Download as pdf or txt

You might also like

- Papermaking 2017Document7 pagesPapermaking 2017quizizz section4No ratings yet

- Module 1 (Database Management in Construction)Document42 pagesModule 1 (Database Management in Construction)MARTHIE JASELLYN LOPENANo ratings yet

- Jindal Steel - Swot AnalysisDocument6 pagesJindal Steel - Swot AnalysisRitesh JainNo ratings yet

- Management Discussion and Analysis: Global Economic Scenario & Outlook A) Macro-Economic ConditionsDocument3 pagesManagement Discussion and Analysis: Global Economic Scenario & Outlook A) Macro-Economic Conditionsravi.youNo ratings yet

- Market Analysis 538Document7 pagesMarket Analysis 538checkoutdanielNo ratings yet

- The Health and Growth Potential of The Steel Manufacturing Industries in SADocument94 pagesThe Health and Growth Potential of The Steel Manufacturing Industries in SAShumani PharamelaNo ratings yet

- Chapter 6 - Risk Analysis and Mitigation: Cost OverrunDocument4 pagesChapter 6 - Risk Analysis and Mitigation: Cost OverrunISHITA GROVERNo ratings yet

- 7 Isl Directors Report 2020pdfDocument5 pages7 Isl Directors Report 2020pdfMohsin Khan NiaziNo ratings yet

- Impact of COVID-19 On Steel IndustryDocument15 pagesImpact of COVID-19 On Steel IndustryVishal Advani100% (1)

- Management Discussion and Analysis: Business ReviewDocument10 pagesManagement Discussion and Analysis: Business Reviewshamanthshami623No ratings yet

- Stainless Steel Magazine August 2012 PDFDocument36 pagesStainless Steel Magazine August 2012 PDFeugenio.gutenbertNo ratings yet

- Copper Market Analysis RFC Ambrian May 2022Document30 pagesCopper Market Analysis RFC Ambrian May 2022qleapNo ratings yet

- 59 334 6794 File PDF 1499150181Document8 pages59 334 6794 File PDF 1499150181Nachiappan ArumugamNo ratings yet

- Hindalco Annual Report 2019 PDFDocument379 pagesHindalco Annual Report 2019 PDFDharmnath Prasad Srivatava100% (1)

- Global Steel Market Outlook 2021 Cumic SteelDocument13 pagesGlobal Steel Market Outlook 2021 Cumic SteelBrion Bara IndonesiaNo ratings yet

- Strama (Threats)Document110 pagesStrama (Threats)joshNo ratings yet

- CRISIL Melting-Steel April 2020Document8 pagesCRISIL Melting-Steel April 2020Puneet367No ratings yet

- Metal Mining Sector Update - MNC SekuritasDocument8 pagesMetal Mining Sector Update - MNC SekuritasZhuanjian LiuNo ratings yet

- Report-Changing Economies of SteelDocument16 pagesReport-Changing Economies of SteelprtapbistNo ratings yet

- Wcms 746917Document6 pagesWcms 746917Maryalyn SutilNo ratings yet

- MA EngDocument7 pagesMA Engthoolakshay193No ratings yet

- Automotive Industry Update: Coronavirus ImpactDocument15 pagesAutomotive Industry Update: Coronavirus ImpactShshankNo ratings yet

- Product Management: Assignment 2 MidtermDocument17 pagesProduct Management: Assignment 2 MidtermJirecho CatapangNo ratings yet

- Extract of Report of The Working Group On Steel Industry For The Twelfth Five Year Plan (2012 - 2017) Ministry of SteelDocument15 pagesExtract of Report of The Working Group On Steel Industry For The Twelfth Five Year Plan (2012 - 2017) Ministry of SteelSuraj ShawNo ratings yet

- Stainless Steel September 2010Document36 pagesStainless Steel September 2010Joshua WalkerNo ratings yet

- Inside Track 194 Oct 12 2021 DesbloqueadoDocument46 pagesInside Track 194 Oct 12 2021 Desbloqueadojose de la cruzNo ratings yet

- Aluminum IndustryDocument5 pagesAluminum IndustryAkshay PatelNo ratings yet

- Wind Power Report 2010Document50 pagesWind Power Report 2010sebascianNo ratings yet

- Metals and Mining Industry Outlook 2023 Big Picture ReportDocument14 pagesMetals and Mining Industry Outlook 2023 Big Picture ReportLeandro OliveiraNo ratings yet

- Aluminium LeaderSpeak 2020Document68 pagesAluminium LeaderSpeak 2020Anver AkperovNo ratings yet

