Ifm Sorular 1

Ifm Sorular 1

You might also like

- Fundamentals of Futures and Options Markets 8th Edition Hull Solutions ManualDocument25 pagesFundamentals of Futures and Options Markets 8th Edition Hull Solutions ManualBeckySmithnxro98% (65)

- 40 Transactions With Their Journal Entries, Ledger, Trial Balanc - MeritnationDocument12 pages40 Transactions With Their Journal Entries, Ledger, Trial Balanc - MeritnationAbhishek Verma53% (126)

- Kelani Vs ACLDocument39 pagesKelani Vs ACLSasindu GimhanNo ratings yet

- Accelerator PPT FinalDocument41 pagesAccelerator PPT FinalnavdeepNo ratings yet

- Chap07 Ques MBF14eDocument4 pagesChap07 Ques MBF14eÂn TrầnNo ratings yet

- Chapter 6 - Hedging Foreign Exchange RiskDocument66 pagesChapter 6 - Hedging Foreign Exchange RiskHay JirenyaaNo ratings yet

- Tutorial 1 AnswersDocument3 pagesTutorial 1 AnswersAmeer FulatNo ratings yet

- Futures Trading Strategies: Enter and Exit the Market Like a Pro with Proven and Powerful Techniques For ProfitsFrom EverandFutures Trading Strategies: Enter and Exit the Market Like a Pro with Proven and Powerful Techniques For ProfitsRating: 1 out of 5 stars1/5 (1)

- Engineering Economy QuestionsDocument134 pagesEngineering Economy QuestionsJE Genobili100% (4)

- Gitman-Working Capital & Current AssetDocument64 pagesGitman-Working Capital & Current AssetSugim Winata EinsteinNo ratings yet

- Example - 2: A Bulldozer, Which Has A Service Life of 10 Years, Can Be PurchasedDocument4 pagesExample - 2: A Bulldozer, Which Has A Service Life of 10 Years, Can Be PurchasedNNo ratings yet

- FIN 4604 Sample Questions IIDocument25 pagesFIN 4604 Sample Questions IIEvelyn-Jiewei LiNo ratings yet

- Eiteman 178963 Im05Document7 pagesEiteman 178963 Im05Jane TitoNo ratings yet

- Fundamentals of Multinational Finance 3rd Edition Moffett Solutions ManualDocument4 pagesFundamentals of Multinational Finance 3rd Edition Moffett Solutions Manualkhuyenjohncqn100% (22)

- Fundamentals of Multinational Finance 3Rd Edition Moffett Solutions Manual Full Chapter PDFDocument25 pagesFundamentals of Multinational Finance 3Rd Edition Moffett Solutions Manual Full Chapter PDFdanielaidan4rf7100% (13)

- Solutions Chapters 10 & 11 Transactions and Economic ExposureDocument46 pagesSolutions Chapters 10 & 11 Transactions and Economic ExposureJoão Côrte-Real Rodrigues50% (2)

- Quiz Thị Trường Tài Chính Phái SinhDocument25 pagesQuiz Thị Trường Tài Chính Phái SinhNguyễn Thế BảoNo ratings yet

- Chapter 2 MNCsDocument37 pagesChapter 2 MNCsPhúc LêNo ratings yet

- International Financial Management Canadian Canadian 3Rd Edition Brean Test Bank Full Chapter PDFDocument41 pagesInternational Financial Management Canadian Canadian 3Rd Edition Brean Test Bank Full Chapter PDFPatriciaSimonrdio100% (14)

- Forward and Futures ContractsDocument29 pagesForward and Futures ContractsMaulik ShahNo ratings yet

- Currency DerivativesDocument28 pagesCurrency DerivativesChetan Patel100% (1)

- MD 5Document18 pagesMD 5adityaraaviNo ratings yet

- Exchange Rate Derivatives: South-Western/Thomson Learning © 2006Document30 pagesExchange Rate Derivatives: South-Western/Thomson Learning © 2006Adi PhasaNo ratings yet

- Chapter 8Document20 pagesChapter 8Ersin AnatacaNo ratings yet

- 02 Lecture21Document29 pages02 Lecture21Ashi GargNo ratings yet

- Homework 6Document4 pagesHomework 6Chang Chun-MinNo ratings yet

- Practice Midterm Bus331 SpringDocument3 pagesPractice Midterm Bus331 SpringJavan OdephNo ratings yet

- Foreign Currency Derivatives and Swaps: QuestionsDocument6 pagesForeign Currency Derivatives and Swaps: QuestionsCarl AzizNo ratings yet

