Financial Statements Guide

Financial Statements Guide

You might also like

- D196 Study Guide Answers & NotesDocument21 pagesD196 Study Guide Answers & NotesAsril Doank100% (1)

- Questions For IFRS HighlightedDocument28 pagesQuestions For IFRS HighlightedWowee Cruz100% (1)

- CHAPTER 7 Caselette - Audit of PPEDocument34 pagesCHAPTER 7 Caselette - Audit of PPErochielanciola60% (5)

- Understanding Financial Statements (Review and Analysis of Straub's Book)From EverandUnderstanding Financial Statements (Review and Analysis of Straub's Book)Rating: 5 out of 5 stars5/5 (5)

- Fixed Asset ManagementDocument85 pagesFixed Asset Managementrasheedshaikh2003100% (2)

- Income StatementDocument6 pagesIncome Statementkyrian chimaNo ratings yet

- FNCE Assignment Week 6Document10 pagesFNCE Assignment Week 6Rajeev ShahdadpuriNo ratings yet

- Income StatementDocument3 pagesIncome StatementMamta LallNo ratings yet

- Week 15 Lesson 11Document53 pagesWeek 15 Lesson 11D A M N E R ANo ratings yet

- Accounting ReportDocument23 pagesAccounting ReportAreeba FatimaNo ratings yet

- Masan Group CorporationDocument31 pagesMasan Group Corporationhồ nam longNo ratings yet

- How To Write A Traditional Business Plan: Step 1Document5 pagesHow To Write A Traditional Business Plan: Step 1Leslie Ann Elazegui UntalanNo ratings yet

- Financial Statement PresentationDocument33 pagesFinancial Statement Presentationcyrene jamnagueNo ratings yet

- All AccountingDocument122 pagesAll AccountingHassen ReshidNo ratings yet

- Financial TrainingDocument15 pagesFinancial TrainingGismon PereiraNo ratings yet

- Finance QuestionsDocument14 pagesFinance QuestionsGeetika YadavNo ratings yet

- Sat Pra 13Document7 pagesSat Pra 13Samyak KalaskarNo ratings yet

- Understanding The Income StatementDocument4 pagesUnderstanding The Income Statementluvujaya100% (1)

- FINFO Week 3 Learner GuideDocument14 pagesFINFO Week 3 Learner GuideAngelica Caballes TabaniaNo ratings yet

- Financial StatementsDocument8 pagesFinancial StatementsbouhaddihayetNo ratings yet

- What Is RevenueDocument31 pagesWhat Is RevenueLEARN WITH AGALYANo ratings yet

- Key Takeaways: DirectDocument13 pagesKey Takeaways: DirectSB CorporationNo ratings yet

- Managerial Finance, Financial Accounting and Analysis For Engineering Managers PDFDocument5 pagesManagerial Finance, Financial Accounting and Analysis For Engineering Managers PDFAshuriko KazuNo ratings yet

- Script For ReportingDocument14 pagesScript For Reportingvelasco.mhervin08No ratings yet

- Income Statement: Profit/Loss Account Dr. Satish Jangra (2009A229M)Document14 pagesIncome Statement: Profit/Loss Account Dr. Satish Jangra (2009A229M)Dr. Satish Jangra100% (1)

- Clo-3 Assignment: Chemical Engineering Economics 2016-CH-454Document9 pagesClo-3 Assignment: Chemical Engineering Economics 2016-CH-454ali ayanNo ratings yet

- Task 4b UBODocument3 pagesTask 4b UBOEdem Augustin AGBEVENo ratings yet

- Bookkeeping Module 1Document11 pagesBookkeeping Module 1Cindy TorresNo ratings yet

- Final Accounts LessonDocument12 pagesFinal Accounts LessonSiham KhayetNo ratings yet

- CH 4 - Financial AnalysisDocument13 pagesCH 4 - Financial AnalysisbavanthinilNo ratings yet

- Business Notes: Reak Even AnalysisDocument8 pagesBusiness Notes: Reak Even AnalysisIvyNo ratings yet

- Proforma Fin Statement AssignmentDocument11 pagesProforma Fin Statement Assignmentashoo khoslaNo ratings yet

- Sample Operational Financial Analysis ReportDocument8 pagesSample Operational Financial Analysis ReportValentinorossiNo ratings yet

- Financial Accounting: Sir Syed Adeel Ali BukhariDocument25 pagesFinancial Accounting: Sir Syed Adeel Ali Bukhariadeelali849714No ratings yet

