06 Laboratory Exercise 1

06 Laboratory Exercise 1

You might also like

- Topic 6 - Bank ReconciliationRev (Students)Document26 pagesTopic 6 - Bank ReconciliationRev (Students)Romzi100% (1)

- Proof of CashDocument7 pagesProof of CashPeachy80% (5)

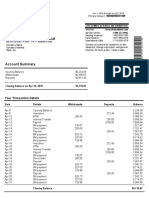

- Account Summary: Your Transaction DetailsDocument1 pageAccount Summary: Your Transaction Detailsdelfa100% (1)

- Bank Reconciliation StatementDocument3 pagesBank Reconciliation StatementZoie JulienNo ratings yet

- FABM2-MODULE 9 - With ActivitiesDocument7 pagesFABM2-MODULE 9 - With ActivitiesROWENA MARAMBANo ratings yet

- Module 1C - Bank ReconciliationDocument4 pagesModule 1C - Bank ReconciliationtoshirohanamaruNo ratings yet

- Bank Reconcilition NotesDocument6 pagesBank Reconcilition NotesNurul Hazirah ZulkifliNo ratings yet

- Ch#7 BANK RECONCILIATION STATEMENTDocument4 pagesCh#7 BANK RECONCILIATION STATEMENTeaglerealestate31No ratings yet

- Bank ReconciliationDocument19 pagesBank ReconciliationSheenaGaliciaNew100% (4)

- Bank Reconcillation StatementDocument22 pagesBank Reconcillation StatementZaid SiddiqueNo ratings yet

- Bank Reconciliation, Petty Cash & Voucher SystemDocument4 pagesBank Reconciliation, Petty Cash & Voucher SystemYellow CarterNo ratings yet

- Fabm2 Q2 M3 - 4Document9 pagesFabm2 Q2 M3 - 4Zeus MalicdemNo ratings yet

- INTERMEDIATE ACCOUNTING I Bank ReconciliationDocument3 pagesINTERMEDIATE ACCOUNTING I Bank ReconciliationMark Navida AgunaNo ratings yet

- Bank ReconciliationDocument1 pageBank ReconciliationopticalgridcivilNo ratings yet

- Cfas CashDocument5 pagesCfas CashGeelyka MarquezNo ratings yet

- Audit Form - Working Paper - PCFDocument18 pagesAudit Form - Working Paper - PCFIra YbanezNo ratings yet

- Bank ReconciliationDocument1 pageBank ReconciliationMary Jullianne Caile SalcedoNo ratings yet

- 6 Lesson Six Bank ReconciliationDocument4 pages6 Lesson Six Bank ReconciliationmeshackcheruiyottNo ratings yet

- Module 1b - Bank ReconDocument37 pagesModule 1b - Bank ReconChen HaoNo ratings yet

- Module 3Document5 pagesModule 3Simoun EnriqueNo ratings yet

- Finals FABM2 Lesson 2 Bank ReconciliationDocument4 pagesFinals FABM2 Lesson 2 Bank ReconciliationJasmine VelosoNo ratings yet

- Two-Date Bank ReconciliationDocument5 pagesTwo-Date Bank Reconciliationsweet ecstacyNo ratings yet

- Topic 6 - Bank ReconciliationRev (Students)Document32 pagesTopic 6 - Bank ReconciliationRev (Students)Novian Dwi RamadanaNo ratings yet

- Chapter 6 Bank ReconciliationRev StudentsDocument20 pagesChapter 6 Bank ReconciliationRev StudentsNemalai VitalNo ratings yet

- ACC 124 HO 5 Bank Reconciliation and Proof of Cash - 0Document4 pagesACC 124 HO 5 Bank Reconciliation and Proof of Cash - 0Lily Scarlett ChìnNo ratings yet

- Basic Instructions For A Bank Reconciliation Statement PDFDocument4 pagesBasic Instructions For A Bank Reconciliation Statement PDFAman KodwaniNo ratings yet

- CHAPTER 09.bank Reconciliation StatementsDocument10 pagesCHAPTER 09.bank Reconciliation StatementsZaid SiddiqueNo ratings yet