- Preguntas y Respuestas de Los Parciales de FinanzasDocument3 pagesPreguntas y Respuestas de Los Parciales de FinanzasJaime A. LópezNo ratings yet

- FMPMC 411: Course Learning OutcomesDocument8 pagesFMPMC 411: Course Learning OutcomesAliah de GuzmanNo ratings yet

- Dwnload Full Options Futures and Other Derivatives 8th Edition Hull Test Bank PDFDocument35 pagesDwnload Full Options Futures and Other Derivatives 8th Edition Hull Test Bank PDFwhalemanfrauleinshlwvz100% (13)

- Mid Term - IIIDocument2 pagesMid Term - IIIvasanthbabu26No ratings yet

- Currency Derivatives: South-Western/Thomson Learning © 2006Document26 pagesCurrency Derivatives: South-Western/Thomson Learning © 2006Harish Chowdary TummalaNo ratings yet

- International Financial Management: by Jeff MaduraDocument48 pagesInternational Financial Management: by Jeff MaduraBe Like ComsianNo ratings yet

- CUHK FINA4110 Assignment2Document5 pagesCUHK FINA4110 Assignment2MOON TVNo ratings yet

- Financial Institutions Management - Chap024Document20 pagesFinancial Institutions Management - Chap024Wendy YipNo ratings yet

- Currency Future and OptionsDocument60 pagesCurrency Future and Optionspanicker_maheshNo ratings yet

- Chapter 5Document4 pagesChapter 5vandung19100% (1)

- Solutions Chapters 10 & 11 Transactions and Economic ExposureDocument46 pagesSolutions Chapters 10 & 11 Transactions and Economic Exposurerakhiitsme83% (6)

- Chapter 13 AnswersDocument5 pagesChapter 13 Answersvandung19No ratings yet

- Managing Foreign Exchange Risk: International Service CentreDocument8 pagesManaging Foreign Exchange Risk: International Service CentrenadeenaNo ratings yet

- Sample MidTerm Multiple Choice Spring 2018Document3 pagesSample MidTerm Multiple Choice Spring 2018Barbie LCNo ratings yet

- Task-1 Explain With Suitable Examples, Hedging in Forward Market. Meaning of HedgingDocument6 pagesTask-1 Explain With Suitable Examples, Hedging in Forward Market. Meaning of HedgingAnita ThakurNo ratings yet

- Derivative MarketsDocument4 pagesDerivative MarketsMorelate KupfurwaNo ratings yet

- Chapter 7 Futures and Options On Foreign Exchange Suggested Answers and Solutions To End-Of-Chapter Questions and ProblemsDocument12 pagesChapter 7 Futures and Options On Foreign Exchange Suggested Answers and Solutions To End-Of-Chapter Questions and ProblemsnaveenNo ratings yet

- 7Document86 pages7mg199224No ratings yet

- International Financial Management 5Document53 pagesInternational Financial Management 5胡依然100% (1)

- Money Market HedgeingDocument19 pagesMoney Market HedgeingHussain khawajaNo ratings yet

- Derivatives and RMDocument35 pagesDerivatives and RMMichael WardNo ratings yet

- FINS 3616 Tutorial Questions-Week 6-AnswersDocument7 pagesFINS 3616 Tutorial Questions-Week 6-AnswersOscarHigson-SpenceNo ratings yet

- Bonds and DerivativesDocument149 pagesBonds and DerivativesLinh LinhNo ratings yet

- LNIntlFin 4Document14 pagesLNIntlFin 4Wina WinaNo ratings yet

- Srrmra Final Master MCQDocument18 pagesSrrmra Final Master MCQTwinkle ChettriNo ratings yet

- Problem SolutionsDocument4 pagesProblem SolutionsParas JangirNo ratings yet

- Functions of Euro Currency Markets. 1.cheap Resource of Working CapitalDocument5 pagesFunctions of Euro Currency Markets. 1.cheap Resource of Working CapitalzacknowledgementNo ratings yet

- FINS 3616 Tutorial Questions-Week 4Document6 pagesFINS 3616 Tutorial Questions-Week 4Alex WuNo ratings yet

- Unit 3 - Lò Khánh Huyền - 2114410073Document14 pagesUnit 3 - Lò Khánh Huyền - 2114410073K60 LÒ KHÁNH HUYỀNNo ratings yet