- Guide To Financial TermsDocument21 pagesGuide To Financial TermsShahrokh Paravarzar100% (1)

- Terms of Share MarketDocument6 pagesTerms of Share Marketsearchanirban6474No ratings yet

- Financial Accounting & AnalysisDocument5 pagesFinancial Accounting & AnalysisSourav SaraswatNo ratings yet

- Sample Operational Financial Analysis ReportDocument13 pagesSample Operational Financial Analysis Reportshivkumara27No ratings yet

- Fm108 ModuleDocument17 pagesFm108 ModuleKarl Dennis TiansayNo ratings yet

- Key Financial Performance IndicatorsDocument19 pagesKey Financial Performance Indicatorsmariana.zamudio7aNo ratings yet

- Assignment On SCMDocument5 pagesAssignment On SCMcattiger123No ratings yet

- VU Lesson 8Document5 pagesVU Lesson 8ranawaseem100% (1)

- Lecture Three Chapter FiveDocument4 pagesLecture Three Chapter Fivebouchra bouchraNo ratings yet

- What Is The Statement of Comprehensive Income?: EquityDocument4 pagesWhat Is The Statement of Comprehensive Income?: EquityKatherine Canisguin AlvarecoNo ratings yet

- finance conceptsDocument15 pagesfinance conceptsgodwillinno1997No ratings yet

- Information Sheet - BKKPG-8 - Preparing Financial StatementsDocument10 pagesInformation Sheet - BKKPG-8 - Preparing Financial StatementsEron Roi Centina-gacutanNo ratings yet

- Financial Accounting: Salal Durrani 2020Document12 pagesFinancial Accounting: Salal Durrani 2020Rahat BatoolNo ratings yet

- Financial Analysis FundamentalsDocument12 pagesFinancial Analysis FundamentalsAni Dwi Rahmanti RNo ratings yet

- Sevilla, Renz Marie A. Bsba FM 2-C: Assignment # 2Document4 pagesSevilla, Renz Marie A. Bsba FM 2-C: Assignment # 2Gerald Noveda RomanNo ratings yet

- AssignmentDocument4 pagesAssignmentRithik TiwariNo ratings yet

- Unit 3 Assignment 2 Task 2Document4 pagesUnit 3 Assignment 2 Task 2Noor KilaniNo ratings yet

- Profit and Loss AccountDocument9 pagesProfit and Loss AccountMurad Shah PatelNo ratings yet

- Topics For The Exam 2ND BaccDocument4 pagesTopics For The Exam 2ND BaccJose rendonNo ratings yet

- Interpretation On RatiosDocument3 pagesInterpretation On RatiosLorraine CalderonNo ratings yet

- Week 004 - Module Statement of Comprehensive Income IDocument7 pagesWeek 004 - Module Statement of Comprehensive Income IJulia AcostaNo ratings yet

- Chapter-3 FINANCIAL STATEMENT PREPARATIONDocument21 pagesChapter-3 FINANCIAL STATEMENT PREPARATIONWoldeNo ratings yet

- Questions DuresDocument25 pagesQuestions DuresAnna-Maria Müller-SchmidtNo ratings yet

- Financial PlanDocument20 pagesFinancial PlanHarold FilomenoNo ratings yet

- A Study On Profitability Analysis atDocument13 pagesA Study On Profitability Analysis atAsishNo ratings yet

- How To Read A Financial StatementDocument23 pagesHow To Read A Financial Statementbuvana1980No ratings yet

- Income Statement Balance SheetDocument19 pagesIncome Statement Balance SheetJeff Lacasandile100% (2)

- A Poem About Alcoholism, Drugs, Suicide and Murder. - B.U.XD.Document1 pageA Poem About Alcoholism, Drugs, Suicide and Murder. - B.U.XD.henaa sssaaaaeeeettNo ratings yet

- A Short Hilarious Drunk Story From 1990's Brooklyn - B.U.XD.Document1 pageA Short Hilarious Drunk Story From 1990's Brooklyn - B.U.XD.henaa sssaaaaeeeettNo ratings yet

- A Sad TaleDocument1 pageA Sad Talehenaa sssaaaaeeeettNo ratings yet

- A Short Story About Thumbs - B.u.xd.Document1 pageA Short Story About Thumbs - B.u.xd.henaa sssaaaaeeeettNo ratings yet

- January 2023 Private Candidate CentresDocument2 pagesJanuary 2023 Private Candidate Centreshenaa sssaaaaeeeettNo ratings yet