- Annual Report 2020Document23 pagesAnnual Report 2020dsfdsNo ratings yet

- BTIG OCTG Jan 28 2021Document18 pagesBTIG OCTG Jan 28 2021michaellunetteNo ratings yet

- Middle East Steel Supplement 2012Document24 pagesMiddle East Steel Supplement 2012Rajib ChatterjeeNo ratings yet

- Gfsec Ministerial Report 2021Document61 pagesGfsec Ministerial Report 2021regallydivineNo ratings yet

- Mbdaily 20150430Document34 pagesMbdaily 20150430ClaudiaKlausyNo ratings yet

- Steel CRGPDocument7 pagesSteel CRGPPrakhar RatheeNo ratings yet

- Methods Are We Going To Implement For Concentration 2222Document3 pagesMethods Are We Going To Implement For Concentration 2222Mash RanoNo ratings yet

- Chairman'S Address: Dear Esteemed MembersDocument7 pagesChairman'S Address: Dear Esteemed MembersSFDC TESTNo ratings yet

- Latest Developments in Steelmaking Capacity 2023Document58 pagesLatest Developments in Steelmaking Capacity 2023Hossam AbdelhalimNo ratings yet

- 2022年全球汽车供应商研究Document9 pages2022年全球汽车供应商研究jack allenNo ratings yet

- Bangladesh Industrial Sector and Challenges AheadDocument17 pagesBangladesh Industrial Sector and Challenges AheadGSO-1 R&PNo ratings yet

- Eurofer Quarter4 2020 Report - 201027 002Document27 pagesEurofer Quarter4 2020 Report - 201027 002ehtesabiNo ratings yet

- B0611 GLDocument36 pagesB0611 GLArnu Felix CamposNo ratings yet

- Business Model of Steel IndustryDocument3 pagesBusiness Model of Steel IndustrySmaran Pathak67% (3)

- Us Eri Ogc Report 2021Document11 pagesUs Eri Ogc Report 2021Truman LauNo ratings yet

- Indian Coal SectorDocument9 pagesIndian Coal Sectorhimadri.banerji60No ratings yet

- Critical Financial Problems: Q1. What Are The Situations in The Steel Industry in 2006?Document1 pageCritical Financial Problems: Q1. What Are The Situations in The Steel Industry in 2006?debmatraNo ratings yet

- Eco Project ReportDocument21 pagesEco Project Reportswapnil_thakre_1No ratings yet

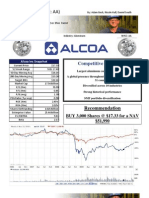

- Alcoa SwotDocument44 pagesAlcoa SwotKURATHEESH1No ratings yet

- ICRA-Ferrous MetalsDocument9 pagesICRA-Ferrous MetalsRohan ShahNo ratings yet

- The Impact of COVID-19 On The Steel IndustryDocument25 pagesThe Impact of COVID-19 On The Steel IndustryAyesha KhalidNo ratings yet

- Tata Steel Stock AnalysisDocument50 pagesTata Steel Stock AnalysisAmitabh VatsyaNo ratings yet

- Global and Regional Developments in Primary and Secondary Lead SupplyDocument4 pagesGlobal and Regional Developments in Primary and Secondary Lead SupplyetayojcNo ratings yet

- CobaltInstitute Market Report 2020Document20 pagesCobaltInstitute Market Report 2020Elie MaltzNo ratings yet

- Effects of Covid-19 On Energy InvestmentDocument4 pagesEffects of Covid-19 On Energy InvestmentSaagar SenniNo ratings yet

- Nucor PDFDocument63 pagesNucor PDFJorge ViceNo ratings yet

- 37 79 1 SMDocument23 pages37 79 1 SMAdry AdrytzaNo ratings yet

- R&D in Mining Industry - Knowledge RidgeDocument10 pagesR&D in Mining Industry - Knowledge RidgeВладимир ШалагинNo ratings yet

- Demand-Supply Gap (Rating-5) : TH TH THDocument9 pagesDemand-Supply Gap (Rating-5) : TH TH THShreyansh ParakhNo ratings yet

- Identifying A Steel StockDocument4 pagesIdentifying A Steel Stockanalyst_anil14No ratings yet

- COVID-19 and Energy Sector Development in Asia and the Pacific: Guidance NoteFrom EverandCOVID-19 and Energy Sector Development in Asia and the Pacific: Guidance NoteNo ratings yet

- bosch_sventa_flyer_v1_digital_1 (2)Document2 pagesbosch_sventa_flyer_v1_digital_1 (2)rohithranjan2011No ratings yet

- Blor To AhmedbDocument2 pagesBlor To Ahmedbrohithranjan2011No ratings yet

- Ahmed To BlorDocument2 pagesAhmed To Blorrohithranjan2011No ratings yet

- Receipt 26feb2024 132306Document1 pageReceipt 26feb2024 132306rohithranjan2011No ratings yet