- F3 Chapter 9Document42 pagesF3 Chapter 9Ali ShahnawazNo ratings yet

- International Financial Management PgapteDocument25 pagesInternational Financial Management PgapterameshmbaNo ratings yet

- Summary of Philip J. Romero & Tucker Balch's What Hedge Funds Really DoFrom EverandSummary of Philip J. Romero & Tucker Balch's What Hedge Funds Really DoNo ratings yet

- 801fea8a-e4a9-4105-8499-18b1dca26120Document3 pages801fea8a-e4a9-4105-8499-18b1dca26120Mustafa TotanNo ratings yet

- 4Document4 pages4Mustafa TotanNo ratings yet

- A) Reconciling In-Consistent Data Can Require A Sig - Nificant Amount of Time and MoneyDocument11 pagesA) Reconciling In-Consistent Data Can Require A Sig - Nificant Amount of Time and MoneyMustafa TotanNo ratings yet

- ÖrnekSoru IFM MidtermDocument5 pagesÖrnekSoru IFM MidtermMustafa TotanNo ratings yet

- Adv. Accounting. Business Comb. MCQDocument13 pagesAdv. Accounting. Business Comb. MCQalmira garciaNo ratings yet

- Bus Com Acq Date IllustrationDocument1 pageBus Com Acq Date IllustrationJhona May Golilao QuiamcoNo ratings yet

- Case2.Bill MillerDocument3 pagesCase2.Bill Millercalvin100% (1)

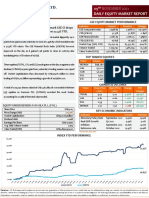

- Daily Equity Market Report - 09.11.2021Document1 pageDaily Equity Market Report - 09.11.2021Fuaad DodooNo ratings yet

- Income Tax BasicsDocument20 pagesIncome Tax BasicsShivajee SNo ratings yet

- Foreign Investment Act RA 7042 As Amended by RA 8179 RA 11647Document2 pagesForeign Investment Act RA 7042 As Amended by RA 8179 RA 11647devillaleizel12No ratings yet

- Economic Value AddedDocument4 pagesEconomic Value AddedsinghdamanNo ratings yet

- 380 FinalDocument15 pages380 Finalm_ihamNo ratings yet

- Alternative Sources of FinanceDocument8 pagesAlternative Sources of FinancediahNo ratings yet

- Engro CorDocument28 pagesEngro CorAbNo ratings yet

- Business Environment: ApprovedDocument1 pageBusiness Environment: ApprovedRitaSethiNo ratings yet

- Rek Koran BriDocument4 pagesRek Koran BriHaikal IdrisNo ratings yet

- UNIT 1 A Basics of Income TaxDocument43 pagesUNIT 1 A Basics of Income TaxWinsomeboi HoodlegendNo ratings yet

- Akash Eco PRJCTDocument15 pagesAkash Eco PRJCTLogan DavisNo ratings yet

- EE4209 - Lecture 3 - Economic and Financial Evaluation of Energy Sector ProjectsDocument20 pagesEE4209 - Lecture 3 - Economic and Financial Evaluation of Energy Sector ProjectsVindula LakshaniNo ratings yet

- To Study Credit Appraisal in Home Loan CONTENTDocument57 pagesTo Study Credit Appraisal in Home Loan CONTENTSwapnil BhagatNo ratings yet

- GCMMF Balance Sheet 1994 To 2009Document37 pagesGCMMF Balance Sheet 1994 To 2009Tapankhamar100% (1)

- Problem 4: Multiple Choice - ComputationalDocument5 pagesProblem 4: Multiple Choice - ComputationalKATHRYN CLAUDETTE RESENTENo ratings yet

- U.S.basel .III .Final .Rule .Visual - MemoDocument79 pagesU.S.basel .III .Final .Rule .Visual - Memoswapnit9995No ratings yet

- Activa InsuranceDocument1 pageActiva Insuranceyash shahNo ratings yet

- !fusion Tax - CompleteDocument3 pages!fusion Tax - Completewaste wasteNo ratings yet

- Accounts Payable Turnover Ratio Definition - InvestopediaDocument4 pagesAccounts Payable Turnover Ratio Definition - InvestopediaBob KaneNo ratings yet

- Tax Invoice: Amount in Words: Forty Three Thousand One Hundred Twenty Five Saudi Riyal OnlyDocument6 pagesTax Invoice: Amount in Words: Forty Three Thousand One Hundred Twenty Five Saudi Riyal Onlyabod7abobNo ratings yet