- An Easy Essay DocumentDocument1 pageAn Easy Essay Documenthenaa sssaaaaeeeettNo ratings yet

- Tata Motors Fundamental AnalysisDocument3 pagesTata Motors Fundamental AnalysisRahul RaghwaniNo ratings yet

- Module 1 & 2 Accounting For Special TransactionsDocument19 pagesModule 1 & 2 Accounting For Special TransactionsLian MaragayNo ratings yet

- Sip Project of MD Shamim AkhtarDocument89 pagesSip Project of MD Shamim AkhtarSami ZamaNo ratings yet

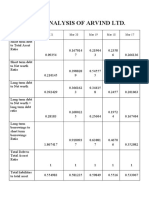

- Ratio Analysis of Arvind LTD.: Ratios Mar 21 Mar 20 Mar 19 Mar 18 Mar 17Document10 pagesRatio Analysis of Arvind LTD.: Ratios Mar 21 Mar 20 Mar 19 Mar 18 Mar 17simranNo ratings yet

- Financial AnalysisDocument73 pagesFinancial AnalysisAqdas ShahNo ratings yet

- FIS and Audit Statement TemplateDocument4 pagesFIS and Audit Statement Templateissam jendoubiNo ratings yet

- Coop Updates 3Document52 pagesCoop Updates 3nelsonpm81No ratings yet

- Quizzer - Revised Conceptual FrameworkDocument6 pagesQuizzer - Revised Conceptual FrameworkJohn Reiven Adaya Mendoza100% (1)

- What Is SFP?: Statement of Financial PositionDocument1 pageWhat Is SFP?: Statement of Financial PositionJessel Jean Lascoña OntialNo ratings yet

- Ar Pegadaian 2018 Eng V3 PDFDocument554 pagesAr Pegadaian 2018 Eng V3 PDFKamelia AgustiniNo ratings yet

- The Financial Statements: Chapter OutlineDocument15 pagesThe Financial Statements: Chapter OutlineBhagaban DasNo ratings yet

- ACCA F8 - AUDIT RISK by Alan Biju Palak ACCADocument5 pagesACCA F8 - AUDIT RISK by Alan Biju Palak ACCAkasimranjhaNo ratings yet

- Statement of Cash Flows and Book Value Per Share - Group 4Document67 pagesStatement of Cash Flows and Book Value Per Share - Group 4Karen MagsayoNo ratings yet

- Worksheet - Income Sheet and Form Series 18 AICPA, AICPA Risk of Material Misstatement WorksheetsDocument20 pagesWorksheet - Income Sheet and Form Series 18 AICPA, AICPA Risk of Material Misstatement WorksheetswellawalalasithNo ratings yet

- 1 20180905052123Document194 pages1 20180905052123Gupllo Kin'emonJrNo ratings yet

- Case Study November 2010 Exam Paper ICAEWDocument20 pagesCase Study November 2010 Exam Paper ICAEWmanofhonourNo ratings yet

- NolascoDocument23 pagesNolascojuztine dofitasNo ratings yet

- IPSAS Detil StandardDocument94 pagesIPSAS Detil StandardMaya IndriNo ratings yet

- PT MNC Vision Networks TBK - 31 Desember 2021 PDFDocument70 pagesPT MNC Vision Networks TBK - 31 Desember 2021 PDFSULTHAN ATHAYA AWDIHANSYAHNo ratings yet

- Beams10e - Ch02 Stock Investments-Investor Accounting and ReportingDocument37 pagesBeams10e - Ch02 Stock Investments-Investor Accounting and ReportingNadiaAmaliaNo ratings yet

- Project DetailsDocument1,325 pagesProject DetailsShrikanth SolaNo ratings yet

- AccountingDocument4 pagesAccountingAnimaw YayehNo ratings yet

- Investment and Decision Analysis For Petroleum ExplorationDocument24 pagesInvestment and Decision Analysis For Petroleum Explorationsandro0112No ratings yet

- BAFACR16 04 Problem IllustrationsDocument3 pagesBAFACR16 04 Problem IllustrationsThats BellaNo ratings yet

- IPCC MTP2 AccountingDocument7 pagesIPCC MTP2 AccountingBalaji SiddhuNo ratings yet

- The Trading and Profit and Loss Account and The Balance SheetDocument62 pagesThe Trading and Profit and Loss Account and The Balance SheetMir AqibNo ratings yet

- There Are Some Major Key Performance Indicators For Chemical Industry: 1. FinancialDocument3 pagesThere Are Some Major Key Performance Indicators For Chemical Industry: 1. FinancialsonuNo ratings yet

