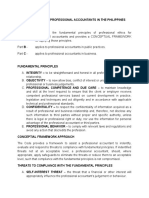

COE. Act. 9298

COE. Act. 9298

You might also like

- Sydney Safety Confined Space Rescue PlanDocument4 pagesSydney Safety Confined Space Rescue PlanFranscois Van RooyenNo ratings yet

- Chapter Three: Professional Ethics and Legal Liability of AuditorsDocument35 pagesChapter Three: Professional Ethics and Legal Liability of Auditorseferem100% (1)

- Mas Practice Standards and EthicalconsiderationsDocument6 pagesMas Practice Standards and EthicalconsiderationsRolanElumbreNo ratings yet

- Mas Practice Standards and Ethical ConsiderationsACDocument3 pagesMas Practice Standards and Ethical ConsiderationsACLorenz BaguioNo ratings yet

- Assurance Principle ReportDocument4 pagesAssurance Principle ReportVictoria Lovely May MediloNo ratings yet

- Code of EthicsDocument78 pagesCode of EthicsNeriza PonceNo ratings yet

- Professional Ethics P2Document19 pagesProfessional Ethics P2chandrsenNo ratings yet

- Code of Ethics - EditedDocument76 pagesCode of Ethics - EditedAaron Mañacap100% (1)

- Bacc307 Assignment 1Document7 pagesBacc307 Assignment 1Denny ChakauyaNo ratings yet

- Code of EthicsDocument5 pagesCode of EthicsZeus GamoNo ratings yet

- WV&PE Lesson 3Document14 pagesWV&PE Lesson 3Daniel S. GonzalesNo ratings yet

- Code of EthicsDocument37 pagesCode of EthicsDawn Rei Dangkiw100% (1)

- Code of Ethics Reviewer - CompressDocument44 pagesCode of Ethics Reviewer - CompressGlance Piscasio CruzNo ratings yet

- The Code of Professional Ethics of CPA-Tyrelle Garth R. Dela CruzDocument1 pageThe Code of Professional Ethics of CPA-Tyrelle Garth R. Dela CruzTyrelle Dela CruzNo ratings yet

- Accounting Ethics: Lect. Victor-Octavian Müller, PH.DDocument7 pagesAccounting Ethics: Lect. Victor-Octavian Müller, PH.DavalentinNo ratings yet

- Auditing TheoryDocument3 pagesAuditing TheoryJereza Joy LastreNo ratings yet

- Code of Ethics For Professional AccountantsDocument17 pagesCode of Ethics For Professional AccountantsJay Mark AbellarNo ratings yet

- Lecture Notes - Code of EthicsDocument5 pagesLecture Notes - Code of EthicsHalim Matuan MaamorNo ratings yet

- Code of Ethics For Professional Accountants in The PhilippinesDocument4 pagesCode of Ethics For Professional Accountants in The PhilippinesAlex Ong0% (1)

- Revised Code of Ethics For CPA's: BackgroundDocument6 pagesRevised Code of Ethics For CPA's: BackgroundMaria Lucy MendozaNo ratings yet

- BKAA 3023 Â " Topic 1 - Code of Ethics For AuditorsDocument20 pagesBKAA 3023 Â " Topic 1 - Code of Ethics For AuditorsDarren 雷丰威No ratings yet

- A$a L2 EditedDocument6 pagesA$a L2 EditedKimosop Isaac KipngetichNo ratings yet

- Ethical and Professional IssuesDocument3 pagesEthical and Professional Issuesmojoxig961No ratings yet

- The Code of Ethics For Cpas in The Philippines: Chapter SixDocument24 pagesThe Code of Ethics For Cpas in The Philippines: Chapter SixQueenie QuisidoNo ratings yet

- Adv 12Document15 pagesAdv 12Asfawosen DingamaNo ratings yet

- Final Exam Good GovernanceDocument2 pagesFinal Exam Good GovernanceJoylyn CombongNo ratings yet

