Download as docx, pdf, or txt

You might also like

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- EvalsDocument11 pagesEvalsPaul Adriel Balmes50% (2)

- Illustration 1: Illustration 4Document2 pagesIllustration 1: Illustration 4Allessa FrezaNo ratings yet

- ASSET 2019 Mock Boards - FARDocument7 pagesASSET 2019 Mock Boards - FARKenneth Christian WilburNo ratings yet

- Current LiabilitiesDocument3 pagesCurrent LiabilitiesAhlaya Lyrica Cadence SadoresNo ratings yet

- Prelim Exam - Intermediate AccountingDocument4 pagesPrelim Exam - Intermediate AccountingLea Gabrielle Fariola0% (1)

- DocumentDocument8 pagesDocumentShaneNo ratings yet

- Module 2Document28 pagesModule 2Jiane SanicoNo ratings yet

- First Evaluation Examination Practical Accounting Problems 2 (BSA 4-1 P2 EVALS)Document18 pagesFirst Evaluation Examination Practical Accounting Problems 2 (BSA 4-1 P2 EVALS)LJBernardoNo ratings yet

- Correct!: Accrued and DisclosedDocument111 pagesCorrect!: Accrued and DisclosedJaeNo ratings yet

- Quiz-Current Liability MULTIPLE CHOICE. Select The Best Answer For Each of The Following QuestionsDocument3 pagesQuiz-Current Liability MULTIPLE CHOICE. Select The Best Answer For Each of The Following QuestionsNicole Anne Santiago Sibulo0% (1)

- Burma Company Disclosed The Following Information About Liabilities at YearDocument1 pageBurma Company Disclosed The Following Information About Liabilities at YearMayuki TakizawaNo ratings yet

- IA2 Quiz 1 QuestionsDocument6 pagesIA2 Quiz 1 QuestionsJames Daniel SwintonNo ratings yet

- IA2 Practice Set 1Document2 pagesIA2 Practice Set 1jazonvaleraNo ratings yet

- 2018 ACCO 4103 2nd Summer ExamDocument5 pages2018 ACCO 4103 2nd Summer ExamSherri BonquinNo ratings yet

- ACCT. Cycle Reviewer 2Document7 pagesACCT. Cycle Reviewer 2Rosemarie GoNo ratings yet

- Ass Premium LiabDocument2 pagesAss Premium LiabRoschelle MiguelNo ratings yet

- Inbound 874801235495269853Document5 pagesInbound 874801235495269853MarielleNo ratings yet

- Far CeggDocument17 pagesFar CeggMaurice AgbayaniNo ratings yet

- Current LiabilitiesDocument3 pagesCurrent LiabilitiesROB101512No ratings yet

- 105 DepaDocument12 pages105 DepaLA M AENo ratings yet

- Prac 1 Final PreboardDocument10 pagesPrac 1 Final Preboardbobo kaNo ratings yet

- Acc17 - Liabilities and Income TaxDocument7 pagesAcc17 - Liabilities and Income TaxRarajNo ratings yet

- Local Media271226407970108268Document17 pagesLocal Media271226407970108268Jana Rose PaladaNo ratings yet

- Final Reviewer For ACC221Document91 pagesFinal Reviewer For ACC221ZalaR0cksNo ratings yet

- Notes With Unrealist RateDocument6 pagesNotes With Unrealist RateLauNo ratings yet

- Liabilities Part 2Document4 pagesLiabilities Part 2Jay LloydNo ratings yet

- AnswerDocument21 pagesAnswerStephanie EspalabraNo ratings yet

- Exercises Short ProblemsDocument6 pagesExercises Short ProblemsKlaire SwswswsNo ratings yet

- Intermediate Accounting 2 Prelim Exam Part II PDF FreeDocument5 pagesIntermediate Accounting 2 Prelim Exam Part II PDF FreeShairine AquinoNo ratings yet

- SGV Cup AccountingDocument13 pagesSGV Cup AccountingMCDABCNo ratings yet

- Problem Set 7. Contingencies and Other LiabilitiesDocument3 pagesProblem Set 7. Contingencies and Other LiabilitiesAngeline Gonzales PaneloNo ratings yet

- C. The Results of Operations, Cash Flow, and The Balance Sheet As If The Parent and Subsidiary Were A Single EntityDocument13 pagesC. The Results of Operations, Cash Flow, and The Balance Sheet As If The Parent and Subsidiary Were A Single EntityAlijah MercadoNo ratings yet

