- Internal Audit Manual Example 2024Document24 pagesInternal Audit Manual Example 2024DEEPAKNo ratings yet

- Soal Internal Control FinalDocument51 pagesSoal Internal Control FinalneysascribdNo ratings yet

- TheProcure To PayCyclebyChristineDoxeyDocument6 pagesTheProcure To PayCyclebyChristineDoxeyManna MahadiNo ratings yet

- Auditing in An ERP Environment Chapter 3: Automated Application ControlsDocument39 pagesAuditing in An ERP Environment Chapter 3: Automated Application Controlssrinathaladi shilpa100% (1)

- KVSS 2022 Financial StatementDocument36 pagesKVSS 2022 Financial StatementKristofer PlonaNo ratings yet

- 2020 Inspection Grant Thornton LLP: (Headquartered in Chicago, Illinois)Document24 pages2020 Inspection Grant Thornton LLP: (Headquartered in Chicago, Illinois)Jason BramwellNo ratings yet

- Fintech and Covid 19 Web (2022)Document261 pagesFintech and Covid 19 Web (2022)max tesNo ratings yet

- Risks and Controls For AML Monitoring SystemsDocument25 pagesRisks and Controls For AML Monitoring SystemsSanjay SainiNo ratings yet

- Forensic Accounting Vs Investigative Auditing On Fraud Detection-MatDocument40 pagesForensic Accounting Vs Investigative Auditing On Fraud Detection-MatUpdater proNo ratings yet

- Module 6 - Understanding The Entity and Its EnvironmentDocument11 pagesModule 6 - Understanding The Entity and Its EnvironmentMa Jessa Kathryl Alar IINo ratings yet

- Related Parties ISA 550 Audit CAF 9 (ARM+AMK)Document11 pagesRelated Parties ISA 550 Audit CAF 9 (ARM+AMK)Abdul WahabNo ratings yet

- Independence Confirmation Affidavit For Managers 2019Document12 pagesIndependence Confirmation Affidavit For Managers 2019Kushagra AgarwalNo ratings yet

- 2020 Internal Audit Report Stateof Good RepairDocument8 pages2020 Internal Audit Report Stateof Good RepairRamzi MHIRINo ratings yet

- Wiley Not-for-Profit GAAP 2017: Interpretation and Application of Generally Accepted Accounting PrinciplesFrom EverandWiley Not-for-Profit GAAP 2017: Interpretation and Application of Generally Accepted Accounting PrinciplesNo ratings yet

- List of Older CircularsDocument3 pagesList of Older CircularsBhaskar GarimellaNo ratings yet

- Reference Layout of KYC Circular - RBIDocument6 pagesReference Layout of KYC Circular - RBIBhaskar GarimellaNo ratings yet

- Islamic BankingDocument26 pagesIslamic BankingBhaskar GarimellaNo ratings yet

- RBI - Determination of A Beneficiary OwnerDocument2 pagesRBI - Determination of A Beneficiary OwnerBhaskar GarimellaNo ratings yet

- Digital-Alternate ChannelDocument146 pagesDigital-Alternate ChannelBhaskar GarimellaNo ratings yet

- RBI - Definition of 'Infrastructure Lending'Document9 pagesRBI - Definition of 'Infrastructure Lending'Bhaskar GarimellaNo ratings yet

- Revision in Pay and Allowance 01.04.2021Document26 pagesRevision in Pay and Allowance 01.04.2021Bhaskar GarimellaNo ratings yet

- Research Methodology To InputDocument13 pagesResearch Methodology To InputBhaskar GarimellaNo ratings yet

- List of Firms SampledDocument90 pagesList of Firms SampledBhaskar GarimellaNo ratings yet

- IEEE TemplateDocument8 pagesIEEE TemplateBhaskar GarimellaNo ratings yet

- Industry-Wise Benchmarks Key Fin RatiosDocument18 pagesIndustry-Wise Benchmarks Key Fin RatiosBhaskar GarimellaNo ratings yet

- Schedules of Balance SheetDocument3 pagesSchedules of Balance SheetBhaskar GarimellaNo ratings yet

- Credit Scoring ChecklistDocument2 pagesCredit Scoring ChecklistBhaskar GarimellaNo ratings yet

