Download as pdf or txt

You might also like

- CPA Taxation by Ampongan - Principles of TaxationDocument43 pagesCPA Taxation by Ampongan - Principles of TaxationVictor Tuco100% (1)

- Oscar Velazquez Ortega 2021 - TaxReturnDocument12 pagesOscar Velazquez Ortega 2021 - TaxReturnoscar velasquezNo ratings yet

- Salaried Individuals For AY 2023-24 - Income Tax DepartmentDocument26 pagesSalaried Individuals For AY 2023-24 - Income Tax DepartmentSunitha GNo ratings yet

- Hindu Undivided Family (HUF) For AY 2022-2023 - Income Tax DepartmentDocument13 pagesHindu Undivided Family (HUF) For AY 2022-2023 - Income Tax DepartmentAnkit A DesaiNo ratings yet

- (/iec/foportal/) : How To File Tax ReturnsDocument2 pages(/iec/foportal/) : How To File Tax Returnsgino.kamarianNo ratings yet

- Income TaxDocument20 pagesIncome TaxEjNo ratings yet

- Deductions and E-Filing ITR For Partnership BusinessDocument20 pagesDeductions and E-Filing ITR For Partnership BusinessAyushi BhallaNo ratings yet

- (/iec/foportal/) : How To File ReturnsDocument2 pages(/iec/foportal/) : How To File Returnsgino.kamarianNo ratings yet

- Manual Return Ty 2017Document56 pagesManual Return Ty 2017Muhammad RizwanNo ratings yet

- Income Tax - Bureau of Internal RevenueDocument21 pagesIncome Tax - Bureau of Internal Revenue홍혜연No ratings yet

- Instructions For Filling in Return Form & Wealth Statement Form Sr. InstructionDocument40 pagesInstructions For Filling in Return Form & Wealth Statement Form Sr. InstructionSammar EllahiNo ratings yet

- Tax AssignmentDocument14 pagesTax Assignmentrushi sreedhar100% (1)

- Taxation ReviewerDocument25 pagesTaxation ReviewerLes EvangeListaNo ratings yet

- Types of ITR Forms For FY 2022-23 (AY 2023-24)Document21 pagesTypes of ITR Forms For FY 2022-23 (AY 2023-24)DRK FrOsTeRNo ratings yet

- Sro 792Document34 pagesSro 792asfand yarNo ratings yet

- 2.5 Income Tax FilingDocument17 pages2.5 Income Tax Filing128hrithikabishtNo ratings yet

- Amendments in It Returns - AY 2020-21 in It Returns - AY 2020-21Document22 pagesAmendments in It Returns - AY 2020-21 in It Returns - AY 2020-21Abinaya GunasekarNo ratings yet

- IT ReturnsDocument11 pagesIT ReturnsAnjali Krishna SNo ratings yet

- Residential Status of An IndividualDocument11 pagesResidential Status of An IndividualRevathy PrasannanNo ratings yet

- Return of Income: (Date in Connection With Assessment Order Is Ignored From All Sections)Document6 pagesReturn of Income: (Date in Connection With Assessment Order Is Ignored From All Sections)omar zohorianNo ratings yet

- Cimage College Patna: Abhijit PrasadDocument31 pagesCimage College Patna: Abhijit Prasadabhijit prasadNo ratings yet

- Desi Town: Income Tax, Income Tax Return Form, WWW - Incometaxindia.gov - In, Last Date Income Tax ReturnDocument3 pagesDesi Town: Income Tax, Income Tax Return Form, WWW - Incometaxindia.gov - In, Last Date Income Tax ReturnarulmcaNo ratings yet

- Instructions For Filling in Return Form & Wealth Statement Form Sr. InstructionDocument7 pagesInstructions For Filling in Return Form & Wealth Statement Form Sr. InstructionfiazNo ratings yet

- 19 Personal Equity Retirement Account PERADocument4 pages19 Personal Equity Retirement Account PERALumingNo ratings yet

- Frequently Asked QuestionsDocument16 pagesFrequently Asked QuestionsKenneth DomingoNo ratings yet

- Guide ITProof SubmissionDocument9 pagesGuide ITProof SubmissionSrikanthNo ratings yet

- FAQ - PERA (As of 31 July 2021)Document16 pagesFAQ - PERA (As of 31 July 2021)Jomar Joseph Cabigon Jr.No ratings yet

- CA Viswanadha Manohar: Hyderabad & AmaravatiDocument47 pagesCA Viswanadha Manohar: Hyderabad & AmaravatiranjitNo ratings yet

- US Internal Revenue Service: I5498e 07Document1 pageUS Internal Revenue Service: I5498e 07IRSNo ratings yet