- SSSForm ADA EnrollmentDocument2 pagesSSSForm ADA EnrollmentJohnbree BreeNo ratings yet

Download as pdf or txt

You might also like

- Fundamentals of Futures and Options Markets 8th Edition Hull Solutions ManualDocument25 pagesFundamentals of Futures and Options Markets 8th Edition Hull Solutions ManualBeckySmithnxro98% (65)

- 40 Transactions With Their Journal Entries, Ledger, Trial Balanc - MeritnationDocument12 pages40 Transactions With Their Journal Entries, Ledger, Trial Balanc - MeritnationAbhishek Verma53% (126)

- Kelani Vs ACLDocument39 pagesKelani Vs ACLSasindu GimhanNo ratings yet

- Accelerator PPT FinalDocument41 pagesAccelerator PPT FinalnavdeepNo ratings yet

- Chap07 Ques MBF14eDocument4 pagesChap07 Ques MBF14eÂn TrầnNo ratings yet

- Chapter 6 - Hedging Foreign Exchange RiskDocument66 pagesChapter 6 - Hedging Foreign Exchange RiskHay JirenyaaNo ratings yet

- Tutorial 1 AnswersDocument3 pagesTutorial 1 AnswersAmeer FulatNo ratings yet

- Futures Trading Strategies: Enter and Exit the Market Like a Pro with Proven and Powerful Techniques For ProfitsFrom EverandFutures Trading Strategies: Enter and Exit the Market Like a Pro with Proven and Powerful Techniques For ProfitsRating: 1 out of 5 stars1/5 (1)

- Engineering Economy QuestionsDocument134 pagesEngineering Economy QuestionsJE Genobili100% (4)

- Gitman-Working Capital & Current AssetDocument64 pagesGitman-Working Capital & Current AssetSugim Winata EinsteinNo ratings yet

- Example - 2: A Bulldozer, Which Has A Service Life of 10 Years, Can Be PurchasedDocument4 pagesExample - 2: A Bulldozer, Which Has A Service Life of 10 Years, Can Be PurchasedNNo ratings yet

- FIN 4604 Sample Questions IIDocument25 pagesFIN 4604 Sample Questions IIEvelyn-Jiewei LiNo ratings yet

- Eiteman 178963 Im05Document7 pagesEiteman 178963 Im05Jane TitoNo ratings yet

- Fundamentals of Multinational Finance 3rd Edition Moffett Solutions ManualDocument4 pagesFundamentals of Multinational Finance 3rd Edition Moffett Solutions Manualkhuyenjohncqn100% (22)

- Fundamentals of Multinational Finance 3Rd Edition Moffett Solutions Manual Full Chapter PDFDocument25 pagesFundamentals of Multinational Finance 3Rd Edition Moffett Solutions Manual Full Chapter PDFdanielaidan4rf7100% (13)

- Solutions Chapters 10 & 11 Transactions and Economic ExposureDocument46 pagesSolutions Chapters 10 & 11 Transactions and Economic ExposureJoão Côrte-Real Rodrigues50% (2)

- Quiz Thị Trường Tài Chính Phái SinhDocument25 pagesQuiz Thị Trường Tài Chính Phái SinhNguyễn Thế BảoNo ratings yet

- Chapter 2 MNCsDocument37 pagesChapter 2 MNCsPhúc LêNo ratings yet

- International Financial Management Canadian Canadian 3Rd Edition Brean Test Bank Full Chapter PDFDocument41 pagesInternational Financial Management Canadian Canadian 3Rd Edition Brean Test Bank Full Chapter PDFPatriciaSimonrdio100% (14)

- Forward and Futures ContractsDocument29 pagesForward and Futures ContractsMaulik ShahNo ratings yet

- Currency DerivativesDocument28 pagesCurrency DerivativesChetan Patel100% (1)

- MD 5Document18 pagesMD 5adityaraaviNo ratings yet

- Exchange Rate Derivatives: South-Western/Thomson Learning © 2006Document30 pagesExchange Rate Derivatives: South-Western/Thomson Learning © 2006Adi PhasaNo ratings yet

- Chapter 8Document20 pagesChapter 8Ersin AnatacaNo ratings yet

- 02 Lecture21Document29 pages02 Lecture21Ashi GargNo ratings yet

- Homework 6Document4 pagesHomework 6Chang Chun-MinNo ratings yet

- Practice Midterm Bus331 SpringDocument3 pagesPractice Midterm Bus331 SpringJavan OdephNo ratings yet