- (Studocu) Int Acc Chapter 3 - Valix, Robles, Empleo, MillanDocument4 pages(Studocu) Int Acc Chapter 3 - Valix, Robles, Empleo, MillanHufana, Shelley100% (1)

- ACCOUNTING 102 - Topic #3 "Proof of Cash"Document4 pagesACCOUNTING 102 - Topic #3 "Proof of Cash"CLEAR MELODY VILLARANNo ratings yet

- Bank ReconciliationDocument14 pagesBank Reconciliationnicolettecatamio015No ratings yet

- 6_Bank_Reconciliation Additional Notes and IllustrationDocument9 pages6_Bank_Reconciliation Additional Notes and IllustrationmeshackcheruiyottNo ratings yet

- FINACC1 - Bank Reconciliation and Proof of CashDocument2 pagesFINACC1 - Bank Reconciliation and Proof of CashJerico DungcaNo ratings yet

- Bank ReconciliationDocument15 pagesBank Reconciliationhay buhayNo ratings yet

- FAR1 - Bank Reconciliation and Proof of CashDocument2 pagesFAR1 - Bank Reconciliation and Proof of CashHoney MuliNo ratings yet

- Bank ReconciliationDocument26 pagesBank ReconciliationQuennie Kate RomeroNo ratings yet

- Module 2 - Topic 2 Bank Reconciliation: Ms. Daizy Marie P. Nicart, CPADocument24 pagesModule 2 - Topic 2 Bank Reconciliation: Ms. Daizy Marie P. Nicart, CPALucas BantilingNo ratings yet

- Module 2 - Bank Reconciliation - With Sample ExercisesDocument24 pagesModule 2 - Bank Reconciliation - With Sample ExercisesJudie Ellaine SumandacNo ratings yet

- Cash and Cash Equivalents 1Document22 pagesCash and Cash Equivalents 1Mark GilNo ratings yet

- 03 Bank ReconciliationDocument5 pages03 Bank ReconciliationalteregoNo ratings yet

- Bank Reconciliation Journal Entries - Double Entry BookkeepingDocument9 pagesBank Reconciliation Journal Entries - Double Entry BookkeepingMizanur RahmanNo ratings yet

- CWTS1-USA-B-SAPE InfographicDocument1 pageCWTS1-USA-B-SAPE InfographiccyriljunaicamaranquezNo ratings yet

- Fabm2 QTR.2 Las 7.1Document10 pagesFabm2 QTR.2 Las 7.1Trunks KunNo ratings yet

- Chapter 5 Bank Reconciliation StatementDocument2 pagesChapter 5 Bank Reconciliation StatementDeveender Kaur JudgeNo ratings yet

- Receivable FinancingDocument34 pagesReceivable FinancingmaryzeenNo ratings yet

- Receivable Financing CH14 by LailaneDocument30 pagesReceivable Financing CH14 by LailaneEunice BernalNo ratings yet

- Module 8Document3 pagesModule 8Rainielle Sy DulatreNo ratings yet

- Bank Reconciliation StatementDocument12 pagesBank Reconciliation StatementMuhammad BilalNo ratings yet

- Chapter 3 Bank Recon Lecture StudentDocument5 pagesChapter 3 Bank Recon Lecture StudentAshlene CruzNo ratings yet

- Bank ReconciliationDocument3 pagesBank ReconciliationZejkeara ImperialNo ratings yet

- Journal Entries For Bank ReconciliationDocument2 pagesJournal Entries For Bank ReconciliationAira Mae Quinones OrendainNo ratings yet

- Bank ReconciliationDocument27 pagesBank Reconciliationnaruto uzumakiNo ratings yet

- Bank ReconciliationDocument23 pagesBank ReconciliationJohn Anjelo MoraldeNo ratings yet

- Bank Reconciliations - 1Document9 pagesBank Reconciliations - 1ZAKAYO NJONYNo ratings yet

- Receivable Financing: Pledge, Assignment, and FactoringDocument30 pagesReceivable Financing: Pledge, Assignment, and FactoringJoy UyNo ratings yet