- Code of EthicsDocument5 pagesCode of EthicsAira Shynne AsperaNo ratings yet

- Code of Ethics: Prof. Zeus A. Aboy, CPA MBA EDL (Candidate)Document75 pagesCode of Ethics: Prof. Zeus A. Aboy, CPA MBA EDL (Candidate)Io AyaNo ratings yet

- The Code of Professional EthicsDocument33 pagesThe Code of Professional EthicsLaezelie PalajeNo ratings yet

- Code of Ethics For Professional Accountants: B&P Inter ConsultDocument12 pagesCode of Ethics For Professional Accountants: B&P Inter ConsultKalimullah KhanNo ratings yet

- Unit 2 Regulation of The Practice of Public Accountancy and Within The Accounting FirmDocument136 pagesUnit 2 Regulation of The Practice of Public Accountancy and Within The Accounting FirmDia Mae Ablao GenerosoNo ratings yet

- Mas Practice Standards and Ethical Considerations MAS Practice Standards Personal CharacteristicsDocument4 pagesMas Practice Standards and Ethical Considerations MAS Practice Standards Personal CharacteristicsRoderick RonidelNo ratings yet

- The Regulatory Framework, Ethics and Conceptual FrameworkDocument14 pagesThe Regulatory Framework, Ethics and Conceptual FrameworkMelvin AmohNo ratings yet

- Code of Ethics: For Professional AccountantsDocument130 pagesCode of Ethics: For Professional AccountantsSalvador BrionesNo ratings yet

- Code of Ethics For AccountantsDocument49 pagesCode of Ethics For AccountantsAlly CapacioNo ratings yet

- Accounting Ethics: Lect. Victor-Octavian Müller, PH.DDocument9 pagesAccounting Ethics: Lect. Victor-Octavian Müller, PH.DavalentinNo ratings yet

- Chapter One: Ethical Issues and Financial Statement Fraud in Advanced AccountingDocument74 pagesChapter One: Ethical Issues and Financial Statement Fraud in Advanced AccountingYismawNo ratings yet

- 08 Code of Ethics For CPAs in The PhilippinesDocument12 pages08 Code of Ethics For CPAs in The PhilippinesBack Up StorageNo ratings yet

- Code of Ethics of Professional AccountantsDocument3 pagesCode of Ethics of Professional AccountantsYamateNo ratings yet

- 210 Professional AppointmentDocument9 pages210 Professional AppointmentHendry TupaiNo ratings yet

- The Code of Professional EthicsDocument50 pagesThe Code of Professional EthicsMicaela MarimlaNo ratings yet

- 4 Quality ControlDocument10 pages4 Quality ControlMoffat MakambaNo ratings yet

- Auditors Independence Review - 1Document22 pagesAuditors Independence Review - 1Mohammad Abu Kawsar FcaNo ratings yet

- Code of Ethics For Professional Accountants in The PhilippinesDocument4 pagesCode of Ethics For Professional Accountants in The PhilippinesSarah GoNo ratings yet

- DEH-AC-2018-P-109 - M F F RusdhaDocument6 pagesDEH-AC-2018-P-109 - M F F Rusdhafathima rusdhaNo ratings yet

- Code of Ethics For Professional Accountants-2Document25 pagesCode of Ethics For Professional Accountants-2davidwijaya1986100% (1)

- Code of Ethics For Professional Accountants in The PhilippinesDocument3 pagesCode of Ethics For Professional Accountants in The Philippinesmac mercadoNo ratings yet

- 25.code of Ethics For Professional AccountantsDocument11 pages25.code of Ethics For Professional Accountantsbuxtone67% (3)

- Subject: - Law, Ethics and Management Bba Sem-VDocument31 pagesSubject: - Law, Ethics and Management Bba Sem-VsnehalNo ratings yet