- Chapter 2Document8 pagesChapter 2cindyNo ratings yet

- Ia 2 Compilation of Quiz and ExercisesDocument16 pagesIa 2 Compilation of Quiz and ExercisesclairedennprztananNo ratings yet

- Prelim Lecture 1 Assignment: Multiple ChoiceDocument4 pagesPrelim Lecture 1 Assignment: Multiple Choicelinkin soyNo ratings yet

- UB FINALS 1stSEMDocument9 pagesUB FINALS 1stSEMChristian GarciaNo ratings yet

- Answer: P 4,800,000.: Nondetachable Warrants Givingthebondholderstherighttopurchase16,000p100parDocument5 pagesAnswer: P 4,800,000.: Nondetachable Warrants Givingthebondholderstherighttopurchase16,000p100parGenelayn TalabocNo ratings yet

- INTERMEDIATEACCOUNTINGIIDocument154 pagesINTERMEDIATEACCOUNTINGIINita Costillas De MattaNo ratings yet

- Eos CupFinal RoundDocument7 pagesEos CupFinal RoundMJ YaconNo ratings yet

- Level 1 AVERAGEDocument4 pagesLevel 1 AVERAGEJaime II LustadoNo ratings yet

- Receivable-to-Receivable-Financing (PRACTICE)Document3 pagesReceivable-to-Receivable-Financing (PRACTICE)liezelkatemesina82No ratings yet

- Financial Accounting and ReportingDocument8 pagesFinancial Accounting and ReportingPauline Idra100% (1)

- IA 3 MidtermDocument9 pagesIA 3 MidtermMelanie Samsona100% (1)

- AFARDocument10 pagesAFARby ScribdNo ratings yet

- FAR 1st PreboardDocument10 pagesFAR 1st PreboardLui100% (2)

- Practice Set Financial AccountingDocument6 pagesPractice Set Financial AccountingAJ'S GAMING CHANNELNo ratings yet

- Cfas Fs PreparationDocument3 pagesCfas Fs PreparationEvelina Del RosarioNo ratings yet

- ACC 111 Review Materials For Final Exam COPY To StudentsDocument4 pagesACC 111 Review Materials For Final Exam COPY To StudentsCondoriano BatumbakalNo ratings yet

- Seatwork 3-Liabilities 22Aug2019JMDocument3 pagesSeatwork 3-Liabilities 22Aug2019JMJoseph II MendozaNo ratings yet

- AFAR Compi For SA2Document82 pagesAFAR Compi For SA2jajajaredredNo ratings yet

- MIDTERMDocument8 pagesMIDTERMhaech jaemNo ratings yet

- Final Examination AK (60 COPIES)Document9 pagesFinal Examination AK (60 COPIES)Sittie Ainna A. UnteNo ratings yet

- QP Class Xii AccountancyDocument8 pagesQP Class Xii AccountancyRKS TECHNo ratings yet

- EA1 Ia2Document6 pagesEA1 Ia2alia fauniNo ratings yet

- Instructions: Answer The Following Carefully. Highlight Your Answer With Color Yellow. AfterDocument8 pagesInstructions: Answer The Following Carefully. Highlight Your Answer With Color Yellow. AfterMIKASANo ratings yet

- Advacc Quiz On PartnershipDocument10 pagesAdvacc Quiz On PartnershipLenie Lyn Pasion TorresNo ratings yet

- NOTES PROBLEMS ACCTG-323-newDocument3 pagesNOTES PROBLEMS ACCTG-323-newJoyluxxiNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Wiley GAAP for Governments 2012: Interpretation and Application of Generally Accepted Accounting Principles for State and Local GovernmentsFrom EverandWiley GAAP for Governments 2012: Interpretation and Application of Generally Accepted Accounting Principles for State and Local GovernmentsNo ratings yet

- Auditing: Control & Substantive Tests in Personnel & Payroll by David N. RicchiuteDocument19 pagesAuditing: Control & Substantive Tests in Personnel & Payroll by David N. RicchiuteTri Yuli ManurungNo ratings yet

- Fabm2 12 Q2 1002 SGDocument27 pagesFabm2 12 Q2 1002 SGTin CabosNo ratings yet

- ACE Bangladesh Payroll Handbook 2021Document32 pagesACE Bangladesh Payroll Handbook 2021Shuvo YeasinNo ratings yet

- NSSA Threshold April To June 2022Document2 pagesNSSA Threshold April To June 2022Daniel FerreiraNo ratings yet