- Aa21 Afa Chapter 01 EnglishDocument12 pagesAa21 Afa Chapter 01 EnglishnafeesNo ratings yet

- Fabm2 - 8.2Document15 pagesFabm2 - 8.2Kervin GuevaraNo ratings yet

- Chap 9 - Proof of Cash Fin Acct 1 - Barter Summary Team PDFDocument7 pagesChap 9 - Proof of Cash Fin Acct 1 - Barter Summary Team PDFCarl James Austria100% (1)

- Dictioformula ProblemsDocument42 pagesDictioformula ProblemsEza Joy ClaveriasNo ratings yet

- CH08 Bank ReconciliationDocument12 pagesCH08 Bank ReconciliationRose DionioNo ratings yet

- ABM FABM2 Q2 Wk3 LAS3Document11 pagesABM FABM2 Q2 Wk3 LAS3ayaNo ratings yet

- 05 Laboratory Exercise 1Document2 pages05 Laboratory Exercise 1Praisen JoyNo ratings yet

- Formulas in Business FinanceDocument4 pagesFormulas in Business FinancePraisen JoyNo ratings yet

- 07 Laboratory Exercise 1Document3 pages07 Laboratory Exercise 1Praisen JoyNo ratings yet

- 08 Quiz 1Document3 pages08 Quiz 1Praisen JoyNo ratings yet

- Fixedline and Broadband Services: Your Account Summary This Month'S ChargesDocument2 pagesFixedline and Broadband Services: Your Account Summary This Month'S ChargesMaximuzNo ratings yet

- Faqs On Internet Banking Services (Ibs) For NrisDocument2 pagesFaqs On Internet Banking Services (Ibs) For NrisABMNo ratings yet

- Marketing of Financial Services NMIMS AssignmentDocument4 pagesMarketing of Financial Services NMIMS AssignmentN. Karthik UdupaNo ratings yet

- Check-Out Procedures: B.Sc. (HHA) / 2 Year/ Checkout ProceduresDocument10 pagesCheck-Out Procedures: B.Sc. (HHA) / 2 Year/ Checkout ProceduresAryan BishtNo ratings yet

- Business Banking Price ListDocument15 pagesBusiness Banking Price ListSARFRAZ ALINo ratings yet

- Mastering Personal Credit and Personal FudningDocument15 pagesMastering Personal Credit and Personal FudningAli Tarafdar, QFOPNo ratings yet

- Lecture Sheet of Final Syllabus: Negotiable Instruments Act, 1881Document4 pagesLecture Sheet of Final Syllabus: Negotiable Instruments Act, 1881Eshthiak HossainNo ratings yet

- Niam Knoll - TransUnion Personal Credit Report - 20200802Document4 pagesNiam Knoll - TransUnion Personal Credit Report - 20200802Bruce WaynneNo ratings yet

- Individual Assignment - On - COMPANY - STRATEGIC - ANALYSIS.Document14 pagesIndividual Assignment - On - COMPANY - STRATEGIC - ANALYSIS.Adanech100% (1)

- First American Bank's Donald Roubitcheck, Chief Financial Officer - Completed TARP - Use of Capital Survey, Donald Roubitchek CFO July 24, 2009Document3 pagesFirst American Bank's Donald Roubitcheck, Chief Financial Officer - Completed TARP - Use of Capital Survey, Donald Roubitchek CFO July 24, 2009larry-612445No ratings yet

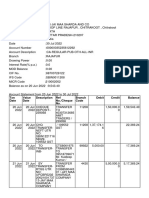

- Account Details and Transaction History: Mohd Salleh Bin AmboDocument2 pagesAccount Details and Transaction History: Mohd Salleh Bin AmboMohd Salleh AmboNo ratings yet

- Nilson Report Issue 1169Document12 pagesNilson Report Issue 1169John Mulder100% (1)

- Sob Select 30 12 2022Document2 pagesSob Select 30 12 2022nishan1187No ratings yet

- Canara Bank Project ReportDocument16 pagesCanara Bank Project Reportsagar m100% (1)

