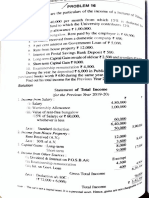

Sum On House Property

Sum On House Property

You might also like

- Webinar 6 and 7 Revision CGT and Tax Computation Indiv QuestionsDocument4 pagesWebinar 6 and 7 Revision CGT and Tax Computation Indiv QuestionsOlivia KhumaloNo ratings yet

- Cash Flow Statement Problems PDFDocument32 pagesCash Flow Statement Problems PDFnsrivastav181% (31)

- ABM Applied Economics Module 1 Differentiate Economics As Social Science and Applied Science in Terms of Nature and ScopeDocument37 pagesABM Applied Economics Module 1 Differentiate Economics As Social Science and Applied Science in Terms of Nature and Scopemara ellyn lacson100% (6)

- MNG4801 Assign 1 2015 FeedbackDocument6 pagesMNG4801 Assign 1 2015 FeedbackNadine0% (1)

- Maintenance, Repair and Operations Parts Inventory Management in The Era of Industry 4.0Document6 pagesMaintenance, Repair and Operations Parts Inventory Management in The Era of Industry 4.0Tiago Camargo AlvesNo ratings yet

- CHAPTER5 INCOME FROM HOUSE PROPERTY New2Document7 pagesCHAPTER5 INCOME FROM HOUSE PROPERTY New2SANJAY ShettyNo ratings yet

- Chapter 3 - LeveragesDocument9 pagesChapter 3 - LeveragesParth GargNo ratings yet

- Income Tax Volume 2 Answer KeyDocument137 pagesIncome Tax Volume 2 Answer KeyManish RajNo ratings yet

- INCOME FROM HOUSE PROPERTYcrDocument8 pagesINCOME FROM HOUSE PROPERTYcrShin VhanNo ratings yet

- Leverage QuestionsDocument8 pagesLeverage QuestionsMidhun George VargheseNo ratings yet

- Income From House Property: Solution To Assignment SolutionsDocument4 pagesIncome From House Property: Solution To Assignment SolutionsAsar QabeelNo ratings yet

- @ProCA - Inter Income Tax Book Vol 2 Solution May2022Document139 pages@ProCA - Inter Income Tax Book Vol 2 Solution May2022Indhuja MNo ratings yet

- Income Tax - VK SinghaniaDocument598 pagesIncome Tax - VK SinghaniaKartik67% (3)

- Capital Structure (1) Solved ProbDocument8 pagesCapital Structure (1) Solved Prob121733601011 MADENA KEERTHI PRIYA100% (1)

- Setoff and Carry ForwardDocument5 pagesSetoff and Carry ForwardSrinivas T. Raju100% (1)

- Income From House PropertyDocument26 pagesIncome From House PropertySuyash Patwa100% (1)

- Tax H.P CompilorDocument6 pagesTax H.P CompilorKaran GuptaNo ratings yet

- Income Tax Calculator FY 2022 23Document4 pagesIncome Tax Calculator FY 2022 23Vineet KumarNo ratings yet

- Budget 2Document2 pagesBudget 2qtmjw2tqx8No ratings yet

- CFS ProblemsDocument21 pagesCFS ProblemsNAVYA MITTAL 2224070No ratings yet

- BCom Business Taxation Income Tax and Sales Tax Numerical 2018Document5 pagesBCom Business Taxation Income Tax and Sales Tax Numerical 2018AHSAN LASHARINo ratings yet

- Sets Off and Carry Forward of LossesDocument12 pagesSets Off and Carry Forward of LossesRaghav BhardwajNo ratings yet

- Lab 2Document4 pagesLab 2Danica Jane RamosNo ratings yet

- Requirement No. 1 (20A1) : Acctax1 Problem 1 - Concept of Income and When TaxableDocument338 pagesRequirement No. 1 (20A1) : Acctax1 Problem 1 - Concept of Income and When TaxableRigine MorgadezNo ratings yet

- IT Assessment of Individuals IllustrationDocument5 pagesIT Assessment of Individuals Illustrationsyedfareed596No ratings yet