Download as pdf or txt

You might also like

- D196 Study Guide Answers & NotesDocument21 pagesD196 Study Guide Answers & NotesAsril Doank100% (1)

- Questions For IFRS HighlightedDocument28 pagesQuestions For IFRS HighlightedWowee Cruz100% (1)

- CHAPTER 7 Caselette - Audit of PPEDocument34 pagesCHAPTER 7 Caselette - Audit of PPErochielanciola60% (5)

- Understanding Financial Statements (Review and Analysis of Straub's Book)From EverandUnderstanding Financial Statements (Review and Analysis of Straub's Book)Rating: 5 out of 5 stars5/5 (5)

- Fixed Asset ManagementDocument85 pagesFixed Asset Managementrasheedshaikh2003100% (2)

- Income StatementDocument6 pagesIncome Statementkyrian chimaNo ratings yet

- FNCE Assignment Week 6Document10 pagesFNCE Assignment Week 6Rajeev ShahdadpuriNo ratings yet

- Income StatementDocument3 pagesIncome StatementMamta LallNo ratings yet

- Week 15 Lesson 11Document53 pagesWeek 15 Lesson 11D A M N E R ANo ratings yet

- Accounting ReportDocument23 pagesAccounting ReportAreeba FatimaNo ratings yet

- Masan Group CorporationDocument31 pagesMasan Group Corporationhồ nam longNo ratings yet

- How To Write A Traditional Business Plan: Step 1Document5 pagesHow To Write A Traditional Business Plan: Step 1Leslie Ann Elazegui UntalanNo ratings yet

- Financial Statement PresentationDocument33 pagesFinancial Statement Presentationcyrene jamnagueNo ratings yet

- All AccountingDocument122 pagesAll AccountingHassen ReshidNo ratings yet

- Financial TrainingDocument15 pagesFinancial TrainingGismon PereiraNo ratings yet

- Finance QuestionsDocument14 pagesFinance QuestionsGeetika YadavNo ratings yet

- Sat Pra 13Document7 pagesSat Pra 13Samyak KalaskarNo ratings yet

- Understanding The Income StatementDocument4 pagesUnderstanding The Income Statementluvujaya100% (1)

- FINFO Week 3 Learner GuideDocument14 pagesFINFO Week 3 Learner GuideAngelica Caballes TabaniaNo ratings yet

- Financial StatementsDocument8 pagesFinancial StatementsbouhaddihayetNo ratings yet

- What Is RevenueDocument31 pagesWhat Is RevenueLEARN WITH AGALYANo ratings yet

- Key Takeaways: DirectDocument13 pagesKey Takeaways: DirectSB CorporationNo ratings yet

- Managerial Finance, Financial Accounting and Analysis For Engineering Managers PDFDocument5 pagesManagerial Finance, Financial Accounting and Analysis For Engineering Managers PDFAshuriko KazuNo ratings yet

- Script For ReportingDocument14 pagesScript For Reportingvelasco.mhervin08No ratings yet

- Income Statement: Profit/Loss Account Dr. Satish Jangra (2009A229M)Document14 pagesIncome Statement: Profit/Loss Account Dr. Satish Jangra (2009A229M)Dr. Satish Jangra100% (1)

- Clo-3 Assignment: Chemical Engineering Economics 2016-CH-454Document9 pagesClo-3 Assignment: Chemical Engineering Economics 2016-CH-454ali ayanNo ratings yet

- Task 4b UBODocument3 pagesTask 4b UBOEdem Augustin AGBEVENo ratings yet

- Bookkeeping Module 1Document11 pagesBookkeeping Module 1Cindy TorresNo ratings yet

- Final Accounts LessonDocument12 pagesFinal Accounts LessonSiham KhayetNo ratings yet

- CH 4 - Financial AnalysisDocument13 pagesCH 4 - Financial AnalysisbavanthinilNo ratings yet

- Business Notes: Reak Even AnalysisDocument8 pagesBusiness Notes: Reak Even AnalysisIvyNo ratings yet

- Proforma Fin Statement AssignmentDocument11 pagesProforma Fin Statement Assignmentashoo khoslaNo ratings yet

- Sample Operational Financial Analysis ReportDocument8 pagesSample Operational Financial Analysis ReportValentinorossiNo ratings yet

- Financial Accounting: Sir Syed Adeel Ali BukhariDocument25 pagesFinancial Accounting: Sir Syed Adeel Ali Bukhariadeelali849714No ratings yet