- Currency Seasonal Patterns Free EbookDocument21 pagesCurrency Seasonal Patterns Free Ebookkh267aziziNo ratings yet

- Weekly ReportDocument4 pagesWeekly ReportAiane_Reyes_5594No ratings yet

- Daftar Bank Yang Ada Di Wilayah PontianakDocument4 pagesDaftar Bank Yang Ada Di Wilayah PontianakWindia SariNo ratings yet

- Seminar Questions Set III A-2Document3 pagesSeminar Questions Set III A-2fanuel kijojiNo ratings yet

- FRM & VIGILANCE OF BANK POLICY J&K BankDocument37 pagesFRM & VIGILANCE OF BANK POLICY J&K BankAnshul BishtNo ratings yet

- Akong'a, Cynthia J - The Effect of Financial Risk Management On The Financial Performance of Commercial Banks in KenyaDocument57 pagesAkong'a, Cynthia J - The Effect of Financial Risk Management On The Financial Performance of Commercial Banks in KenyaEsobiebi ChristabelNo ratings yet

- Ch02-Cash Inflow OutFlowDocument45 pagesCh02-Cash Inflow OutFlowismat arteeNo ratings yet

- Moroz IlonaDocument1 pageMoroz IlonaСергей АлексеевичNo ratings yet

- Ch-2 FRONT OFFICE (ACCOUNTING)Document11 pagesCh-2 FRONT OFFICE (ACCOUNTING)DawaNo ratings yet

- Basu and Dutta Journal EntriesDocument7 pagesBasu and Dutta Journal EntriesAranya Haldar100% (2)

- Cambridge Ordinary LevelDocument12 pagesCambridge Ordinary LevelAlexNo ratings yet

- RamishDocument14 pagesRamishpradeep swatiNo ratings yet

- Updated - Note On NeobanksDocument38 pagesUpdated - Note On NeobanksAnirudh SoodNo ratings yet

- Chapter 2 AccountingDocument12 pagesChapter 2 Accountingmoon loverNo ratings yet

- 0151xxxxxxxx6295 - 2023 12 01Document6 pages0151xxxxxxxx6295 - 2023 12 01George GeranisNo ratings yet

Download as pdf or txt

You might also like

- Topic 6 - Bank ReconciliationRev (Students)Document26 pagesTopic 6 - Bank ReconciliationRev (Students)Romzi100% (1)

- Proof of CashDocument7 pagesProof of CashPeachy80% (5)

- Account Summary: Your Transaction DetailsDocument1 pageAccount Summary: Your Transaction Detailsdelfa100% (1)

- Bank Reconciliation StatementDocument3 pagesBank Reconciliation StatementZoie JulienNo ratings yet

- FABM2-MODULE 9 - With ActivitiesDocument7 pagesFABM2-MODULE 9 - With ActivitiesROWENA MARAMBANo ratings yet

- Module 1C - Bank ReconciliationDocument4 pagesModule 1C - Bank ReconciliationtoshirohanamaruNo ratings yet

- Bank Reconcilition NotesDocument6 pagesBank Reconcilition NotesNurul Hazirah ZulkifliNo ratings yet

- Ch#7 BANK RECONCILIATION STATEMENTDocument4 pagesCh#7 BANK RECONCILIATION STATEMENTeaglerealestate31No ratings yet

- Bank ReconciliationDocument19 pagesBank ReconciliationSheenaGaliciaNew100% (4)

- Bank Reconcillation StatementDocument22 pagesBank Reconcillation StatementZaid SiddiqueNo ratings yet

- Bank Reconciliation, Petty Cash & Voucher SystemDocument4 pagesBank Reconciliation, Petty Cash & Voucher SystemYellow CarterNo ratings yet

- Fabm2 Q2 M3 - 4Document9 pagesFabm2 Q2 M3 - 4Zeus MalicdemNo ratings yet

- INTERMEDIATE ACCOUNTING I Bank ReconciliationDocument3 pagesINTERMEDIATE ACCOUNTING I Bank ReconciliationMark Navida AgunaNo ratings yet