- Set Off and Carry Forward of LossesDocument23 pagesSet Off and Carry Forward of LossesKartikNo ratings yet

- ItDocument4 pagesItCharles RussellNo ratings yet

- Tax 2 Final Cheat Sheet 1.2Document2 pagesTax 2 Final Cheat Sheet 1.2HelloWorldNowNo ratings yet

- Computation of Total IncomeDocument2 pagesComputation of Total Income2154 taibakhatunNo ratings yet

- Problems On Total IncomeDocument12 pagesProblems On Total IncomedipakNo ratings yet

- Ws CmaDocument11 pagesWs CmaVRNo ratings yet

- BSL Assignment 03Document5 pagesBSL Assignment 03Akash KumarNo ratings yet

- 02 Edu91 FM Practice Sheets QuestionsDocument77 pages02 Edu91 FM Practice Sheets Questionsprince soniNo ratings yet

- DT CPS TEST 2 SolnDocument11 pagesDT CPS TEST 2 SolnMayank GoyalNo ratings yet

- Solved Past Papers Income Tax Numericals of ICMAP STAGE IV - (2003 TO 2015)Document45 pagesSolved Past Papers Income Tax Numericals of ICMAP STAGE IV - (2003 TO 2015)muneeb razaNo ratings yet

- Ratio Analysis Numericals Including Reverse RatiosDocument6 pagesRatio Analysis Numericals Including Reverse RatiosFunny ManNo ratings yet

- Provisional Taxsheet Mar 2020Document1 pageProvisional Taxsheet Mar 2020vivianNo ratings yet

- Cash Flow Statement-1Document20 pagesCash Flow Statement-1rajesh337masssNo ratings yet

- Income Tax Calculation For The Period 01/04/2021 To 07/07/2021Document4 pagesIncome Tax Calculation For The Period 01/04/2021 To 07/07/2021Srinath AllaNo ratings yet

- ABC Chap 9 SolmanDocument11 pagesABC Chap 9 SolmanKimberly ToraldeNo ratings yet

- F6mys 2016 Jun A Hybrid PDFDocument9 pagesF6mys 2016 Jun A Hybrid PDFsahrasaqsdNo ratings yet

- Levergae WsDocument6 pagesLevergae WsDisha Commerce AcademyNo ratings yet

- IT AssignmentDocument7 pagesIT AssignmentNipun AroraNo ratings yet

- IPCC Mock Test Taxation - Only Solution - 25.09.2018Document12 pagesIPCC Mock Test Taxation - Only Solution - 25.09.2018KaustubhNo ratings yet

- PEOBLEMS2Document3 pagesPEOBLEMS2Awesome AngelNo ratings yet

- Current Assets Noncurrent Assets Curre NT Liabilit Ies Noncurr Ent Liabilitie S Total Shareholder's EquityDocument3 pagesCurrent Assets Noncurrent Assets Curre NT Liabilit Ies Noncurr Ent Liabilitie S Total Shareholder's EquityVannesaNo ratings yet

- Accounting SolutionDocument3 pagesAccounting SolutionVannesaNo ratings yet

- A Practical Introduction To Australian Taxation Pages 301 To 325Document25 pagesA Practical Introduction To Australian Taxation Pages 301 To 325PuffleNo ratings yet

- 07 Activity AtanezDocument2 pages07 Activity AtanezSteff Atañez100% (1)

- Problems On House Property - AY 2020-21Document4 pagesProblems On House Property - AY 2020-21Adarsh PandeyNo ratings yet

- Sol - PTP 29 11 2018Document6 pagesSol - PTP 29 11 2018riyagoel12329dspsNo ratings yet

- AE 22 Activity 8Document2 pagesAE 22 Activity 8Venus PalmencoNo ratings yet

- Mahusay Bsa 315 Module 4 CaseletsDocument9 pagesMahusay Bsa 315 Module 4 CaseletsJeth MahusayNo ratings yet

- IT Detections From Gross Total Income Pt-1Document25 pagesIT Detections From Gross Total Income Pt-1syedfareed596100% (1)

- T11 Ans. 1Document1 pageT11 Ans. 1PUI TUNG CHONGNo ratings yet

- 12-Fall 2016 - BT - SADocument8 pages12-Fall 2016 - BT - SApabloescobar11yNo ratings yet