- Foreign Currency Derivatives and Swaps: QuestionsDocument6 pagesForeign Currency Derivatives and Swaps: QuestionsCarl AzizNo ratings yet

- Preguntas y Respuestas de Los Parciales de FinanzasDocument3 pagesPreguntas y Respuestas de Los Parciales de FinanzasJaime A. LópezNo ratings yet

- FMPMC 411: Course Learning OutcomesDocument8 pagesFMPMC 411: Course Learning OutcomesAliah de GuzmanNo ratings yet

- Dwnload Full Options Futures and Other Derivatives 8th Edition Hull Test Bank PDFDocument35 pagesDwnload Full Options Futures and Other Derivatives 8th Edition Hull Test Bank PDFwhalemanfrauleinshlwvz100% (13)

- Mid Term - IIIDocument2 pagesMid Term - IIIvasanthbabu26No ratings yet

- Currency Derivatives: South-Western/Thomson Learning © 2006Document26 pagesCurrency Derivatives: South-Western/Thomson Learning © 2006Harish Chowdary TummalaNo ratings yet

- International Financial Management: by Jeff MaduraDocument48 pagesInternational Financial Management: by Jeff MaduraBe Like ComsianNo ratings yet

- CUHK FINA4110 Assignment2Document5 pagesCUHK FINA4110 Assignment2MOON TVNo ratings yet

- Financial Institutions Management - Chap024Document20 pagesFinancial Institutions Management - Chap024Wendy YipNo ratings yet

- Currency Future and OptionsDocument60 pagesCurrency Future and Optionspanicker_maheshNo ratings yet

- Chapter 5Document4 pagesChapter 5vandung19100% (1)

- Solutions Chapters 10 & 11 Transactions and Economic ExposureDocument46 pagesSolutions Chapters 10 & 11 Transactions and Economic Exposurerakhiitsme83% (6)

- Chapter 13 AnswersDocument5 pagesChapter 13 Answersvandung19No ratings yet

- Managing Foreign Exchange Risk: International Service CentreDocument8 pagesManaging Foreign Exchange Risk: International Service CentrenadeenaNo ratings yet

- Sample MidTerm Multiple Choice Spring 2018Document3 pagesSample MidTerm Multiple Choice Spring 2018Barbie LCNo ratings yet

- Task-1 Explain With Suitable Examples, Hedging in Forward Market. Meaning of HedgingDocument6 pagesTask-1 Explain With Suitable Examples, Hedging in Forward Market. Meaning of HedgingAnita ThakurNo ratings yet

- Derivative MarketsDocument4 pagesDerivative MarketsMorelate KupfurwaNo ratings yet

- Chapter 7 Futures and Options On Foreign Exchange Suggested Answers and Solutions To End-Of-Chapter Questions and ProblemsDocument12 pagesChapter 7 Futures and Options On Foreign Exchange Suggested Answers and Solutions To End-Of-Chapter Questions and ProblemsnaveenNo ratings yet

- 7Document86 pages7mg199224No ratings yet

- International Financial Management 5Document53 pagesInternational Financial Management 5胡依然100% (1)

- Money Market HedgeingDocument19 pagesMoney Market HedgeingHussain khawajaNo ratings yet

- Derivatives and RMDocument35 pagesDerivatives and RMMichael WardNo ratings yet

- FINS 3616 Tutorial Questions-Week 6-AnswersDocument7 pagesFINS 3616 Tutorial Questions-Week 6-AnswersOscarHigson-SpenceNo ratings yet

- Bonds and DerivativesDocument149 pagesBonds and DerivativesLinh LinhNo ratings yet

- LNIntlFin 4Document14 pagesLNIntlFin 4Wina WinaNo ratings yet

- Srrmra Final Master MCQDocument18 pagesSrrmra Final Master MCQTwinkle ChettriNo ratings yet

- Problem SolutionsDocument4 pagesProblem SolutionsParas JangirNo ratings yet

- Functions of Euro Currency Markets. 1.cheap Resource of Working CapitalDocument5 pagesFunctions of Euro Currency Markets. 1.cheap Resource of Working CapitalzacknowledgementNo ratings yet

- FINS 3616 Tutorial Questions-Week 4Document6 pagesFINS 3616 Tutorial Questions-Week 4Alex WuNo ratings yet

- Unit 3 - Lò Khánh Huyền - 2114410073Document14 pagesUnit 3 - Lò Khánh Huyền - 2114410073K60 LÒ KHÁNH HUYỀNNo ratings yet