- PFT Chapter 4Document27 pagesPFT Chapter 4DanisaraNo ratings yet

- 19950713ra SPD - Legal Rudiments Checklist For US MissionsDocument7 pages19950713ra SPD - Legal Rudiments Checklist For US MissionsFlibberdygibberNo ratings yet

- W2 Hyatt PLaceDocument5 pagesW2 Hyatt PLaceJuan Diego Velandia DuarteNo ratings yet

- Anaheim Police ContractDocument77 pagesAnaheim Police ContractCostinel MitreaNo ratings yet

- Mio SoulDocument1 pageMio SoulWel GadayanNo ratings yet

- Kentucky Tax Registration Application and Instructions: WWW - Revenue.ky - GovDocument28 pagesKentucky Tax Registration Application and Instructions: WWW - Revenue.ky - GovCharles Lamont BrewerNo ratings yet

- Financial Accounting Fundamentals: John J. Wild 2009 EditionDocument42 pagesFinancial Accounting Fundamentals: John J. Wild 2009 EditionMariamiNo ratings yet

- Test Bank For Payroll Accounting 2020 6th Edition Jeanette Landin Paulette SchirmerDocument38 pagesTest Bank For Payroll Accounting 2020 6th Edition Jeanette Landin Paulette SchirmerRobert Booth100% (41)

- Group Assignment Accounting Cycle - ADDocument4 pagesGroup Assignment Accounting Cycle - ADShewatatek MelakuNo ratings yet

- Paper 24Document38 pagesPaper 24ABEL KETEMANo ratings yet

- Principles of Taxation For Business and Investment Planning 14th Edition Jones Solutions ManualDocument18 pagesPrinciples of Taxation For Business and Investment Planning 14th Edition Jones Solutions Manualelmerthuy6ns76100% (28)

- PF1 Chapter 3 SlidesDocument98 pagesPF1 Chapter 3 SlidesNamie NamieNo ratings yet

- Horngrens Accounting 11Th Edition Miller Nobles Solutions Manual Full Chapter PDFDocument59 pagesHorngrens Accounting 11Th Edition Miller Nobles Solutions Manual Full Chapter PDFconatusimploded.bi6q100% (13)

- Sample Consulting AgreementDocument5 pagesSample Consulting AgreementJasmine TsoNo ratings yet

- Solution Manual For South Western Federal Taxation 2020 Individual Income Taxes 43rd Edition James C YoungDocument24 pagesSolution Manual For South Western Federal Taxation 2020 Individual Income Taxes 43rd Edition James C YoungJohnValenciaajgq100% (40)

- Documents PDFDocument2 pagesDocuments PDFNeena KumarNo ratings yet

- Payroll Accounting 2014 24th Edition Bieg Test BankDocument35 pagesPayroll Accounting 2014 24th Edition Bieg Test Bankeyghtgrosbeakr01sr100% (19)

- Checklist WCA 2019Document6 pagesChecklist WCA 2019atika kusumondariNo ratings yet

- Acctsys Formativ TriasDocument11 pagesAcctsys Formativ TriasMila Mercado100% (1)

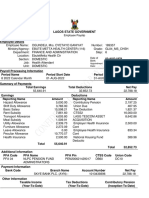

- Httpsmail Lagosstate Gov Ngowaservice svcsGetFileAttachmentid AAMkADFmZmUyMzcxLTQyNWEtNDZmOS1hMjFkLWZhNzg2N2JhNDYzYwBGAADocument3 pagesHttpsmail Lagosstate Gov Ngowaservice svcsGetFileAttachmentid AAMkADFmZmUyMzcxLTQyNWEtNDZmOS1hMjFkLWZhNzg2N2JhNDYzYwBGAADeborah LucridaNo ratings yet

- Concentrix Services India Private Limited Payslip For The Month of Oct - 2023Document1 pageConcentrix Services India Private Limited Payslip For The Month of Oct - 2023Bujji BabuNo ratings yet

- Payroll: Compensation AnalysisDocument4 pagesPayroll: Compensation AnalysisAlexanderJacobVielMartinezNo ratings yet

- All Job OrderDocument11 pagesAll Job OrderBPH MaramagNo ratings yet

- Non-Negotiable: Nvidia CorporationDocument1 pageNon-Negotiable: Nvidia CorporationSteven LinNo ratings yet

- SK Payroll 2023Document4 pagesSK Payroll 2023Jane Ann Parcullo PedereNo ratings yet

- Chapter 9 Acctng For LaborDocument4 pagesChapter 9 Acctng For LaborJoan Tanto MagdalenoNo ratings yet