- Bacayo 07 Activity 1 EntrepDocument3 pagesBacayo 07 Activity 1 EntrepDavid GutierrezNo ratings yet

- 3.1 Workshop 7 Capital Structure 2021Document2 pages3.1 Workshop 7 Capital Structure 2021bobhamilton3489No ratings yet

- Qdoc - Tips LeverageDocument20 pagesQdoc - Tips LeverageHakim VersozaNo ratings yet

- Dream World CompanyDocument9 pagesDream World CompanyJC NicaveraNo ratings yet

- Joint Venture Account PracticalDocument15 pagesJoint Venture Account Practicalasmita23840No ratings yet

- Quiz 2 - Income Tax Concepts and ComplianceDocument3 pagesQuiz 2 - Income Tax Concepts and Compliancelc100% (1)

- Imp Ques With SynopsisDocument3 pagesImp Ques With SynopsisVaishnaviNo ratings yet

- Moot Proposition - State of KeralaDocument12 pagesMoot Proposition - State of KeralaVaishnaviNo ratings yet

- Filing of ReturnsDocument15 pagesFiling of ReturnsVaishnaviNo ratings yet

- Direct Tax - Likely QuestionsDocument4 pagesDirect Tax - Likely QuestionsVaishnaviNo ratings yet

- Offences and Penalties Income TaxDocument13 pagesOffences and Penalties Income TaxVaishnaviNo ratings yet

- Unit 3 - Other SourcesDocument15 pagesUnit 3 - Other SourcesVaishnaviNo ratings yet

- Unit 3 - Capital GainsDocument32 pagesUnit 3 - Capital GainsVaishnaviNo ratings yet

- Unit 6 - Appeals and RevisionsDocument24 pagesUnit 6 - Appeals and RevisionsVaishnaviNo ratings yet

- Unit 1 - Basic ConceptsDocument8 pagesUnit 1 - Basic ConceptsVaishnaviNo ratings yet

- I3 Marketing AspectDocument9 pagesI3 Marketing AspectJulliena BakersNo ratings yet

- Greyhound Fleet Manager: Mca Project ReportDocument4 pagesGreyhound Fleet Manager: Mca Project ReportShalu OjhaNo ratings yet

- Unit 4-L1Document14 pagesUnit 4-L1technical analysisNo ratings yet

- ETSE Zeiss True Position Bore Pattern 10-2 UpdateDocument29 pagesETSE Zeiss True Position Bore Pattern 10-2 UpdateJuan Posada GNo ratings yet

- Quiz Ch. 6&7 Statistics & FractionsDocument2 pagesQuiz Ch. 6&7 Statistics & FractionsAkbar Suhendi TeacherNo ratings yet

- Important Circular June 2019 ETE 115Document1 pageImportant Circular June 2019 ETE 115binalamitNo ratings yet

- Indian Institute of Materials Management: Graduate Diploma in Public Procurement Paper No.5Document3 pagesIndian Institute of Materials Management: Graduate Diploma in Public Procurement Paper No.5shivamdubey12No ratings yet

- LePage AdaptiveMultidimInteg JCompPhys78Document12 pagesLePage AdaptiveMultidimInteg JCompPhys78Tiến Đạt NguyễnNo ratings yet

- Financial AccountingDocument376 pagesFinancial AccountingMizalem Cantila50% (2)

- EntreDocument66 pagesEntrejashley_janeNo ratings yet

- University of KarachiDocument53 pagesUniversity of KarachiWaqasBakaliNo ratings yet

- BDA PresentationsDocument26 pagesBDA PresentationsTejaswiniNo ratings yet

- MPLUN-DSC User ManualDocument5 pagesMPLUN-DSC User ManualAccounts DepartmentNo ratings yet

- Assessment of CG in The Phil PDFDocument34 pagesAssessment of CG in The Phil PDFJoyce Kay AzucenaNo ratings yet

- Boq of Dire Dawa Project Final Price AdjustedDocument67 pagesBoq of Dire Dawa Project Final Price Adjustedbings1997 BiniamNo ratings yet