- Guide To Financial TermsDocument21 pagesGuide To Financial TermsShahrokh Paravarzar100% (1)

- Terms of Share MarketDocument6 pagesTerms of Share Marketsearchanirban6474No ratings yet

- Financial Accounting & AnalysisDocument5 pagesFinancial Accounting & AnalysisSourav SaraswatNo ratings yet

- Sample Operational Financial Analysis ReportDocument13 pagesSample Operational Financial Analysis Reportshivkumara27No ratings yet

- Fm108 ModuleDocument17 pagesFm108 ModuleKarl Dennis TiansayNo ratings yet

- Key Financial Performance IndicatorsDocument19 pagesKey Financial Performance Indicatorsmariana.zamudio7aNo ratings yet

- Assignment On SCMDocument5 pagesAssignment On SCMcattiger123No ratings yet

- VU Lesson 8Document5 pagesVU Lesson 8ranawaseem100% (1)

- Lecture Three Chapter FiveDocument4 pagesLecture Three Chapter Fivebouchra bouchraNo ratings yet

- What Is The Statement of Comprehensive Income?: EquityDocument4 pagesWhat Is The Statement of Comprehensive Income?: EquityKatherine Canisguin AlvarecoNo ratings yet

- finance conceptsDocument15 pagesfinance conceptsgodwillinno1997No ratings yet

- Information Sheet - BKKPG-8 - Preparing Financial StatementsDocument10 pagesInformation Sheet - BKKPG-8 - Preparing Financial StatementsEron Roi Centina-gacutanNo ratings yet

- Financial Accounting: Salal Durrani 2020Document12 pagesFinancial Accounting: Salal Durrani 2020Rahat BatoolNo ratings yet

- Financial Analysis FundamentalsDocument12 pagesFinancial Analysis FundamentalsAni Dwi Rahmanti RNo ratings yet

- Sevilla, Renz Marie A. Bsba FM 2-C: Assignment # 2Document4 pagesSevilla, Renz Marie A. Bsba FM 2-C: Assignment # 2Gerald Noveda RomanNo ratings yet

- AssignmentDocument4 pagesAssignmentRithik TiwariNo ratings yet

- Unit 3 Assignment 2 Task 2Document4 pagesUnit 3 Assignment 2 Task 2Noor KilaniNo ratings yet

- Profit and Loss AccountDocument9 pagesProfit and Loss AccountMurad Shah PatelNo ratings yet

- Topics For The Exam 2ND BaccDocument4 pagesTopics For The Exam 2ND BaccJose rendonNo ratings yet

- Interpretation On RatiosDocument3 pagesInterpretation On RatiosLorraine CalderonNo ratings yet

- Week 004 - Module Statement of Comprehensive Income IDocument7 pagesWeek 004 - Module Statement of Comprehensive Income IJulia AcostaNo ratings yet

- Chapter-3 FINANCIAL STATEMENT PREPARATIONDocument21 pagesChapter-3 FINANCIAL STATEMENT PREPARATIONWoldeNo ratings yet

- Questions DuresDocument25 pagesQuestions DuresAnna-Maria Müller-SchmidtNo ratings yet

- Financial PlanDocument20 pagesFinancial PlanHarold FilomenoNo ratings yet

- A Study On Profitability Analysis atDocument13 pagesA Study On Profitability Analysis atAsishNo ratings yet

- How To Read A Financial StatementDocument23 pagesHow To Read A Financial Statementbuvana1980No ratings yet

- Income Statement Balance SheetDocument19 pagesIncome Statement Balance SheetJeff Lacasandile100% (2)

- A Poem About Alcoholism, Drugs, Suicide and Murder. - B.U.XD.Document1 pageA Poem About Alcoholism, Drugs, Suicide and Murder. - B.U.XD.henaa sssaaaaeeeettNo ratings yet

- A Short Hilarious Drunk Story From 1990's Brooklyn - B.U.XD.Document1 pageA Short Hilarious Drunk Story From 1990's Brooklyn - B.U.XD.henaa sssaaaaeeeettNo ratings yet

- A Sad TaleDocument1 pageA Sad Talehenaa sssaaaaeeeettNo ratings yet

- A Short Story About Thumbs - B.u.xd.Document1 pageA Short Story About Thumbs - B.u.xd.henaa sssaaaaeeeettNo ratings yet

- January 2023 Private Candidate CentresDocument2 pagesJanuary 2023 Private Candidate Centreshenaa sssaaaaeeeettNo ratings yet

