Download as docx, pdf, or txt

You might also like

- Madhuri Micro Economics Project Semester 1 1Document24 pagesMadhuri Micro Economics Project Semester 1 1Ananiya TiwariNo ratings yet

- SOcial CapitalDocument7 pagesSOcial Capitalmelicruz14No ratings yet

- On The Concept of Health Capital and The Demand For HealthDocument34 pagesOn The Concept of Health Capital and The Demand For Healthbrayanseixas7840No ratings yet

- Grossman On The Concept of Health Capital and The Demand For HealthDocument34 pagesGrossman On The Concept of Health Capital and The Demand For Healthvalentina-bnNo ratings yet

- Grossman M. (1972) PDFDocument33 pagesGrossman M. (1972) PDFMichele DalenaNo ratings yet

- Michael Grossman: The Journal of Political Economy, Vol. 80, No. 2. (Mar. - Apr., 1972), Pp. 223-255Document36 pagesMichael Grossman: The Journal of Political Economy, Vol. 80, No. 2. (Mar. - Apr., 1972), Pp. 223-255José Rodrigo GobiNo ratings yet

- Dishant Tiwari-National and State Welfare Schemes and Policies For Senior Citizens - A Critical Analysis.Document12 pagesDishant Tiwari-National and State Welfare Schemes and Policies For Senior Citizens - A Critical Analysis.joysoncgeorge2001No ratings yet

- Human Development - Meaning, Objectives and ComponentsDocument7 pagesHuman Development - Meaning, Objectives and ComponentsVijay Kulkarni50% (2)

- 1972 Grossman On The Concept of Health CapitalDocument33 pages1972 Grossman On The Concept of Health CapitalRaoul Guillen-RodriguezNo ratings yet

- 12 Economics - Human Capital Formation in India - Notes & Video LinkDocument7 pages12 Economics - Human Capital Formation in India - Notes & Video LinkA.Mohammed Aahil100% (1)

- HEALTH As Human CapitalDocument5 pagesHEALTH As Human Capitalhira hassanNo ratings yet

- Chapter 3-The DemandDocument11 pagesChapter 3-The DemandLalita A/P AnbarasenNo ratings yet

- 11th Economics Chapter 5 & 6Document34 pages11th Economics Chapter 5 & 6anupsorenNo ratings yet

- Health Economic GrowthDocument25 pagesHealth Economic GrowthCarmen Ulloa MéndezNo ratings yet

- Financing of Health Services and Alternative Methods: Some SuggestionsDocument19 pagesFinancing of Health Services and Alternative Methods: Some SuggestionsAbdelrhman M. ElhadidyNo ratings yet

- Wheevery Your R NeDocument4 pagesWheevery Your R NeTtius KCNo ratings yet

- Human Capital FormationDocument17 pagesHuman Capital FormationSimar SinghNo ratings yet

- Unit 7 Demand For Health Services: StructureDocument27 pagesUnit 7 Demand For Health Services: StructureThamilnila GowthamNo ratings yet

- Development: Short Essay On DevelopmentDocument10 pagesDevelopment: Short Essay On DevelopmentianNo ratings yet

- H C F I: Uman Apital Ormation IN NdiaDocument17 pagesH C F I: Uman Apital Ormation IN Ndiaramana3339No ratings yet

- Health and EducationDocument2 pagesHealth and EducationGreyie kimNo ratings yet

- Project Work: Conomic EvelpomentDocument8 pagesProject Work: Conomic Evelpomenttanmaya_purohitNo ratings yet

- Human Capital FormationDocument9 pagesHuman Capital Formationnakulshali1No ratings yet

- Human CapitalDocument14 pagesHuman CapitalTeddy AdaneNo ratings yet

- Health Eco ModuleDocument4 pagesHealth Eco ModuleRenaNo ratings yet

- Lec5-Health and DevelopmentDocument11 pagesLec5-Health and Developmentdouglaskiprono99No ratings yet

- Financial Wellness Enters The MainstreamDocument7 pagesFinancial Wellness Enters The Mainstreampink_677dNo ratings yet

- The Importance of Healthy Human Life On Economic DevelopmentDocument6 pagesThe Importance of Healthy Human Life On Economic DevelopmentRahul TambiNo ratings yet

- Tugas 2 Bahasa Inggris Niaga - 042274253Document2 pagesTugas 2 Bahasa Inggris Niaga - 042274253intan lioniNo ratings yet