- Micro Research - Advt-19-20Document1 pageMicro Research - Advt-19-20Bhaskar GarimellaNo ratings yet

- Risk-Spectrum - Vehicles (CRISIL Report)Document7 pagesRisk-Spectrum - Vehicles (CRISIL Report)Bhaskar GarimellaNo ratings yet

- JSS Brochure 2022Document30 pagesJSS Brochure 2022Bhaskar GarimellaNo ratings yet

- Credit Processing For CVDocument5 pagesCredit Processing For CVBhaskar GarimellaNo ratings yet

- Case Reference - SK FinanceDocument2 pagesCase Reference - SK FinanceBhaskar GarimellaNo ratings yet

- RBI Circular On VigilanceDocument8 pagesRBI Circular On VigilanceBhaskar Garimella100% (1)

- I Wayan Artha Wijaya: RingkasanDocument2 pagesI Wayan Artha Wijaya: RingkasanBerlian JosephNo ratings yet

- Procurement PlanDocument3 pagesProcurement Planmmalnar1No ratings yet

- 'XSK-1100894-south Bay - BDocument5 pages'XSK-1100894-south Bay - BngNo ratings yet

- 2010 - Rosly - Shariah Parameter ReconsideredDocument19 pages2010 - Rosly - Shariah Parameter ReconsideredyuwonliloNo ratings yet

- Learn To Profit From Intraday Trading in NiftyDocument10 pagesLearn To Profit From Intraday Trading in Niftyuday_kendhe90050% (1)

- A Project Report Prakash ThapaDocument67 pagesA Project Report Prakash ThapaMitesh Prajapati 7765No ratings yet

- Taxation Enhancement ExercisesDocument13 pagesTaxation Enhancement ExercisesRachel LeachonNo ratings yet

- Black BookDocument55 pagesBlack Bookprabhas MakwanaNo ratings yet

- Info SysDocument58 pagesInfo SysBirddoxyNo ratings yet

- Presentation On DerevativeDocument19 pagesPresentation On DerevativeAnkitaParabNo ratings yet

- TQM Brief 1Document39 pagesTQM Brief 1selvaganapathy1992100% (1)

- Iqmin A Jktinv0087205 Jktyulia 20230408071006Document1 pageIqmin A Jktinv0087205 Jktyulia 20230408071006Rahayu UmarNo ratings yet

- AF301 Unit 8 System Oriented TheoriesDocument28 pagesAF301 Unit 8 System Oriented TheoriesNarayan DiviyaNo ratings yet

- Problems For Cash and Cash EquivalentsDocument1 pageProblems For Cash and Cash EquivalentsTine Vasiana DuermeNo ratings yet

- Cbroa News December 2020 2 PDFDocument37 pagesCbroa News December 2020 2 PDFVijay IyerNo ratings yet

- Bond and Bond Features and Its Example AssignmentDocument4 pagesBond and Bond Features and Its Example AssignmentWaqaarNo ratings yet

- Company Profile PT Geo Explo OptimaDocument6 pagesCompany Profile PT Geo Explo OptimaRinaldi SatriaNo ratings yet

- Jose Ramona InvoiceDocument1 pageJose Ramona InvoiceDavid MendozaNo ratings yet

- Seminar 6.1Document2 pagesSeminar 6.1Đạt PhạmNo ratings yet

- TKRS TOT Calon Surveior Akreditasi RS Arjaty 29 Desember 2021Document47 pagesTKRS TOT Calon Surveior Akreditasi RS Arjaty 29 Desember 2021Yuliana SariNo ratings yet

- Elasticity and Tax IncidenceDocument11 pagesElasticity and Tax IncidenceKiara RamdhawNo ratings yet

- Activity 3 - Doing in The EnvironmentDocument1 pageActivity 3 - Doing in The EnvironmentKin Anthony NocumNo ratings yet

- 12.2% CAGR: Fuel Containment Processing Equipment Service Canada United StatesDocument1 page12.2% CAGR: Fuel Containment Processing Equipment Service Canada United StatesRandy LaheyNo ratings yet

- Financial Management: Financial Management Refers To That Part of TheDocument19 pagesFinancial Management: Financial Management Refers To That Part of TheMayuraa ShekatkarNo ratings yet