- An Easy Essay DocumentDocument1 pageAn Easy Essay Documenthenaa sssaaaaeeeettNo ratings yet

- Tata Motors Fundamental AnalysisDocument3 pagesTata Motors Fundamental AnalysisRahul RaghwaniNo ratings yet

- Module 1 & 2 Accounting For Special TransactionsDocument19 pagesModule 1 & 2 Accounting For Special TransactionsLian MaragayNo ratings yet

- Sip Project of MD Shamim AkhtarDocument89 pagesSip Project of MD Shamim AkhtarSami ZamaNo ratings yet

- Ratio Analysis of Arvind LTD.: Ratios Mar 21 Mar 20 Mar 19 Mar 18 Mar 17Document10 pagesRatio Analysis of Arvind LTD.: Ratios Mar 21 Mar 20 Mar 19 Mar 18 Mar 17simranNo ratings yet

- Financial AnalysisDocument73 pagesFinancial AnalysisAqdas ShahNo ratings yet

- FIS and Audit Statement TemplateDocument4 pagesFIS and Audit Statement Templateissam jendoubiNo ratings yet

- Coop Updates 3Document52 pagesCoop Updates 3nelsonpm81No ratings yet

- Quizzer - Revised Conceptual FrameworkDocument6 pagesQuizzer - Revised Conceptual FrameworkJohn Reiven Adaya Mendoza100% (1)

- What Is SFP?: Statement of Financial PositionDocument1 pageWhat Is SFP?: Statement of Financial PositionJessel Jean Lascoña OntialNo ratings yet

- Ar Pegadaian 2018 Eng V3 PDFDocument554 pagesAr Pegadaian 2018 Eng V3 PDFKamelia AgustiniNo ratings yet

- The Financial Statements: Chapter OutlineDocument15 pagesThe Financial Statements: Chapter OutlineBhagaban DasNo ratings yet

- ACCA F8 - AUDIT RISK by Alan Biju Palak ACCADocument5 pagesACCA F8 - AUDIT RISK by Alan Biju Palak ACCAkasimranjhaNo ratings yet

- Statement of Cash Flows and Book Value Per Share - Group 4Document67 pagesStatement of Cash Flows and Book Value Per Share - Group 4Karen MagsayoNo ratings yet

- Worksheet - Income Sheet and Form Series 18 AICPA, AICPA Risk of Material Misstatement WorksheetsDocument20 pagesWorksheet - Income Sheet and Form Series 18 AICPA, AICPA Risk of Material Misstatement WorksheetswellawalalasithNo ratings yet

- 1 20180905052123Document194 pages1 20180905052123Gupllo Kin'emonJrNo ratings yet

- Case Study November 2010 Exam Paper ICAEWDocument20 pagesCase Study November 2010 Exam Paper ICAEWmanofhonourNo ratings yet

- NolascoDocument23 pagesNolascojuztine dofitasNo ratings yet

- IPSAS Detil StandardDocument94 pagesIPSAS Detil StandardMaya IndriNo ratings yet

- PT MNC Vision Networks TBK - 31 Desember 2021 PDFDocument70 pagesPT MNC Vision Networks TBK - 31 Desember 2021 PDFSULTHAN ATHAYA AWDIHANSYAHNo ratings yet

- Beams10e - Ch02 Stock Investments-Investor Accounting and ReportingDocument37 pagesBeams10e - Ch02 Stock Investments-Investor Accounting and ReportingNadiaAmaliaNo ratings yet

- Project DetailsDocument1,325 pagesProject DetailsShrikanth SolaNo ratings yet

- AccountingDocument4 pagesAccountingAnimaw YayehNo ratings yet

- Investment and Decision Analysis For Petroleum ExplorationDocument24 pagesInvestment and Decision Analysis For Petroleum Explorationsandro0112No ratings yet

- BAFACR16 04 Problem IllustrationsDocument3 pagesBAFACR16 04 Problem IllustrationsThats BellaNo ratings yet

- IPCC MTP2 AccountingDocument7 pagesIPCC MTP2 AccountingBalaji SiddhuNo ratings yet

- The Trading and Profit and Loss Account and The Balance SheetDocument62 pagesThe Trading and Profit and Loss Account and The Balance SheetMir AqibNo ratings yet

- There Are Some Major Key Performance Indicators For Chemical Industry: 1. FinancialDocument3 pagesThere Are Some Major Key Performance Indicators For Chemical Industry: 1. FinancialsonuNo ratings yet