- 23BLR0052580Document2 pages23BLR0052580rohithranjan2011No ratings yet

- Invoice: Thank You!Document1 pageInvoice: Thank You!rohithranjan2011No ratings yet

- Item 12bDocument23 pagesItem 12brohithranjan2011No ratings yet

- Award Scheme For Secondary Steel Producers 1.0 Background:: Page 1 of 6Document6 pagesAward Scheme For Secondary Steel Producers 1.0 Background:: Page 1 of 6rohithranjan2011No ratings yet

- Iron Steel 2finalDocument22 pagesIron Steel 2finalrohithranjan2011No ratings yet

- DPR TemplateDocument2 pagesDPR TemplateAM PRABAKARANNo ratings yet

- BC LetterDocument10 pagesBC LetterMehnoor SiddiquiNo ratings yet

- CSE116 Spring 2017 SyllabusDocument7 pagesCSE116 Spring 2017 SyllabusBlakeHurlburtNo ratings yet

- Suffolk Times Classifieds and Service Directory: Oct. 26, 2017Document13 pagesSuffolk Times Classifieds and Service Directory: Oct. 26, 2017TimesreviewNo ratings yet

- Derivative SecuritiesDocument3 pagesDerivative SecuritiesWataru TeradaNo ratings yet

- Hammad Hussian: Mass and Weight Gravitational Fields DensityDocument95 pagesHammad Hussian: Mass and Weight Gravitational Fields DensityRaiyaan BawanyNo ratings yet

- Cox OstromDocument20 pagesCox OstromPeterNo ratings yet

- Machine Learning Primer 108796Document15 pagesMachine Learning Primer 108796Vinay Nagnath JokareNo ratings yet

- Summaries of IFRSs and IASsDocument2 pagesSummaries of IFRSs and IASsnehseulNo ratings yet

- Calculation of Natural Gas Isentropic ExponentDocument8 pagesCalculation of Natural Gas Isentropic ExponentsekharsamyNo ratings yet

- FX2N-16DNET Devicenet User ManualDocument126 pagesFX2N-16DNET Devicenet User ManualNguyen QuanNo ratings yet

- Woodworks Design Example - Four-Story Wood-Frame Structure Over Podium SlabDocument52 pagesWoodworks Design Example - Four-Story Wood-Frame Structure Over Podium Slabcancery0707No ratings yet

- Alyssa Locken Resume Jan 2021Document3 pagesAlyssa Locken Resume Jan 2021api-544203584No ratings yet

- Zaher Master ThesisDocument110 pagesZaher Master Thesisikhlas100% (1)

- List of NFPA Codes and StandardsDocument28 pagesList of NFPA Codes and StandardsjteranlavillaNo ratings yet

- Caption Text Tgas Bhs InggrisDocument6 pagesCaption Text Tgas Bhs InggrisPangbaterek PekaryaNo ratings yet

- BDA PresentationsDocument26 pagesBDA PresentationsTejaswiniNo ratings yet

- Trend Micro Apex One: Endpoint Security RedefinedDocument2 pagesTrend Micro Apex One: Endpoint Security RedefinedtestNo ratings yet

- T10 Government Accounting PDFDocument9 pagesT10 Government Accounting PDFnicahNo ratings yet

- Assessment ProcedureDocument8 pagesAssessment ProcedureAbhishek SharmaNo ratings yet

- Literature Review On Motivation TheoriesDocument9 pagesLiterature Review On Motivation Theoriesafdtslawm100% (1)

- World Economic Forum - Annual Report 2000/2001Document20 pagesWorld Economic Forum - Annual Report 2000/2001World Economic Forum100% (2)

- FULL TEXT - President Duterte's 2018 State of The Nation Address PDFDocument37 pagesFULL TEXT - President Duterte's 2018 State of The Nation Address PDFDarlene VenturaNo ratings yet

- Sta 9 1Document125 pagesSta 9 1Jayaprakash Polimetla100% (1)

- JDM 16305Document9 pagesJDM 16305mega smallNo ratings yet

- Organisational Behaviour EXAM 2022Document3 pagesOrganisational Behaviour EXAM 2022venyena ericNo ratings yet

- BITS Herald Summer Issue 2013Document23 pagesBITS Herald Summer Issue 2013Bits Herald100% (1)

- The Proprietary Theory and The Entity Theory of Corporate Enterpr PDFDocument242 pagesThe Proprietary Theory and The Entity Theory of Corporate Enterpr PDFAnusha GowdaNo ratings yet