- BRM Assignment Done by Omar Gamal Tawfik 291800293: UnbiasedDocument2 pagesBRM Assignment Done by Omar Gamal Tawfik 291800293: UnbiasedOmar SoussaNo ratings yet

- The Revised Code of Ethics at A GlanceDocument11 pagesThe Revised Code of Ethics at A GlanceDan PatrickNo ratings yet

- Professional Accountant Ought To Be Straightforward and Honest in Conduct of All Professional Services IntegrityDocument17 pagesProfessional Accountant Ought To Be Straightforward and Honest in Conduct of All Professional Services IntegrityVictorNo ratings yet

- Audit Lecture #6 - Ethical ThreatsDocument9 pagesAudit Lecture #6 - Ethical ThreatsAkira CambridgeNo ratings yet

- 03.2 Handbook of The International Code of Ethics For Professional AccountantsDocument92 pages03.2 Handbook of The International Code of Ethics For Professional AccountantsnuggsNo ratings yet

- Code of Ethics Updated PDFDocument130 pagesCode of Ethics Updated PDFSalvador BrionesNo ratings yet

- Audit Chapter 14Document4 pagesAudit Chapter 14Areej AzharNo ratings yet

- Lecturer 2 (Ii) - Professional EthicsDocument41 pagesLecturer 2 (Ii) - Professional EthicskhooNo ratings yet

- Textbook of Urgent Care Management: Chapter 21, Employment Contracts and CompensationFrom EverandTextbook of Urgent Care Management: Chapter 21, Employment Contracts and CompensationNo ratings yet

- An Introduction to Anti-Bribery Management Systems (BS 10500): Doing right thingsFrom EverandAn Introduction to Anti-Bribery Management Systems (BS 10500): Doing right thingsNo ratings yet

- Chapter 7Document6 pagesChapter 7Mark Kenneth ParagasNo ratings yet

- Chapter 7 InuDocument4 pagesChapter 7 InuMark Kenneth ParagasNo ratings yet

- Chapter 10 IdenDocument4 pagesChapter 10 IdenMark Kenneth ParagasNo ratings yet

- Chapter 10Document8 pagesChapter 10Mark Kenneth ParagasNo ratings yet

- Management Science Chpt6Document16 pagesManagement Science Chpt6Mark Kenneth ParagasNo ratings yet

- Accounting Information SystemDocument12 pagesAccounting Information SystemMark Kenneth ParagasNo ratings yet

- Management Science chpt8Document20 pagesManagement Science chpt8Mark Kenneth ParagasNo ratings yet

- Management Science chpt9Document10 pagesManagement Science chpt9Mark Kenneth ParagasNo ratings yet

- Discussionquestions: Making Research DecisionsDocument2 pagesDiscussionquestions: Making Research DecisionsRodolfo Mapada Jr.No ratings yet

- Chapter 5-Indigo (Flamingo) NotesDocument10 pagesChapter 5-Indigo (Flamingo) NotesPrince PandeyNo ratings yet

- Who, Summary NotesDocument12 pagesWho, Summary NotesIvan Lohr100% (2)

- Shafer Landau Fundamentals5e Lectureppt Ch22Document11 pagesShafer Landau Fundamentals5e Lectureppt Ch22Pro GamerNo ratings yet

- Toyota Hiace 2017 01 Workshop Service ManualDocument22 pagesToyota Hiace 2017 01 Workshop Service Manualkatherineaguilar241202tne100% (116)

- Week 1 & 2 Module 1 & 2 - Social Issues & Professional PracticesDocument12 pagesWeek 1 & 2 Module 1 & 2 - Social Issues & Professional Practiceslynn may tanNo ratings yet

- B - Code of Ethics (Legal and Governance)Document15 pagesB - Code of Ethics (Legal and Governance)Pranshu SahasrabuddheNo ratings yet

- Universals and ParticularsDocument4 pagesUniversals and ParticularsFabioS ReportsNo ratings yet

