Download as pdf or txt

You might also like

- Confirmed Divergence Manual PDFDocument57 pagesConfirmed Divergence Manual PDFDigitsmarterNo ratings yet

- Measuring The Impact of Microfinance in Hyderabad, IndiaDocument3 pagesMeasuring The Impact of Microfinance in Hyderabad, Indiasweetjar22No ratings yet

- Solutions For End-of-Chapter Questions and Problems: Chapter EightDocument25 pagesSolutions For End-of-Chapter Questions and Problems: Chapter EightSam MNo ratings yet

- Reverse Mortgage - The Emerging Financial Product - An EvaluationDocument8 pagesReverse Mortgage - The Emerging Financial Product - An EvaluationSahil WadhwaNo ratings yet

- Reverse Mortgage in IndiaDocument42 pagesReverse Mortgage in Indiakavi2288No ratings yet

- Main MatterDocument52 pagesMain MatterPraveen SehgalNo ratings yet

- What Is Microcredit and The Idea Behind ItDocument4 pagesWhat Is Microcredit and The Idea Behind Itcông lêNo ratings yet

- Explain Why Microcredit Has LittleDocument10 pagesExplain Why Microcredit Has LittleWajiha KhalidNo ratings yet

- About Microcredit: EmicrocreditDocument6 pagesAbout Microcredit: EmicrocreditRavi SoniNo ratings yet

- Is The Micro-Finance Like India's Sub-Prime?Document18 pagesIs The Micro-Finance Like India's Sub-Prime?scbihari1186No ratings yet

- Micropensions: Old Age Security For The PoorDocument20 pagesMicropensions: Old Age Security For The PoorJunaid AmerNo ratings yet

- Insurance Seminar Paper SynopsisDocument10 pagesInsurance Seminar Paper SynopsisaerosposharshanthNo ratings yet

- A Study On National Pension Schemes in IndiaDocument59 pagesA Study On National Pension Schemes in IndiaRajesh BathulaNo ratings yet

- Submitted To: - Submitted By:-Ms. Taru Baswan Asha (Lecturer) Prateek Agarwal Shanky GuptaDocument18 pagesSubmitted To: - Submitted By:-Ms. Taru Baswan Asha (Lecturer) Prateek Agarwal Shanky GuptaShanky GuptaNo ratings yet

- Unit 12 Risk Management Through Insurance Methods: ObjectivesDocument30 pagesUnit 12 Risk Management Through Insurance Methods: ObjectivesPriya ShindeNo ratings yet

- Annuity SchemesDocument15 pagesAnnuity Schemesmahi ranaNo ratings yet

- Sks Health InsuranceDocument3 pagesSks Health InsuranceRavi SoniNo ratings yet

- Notes - Unit 2Document10 pagesNotes - Unit 2ishita sabooNo ratings yet

- Does Microfinance Lead To Economic Growth?Document2 pagesDoes Microfinance Lead To Economic Growth?Candace100% (2)

- Kapoy Na Jud HuhuhuDocument58 pagesKapoy Na Jud Huhuhumahinayjake09No ratings yet

- Amitesh @insuDocument38 pagesAmitesh @insuAmitesh TejaswiNo ratings yet

- Project Report On Health Law: Limitations On Liabilities and MediclaimDocument17 pagesProject Report On Health Law: Limitations On Liabilities and MediclaimDeepesh SinghNo ratings yet

- Disability InsuranceDocument97 pagesDisability InsurancePoonith Sadanand BangeraNo ratings yet

- BRM ProjectDocument22 pagesBRM ProjectVishnu Vijayakumar100% (1)

- A Study On Factors Influencing of Women Policyholder's Investment Decision Towards Life Insurance Corporation of India Policies in ChennaiDocument6 pagesA Study On Factors Influencing of Women Policyholder's Investment Decision Towards Life Insurance Corporation of India Policies in ChennaiarcherselevatorsNo ratings yet

- Arindam Roy - Insight Research - Dexter Capital-Jayant MudhraDocument16 pagesArindam Roy - Insight Research - Dexter Capital-Jayant MudhraArindam RoyNo ratings yet

- Business Research MethodologyDocument34 pagesBusiness Research MethodologyDivine Truth Life MinistryNo ratings yet

- Benefits of Interest Free LoansDocument4 pagesBenefits of Interest Free Loansmr nNo ratings yet

- Benifits of Micro FinanceDocument12 pagesBenifits of Micro FinanceASHOK KUMAR REDDYNo ratings yet

- Youth of Australia and Their Superannuation AccountsDocument5 pagesYouth of Australia and Their Superannuation AccountsFedrick BuenaventuraNo ratings yet

- MicrofinanceDocument58 pagesMicrofinanceSamuel Davis100% (1)

- Micro Finance AssignmentDocument8 pagesMicro Finance Assignment19DM017 .SubhamNo ratings yet