- DLL Cookery 9 Week 6Document2 pagesDLL Cookery 9 Week 6Negi SotneirrabNo ratings yet

- Psychological Science Modeling Scientific Literacy With DSM-5 Update Mark Krause, Daniel Corts Test BankDocument5 pagesPsychological Science Modeling Scientific Literacy With DSM-5 Update Mark Krause, Daniel Corts Test BanksaxNo ratings yet

- Spar Design of A Fokker D-VII - Aerospace Engineering BlogDocument8 pagesSpar Design of A Fokker D-VII - Aerospace Engineering Blogjohn mtz100% (1)

- The Proprietary Theory and The Entity Theory of Corporate Enterpr PDFDocument242 pagesThe Proprietary Theory and The Entity Theory of Corporate Enterpr PDFAnusha GowdaNo ratings yet

- Rkvy 14th FinDocument38 pagesRkvy 14th FinAfeef AyubNo ratings yet

- Death or Physical Injuries Inflicted Under Exceptional CircumstancesDocument7 pagesDeath or Physical Injuries Inflicted Under Exceptional CircumstancestimothymaderazoNo ratings yet

- Talisic Vs Atty. Rinen Feb. 12,2014Document3 pagesTalisic Vs Atty. Rinen Feb. 12,2014Katharina CantaNo ratings yet

- Compact Concealed Handgun Comparison Chart (Illustrated) - 2011Document10 pagesCompact Concealed Handgun Comparison Chart (Illustrated) - 2011KomodowaranNo ratings yet

- Walkathon Brochure - 2021 Trifold 2Document2 pagesWalkathon Brochure - 2021 Trifold 2api-208159640No ratings yet

- Drilling Bit DesignDocument14 pagesDrilling Bit DesignMajedur Rahman100% (1)

- PCB Design Course - Emtech FoundationDocument6 pagesPCB Design Course - Emtech FoundationAbhishek KumarNo ratings yet

- HLS PON FR12 TheNewConflictMgmt 102021 EdsDocument10 pagesHLS PON FR12 TheNewConflictMgmt 102021 Edskarishma PradhanNo ratings yet

Download as pdf or txt

You might also like

- Webinar 6 and 7 Revision CGT and Tax Computation Indiv QuestionsDocument4 pagesWebinar 6 and 7 Revision CGT and Tax Computation Indiv QuestionsOlivia KhumaloNo ratings yet

- Cash Flow Statement Problems PDFDocument32 pagesCash Flow Statement Problems PDFnsrivastav181% (31)

- ABM Applied Economics Module 1 Differentiate Economics As Social Science and Applied Science in Terms of Nature and ScopeDocument37 pagesABM Applied Economics Module 1 Differentiate Economics As Social Science and Applied Science in Terms of Nature and Scopemara ellyn lacson100% (6)

- MNG4801 Assign 1 2015 FeedbackDocument6 pagesMNG4801 Assign 1 2015 FeedbackNadine0% (1)

- Maintenance, Repair and Operations Parts Inventory Management in The Era of Industry 4.0Document6 pagesMaintenance, Repair and Operations Parts Inventory Management in The Era of Industry 4.0Tiago Camargo AlvesNo ratings yet

- CHAPTER5 INCOME FROM HOUSE PROPERTY New2Document7 pagesCHAPTER5 INCOME FROM HOUSE PROPERTY New2SANJAY ShettyNo ratings yet

- Chapter 3 - LeveragesDocument9 pagesChapter 3 - LeveragesParth GargNo ratings yet

- Income Tax Volume 2 Answer KeyDocument137 pagesIncome Tax Volume 2 Answer KeyManish RajNo ratings yet

- INCOME FROM HOUSE PROPERTYcrDocument8 pagesINCOME FROM HOUSE PROPERTYcrShin VhanNo ratings yet

- Leverage QuestionsDocument8 pagesLeverage QuestionsMidhun George VargheseNo ratings yet

- Income From House Property: Solution To Assignment SolutionsDocument4 pagesIncome From House Property: Solution To Assignment SolutionsAsar QabeelNo ratings yet