- Choice of ITRDocument7 pagesChoice of ITRravirockz128No ratings yet

- BCO 11 Block 03Document70 pagesBCO 11 Block 03Al OkNo ratings yet

- Bureau of Internal Revenue: Republic of The Philippines Department of Finance Quezon CityDocument11 pagesBureau of Internal Revenue: Republic of The Philippines Department of Finance Quezon CityAnj MerisNo ratings yet

- Computerised Accounting and E Filing of Tax ReturnsDocument10 pagesComputerised Accounting and E Filing of Tax ReturnsAnkit SinghNo ratings yet

- Itr 1 Ay 2023-24Document3 pagesItr 1 Ay 2023-24Arup MridhaNo ratings yet

- Iris FAQsDocument74 pagesIris FAQsHammad SalahuddinNo ratings yet

- Government Notifies New Income Tax Return Forms For The Financial Year 2014-15Document8 pagesGovernment Notifies New Income Tax Return Forms For The Financial Year 2014-15HimanshuNo ratings yet

- 5 Features of Economic Zones Under PEZA in The Philippines - Tax and Accounting Center, IncDocument7 pages5 Features of Economic Zones Under PEZA in The Philippines - Tax and Accounting Center, IncMartin MartelNo ratings yet

- User Manuadfgl Application PDFDocument15 pagesUser Manuadfgl Application PDFVengat VenkitasamyNo ratings yet

- Types of Income Tax FormsDocument5 pagesTypes of Income Tax FormsCharishma Sekhar.KNo ratings yet

- Unit No 4 - Tax Planning and Personal FinanceDocument21 pagesUnit No 4 - Tax Planning and Personal FinancepujaskawaleNo ratings yet

- Question 1 Paper13Document6 pagesQuestion 1 Paper13Anshu AbhishekNo ratings yet

- Income Tax Return Forms ArdraDocument25 pagesIncome Tax Return Forms ArdraGangothri AsokNo ratings yet

- Tax Planning AssignmentDocument10 pagesTax Planning AssignmentJayashree Mohandass100% (1)

- CHP 9Document7 pagesCHP 9Jerlmilline Serrano JoseNo ratings yet

- Filing Itr HbookDocument26 pagesFiling Itr HbookRaveendran PmNo ratings yet

- 11 Task Performance TaxDocument2 pages11 Task Performance Taxjeffersam31No ratings yet

- Computation of Total IncomeDocument48 pagesComputation of Total IncomeAlphonsaNo ratings yet

- US Internal Revenue Service: I5498eDocument1 pageUS Internal Revenue Service: I5498eIRSNo ratings yet

- Assignment of Corporate Tax Planning On Rules For Filing Income Tax ReturnDocument8 pagesAssignment of Corporate Tax Planning On Rules For Filing Income Tax ReturnShubhamNo ratings yet

- ANF5ADocument9 pagesANF5ACharles JacobNo ratings yet

- A Primer On Tax Aspects Related To Ma Transactions 1637068495Document11 pagesA Primer On Tax Aspects Related To Ma Transactions 1637068495akshayvermalaw1No ratings yet

- Notes LLB Tax Nav 2Document12 pagesNotes LLB Tax Nav 2amit HCSNo ratings yet

- US Internal Revenue Service: I5500ez - 2004Document9 pagesUS Internal Revenue Service: I5500ez - 2004IRSNo ratings yet

- Withholding TaxDocument21 pagesWithholding TaxTres SanicamNo ratings yet

- 2012 Instructions For Schedule F: Profit or Loss From FarmingDocument20 pages2012 Instructions For Schedule F: Profit or Loss From FarmingRonnie QuimioNo ratings yet

- Wa0002.Document12 pagesWa0002.Noman AkhtarNo ratings yet

- 19770ipcc It Vol1 Cp8Document7 pages19770ipcc It Vol1 Cp8Joseph SalidoNo ratings yet

- Income Tax in India - Wikipedia, The Free EncyclopediaDocument10 pagesIncome Tax in India - Wikipedia, The Free EncyclopediakandurimaruthiNo ratings yet

- Auto Income Tax Calculator Version 5.1 2010-11Document19 pagesAuto Income Tax Calculator Version 5.1 2010-11Bijender Pal ChoudharyNo ratings yet

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesFrom EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesNo ratings yet

- 1040 Exam Prep: Module I: The Form 1040 FormulaFrom Everand1040 Exam Prep: Module I: The Form 1040 FormulaRating: 1 out of 5 stars1/5 (3)

- AvatarnikaDocument48 pagesAvatarnikaDevdatta NaikNo ratings yet

- JBoss As Windows Service in WindowsDocument2 pagesJBoss As Windows Service in WindowsDevdatta NaikNo ratings yet