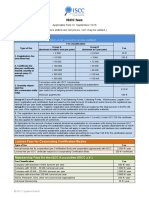

- ISCC FeesDocument1 pageISCC FeesAyoubELBakiriNo ratings yet

- PTMADocument7 pagesPTMAAman Kumar SharanNo ratings yet

- T26 026 902 PDFDocument7 pagesT26 026 902 PDFBenNo ratings yet

- Jaymar M Jabonillo ResumeDocument3 pagesJaymar M Jabonillo ResumeNanjiro EchizenNo ratings yet

Download as pdf or txt

You might also like

- AML KYC Mock Test - Practice TestsDocument16 pagesAML KYC Mock Test - Practice Testsdev100% (1)

- APES 310 Audit ProgramDocument13 pagesAPES 310 Audit ProgramShamir Gupta100% (1)

- 104 2022 218 BdoDocument29 pages104 2022 218 BdoJason BramwellNo ratings yet

- Revenue and Receivables Audit ProgramsDocument26 pagesRevenue and Receivables Audit ProgramsRhea SimoneNo ratings yet

- Power Query - Solution Book PDFDocument113 pagesPower Query - Solution Book PDFGermán Darío León Cardona100% (3)

- Risk of Material Misstatement Worksheet - Overview General InstructionsDocument35 pagesRisk of Material Misstatement Worksheet - Overview General InstructionswellawalalasithNo ratings yet

- Bata Annual Report 2020 MergedDocument248 pagesBata Annual Report 2020 Mergedshree nathNo ratings yet

- Imvula Health Logistics Brochure SingleDocument8 pagesImvula Health Logistics Brochure SingleAndile NtuliNo ratings yet

- Module 1 - What Is RiskDocument19 pagesModule 1 - What Is RiskKim Anh NguyenNo ratings yet

- SOX Deficiencies TraiingDocument49 pagesSOX Deficiencies TraiingSridhair IyengarNo ratings yet

- Office of The Superintendent of Financial Institutions Internal Audit Report On Finance - RevenueDocument19 pagesOffice of The Superintendent of Financial Institutions Internal Audit Report On Finance - RevenueCharu Panchal Bedi100% (1)

- Guidance On Journal Entries - KAM 3.2.20 (Ver01.20)Document9 pagesGuidance On Journal Entries - KAM 3.2.20 (Ver01.20)Aries BautistaNo ratings yet

- Appendix IV - RoMM Control Objectives and Control ActivitiesDocument133 pagesAppendix IV - RoMM Control Objectives and Control ActivitiesNitin goyalNo ratings yet

- AT 06-06 Transaction Cycles Part 1Document9 pagesAT 06-06 Transaction Cycles Part 1Eeuh100% (1)

- PDF PPR 15 FiccaDocument44 pagesPDF PPR 15 FiccaPankaj GoyalNo ratings yet

- SCCPSS Management Action Plan - School Nutrition AuditDocument1 pageSCCPSS Management Action Plan - School Nutrition Auditsavannahnow.comNo ratings yet

- ICSI Internal Controls and Risk Management System 07082022Document56 pagesICSI Internal Controls and Risk Management System 07082022monika vermaNo ratings yet

- Internal Financial Controls-IfCORDocument47 pagesInternal Financial Controls-IfCORGovind PaliwalNo ratings yet

- Risk Analysis MemoDocument7 pagesRisk Analysis MemoAnonymous in4fhbdwkNo ratings yet

- Form 18 Sdi 2 - Loans - Risk of Material Misstatement (Romm) WorksheetDocument27 pagesForm 18 Sdi 2 - Loans - Risk of Material Misstatement (Romm) WorksheetwellawalalasithNo ratings yet

- Commission On Higher Education - Regional Office - Student Services Monitoring InstrumentDocument64 pagesCommission On Higher Education - Regional Office - Student Services Monitoring InstrumentdreaNo ratings yet

- Integration Workplan For Core FunctionsDocument51 pagesIntegration Workplan For Core Functionsthe_playerNo ratings yet

- Risk of Material Misstatement Worksheet - Overview General InstructionsDocument26 pagesRisk of Material Misstatement Worksheet - Overview General InstructionswellawalalasithNo ratings yet

- BSSOXPurchasing&Payables Control MatrixDocument2 pagesBSSOXPurchasing&Payables Control MatrixDivine GraceNo ratings yet