- Bank ReconciliationDocument1 pageBank ReconciliationopticalgridcivilNo ratings yet

- Cfas CashDocument5 pagesCfas CashGeelyka MarquezNo ratings yet

- Audit Form - Working Paper - PCFDocument18 pagesAudit Form - Working Paper - PCFIra YbanezNo ratings yet

- Bank ReconciliationDocument1 pageBank ReconciliationMary Jullianne Caile SalcedoNo ratings yet

- 6 Lesson Six Bank ReconciliationDocument4 pages6 Lesson Six Bank ReconciliationmeshackcheruiyottNo ratings yet

- Module 1b - Bank ReconDocument37 pagesModule 1b - Bank ReconChen HaoNo ratings yet

- Module 3Document5 pagesModule 3Simoun EnriqueNo ratings yet

- Finals FABM2 Lesson 2 Bank ReconciliationDocument4 pagesFinals FABM2 Lesson 2 Bank ReconciliationJasmine VelosoNo ratings yet

- Two-Date Bank ReconciliationDocument5 pagesTwo-Date Bank Reconciliationsweet ecstacyNo ratings yet

- Topic 6 - Bank ReconciliationRev (Students)Document32 pagesTopic 6 - Bank ReconciliationRev (Students)Novian Dwi RamadanaNo ratings yet

- Chapter 6 Bank ReconciliationRev StudentsDocument20 pagesChapter 6 Bank ReconciliationRev StudentsNemalai VitalNo ratings yet

- ACC 124 HO 5 Bank Reconciliation and Proof of Cash - 0Document4 pagesACC 124 HO 5 Bank Reconciliation and Proof of Cash - 0Lily Scarlett ChìnNo ratings yet

- Basic Instructions For A Bank Reconciliation Statement PDFDocument4 pagesBasic Instructions For A Bank Reconciliation Statement PDFAman KodwaniNo ratings yet

- CHAPTER 09.bank Reconciliation StatementsDocument10 pagesCHAPTER 09.bank Reconciliation StatementsZaid SiddiqueNo ratings yet

- (Studocu) Int Acc Chapter 3 - Valix, Robles, Empleo, MillanDocument4 pages(Studocu) Int Acc Chapter 3 - Valix, Robles, Empleo, MillanHufana, Shelley100% (1)

- ACCOUNTING 102 - Topic #3 "Proof of Cash"Document4 pagesACCOUNTING 102 - Topic #3 "Proof of Cash"CLEAR MELODY VILLARANNo ratings yet

- Bank ReconciliationDocument14 pagesBank Reconciliationnicolettecatamio015No ratings yet

- 6_Bank_Reconciliation Additional Notes and IllustrationDocument9 pages6_Bank_Reconciliation Additional Notes and IllustrationmeshackcheruiyottNo ratings yet

- FINACC1 - Bank Reconciliation and Proof of CashDocument2 pagesFINACC1 - Bank Reconciliation and Proof of CashJerico DungcaNo ratings yet

- Bank ReconciliationDocument15 pagesBank Reconciliationhay buhayNo ratings yet

- FAR1 - Bank Reconciliation and Proof of CashDocument2 pagesFAR1 - Bank Reconciliation and Proof of CashHoney MuliNo ratings yet

- Bank ReconciliationDocument26 pagesBank ReconciliationQuennie Kate RomeroNo ratings yet

- Module 2 - Topic 2 Bank Reconciliation: Ms. Daizy Marie P. Nicart, CPADocument24 pagesModule 2 - Topic 2 Bank Reconciliation: Ms. Daizy Marie P. Nicart, CPALucas BantilingNo ratings yet

- Module 2 - Bank Reconciliation - With Sample ExercisesDocument24 pagesModule 2 - Bank Reconciliation - With Sample ExercisesJudie Ellaine SumandacNo ratings yet

- Cash and Cash Equivalents 1Document22 pagesCash and Cash Equivalents 1Mark GilNo ratings yet

- 03 Bank ReconciliationDocument5 pages03 Bank ReconciliationalteregoNo ratings yet