- Ragh 2Document11 pagesRagh 2Muhammad AliNo ratings yet

- Health Insurance LawDocument16 pagesHealth Insurance LawParul NayakNo ratings yet

- Final Chapter 1Document11 pagesFinal Chapter 1Muskan BawejaNo ratings yet

- Lack CollateralDocument4 pagesLack CollateralMudassir AliNo ratings yet

- Cashpor ReportDocument91 pagesCashpor ReportAnand Gautam100% (1)

- Micro CreditDocument24 pagesMicro Creditঅভ্র মাহমুদNo ratings yet

- How Will The Goal Be Achieved?: MicrocreditDocument4 pagesHow Will The Goal Be Achieved?: MicrocreditthundergssNo ratings yet

- Goldberg PaperDocument8 pagesGoldberg PaperTony SsenfumaNo ratings yet

- Chapter 1-5 Kakapoy Na JudDocument47 pagesChapter 1-5 Kakapoy Na JudCarla Jane Maitom TagoyNo ratings yet

- A Study of The Performance of Microfinance Institutions in India in Present Era - A Tool For Poverty AlleviationDocument10 pagesA Study of The Performance of Microfinance Institutions in India in Present Era - A Tool For Poverty AlleviationjyotivermaNo ratings yet

- Mechanics of Finance - Personal Finance Advisory Firm"Finance Friend"Document8 pagesMechanics of Finance - Personal Finance Advisory Firm"Finance Friend"IJRASETPublicationsNo ratings yet

- Ijresm V4 I7 14Document9 pagesIjresm V4 I7 14Sneha KshatriyaNo ratings yet

- A Critical Analysis of Micro Finance in IndiaDocument54 pagesA Critical Analysis of Micro Finance in IndiaArchana MehraNo ratings yet

- Thesis On Insurance Sector in IndiaDocument6 pagesThesis On Insurance Sector in Indiaaprilchesserspringfield100% (2)

- Micro Health Insurance - A Way of Ensuring Financial Security To The Poor. By. Dr.N.JeyaseelanDocument12 pagesMicro Health Insurance - A Way of Ensuring Financial Security To The Poor. By. Dr.N.JeyaseelanvijayjeyaseelanNo ratings yet

- Literature Review of Pension FundDocument8 pagesLiterature Review of Pension Funddhjiiorif100% (1)

- IN INDIA Micro-Finance-In-IndiaDocument65 pagesIN INDIA Micro-Finance-In-IndiaNagireddy Kalluri100% (1)

- Health Benefits of Financial Inclusion A Literature ReviewDocument7 pagesHealth Benefits of Financial Inclusion A Literature Reviewl1wot1j1fon3No ratings yet

- An Analysis of Legal Medical Mental Health Insurance in India: A Comparative Study With Uk, Usa, France, and FinlandDocument14 pagesAn Analysis of Legal Medical Mental Health Insurance in India: A Comparative Study With Uk, Usa, France, and FinlandSumyyaNo ratings yet

- IJCRT2209454Document6 pagesIJCRT2209454venkatesh.s venkatesh.sNo ratings yet

- Literature Review of Life Insurance SectorDocument8 pagesLiterature Review of Life Insurance Sectorfvf442bf100% (1)

- Theory of MicrofinanceDocument9 pagesTheory of Microfinancetaylorbrennan94% (18)

- Health InsuranceDocument8 pagesHealth Insurancesuhitaa sridharNo ratings yet

- Islamic Financial InstitutionsDocument12 pagesIslamic Financial InstitutionshaithamzeinNo ratings yet

- A. About Microfinance: Microfinance Is A General Term To Describe Financial Services ToDocument32 pagesA. About Microfinance: Microfinance Is A General Term To Describe Financial Services ToAnshul ChawraNo ratings yet

- Microfinance in India: Nidhi Bothra Vinod Kothari & CompanyDocument4 pagesMicrofinance in India: Nidhi Bothra Vinod Kothari & CompanyNidhi BothraNo ratings yet

- Maximize Your Medicare: 2022-2023 Edition: Qualify for Benefits, Protect Your Health, and Minimize Your CostsFrom EverandMaximize Your Medicare: 2022-2023 Edition: Qualify for Benefits, Protect Your Health, and Minimize Your CostsRating: 4 out of 5 stars4/5 (1)

- Reverse Mortgage 2024: Unlock Your Home Equity for a Flourishing Retirement: The Essential Guidebook to Understanding Reverse Mortgages, Enhancing Retirement Planning, and Achieving Financial FreedomFrom EverandReverse Mortgage 2024: Unlock Your Home Equity for a Flourishing Retirement: The Essential Guidebook to Understanding Reverse Mortgages, Enhancing Retirement Planning, and Achieving Financial FreedomNo ratings yet

- FTSE4Good Index Series Ground RulesDocument28 pagesFTSE4Good Index Series Ground RulesAdel AdielaNo ratings yet