- Section 80D - The Economic TimesDocument4 pagesSection 80D - The Economic TimesDevdatta NaikNo ratings yet

- Section 80D - Clear TaxDocument12 pagesSection 80D - Clear TaxDevdatta NaikNo ratings yet

- Difference Between NPS Account Tier 1 vs. Tier 2Document3 pagesDifference Between NPS Account Tier 1 vs. Tier 2Devdatta NaikNo ratings yet

- What Are ESOPs and How Are They TaxedDocument3 pagesWhat Are ESOPs and How Are They TaxedDevdatta NaikNo ratings yet

- Request For Taxpayer Identification Number and CertificationDocument4 pagesRequest For Taxpayer Identification Number and CertificationZak CascaNo ratings yet

- 1 Test For Each Chapter 2 Full Syllabus Tests For Each Subject Scheduled Start 26th Jan May 2024 1704696385Document9 pages1 Test For Each Chapter 2 Full Syllabus Tests For Each Subject Scheduled Start 26th Jan May 2024 1704696385Anil ReddyNo ratings yet

- RVZXQ Av Qi Cwigvc: BdwbuDocument19 pagesRVZXQ Av Qi Cwigvc: Bdwbuiliyas shahNo ratings yet

- Nhiel - Serentas Payroll PayslipSelfService ExternalPayslipPDFProcessPHDocument1 pageNhiel - Serentas Payroll PayslipSelfService ExternalPayslipPDFProcessPHnhiel anthony SerentasNo ratings yet

- Ganraj ConstructionDocument2 pagesGanraj ConstructionSUNIL GAIKWADNo ratings yet

- Employee Details Payment & Leave Details: Arrears Amount CurrentDocument2 pagesEmployee Details Payment & Leave Details: Arrears Amount CurrentRamesh yaraboluNo ratings yet

- Final - Assignment 1 (Acctg. For Special Transactions)Document3 pagesFinal - Assignment 1 (Acctg. For Special Transactions)Kimberly AbiaNo ratings yet

- Disclosures Under ICDSDocument11 pagesDisclosures Under ICDScadrjainNo ratings yet

- Chapter 14Document4 pagesChapter 14Richard Jay CamaNo ratings yet

- Peza-Esd Reportorial RequirementsDocument2 pagesPeza-Esd Reportorial RequirementsBelle MadrigalNo ratings yet

- Corporate Tax Planning B.com-VDocument31 pagesCorporate Tax Planning B.com-VSyed Osama YusufNo ratings yet

- Benfitsform Starbucks BeanstockDocument1 pageBenfitsform Starbucks BeanstockAndrew Christopher CaseNo ratings yet

- GST FormDocument16 pagesGST FormPruthiv RajNo ratings yet

- How To Compute Basic Income TaxDocument11 pagesHow To Compute Basic Income Taxkate trishaNo ratings yet

- MAS Diagnostic ExamDocument10 pagesMAS Diagnostic ExamDanielNo ratings yet

- CG - 2018-2019 - Jayshree Jay KariaDocument2 pagesCG - 2018-2019 - Jayshree Jay KariaAnil kadamNo ratings yet

- Ifta 3Document8 pagesIfta 3api-277676712No ratings yet

- California Last Will and Testament TemplateDocument10 pagesCalifornia Last Will and Testament TemplateJa. ENo ratings yet

- DT (Q&a)Document186 pagesDT (Q&a)mktg.seagullshippingNo ratings yet

- TAXATION 2 Chapter 1 Introduction To Transfer TaxationDocument5 pagesTAXATION 2 Chapter 1 Introduction To Transfer TaxationKim Cristian MaañoNo ratings yet

- Tuason V Posadas PDFDocument45 pagesTuason V Posadas PDFMina AragonNo ratings yet

- 2018 - PAL vs. CIRDocument2 pages2018 - PAL vs. CIRJimcris HermosadoNo ratings yet

- Fesco Online BilllDocument1 pageFesco Online BilllToqeer RazaNo ratings yet

- Property Rating As A Source of Local Government RevenueDocument6 pagesProperty Rating As A Source of Local Government RevenuesobhalinbeheraNo ratings yet

- Return 2019 PDFDocument3 pagesReturn 2019 PDFIkramNo ratings yet

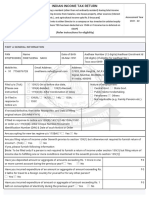

- Indian Income Tax Return: Part A General InformationDocument8 pagesIndian Income Tax Return: Part A General Informationsushilprajapati10_77No ratings yet

- 02 RebatesDocument53 pages02 RebatesughaniNo ratings yet

- Statutory Provisions Case Laws Part 01 02Document12 pagesStatutory Provisions Case Laws Part 01 02wellawalalasithNo ratings yet