- @ProCA - Inter Income Tax Book Vol 2 Solution May2022Document139 pages@ProCA - Inter Income Tax Book Vol 2 Solution May2022Indhuja MNo ratings yet

- Income Tax - VK SinghaniaDocument598 pagesIncome Tax - VK SinghaniaKartik67% (3)

- Capital Structure (1) Solved ProbDocument8 pagesCapital Structure (1) Solved Prob121733601011 MADENA KEERTHI PRIYA100% (1)

- Setoff and Carry ForwardDocument5 pagesSetoff and Carry ForwardSrinivas T. Raju100% (1)

- Income From House PropertyDocument26 pagesIncome From House PropertySuyash Patwa100% (1)

- Tax H.P CompilorDocument6 pagesTax H.P CompilorKaran GuptaNo ratings yet

- Income Tax Calculator FY 2022 23Document4 pagesIncome Tax Calculator FY 2022 23Vineet KumarNo ratings yet

- Budget 2Document2 pagesBudget 2qtmjw2tqx8No ratings yet

- CFS ProblemsDocument21 pagesCFS ProblemsNAVYA MITTAL 2224070No ratings yet

- BCom Business Taxation Income Tax and Sales Tax Numerical 2018Document5 pagesBCom Business Taxation Income Tax and Sales Tax Numerical 2018AHSAN LASHARINo ratings yet

- Sets Off and Carry Forward of LossesDocument12 pagesSets Off and Carry Forward of LossesRaghav BhardwajNo ratings yet

- Lab 2Document4 pagesLab 2Danica Jane RamosNo ratings yet

- Requirement No. 1 (20A1) : Acctax1 Problem 1 - Concept of Income and When TaxableDocument338 pagesRequirement No. 1 (20A1) : Acctax1 Problem 1 - Concept of Income and When TaxableRigine MorgadezNo ratings yet

- IT Assessment of Individuals IllustrationDocument5 pagesIT Assessment of Individuals Illustrationsyedfareed596No ratings yet

- Set Off and Carry Forward of LossesDocument23 pagesSet Off and Carry Forward of LossesKartikNo ratings yet

- ItDocument4 pagesItCharles RussellNo ratings yet

- Tax 2 Final Cheat Sheet 1.2Document2 pagesTax 2 Final Cheat Sheet 1.2HelloWorldNowNo ratings yet

- Computation of Total IncomeDocument2 pagesComputation of Total Income2154 taibakhatunNo ratings yet

- Problems On Total IncomeDocument12 pagesProblems On Total IncomedipakNo ratings yet

- Ws CmaDocument11 pagesWs CmaVRNo ratings yet

- BSL Assignment 03Document5 pagesBSL Assignment 03Akash KumarNo ratings yet

- 02 Edu91 FM Practice Sheets QuestionsDocument77 pages02 Edu91 FM Practice Sheets Questionsprince soniNo ratings yet

- DT CPS TEST 2 SolnDocument11 pagesDT CPS TEST 2 SolnMayank GoyalNo ratings yet

- Solved Past Papers Income Tax Numericals of ICMAP STAGE IV - (2003 TO 2015)Document45 pagesSolved Past Papers Income Tax Numericals of ICMAP STAGE IV - (2003 TO 2015)muneeb razaNo ratings yet

- Ratio Analysis Numericals Including Reverse RatiosDocument6 pagesRatio Analysis Numericals Including Reverse RatiosFunny ManNo ratings yet

- Provisional Taxsheet Mar 2020Document1 pageProvisional Taxsheet Mar 2020vivianNo ratings yet

- Cash Flow Statement-1Document20 pagesCash Flow Statement-1rajesh337masssNo ratings yet

- Income Tax Calculation For The Period 01/04/2021 To 07/07/2021Document4 pagesIncome Tax Calculation For The Period 01/04/2021 To 07/07/2021Srinath AllaNo ratings yet

- ABC Chap 9 SolmanDocument11 pagesABC Chap 9 SolmanKimberly ToraldeNo ratings yet

- F6mys 2016 Jun A Hybrid PDFDocument9 pagesF6mys 2016 Jun A Hybrid PDFsahrasaqsdNo ratings yet