- Bank Reconciliation Journal Entries - Double Entry BookkeepingDocument9 pagesBank Reconciliation Journal Entries - Double Entry BookkeepingMizanur RahmanNo ratings yet

- CWTS1-USA-B-SAPE InfographicDocument1 pageCWTS1-USA-B-SAPE InfographiccyriljunaicamaranquezNo ratings yet

- Fabm2 QTR.2 Las 7.1Document10 pagesFabm2 QTR.2 Las 7.1Trunks KunNo ratings yet

- Chapter 5 Bank Reconciliation StatementDocument2 pagesChapter 5 Bank Reconciliation StatementDeveender Kaur JudgeNo ratings yet

- Receivable FinancingDocument34 pagesReceivable FinancingmaryzeenNo ratings yet

- Receivable Financing CH14 by LailaneDocument30 pagesReceivable Financing CH14 by LailaneEunice BernalNo ratings yet

- Module 8Document3 pagesModule 8Rainielle Sy DulatreNo ratings yet

- Bank Reconciliation StatementDocument12 pagesBank Reconciliation StatementMuhammad BilalNo ratings yet

- Chapter 3 Bank Recon Lecture StudentDocument5 pagesChapter 3 Bank Recon Lecture StudentAshlene CruzNo ratings yet

- Bank ReconciliationDocument3 pagesBank ReconciliationZejkeara ImperialNo ratings yet

- Journal Entries For Bank ReconciliationDocument2 pagesJournal Entries For Bank ReconciliationAira Mae Quinones OrendainNo ratings yet

- Bank ReconciliationDocument27 pagesBank Reconciliationnaruto uzumakiNo ratings yet

- Bank ReconciliationDocument23 pagesBank ReconciliationJohn Anjelo MoraldeNo ratings yet

- Bank Reconciliations - 1Document9 pagesBank Reconciliations - 1ZAKAYO NJONYNo ratings yet

- Receivable Financing: Pledge, Assignment, and FactoringDocument30 pagesReceivable Financing: Pledge, Assignment, and FactoringJoy UyNo ratings yet

- Aa21 Afa Chapter 01 EnglishDocument12 pagesAa21 Afa Chapter 01 EnglishnafeesNo ratings yet

- Fabm2 - 8.2Document15 pagesFabm2 - 8.2Kervin GuevaraNo ratings yet

- Chap 9 - Proof of Cash Fin Acct 1 - Barter Summary Team PDFDocument7 pagesChap 9 - Proof of Cash Fin Acct 1 - Barter Summary Team PDFCarl James Austria100% (1)

- Dictioformula ProblemsDocument42 pagesDictioformula ProblemsEza Joy ClaveriasNo ratings yet

- CH08 Bank ReconciliationDocument12 pagesCH08 Bank ReconciliationRose DionioNo ratings yet

- ABM FABM2 Q2 Wk3 LAS3Document11 pagesABM FABM2 Q2 Wk3 LAS3ayaNo ratings yet

- 05 Laboratory Exercise 1Document2 pages05 Laboratory Exercise 1Praisen JoyNo ratings yet

- Formulas in Business FinanceDocument4 pagesFormulas in Business FinancePraisen JoyNo ratings yet

- 07 Laboratory Exercise 1Document3 pages07 Laboratory Exercise 1Praisen JoyNo ratings yet

- 08 Quiz 1Document3 pages08 Quiz 1Praisen JoyNo ratings yet

- Fixedline and Broadband Services: Your Account Summary This Month'S ChargesDocument2 pagesFixedline and Broadband Services: Your Account Summary This Month'S ChargesMaximuzNo ratings yet

- Faqs On Internet Banking Services (Ibs) For NrisDocument2 pagesFaqs On Internet Banking Services (Ibs) For NrisABMNo ratings yet

- Marketing of Financial Services NMIMS AssignmentDocument4 pagesMarketing of Financial Services NMIMS AssignmentN. Karthik UdupaNo ratings yet

- Check-Out Procedures: B.Sc. (HHA) / 2 Year/ Checkout ProceduresDocument10 pagesCheck-Out Procedures: B.Sc. (HHA) / 2 Year/ Checkout ProceduresAryan BishtNo ratings yet