- Chapter 1 Economic Growth and DevelopmentDocument14 pagesChapter 1 Economic Growth and DevelopmentHyuna KimNo ratings yet

- Chapter 25Document4 pagesChapter 25Nguyễn TâmNo ratings yet

- Financial Literacy: Challenges For Indian EconomyDocument14 pagesFinancial Literacy: Challenges For Indian EconomyJediGodNo ratings yet

- Economic DevelopmentDocument16 pagesEconomic DevelopmentNeha UjjwalNo ratings yet

- Political Activity-Erik 3pgDocument6 pagesPolitical Activity-Erik 3pgcecilia wanjiruNo ratings yet

- The Intergenerational Impact of Health On EconomicDocument11 pagesThe Intergenerational Impact of Health On EconomicgrowlingtoyouNo ratings yet

- Individual Elements of HealthDocument9 pagesIndividual Elements of HealthBianx SarmentaNo ratings yet

- Concept of Economic Development and Its MeasurementDocument27 pagesConcept of Economic Development and Its Measurementsuparswa88% (8)

- 3 Human Capital FormationDocument6 pages3 Human Capital FormationKumar SaurabhNo ratings yet

- HCF Q&a - NotesDocument8 pagesHCF Q&a - NotesRishiNo ratings yet

- CHAPTER1Document43 pagesCHAPTER1gaoiranallyNo ratings yet

- The Nexus of Economic Prosperity and Global HealthDocument22 pagesThe Nexus of Economic Prosperity and Global HealthMohib awanNo ratings yet

- Disease EpidemicsDocument7 pagesDisease EpidemicsTiffany NkhomaNo ratings yet

- Mosquitoe Repellent Plants Final 31 AugustDocument48 pagesMosquitoe Repellent Plants Final 31 AugustHomero SilvaNo ratings yet

- Birinci Temel Ekonomik Sorun Açlık-Asad ZamanDocument11 pagesBirinci Temel Ekonomik Sorun Açlık-Asad ZamanMücahit KumandaverenNo ratings yet

- Human Capital NcertDocument17 pagesHuman Capital NcertYuvika BishnoiNo ratings yet

- EJ868474Document11 pagesEJ868474Jude Michael CelestinoNo ratings yet

- New AnswersDocument8 pagesNew AnswersShreyash PednekarNo ratings yet

- 1 Health Economics With TLR - 2Document160 pages1 Health Economics With TLR - 2Angelo Otañes Gasatan100% (2)

- 203 AssimntDocument5 pages203 AssimntEmmaruiz jbNo ratings yet

- Financial Literacy: Prepared By: Phan, Vincent Thomas, Justin Wang, Huihua Xie, AngelaDocument21 pagesFinancial Literacy: Prepared By: Phan, Vincent Thomas, Justin Wang, Huihua Xie, AngelajosephNo ratings yet

- 004 Jun2023Document13 pages004 Jun2023Humani HumaniNo ratings yet

- Financial Literacy The Case of PolandDocument17 pagesFinancial Literacy The Case of PolandCarlo CalmaNo ratings yet

- Human CapitalDocument4 pagesHuman CapitalKumar DayanidhiNo ratings yet

- We ErentDocument7 pagesWe ErentFranz Soriano IINo ratings yet

- CST HealthcareDocument5 pagesCST Healthcareapi-640140770No ratings yet

- Social SustainabilityDocument18 pagesSocial SustainabilityVíctor Hugo Ramos ArcosNo ratings yet

- Topic 1 Health EconomicsDocument22 pagesTopic 1 Health Economicsedwin osiyelNo ratings yet

- Understanding Health Insurance Literacy A Literature ReviewDocument11 pagesUnderstanding Health Insurance Literacy A Literature Reviewromualdo quiambaoNo ratings yet

- Econ Dev ReviewerDocument20 pagesEcon Dev RevieweritsmiicharlesNo ratings yet

- This Model of Communication Is Composed of Eight VDocument1 pageThis Model of Communication Is Composed of Eight VBULUSAN, RAINA, G.No ratings yet

- ArtDocument1 pageArtBULUSAN, RAINA, G.No ratings yet

- CommunicationDocument2 pagesCommunicationBULUSAN, RAINA, G.No ratings yet

- Info VlogDocument2 pagesInfo VlogBULUSAN, RAINA, G.No ratings yet

- Positive Values Negative ValuesDocument2 pagesPositive Values Negative ValuesBULUSAN, RAINA, G.No ratings yet