- Levergae WsDocument6 pagesLevergae WsDisha Commerce AcademyNo ratings yet

- IT AssignmentDocument7 pagesIT AssignmentNipun AroraNo ratings yet

- IPCC Mock Test Taxation - Only Solution - 25.09.2018Document12 pagesIPCC Mock Test Taxation - Only Solution - 25.09.2018KaustubhNo ratings yet

- PEOBLEMS2Document3 pagesPEOBLEMS2Awesome AngelNo ratings yet

- Current Assets Noncurrent Assets Curre NT Liabilit Ies Noncurr Ent Liabilitie S Total Shareholder's EquityDocument3 pagesCurrent Assets Noncurrent Assets Curre NT Liabilit Ies Noncurr Ent Liabilitie S Total Shareholder's EquityVannesaNo ratings yet

- Accounting SolutionDocument3 pagesAccounting SolutionVannesaNo ratings yet

- A Practical Introduction To Australian Taxation Pages 301 To 325Document25 pagesA Practical Introduction To Australian Taxation Pages 301 To 325PuffleNo ratings yet

- 07 Activity AtanezDocument2 pages07 Activity AtanezSteff Atañez100% (1)

- Problems On House Property - AY 2020-21Document4 pagesProblems On House Property - AY 2020-21Adarsh PandeyNo ratings yet

- Sol - PTP 29 11 2018Document6 pagesSol - PTP 29 11 2018riyagoel12329dspsNo ratings yet

- AE 22 Activity 8Document2 pagesAE 22 Activity 8Venus PalmencoNo ratings yet

- Mahusay Bsa 315 Module 4 CaseletsDocument9 pagesMahusay Bsa 315 Module 4 CaseletsJeth MahusayNo ratings yet

- IT Detections From Gross Total Income Pt-1Document25 pagesIT Detections From Gross Total Income Pt-1syedfareed596100% (1)

- T11 Ans. 1Document1 pageT11 Ans. 1PUI TUNG CHONGNo ratings yet

- 12-Fall 2016 - BT - SADocument8 pages12-Fall 2016 - BT - SApabloescobar11yNo ratings yet

- Bacayo 07 Activity 1 EntrepDocument3 pagesBacayo 07 Activity 1 EntrepDavid GutierrezNo ratings yet

- 3.1 Workshop 7 Capital Structure 2021Document2 pages3.1 Workshop 7 Capital Structure 2021bobhamilton3489No ratings yet

- Qdoc - Tips LeverageDocument20 pagesQdoc - Tips LeverageHakim VersozaNo ratings yet

- Dream World CompanyDocument9 pagesDream World CompanyJC NicaveraNo ratings yet

- Joint Venture Account PracticalDocument15 pagesJoint Venture Account Practicalasmita23840No ratings yet

- Quiz 2 - Income Tax Concepts and ComplianceDocument3 pagesQuiz 2 - Income Tax Concepts and Compliancelc100% (1)

- Imp Ques With SynopsisDocument3 pagesImp Ques With SynopsisVaishnaviNo ratings yet

- Moot Proposition - State of KeralaDocument12 pagesMoot Proposition - State of KeralaVaishnaviNo ratings yet

- Filing of ReturnsDocument15 pagesFiling of ReturnsVaishnaviNo ratings yet

- Direct Tax - Likely QuestionsDocument4 pagesDirect Tax - Likely QuestionsVaishnaviNo ratings yet

- Offences and Penalties Income TaxDocument13 pagesOffences and Penalties Income TaxVaishnaviNo ratings yet

- Unit 3 - Other SourcesDocument15 pagesUnit 3 - Other SourcesVaishnaviNo ratings yet

- Unit 3 - Capital GainsDocument32 pagesUnit 3 - Capital GainsVaishnaviNo ratings yet

- Unit 6 - Appeals and RevisionsDocument24 pagesUnit 6 - Appeals and RevisionsVaishnaviNo ratings yet

- Unit 1 - Basic ConceptsDocument8 pagesUnit 1 - Basic ConceptsVaishnaviNo ratings yet

- I3 Marketing AspectDocument9 pagesI3 Marketing AspectJulliena BakersNo ratings yet