- 2023 06 16 - LogDocument4 pages2023 06 16 - LogLuiza CorreaNo ratings yet

- Bdo Vs YpilDocument2 pagesBdo Vs YpilCE SherNo ratings yet

- Second Call For Paper: National Symposium On Sustainable Waste Management (NSSWM-2019)Document2 pagesSecond Call For Paper: National Symposium On Sustainable Waste Management (NSSWM-2019)Aprizon PutraNo ratings yet

- Hortifrut - Comprar - La Compañía Fortalece Su Presencia en Europa A Lo Largo de La Cadena de ValorDocument2 pagesHortifrut - Comprar - La Compañía Fortalece Su Presencia en Europa A Lo Largo de La Cadena de ValorAndres UrrutiaNo ratings yet

- Project On Compensation and Benefits Ufone: Submitted To: Respected MR - Habib KhanDocument22 pagesProject On Compensation and Benefits Ufone: Submitted To: Respected MR - Habib KhanAbdul QadoosNo ratings yet

- Using Receivables Credit To CashDocument630 pagesUsing Receivables Credit To CashWilliam VelascoNo ratings yet

- ACALawprofile (As of 2021)Document18 pagesACALawprofile (As of 2021)Genesis AdarloNo ratings yet

- Suggestion Direct & Indirect TaxDocument2 pagesSuggestion Direct & Indirect TaxPratik ShahNo ratings yet

- Contract - RegularDocument5 pagesContract - Regularabanganjm08No ratings yet

- 2022-12-15 StrategiesDocument1 page2022-12-15 StrategiesquemilangaNo ratings yet

- Evaluated Receipt Settlement: Vendor Master Data Info Record Purchase OrderDocument6 pagesEvaluated Receipt Settlement: Vendor Master Data Info Record Purchase OrderBenny KhorNo ratings yet

- 31.05.2023 Notificari Sunset PT - Postat Incepand Cu Luna IUNIE 2016Document20 pages31.05.2023 Notificari Sunset PT - Postat Incepand Cu Luna IUNIE 2016Anca ToaderNo ratings yet

- 467 - Age222-Introduction To Farm Machinery-2unitsDocument8 pages467 - Age222-Introduction To Farm Machinery-2unitsAnonymous 1XBCMXNo ratings yet

- Banglalink Nabeela PPT Final (Iv-Vi)Document6 pagesBanglalink Nabeela PPT Final (Iv-Vi)Shahrear AkibNo ratings yet

- GXD0056 en GX WebManager 9.20 WCB Development Tutorial 20111024Document161 pagesGXD0056 en GX WebManager 9.20 WCB Development Tutorial 20111024AbhideepBakshiNo ratings yet

- Accounting Policies, Changes in Accounting Estimates and ErrorsDocument23 pagesAccounting Policies, Changes in Accounting Estimates and ErrorsFery AnnNo ratings yet

- Scaling Robotic Process AutomationDocument17 pagesScaling Robotic Process Automationserge ziehiNo ratings yet

- GSECL TenderDocument116 pagesGSECL TenderUBPL mktgNo ratings yet

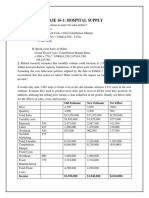

- Case 16-1: Hospital Supply: 1. What Is The Break-Even Volume in Units? in Sales Dollars?Document6 pagesCase 16-1: Hospital Supply: 1. What Is The Break-Even Volume in Units? in Sales Dollars?Lalit SapkaleNo ratings yet

- Vincom Retail Joint Stock Company 2020 Performance and 2021 OutlookDocument28 pagesVincom Retail Joint Stock Company 2020 Performance and 2021 OutlookNeil NguyenNo ratings yet

- Themes (AQA) Test Questions - AQA - GCSE English Language Revision - BBC BitesizeDocument5 pagesThemes (AQA) Test Questions - AQA - GCSE English Language Revision - BBC Bitesizemegolov536No ratings yet

- Case Studies - INDUSTRIAL RELATIONS AND OTHERDocument64 pagesCase Studies - INDUSTRIAL RELATIONS AND OTHERKratikaNo ratings yet

- Clean Air ActDocument31 pagesClean Air ActJulienne Mae Valmonte MapaNo ratings yet

- 1-60261432193 G0060070725 PDFDocument8 pages1-60261432193 G0060070725 PDFIntikhab GoharNo ratings yet

- Aslund - Reform TrapDocument21 pagesAslund - Reform TrapSanket ShrivastavaNo ratings yet

- Press Release - 24 Aug 2023Document2 pagesPress Release - 24 Aug 2023rock6hard7No ratings yet

- Post-Commencement Analysis of The Dutch Mission-Oriented Topsector and Innovation Policy' StrategyDocument55 pagesPost-Commencement Analysis of The Dutch Mission-Oriented Topsector and Innovation Policy' StrategyjlskdfjNo ratings yet