- Solution 20 MarksDocument17 pagesSolution 20 Marksneha MistryNo ratings yet

- Reinventing GovernmentDocument296 pagesReinventing GovernmentPaul PurbaNo ratings yet

- Economic Performance of The Airline Industry: Key PointsDocument6 pagesEconomic Performance of The Airline Industry: Key PointsNguyenThanhDatNo ratings yet

- Using DXY For Confluence - September 17 2021Document9 pagesUsing DXY For Confluence - September 17 2021Robert PhamNo ratings yet

- KTT TELEX CODE PAYMENT (Signed)Document4 pagesKTT TELEX CODE PAYMENT (Signed)ChristianMNo ratings yet

- AS S1 Essay IG-AS SIADocument5 pagesAS S1 Essay IG-AS SIA2537771050No ratings yet

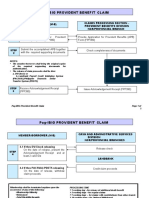

- Claims - Process StepsDocument2 pagesClaims - Process StepsImelda Villareal MontarilNo ratings yet

- 01 Financial Management An OverviewDocument27 pages01 Financial Management An OverviewstgcastillonesNo ratings yet

- Technopreneurship 101: Module 6: Business ModelDocument83 pagesTechnopreneurship 101: Module 6: Business ModelTOLENTINO, Julius Mark VirayNo ratings yet

- Upsell Page Template - Volume 1Document3 pagesUpsell Page Template - Volume 1AranyosiMártonNo ratings yet

- Account Name Account Number Transaction Date Year TIN Transaction AmountDocument6 pagesAccount Name Account Number Transaction Date Year TIN Transaction AmountSahara ReportersNo ratings yet

- Form PDF 710924950260719Document6 pagesForm PDF 710924950260719Parteek SharmaNo ratings yet

- Manajemen Operasi Week 2 PrsentasiDocument46 pagesManajemen Operasi Week 2 PrsentasiCICI SITI BARKAHNo ratings yet

- History of Development of Banking in PakistanDocument4 pagesHistory of Development of Banking in PakistanRamsha ZahidNo ratings yet

- Brealey - Principles of Corporate Finance - 13e - Chap17 - SMDocument14 pagesBrealey - Principles of Corporate Finance - 13e - Chap17 - SMShivamNo ratings yet

- ICC Guide To Responsible SourcingDocument16 pagesICC Guide To Responsible SourcingLoai100% (1)

- Medical Device Regulatory Requirements FDocument26 pagesMedical Device Regulatory Requirements Fmd edaNo ratings yet

- Sources of Finance For EntrepreneursDocument10 pagesSources of Finance For EntrepreneurskingshukbNo ratings yet

- Chap005 + Scm+Hrm+FinmanDocument100 pagesChap005 + Scm+Hrm+FinmanNguyễn NgânNo ratings yet

- Managerial Accounting 10th Edition Crosson Solutions ManualDocument36 pagesManagerial Accounting 10th Edition Crosson Solutions Manualmortgagechoric3yh7100% (30)

- 1.engineering Economics Cost Analysis PDFDocument11 pages1.engineering Economics Cost Analysis PDFAbdulHaseebArifNo ratings yet

- Digital Asset 2021 Outlook The Block ResearchDocument102 pagesDigital Asset 2021 Outlook The Block ResearchChen LiangNo ratings yet

- Home Office and Branch AccountingDocument27 pagesHome Office and Branch AccountingKRABBYPATTY PHNo ratings yet

- Energy Economics Schwarz-2018Document433 pagesEnergy Economics Schwarz-2018Mirwanto Sidabutar100% (1)

- 0x en UsdDocument1 page0x en Usdebaywin2311No ratings yet

- In The Name of Allah The Merciful Holding A Commercial Partnership at Maandeeq Poultry FarmDocument3 pagesIn The Name of Allah The Merciful Holding A Commercial Partnership at Maandeeq Poultry FarmWandaNo ratings yet

- Case 1 New Signal Cable CompanyDocument6 pagesCase 1 New Signal Cable Companymilk teaNo ratings yet

- Customer Statement of Acct Promasidor f12Document59 pagesCustomer Statement of Acct Promasidor f12adiriobinna1532No ratings yet

- Giro Form FinalDocument2 pagesGiro Form FinalJulius Putra Tanu SetiajiNo ratings yet

- GST Refund 26102015 NewDocument30 pagesGST Refund 26102015 NewNikhil SinghalNo ratings yet