- Tony Annese's Clinic Presentation - MHSFCADocument50 pagesTony Annese's Clinic Presentation - MHSFCADougSamuels100% (6)

- Headquarters University of Rizal System - Morong, Pililla, Cardona Rotc Unit 405 (RZL) CDC, 4Rcdg, Arescom Brgy - San Juan, Morong, RizalDocument7 pagesHeadquarters University of Rizal System - Morong, Pililla, Cardona Rotc Unit 405 (RZL) CDC, 4Rcdg, Arescom Brgy - San Juan, Morong, RizalJohn Patric MangantiNo ratings yet

- Learning Outcome 2 Identify Own Role & Responsibility Within A Team ContentsDocument12 pagesLearning Outcome 2 Identify Own Role & Responsibility Within A Team ContentsEmelson VertucioNo ratings yet

- Contract of Sale of GoodsDocument4 pagesContract of Sale of GoodsVanessa Evans CruzNo ratings yet

- Philippine Fake News EssayDocument5 pagesPhilippine Fake News EssayZyrrich RobertNo ratings yet

- 5ta Tarea de Ingles Avanzado IIDocument30 pages5ta Tarea de Ingles Avanzado IIabiel jimenezNo ratings yet

- Model Draft For Written Statement in The Court - of Civil Judge (DISTRICT - ), - SUIT NO. - OF 20XXDocument3 pagesModel Draft For Written Statement in The Court - of Civil Judge (DISTRICT - ), - SUIT NO. - OF 20XXSwaJeet KaDamNo ratings yet

- Omnibus Motion (Motion To Re-Open, Admit Answer and Delist: Republic of The PhilippinesDocument6 pagesOmnibus Motion (Motion To Re-Open, Admit Answer and Delist: Republic of The PhilippinesHIBA INTL. INC.No ratings yet

- Learning Exercise 2.6: THE BASIC VALUES OF THE FILIPINOS (Good Citizenship Clusters)Document7 pagesLearning Exercise 2.6: THE BASIC VALUES OF THE FILIPINOS (Good Citizenship Clusters)AngelaOrosiaDenilaNo ratings yet

- 2004 - Koh - Organisational Ethics and Employee Satisfaction and CommitmentDocument20 pages2004 - Koh - Organisational Ethics and Employee Satisfaction and CommitmentGeorgianaDîdălNo ratings yet

- Business Ethics in Action Lecture & Seminar 2Document29 pagesBusiness Ethics in Action Lecture & Seminar 2Shanuka SapugodaNo ratings yet

- Silibus - Law507 - Admin Law For AuthoritiesDocument3 pagesSilibus - Law507 - Admin Law For AuthoritiesiraNo ratings yet

- Sample DissertationDocument52 pagesSample DissertationBelfacinoNo ratings yet

- The Story of The Seagull and The Cat Who Taught Her To FlightDocument2 pagesThe Story of The Seagull and The Cat Who Taught Her To FlightHiếu Lê ĐắcNo ratings yet

- Confidentiality and Privacy: This Is Page 1 of 7Document7 pagesConfidentiality and Privacy: This Is Page 1 of 7api-534908963No ratings yet

- Englis L ExerciseDocument42 pagesEnglis L ExerciseSneha SharmaNo ratings yet

- In The Hon'Ble District Consumer Disputes Redressal Commission, Mumbai at MumbaiDocument7 pagesIn The Hon'Ble District Consumer Disputes Redressal Commission, Mumbai at MumbaiYaashik HenrageNo ratings yet

- Quiz 4 - Morgia - March 9, 2022Document2 pagesQuiz 4 - Morgia - March 9, 2022Cristina Crong MorgiaNo ratings yet

- Near Miss ReportDocument5 pagesNear Miss ReportAakash GuptaNo ratings yet

- Unit 3 Tender and ContractDocument4 pagesUnit 3 Tender and ContractswathikaNo ratings yet