- Form 18 Sdi 4 - Recourse Liabilities - Risk of Material Misstatement (Romm) WorksheetDocument17 pagesForm 18 Sdi 4 - Recourse Liabilities - Risk of Material Misstatement (Romm) WorksheetwellawalalasithNo ratings yet

- Fraud Awareness Training: Detection and PreventionDocument20 pagesFraud Awareness Training: Detection and PreventionDataMis EliosHealthCareNo ratings yet

- NYC Comptroller Audit of DOT Bridge WorkDocument38 pagesNYC Comptroller Audit of DOT Bridge WorkGersh KuntzmanNo ratings yet

- Scope of Concurrent AuditDocument17 pagesScope of Concurrent AuditAnandNo ratings yet

- ISA 240 - Auditor's Responsibilities Relating To Fraud: Akash Mukesh Kumar, ACADocument20 pagesISA 240 - Auditor's Responsibilities Relating To Fraud: Akash Mukesh Kumar, ACAJ. EDUNo ratings yet

- Inventory Inventory IDR Control NoDocument23 pagesInventory Inventory IDR Control NoCA Rahul GuptaNo ratings yet

- INTERNAL CONTROLS - Section 3 Example of Documentation: FlowchartDocument8 pagesINTERNAL CONTROLS - Section 3 Example of Documentation: Flowchartحسين عبدالرحمنNo ratings yet

- Treasury RCM 2022-2023Document1 pageTreasury RCM 2022-2023Aman ParchaniNo ratings yet

- SUM - Summary of Uncorrected MisstatementsDocument1 pageSUM - Summary of Uncorrected MisstatementsCharielle Esthelin BacuganNo ratings yet

- Ombudsman Victoria Complaint Handling Good Practice Guide1Document58 pagesOmbudsman Victoria Complaint Handling Good Practice Guide1Rhea SimoneNo ratings yet

- Form 1840sdi-2 - Substantive Procedures Guide - Banking and Finance - LoansDocument17 pagesForm 1840sdi-2 - Substantive Procedures Guide - Banking and Finance - LoanswellawalalasithNo ratings yet

- Risk Assesment by Program AreaDocument7 pagesRisk Assesment by Program AreaJoanne PerandoNo ratings yet

- Consideration of Management Override of ControlsDocument2 pagesConsideration of Management Override of ControlsCaterina De LucaNo ratings yet

- Combatting Financial Crime in The UAEDocument11 pagesCombatting Financial Crime in The UAEBellaNo ratings yet

- SWOT Analysis: Organizational Context and Interested Parties Need & ExpectationDocument43 pagesSWOT Analysis: Organizational Context and Interested Parties Need & Expectationamril alrizaNo ratings yet

- Sunera Best Practices For Remediating SoDsDocument7 pagesSunera Best Practices For Remediating SoDssura anil reddyNo ratings yet

- Risk Assessment BackfilligDocument5 pagesRisk Assessment Backfilligmolobe mkhondoNo ratings yet

- Debt Interest Expense Substantive AnalyticalDocument2 pagesDebt Interest Expense Substantive AnalyticalErik RodriguesNo ratings yet

- Risk Management ManualDocument78 pagesRisk Management ManualSaudi MindNo ratings yet

- 2014 PricewaterhouseCoopers LLPDocument56 pages2014 PricewaterhouseCoopers LLPJahidur Rahman FcaNo ratings yet

- Understanding Transaction Monitoring V 1.0Document51 pagesUnderstanding Transaction Monitoring V 1.0Michael O'hare100% (1)

- Related Parties PT 2Document8 pagesRelated Parties PT 2Caterina De LucaNo ratings yet

- 104 2022 221 GTDocument25 pages104 2022 221 GTJason BramwellNo ratings yet

- Credit Monitoring and Early Warning SignalsDocument10 pagesCredit Monitoring and Early Warning Signalssagar7No ratings yet

- Internal Audit Manual Example 2024Document24 pagesInternal Audit Manual Example 2024DEEPAKNo ratings yet

- Soal Internal Control FinalDocument51 pagesSoal Internal Control FinalneysascribdNo ratings yet

- TheProcure To PayCyclebyChristineDoxeyDocument6 pagesTheProcure To PayCyclebyChristineDoxeyManna MahadiNo ratings yet