- Greyhound Fleet Manager: Mca Project ReportDocument4 pagesGreyhound Fleet Manager: Mca Project ReportShalu OjhaNo ratings yet

- Unit 4-L1Document14 pagesUnit 4-L1technical analysisNo ratings yet

- ETSE Zeiss True Position Bore Pattern 10-2 UpdateDocument29 pagesETSE Zeiss True Position Bore Pattern 10-2 UpdateJuan Posada GNo ratings yet

- Quiz Ch. 6&7 Statistics & FractionsDocument2 pagesQuiz Ch. 6&7 Statistics & FractionsAkbar Suhendi TeacherNo ratings yet

- Important Circular June 2019 ETE 115Document1 pageImportant Circular June 2019 ETE 115binalamitNo ratings yet

- Indian Institute of Materials Management: Graduate Diploma in Public Procurement Paper No.5Document3 pagesIndian Institute of Materials Management: Graduate Diploma in Public Procurement Paper No.5shivamdubey12No ratings yet

- LePage AdaptiveMultidimInteg JCompPhys78Document12 pagesLePage AdaptiveMultidimInteg JCompPhys78Tiến Đạt NguyễnNo ratings yet

- Financial AccountingDocument376 pagesFinancial AccountingMizalem Cantila50% (2)

- EntreDocument66 pagesEntrejashley_janeNo ratings yet

- University of KarachiDocument53 pagesUniversity of KarachiWaqasBakaliNo ratings yet

- BDA PresentationsDocument26 pagesBDA PresentationsTejaswiniNo ratings yet

- MPLUN-DSC User ManualDocument5 pagesMPLUN-DSC User ManualAccounts DepartmentNo ratings yet

- Assessment of CG in The Phil PDFDocument34 pagesAssessment of CG in The Phil PDFJoyce Kay AzucenaNo ratings yet

- Boq of Dire Dawa Project Final Price AdjustedDocument67 pagesBoq of Dire Dawa Project Final Price Adjustedbings1997 BiniamNo ratings yet

- DLL Cookery 9 Week 6Document2 pagesDLL Cookery 9 Week 6Negi SotneirrabNo ratings yet

- Psychological Science Modeling Scientific Literacy With DSM-5 Update Mark Krause, Daniel Corts Test BankDocument5 pagesPsychological Science Modeling Scientific Literacy With DSM-5 Update Mark Krause, Daniel Corts Test BanksaxNo ratings yet

- Spar Design of A Fokker D-VII - Aerospace Engineering BlogDocument8 pagesSpar Design of A Fokker D-VII - Aerospace Engineering Blogjohn mtz100% (1)

- The Proprietary Theory and The Entity Theory of Corporate Enterpr PDFDocument242 pagesThe Proprietary Theory and The Entity Theory of Corporate Enterpr PDFAnusha GowdaNo ratings yet

- Rkvy 14th FinDocument38 pagesRkvy 14th FinAfeef AyubNo ratings yet

- Death or Physical Injuries Inflicted Under Exceptional CircumstancesDocument7 pagesDeath or Physical Injuries Inflicted Under Exceptional CircumstancestimothymaderazoNo ratings yet

- Talisic Vs Atty. Rinen Feb. 12,2014Document3 pagesTalisic Vs Atty. Rinen Feb. 12,2014Katharina CantaNo ratings yet

- Compact Concealed Handgun Comparison Chart (Illustrated) - 2011Document10 pagesCompact Concealed Handgun Comparison Chart (Illustrated) - 2011KomodowaranNo ratings yet

- Walkathon Brochure - 2021 Trifold 2Document2 pagesWalkathon Brochure - 2021 Trifold 2api-208159640No ratings yet

- Drilling Bit DesignDocument14 pagesDrilling Bit DesignMajedur Rahman100% (1)

- PCB Design Course - Emtech FoundationDocument6 pagesPCB Design Course - Emtech FoundationAbhishek KumarNo ratings yet

- HLS PON FR12 TheNewConflictMgmt 102021 EdsDocument10 pagesHLS PON FR12 TheNewConflictMgmt 102021 Edskarishma PradhanNo ratings yet