- Business Banking Price ListDocument15 pagesBusiness Banking Price ListSARFRAZ ALINo ratings yet

- Mastering Personal Credit and Personal FudningDocument15 pagesMastering Personal Credit and Personal FudningAli Tarafdar, QFOPNo ratings yet

- Lecture Sheet of Final Syllabus: Negotiable Instruments Act, 1881Document4 pagesLecture Sheet of Final Syllabus: Negotiable Instruments Act, 1881Eshthiak HossainNo ratings yet

- Niam Knoll - TransUnion Personal Credit Report - 20200802Document4 pagesNiam Knoll - TransUnion Personal Credit Report - 20200802Bruce WaynneNo ratings yet

- Individual Assignment - On - COMPANY - STRATEGIC - ANALYSIS.Document14 pagesIndividual Assignment - On - COMPANY - STRATEGIC - ANALYSIS.Adanech100% (1)

- First American Bank's Donald Roubitcheck, Chief Financial Officer - Completed TARP - Use of Capital Survey, Donald Roubitchek CFO July 24, 2009Document3 pagesFirst American Bank's Donald Roubitcheck, Chief Financial Officer - Completed TARP - Use of Capital Survey, Donald Roubitchek CFO July 24, 2009larry-612445No ratings yet

- Account Details and Transaction History: Mohd Salleh Bin AmboDocument2 pagesAccount Details and Transaction History: Mohd Salleh Bin AmboMohd Salleh AmboNo ratings yet

- Nilson Report Issue 1169Document12 pagesNilson Report Issue 1169John Mulder100% (1)

- Sob Select 30 12 2022Document2 pagesSob Select 30 12 2022nishan1187No ratings yet

- Canara Bank Project ReportDocument16 pagesCanara Bank Project Reportsagar m100% (1)

- Currency Seasonal Patterns Free EbookDocument21 pagesCurrency Seasonal Patterns Free Ebookkh267aziziNo ratings yet

- Weekly ReportDocument4 pagesWeekly ReportAiane_Reyes_5594No ratings yet

- Daftar Bank Yang Ada Di Wilayah PontianakDocument4 pagesDaftar Bank Yang Ada Di Wilayah PontianakWindia SariNo ratings yet

- Seminar Questions Set III A-2Document3 pagesSeminar Questions Set III A-2fanuel kijojiNo ratings yet

- FRM & VIGILANCE OF BANK POLICY J&K BankDocument37 pagesFRM & VIGILANCE OF BANK POLICY J&K BankAnshul BishtNo ratings yet

- Akong'a, Cynthia J - The Effect of Financial Risk Management On The Financial Performance of Commercial Banks in KenyaDocument57 pagesAkong'a, Cynthia J - The Effect of Financial Risk Management On The Financial Performance of Commercial Banks in KenyaEsobiebi ChristabelNo ratings yet

- Ch02-Cash Inflow OutFlowDocument45 pagesCh02-Cash Inflow OutFlowismat arteeNo ratings yet

- Moroz IlonaDocument1 pageMoroz IlonaСергей АлексеевичNo ratings yet

- Ch-2 FRONT OFFICE (ACCOUNTING)Document11 pagesCh-2 FRONT OFFICE (ACCOUNTING)DawaNo ratings yet

- Basu and Dutta Journal EntriesDocument7 pagesBasu and Dutta Journal EntriesAranya Haldar100% (2)

- Cambridge Ordinary LevelDocument12 pagesCambridge Ordinary LevelAlexNo ratings yet

- RamishDocument14 pagesRamishpradeep swatiNo ratings yet

- Updated - Note On NeobanksDocument38 pagesUpdated - Note On NeobanksAnirudh SoodNo ratings yet

- Chapter 2 AccountingDocument12 pagesChapter 2 Accountingmoon loverNo ratings yet

- 0151xxxxxxxx6295 - 2023 12 01Document6 pages0151xxxxxxxx6295 - 2023 12 01George GeranisNo ratings yet