- Auditing in An ERP Environment Chapter 3: Automated Application ControlsDocument39 pagesAuditing in An ERP Environment Chapter 3: Automated Application Controlssrinathaladi shilpa100% (1)

- KVSS 2022 Financial StatementDocument36 pagesKVSS 2022 Financial StatementKristofer PlonaNo ratings yet

- 2020 Inspection Grant Thornton LLP: (Headquartered in Chicago, Illinois)Document24 pages2020 Inspection Grant Thornton LLP: (Headquartered in Chicago, Illinois)Jason BramwellNo ratings yet

- Fintech and Covid 19 Web (2022)Document261 pagesFintech and Covid 19 Web (2022)max tesNo ratings yet

- Risks and Controls For AML Monitoring SystemsDocument25 pagesRisks and Controls For AML Monitoring SystemsSanjay SainiNo ratings yet

- Forensic Accounting Vs Investigative Auditing On Fraud Detection-MatDocument40 pagesForensic Accounting Vs Investigative Auditing On Fraud Detection-MatUpdater proNo ratings yet

- Module 6 - Understanding The Entity and Its EnvironmentDocument11 pagesModule 6 - Understanding The Entity and Its EnvironmentMa Jessa Kathryl Alar IINo ratings yet

- Related Parties ISA 550 Audit CAF 9 (ARM+AMK)Document11 pagesRelated Parties ISA 550 Audit CAF 9 (ARM+AMK)Abdul WahabNo ratings yet

- Independence Confirmation Affidavit For Managers 2019Document12 pagesIndependence Confirmation Affidavit For Managers 2019Kushagra AgarwalNo ratings yet

- 2020 Internal Audit Report Stateof Good RepairDocument8 pages2020 Internal Audit Report Stateof Good RepairRamzi MHIRINo ratings yet

- Wiley Not-for-Profit GAAP 2017: Interpretation and Application of Generally Accepted Accounting PrinciplesFrom EverandWiley Not-for-Profit GAAP 2017: Interpretation and Application of Generally Accepted Accounting PrinciplesNo ratings yet

- List of Older CircularsDocument3 pagesList of Older CircularsBhaskar GarimellaNo ratings yet

- Reference Layout of KYC Circular - RBIDocument6 pagesReference Layout of KYC Circular - RBIBhaskar GarimellaNo ratings yet

- Islamic BankingDocument26 pagesIslamic BankingBhaskar GarimellaNo ratings yet

- RBI - Determination of A Beneficiary OwnerDocument2 pagesRBI - Determination of A Beneficiary OwnerBhaskar GarimellaNo ratings yet

- Digital-Alternate ChannelDocument146 pagesDigital-Alternate ChannelBhaskar GarimellaNo ratings yet

- RBI - Definition of 'Infrastructure Lending'Document9 pagesRBI - Definition of 'Infrastructure Lending'Bhaskar GarimellaNo ratings yet

- Revision in Pay and Allowance 01.04.2021Document26 pagesRevision in Pay and Allowance 01.04.2021Bhaskar GarimellaNo ratings yet

- Research Methodology To InputDocument13 pagesResearch Methodology To InputBhaskar GarimellaNo ratings yet

- List of Firms SampledDocument90 pagesList of Firms SampledBhaskar GarimellaNo ratings yet

- IEEE TemplateDocument8 pagesIEEE TemplateBhaskar GarimellaNo ratings yet

- Industry-Wise Benchmarks Key Fin RatiosDocument18 pagesIndustry-Wise Benchmarks Key Fin RatiosBhaskar GarimellaNo ratings yet

- Schedules of Balance SheetDocument3 pagesSchedules of Balance SheetBhaskar GarimellaNo ratings yet

- Credit Scoring ChecklistDocument2 pagesCredit Scoring ChecklistBhaskar GarimellaNo ratings yet

- Micro Research - Advt-19-20Document1 pageMicro Research - Advt-19-20Bhaskar GarimellaNo ratings yet

- Risk-Spectrum - Vehicles (CRISIL Report)Document7 pagesRisk-Spectrum - Vehicles (CRISIL Report)Bhaskar GarimellaNo ratings yet

- JSS Brochure 2022Document30 pagesJSS Brochure 2022Bhaskar GarimellaNo ratings yet

