Download as docx, pdf, or txt

You might also like

- Maria Hernandez & AssociatesDocument2 pagesMaria Hernandez & AssociatesManish Kumar33% (3)

- Iso 10014 2021 en PDFDocument8 pagesIso 10014 2021 en PDFDame Yenyetou0% (1)

- Questoin 1Document6 pagesQuestoin 1Abdullah EjazNo ratings yet

- Financial Accounting - Reporting November 2021 Suggested SolutionsDocument6 pagesFinancial Accounting - Reporting November 2021 Suggested SolutionsMunodawafa ChimhamhiwaNo ratings yet

- Financial Management Mock 2Document7 pagesFinancial Management Mock 2sadathamid03No ratings yet

- FR 2019 Marjun Sample A PDFDocument10 pagesFR 2019 Marjun Sample A PDFJenifer KlintonNo ratings yet

- Consolidated Financial Statements As of December 31 2020Document86 pagesConsolidated Financial Statements As of December 31 2020Raka AryawanNo ratings yet

- The Colombo Fort Land & Building PLC: Annual Report 2020/21Document156 pagesThe Colombo Fort Land & Building PLC: Annual Report 2020/21sandun suranjanNo ratings yet

- ACCA P2 Corporate Reporting - Mock Exam Answers 1 PDFDocument24 pagesACCA P2 Corporate Reporting - Mock Exam Answers 1 PDFමිලන්No ratings yet

- Consolidated Statement of Cash Flows (MFRS 107)Document41 pagesConsolidated Statement of Cash Flows (MFRS 107)Sing YeeNo ratings yet

- Taxation Solution 2017 SeptemberDocument11 pagesTaxation Solution 2017 Septemberzezu zazaNo ratings yet

- Ifrs9 For BanksDocument58 pagesIfrs9 For BanksMiladNo ratings yet

- KIL Result June-2022Document3 pagesKIL Result June-2022akshay kausaleNo ratings yet

- b02037 Chapter 10 Financial PlanningDocument14 pagesb02037 Chapter 10 Financial PlanningLê Tấn TàiNo ratings yet

- Projected P&L and BSDocument9 pagesProjected P&L and BSbipin kumarNo ratings yet

- IAS 19 - Class Practice (Solutions)Document4 pagesIAS 19 - Class Practice (Solutions)Muhammed NaqiNo ratings yet

- LVMH 2020 Consolidated Financial StatementDocument99 pagesLVMH 2020 Consolidated Financial StatementGEETIKA PATRANo ratings yet

- Chapter 22Document9 pagesChapter 22Mahmoud DakikNo ratings yet

- Financial Statements AnalysisDocument5 pagesFinancial Statements AnalysisSAQIB SAEEDNo ratings yet

- WBSLive Lecture 5 Slides Pres VevoxDocument25 pagesWBSLive Lecture 5 Slides Pres VevoxabhirejanilNo ratings yet

- Consolidation Q61 PDFDocument5 pagesConsolidation Q61 PDFAmrita TamangNo ratings yet

- Royal DSM AGM Report 2020Document298 pagesRoyal DSM AGM Report 2020Ike EdmondNo ratings yet

- 7001 Assignment #3Document9 pages7001 Assignment #3南玖No ratings yet

- SBR INT-2018-dec-QPDocument7 pagesSBR INT-2018-dec-QPkeyn1230No ratings yet

- Cashflows From Operating Activities: Code Profit Before Tax 1Document21 pagesCashflows From Operating Activities: Code Profit Before Tax 1Lâm Ninh TùngNo ratings yet

- RemunerationDocument15 pagesRemunerationHarry ScoldfieldNo ratings yet

- Financial StatementsDocument92 pagesFinancial StatementsJaspreet KaurNo ratings yet

- InvestorPresentation-1H2016vFpinang CoalDocument20 pagesInvestorPresentation-1H2016vFpinang CoalHendry ChristiantoNo ratings yet

- Far 202324 t2 Normal LVMH 2019 Eng FinancialstatementsDocument88 pagesFar 202324 t2 Normal LVMH 2019 Eng Financialstatementslingling9905No ratings yet

- Eramet Annual Consolidated Financial Statements at 31december2020Document90 pagesEramet Annual Consolidated Financial Statements at 31december2020hyenadogNo ratings yet