- F3 Chapter 9Document42 pagesF3 Chapter 9Ali ShahnawazNo ratings yet

- International Financial Management PgapteDocument25 pagesInternational Financial Management PgapterameshmbaNo ratings yet

- Summary of Philip J. Romero & Tucker Balch's What Hedge Funds Really DoFrom EverandSummary of Philip J. Romero & Tucker Balch's What Hedge Funds Really DoNo ratings yet

- 801fea8a-e4a9-4105-8499-18b1dca26120Document3 pages801fea8a-e4a9-4105-8499-18b1dca26120Mustafa TotanNo ratings yet

- 4Document4 pages4Mustafa TotanNo ratings yet

- A) Reconciling In-Consistent Data Can Require A Sig - Nificant Amount of Time and MoneyDocument11 pagesA) Reconciling In-Consistent Data Can Require A Sig - Nificant Amount of Time and MoneyMustafa TotanNo ratings yet

- ÖrnekSoru IFM MidtermDocument5 pagesÖrnekSoru IFM MidtermMustafa TotanNo ratings yet

- Adv. Accounting. Business Comb. MCQDocument13 pagesAdv. Accounting. Business Comb. MCQalmira garciaNo ratings yet

- Bus Com Acq Date IllustrationDocument1 pageBus Com Acq Date IllustrationJhona May Golilao QuiamcoNo ratings yet

- Case2.Bill MillerDocument3 pagesCase2.Bill Millercalvin100% (1)

- Daily Equity Market Report - 09.11.2021Document1 pageDaily Equity Market Report - 09.11.2021Fuaad DodooNo ratings yet

- Income Tax BasicsDocument20 pagesIncome Tax BasicsShivajee SNo ratings yet

- Foreign Investment Act RA 7042 As Amended by RA 8179 RA 11647Document2 pagesForeign Investment Act RA 7042 As Amended by RA 8179 RA 11647devillaleizel12No ratings yet

- Economic Value AddedDocument4 pagesEconomic Value AddedsinghdamanNo ratings yet

- 380 FinalDocument15 pages380 Finalm_ihamNo ratings yet

- Alternative Sources of FinanceDocument8 pagesAlternative Sources of FinancediahNo ratings yet

- Engro CorDocument28 pagesEngro CorAbNo ratings yet

- Business Environment: ApprovedDocument1 pageBusiness Environment: ApprovedRitaSethiNo ratings yet

- Rek Koran BriDocument4 pagesRek Koran BriHaikal IdrisNo ratings yet

- UNIT 1 A Basics of Income TaxDocument43 pagesUNIT 1 A Basics of Income TaxWinsomeboi HoodlegendNo ratings yet

- Akash Eco PRJCTDocument15 pagesAkash Eco PRJCTLogan DavisNo ratings yet

- EE4209 - Lecture 3 - Economic and Financial Evaluation of Energy Sector ProjectsDocument20 pagesEE4209 - Lecture 3 - Economic and Financial Evaluation of Energy Sector ProjectsVindula LakshaniNo ratings yet

- To Study Credit Appraisal in Home Loan CONTENTDocument57 pagesTo Study Credit Appraisal in Home Loan CONTENTSwapnil BhagatNo ratings yet

- GCMMF Balance Sheet 1994 To 2009Document37 pagesGCMMF Balance Sheet 1994 To 2009Tapankhamar100% (1)

- Problem 4: Multiple Choice - ComputationalDocument5 pagesProblem 4: Multiple Choice - ComputationalKATHRYN CLAUDETTE RESENTENo ratings yet

- U.S.basel .III .Final .Rule .Visual - MemoDocument79 pagesU.S.basel .III .Final .Rule .Visual - Memoswapnit9995No ratings yet

- Activa InsuranceDocument1 pageActiva Insuranceyash shahNo ratings yet

- !fusion Tax - CompleteDocument3 pages!fusion Tax - Completewaste wasteNo ratings yet

- Accounts Payable Turnover Ratio Definition - InvestopediaDocument4 pagesAccounts Payable Turnover Ratio Definition - InvestopediaBob KaneNo ratings yet

- Tax Invoice: Amount in Words: Forty Three Thousand One Hundred Twenty Five Saudi Riyal OnlyDocument6 pagesTax Invoice: Amount in Words: Forty Three Thousand One Hundred Twenty Five Saudi Riyal Onlyabod7abobNo ratings yet

- SSSForm ADA EnrollmentDocument2 pagesSSSForm ADA EnrollmentJohnbree BreeNo ratings yet