- Credit Processing For CVDocument5 pagesCredit Processing For CVBhaskar GarimellaNo ratings yet

- Case Reference - SK FinanceDocument2 pagesCase Reference - SK FinanceBhaskar GarimellaNo ratings yet

- RBI Circular On VigilanceDocument8 pagesRBI Circular On VigilanceBhaskar Garimella100% (1)

- I Wayan Artha Wijaya: RingkasanDocument2 pagesI Wayan Artha Wijaya: RingkasanBerlian JosephNo ratings yet

- Procurement PlanDocument3 pagesProcurement Planmmalnar1No ratings yet

- 'XSK-1100894-south Bay - BDocument5 pages'XSK-1100894-south Bay - BngNo ratings yet

- 2010 - Rosly - Shariah Parameter ReconsideredDocument19 pages2010 - Rosly - Shariah Parameter ReconsideredyuwonliloNo ratings yet

- Learn To Profit From Intraday Trading in NiftyDocument10 pagesLearn To Profit From Intraday Trading in Niftyuday_kendhe90050% (1)

- A Project Report Prakash ThapaDocument67 pagesA Project Report Prakash ThapaMitesh Prajapati 7765No ratings yet

- Taxation Enhancement ExercisesDocument13 pagesTaxation Enhancement ExercisesRachel LeachonNo ratings yet

- Black BookDocument55 pagesBlack Bookprabhas MakwanaNo ratings yet

- Info SysDocument58 pagesInfo SysBirddoxyNo ratings yet

- Presentation On DerevativeDocument19 pagesPresentation On DerevativeAnkitaParabNo ratings yet

- TQM Brief 1Document39 pagesTQM Brief 1selvaganapathy1992100% (1)

- Iqmin A Jktinv0087205 Jktyulia 20230408071006Document1 pageIqmin A Jktinv0087205 Jktyulia 20230408071006Rahayu UmarNo ratings yet

- AF301 Unit 8 System Oriented TheoriesDocument28 pagesAF301 Unit 8 System Oriented TheoriesNarayan DiviyaNo ratings yet

- Problems For Cash and Cash EquivalentsDocument1 pageProblems For Cash and Cash EquivalentsTine Vasiana DuermeNo ratings yet

- Cbroa News December 2020 2 PDFDocument37 pagesCbroa News December 2020 2 PDFVijay IyerNo ratings yet

- Bond and Bond Features and Its Example AssignmentDocument4 pagesBond and Bond Features and Its Example AssignmentWaqaarNo ratings yet

- Company Profile PT Geo Explo OptimaDocument6 pagesCompany Profile PT Geo Explo OptimaRinaldi SatriaNo ratings yet

- Jose Ramona InvoiceDocument1 pageJose Ramona InvoiceDavid MendozaNo ratings yet

- Seminar 6.1Document2 pagesSeminar 6.1Đạt PhạmNo ratings yet

- TKRS TOT Calon Surveior Akreditasi RS Arjaty 29 Desember 2021Document47 pagesTKRS TOT Calon Surveior Akreditasi RS Arjaty 29 Desember 2021Yuliana SariNo ratings yet

- Elasticity and Tax IncidenceDocument11 pagesElasticity and Tax IncidenceKiara RamdhawNo ratings yet

- Activity 3 - Doing in The EnvironmentDocument1 pageActivity 3 - Doing in The EnvironmentKin Anthony NocumNo ratings yet

- 12.2% CAGR: Fuel Containment Processing Equipment Service Canada United StatesDocument1 page12.2% CAGR: Fuel Containment Processing Equipment Service Canada United StatesRandy LaheyNo ratings yet

- Financial Management: Financial Management Refers To That Part of TheDocument19 pagesFinancial Management: Financial Management Refers To That Part of TheMayuraa ShekatkarNo ratings yet

- ISCC FeesDocument1 pageISCC FeesAyoubELBakiriNo ratings yet

- PTMADocument7 pagesPTMAAman Kumar SharanNo ratings yet

- T26 026 902 PDFDocument7 pagesT26 026 902 PDFBenNo ratings yet

- Jaymar M Jabonillo ResumeDocument3 pagesJaymar M Jabonillo ResumeNanjiro EchizenNo ratings yet