- Ifrs (Usd) (En)Document49 pagesIfrs (Usd) (En)Ameya KulkarniNo ratings yet

- O Reissue of 2019 Financial Statements o 1Q20 ResultsDocument17 pagesO Reissue of 2019 Financial Statements o 1Q20 Resultsjenric19No ratings yet

- Questions - Cost of Capital and Sources of FinanceDocument3 pagesQuestions - Cost of Capital and Sources of Financepercy mapetereNo ratings yet

- ACCA SBR Mar-20 FightingDocument34 pagesACCA SBR Mar-20 FightingThu Lê HoàiNo ratings yet

- Model Solution: Company-Operated RestaurantsDocument16 pagesModel Solution: Company-Operated Restaurantspranjal92pandeyNo ratings yet

- Employee Benefits IAS 19Document17 pagesEmployee Benefits IAS 19Tinashe ZhouNo ratings yet

- Tutorial 2 AnswerDocument2 pagesTutorial 2 AnswerDiana TuckerNo ratings yet

- 13 Chapter 6.2 - LeverageDocument12 pages13 Chapter 6.2 - Leverageatishayjjj123No ratings yet

- 2020 LBG q1 Ims Excel Download v2Document16 pages2020 LBG q1 Ims Excel Download v2saxobobNo ratings yet

- Kering V2Document6 pagesKering V2Pranav HansonNo ratings yet

- © The Institute of Chartered Accountants of IndiaDocument24 pages© The Institute of Chartered Accountants of IndiaAniketNo ratings yet

- Sap Fi Gen FinanceDocument7 pagesSap Fi Gen FinanceRavi Chandra LNo ratings yet

- Q123 Investor Call Presentation - Financial Slides 15.05.2023 - VFDocument12 pagesQ123 Investor Call Presentation - Financial Slides 15.05.2023 - VFKA-11 Єфіменко ІванNo ratings yet

- Greenko - Dutch - Audited - Combined - Financial - Statements - FY 2018 - 19Document1 pageGreenko - Dutch - Audited - Combined - Financial - Statements - FY 2018 - 19hNo ratings yet

- DirectorsreportDocument13 pagesDirectorsreportSuri KunalNo ratings yet

- In Millions of Euros, Except For Per Share DataDocument33 pagesIn Millions of Euros, Except For Per Share DataGrace StylesNo ratings yet

- Report Q1 2010Document24 pagesReport Q1 2010Frode HaukenesNo ratings yet

- EPFLAcforFinance17 5Document67 pagesEPFLAcforFinance17 5ddd huangNo ratings yet

- Profe03 - Chapter 5 Consolidated FS Intercompany TopicsDocument8 pagesProfe03 - Chapter 5 Consolidated FS Intercompany TopicsSteffany RoqueNo ratings yet

- Financial Accounting: Income Statement StructureDocument16 pagesFinancial Accounting: Income Statement StructureEdward AbgarNo ratings yet

- Practice Set (Solutions) - IAS 19 PDFDocument4 pagesPractice Set (Solutions) - IAS 19 PDFAli HaiderNo ratings yet

- FCMB Group PLC - Quarter 1 - Financial Statement For 2023 Financial Statements April 2023Document40 pagesFCMB Group PLC - Quarter 1 - Financial Statement For 2023 Financial Statements April 202381Clouds UniverseNo ratings yet

- NYSE_CIT_1997Document8 pagesNYSE_CIT_1997pcelica77No ratings yet

- Citigroup Q1 Earnings Financial SupplementDocument33 pagesCitigroup Q1 Earnings Financial SupplementWall Street FollyNo ratings yet

- Consolidated Balance Sheet For Hindustan Unilever LTDDocument11 pagesConsolidated Balance Sheet For Hindustan Unilever LTDMohit ChughNo ratings yet

- GK Audited Financial 31-Dec-2010Document97 pagesGK Audited Financial 31-Dec-2010Dante GillespieNo ratings yet

- Case 6 1Document3 pagesCase 6 1dianedinzila.ddNo ratings yet

- Statement of Profit and LossDocument2 pagesStatement of Profit and LossradhikaNo ratings yet

- Statement of Profit and LossDocument2 pagesStatement of Profit and Lossradhika100% (1)

- Cash Flow Explanatory SheetDocument4 pagesCash Flow Explanatory SheetTony DarwishNo ratings yet

- Financial Results Annual 2010 RMWLDocument1 pageFinancial Results Annual 2010 RMWLSanjay GulatiNo ratings yet

- Lesson 14 - Maintenance of Registers and RecordsDocument4 pagesLesson 14 - Maintenance of Registers and RecordshemaNo ratings yet

- The Economic Problems of The PhilippinesDocument3 pagesThe Economic Problems of The PhilippinesRodolfo Esmejarda Laycano Jr.50% (6)

- Costing MCQ 1 PDFDocument19 pagesCosting MCQ 1 PDFCostas Pinto100% (1)

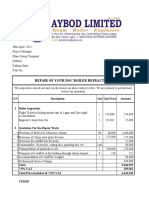

- Repair of Doc Boiler RefractoryDocument2 pagesRepair of Doc Boiler RefractoryIshola TaiwoNo ratings yet

- Dental Clinic Management System Rationale Chapter 1Document3 pagesDental Clinic Management System Rationale Chapter 1bryle.alegada03No ratings yet

- Direct and Indirect TaxDocument10 pagesDirect and Indirect TaxAman KumarNo ratings yet

- tài chính doanh nghiệpDocument44 pagestài chính doanh nghiệptieuma712No ratings yet

- 06 Consolidation AnnotatedDocument18 pages06 Consolidation AnnotatedLloydNo ratings yet

- Partnership AgreementDocument4 pagesPartnership AgreementLYNETTE MAREY APOLINARIONo ratings yet

- ROMARIC SENA DJIDONOU - Derniers Chiffres de La Carte - 0114Document2 pagesROMARIC SENA DJIDONOU - Derniers Chiffres de La Carte - 0114Franck LawNo ratings yet

- As 4 Contingencies and Events Occuring After The Balance Sheet DateDocument9 pagesAs 4 Contingencies and Events Occuring After The Balance Sheet Dateanon_672065362No ratings yet

- Bal Bharati Mid Term XIi - 2023-24Document9 pagesBal Bharati Mid Term XIi - 2023-24Thakur ShikharNo ratings yet

- EmergingDocument14 pagesEmergingleulsiraj0No ratings yet

- Set Off Carry Forward of LossesDocument9 pagesSet Off Carry Forward of LossesMueen KhanNo ratings yet

- The Wall Street Journal - 16.06.2021Document32 pagesThe Wall Street Journal - 16.06.2021Adolfo PerezNo ratings yet

- Principle of AccountsDocument153 pagesPrinciple of AccountsAndrea MalubaNo ratings yet

- Feasibility Study FormatDocument20 pagesFeasibility Study FormatMichelle UrbodaNo ratings yet

- Global Operations & Supply Chain ManagementDocument37 pagesGlobal Operations & Supply Chain ManagementAnonymousNo ratings yet

- Antony Waste Handling Cell Limited - DRHP - 20200930183544Document428 pagesAntony Waste Handling Cell Limited - DRHP - 20200930183544SubscriptionNo ratings yet

- Does Effeciency Wage Hypothesis Hold in Tanzanian Labour Market? Godius KahyararaDocument18 pagesDoes Effeciency Wage Hypothesis Hold in Tanzanian Labour Market? Godius KahyararaCepade ProjectosNo ratings yet

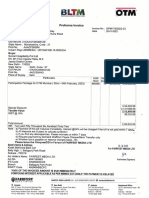

- Sorrel Otm FebDocument1 pageSorrel Otm FebGagandeep SinghNo ratings yet

- Internship Report Saqlain ArifDocument65 pagesInternship Report Saqlain ArifSaqlain KhanNo ratings yet

- GH DoceDocument4 pagesGH DoceippiliNo ratings yet

- Rs Agarwal BillDocument1 pageRs Agarwal BillrithinNo ratings yet

- Financial ServicesDocument23 pagesFinancial ServicesMidhun ManoharNo ratings yet

- Assignment 2 - SCMDocument3 pagesAssignment 2 - SCMdhanu rithikNo ratings yet

- Unit 4 Allocation of Overhead CostDocument27 pagesUnit 4 Allocation of Overhead CostTanishq KambojNo ratings yet

- Working Capital Management: A Case Study of Hero Motocorp Pvt. LTDDocument7 pagesWorking Capital Management: A Case Study of Hero Motocorp Pvt. LTDaloksingh420aloksigh420No ratings yet