- School of Law and GovernanceDocument3 pagesSchool of Law and GovernanceMelody EngNo ratings yet

Download as docx, pdf, or txt

You might also like

- Sydney Safety Confined Space Rescue PlanDocument4 pagesSydney Safety Confined Space Rescue PlanFranscois Van RooyenNo ratings yet

- Chapter Three: Professional Ethics and Legal Liability of AuditorsDocument35 pagesChapter Three: Professional Ethics and Legal Liability of Auditorseferem100% (1)

- Mas Practice Standards and EthicalconsiderationsDocument6 pagesMas Practice Standards and EthicalconsiderationsRolanElumbreNo ratings yet

- Mas Practice Standards and Ethical ConsiderationsACDocument3 pagesMas Practice Standards and Ethical ConsiderationsACLorenz BaguioNo ratings yet

- Assurance Principle ReportDocument4 pagesAssurance Principle ReportVictoria Lovely May MediloNo ratings yet

- Code of EthicsDocument78 pagesCode of EthicsNeriza PonceNo ratings yet

- Professional Ethics P2Document19 pagesProfessional Ethics P2chandrsenNo ratings yet

- Code of Ethics - EditedDocument76 pagesCode of Ethics - EditedAaron Mañacap100% (1)

- Bacc307 Assignment 1Document7 pagesBacc307 Assignment 1Denny ChakauyaNo ratings yet

- Code of EthicsDocument5 pagesCode of EthicsZeus GamoNo ratings yet

- WV&PE Lesson 3Document14 pagesWV&PE Lesson 3Daniel S. GonzalesNo ratings yet

- Code of EthicsDocument37 pagesCode of EthicsDawn Rei Dangkiw100% (1)

- Code of Ethics Reviewer - CompressDocument44 pagesCode of Ethics Reviewer - CompressGlance Piscasio CruzNo ratings yet

- The Code of Professional Ethics of CPA-Tyrelle Garth R. Dela CruzDocument1 pageThe Code of Professional Ethics of CPA-Tyrelle Garth R. Dela CruzTyrelle Dela CruzNo ratings yet

- Accounting Ethics: Lect. Victor-Octavian Müller, PH.DDocument7 pagesAccounting Ethics: Lect. Victor-Octavian Müller, PH.DavalentinNo ratings yet

- Auditing TheoryDocument3 pagesAuditing TheoryJereza Joy LastreNo ratings yet

- Code of Ethics For Professional AccountantsDocument17 pagesCode of Ethics For Professional AccountantsJay Mark AbellarNo ratings yet

- Lecture Notes - Code of EthicsDocument5 pagesLecture Notes - Code of EthicsHalim Matuan MaamorNo ratings yet

- Code of Ethics For Professional Accountants in The PhilippinesDocument4 pagesCode of Ethics For Professional Accountants in The PhilippinesAlex Ong0% (1)

- Revised Code of Ethics For CPA's: BackgroundDocument6 pagesRevised Code of Ethics For CPA's: BackgroundMaria Lucy MendozaNo ratings yet

- BKAA 3023 Â " Topic 1 - Code of Ethics For AuditorsDocument20 pagesBKAA 3023 Â " Topic 1 - Code of Ethics For AuditorsDarren 雷丰威No ratings yet

- A$a L2 EditedDocument6 pagesA$a L2 EditedKimosop Isaac KipngetichNo ratings yet

- Ethical and Professional IssuesDocument3 pagesEthical and Professional Issuesmojoxig961No ratings yet

- The Code of Ethics For Cpas in The Philippines: Chapter SixDocument24 pagesThe Code of Ethics For Cpas in The Philippines: Chapter SixQueenie QuisidoNo ratings yet

- Adv 12Document15 pagesAdv 12Asfawosen DingamaNo ratings yet

- Final Exam Good GovernanceDocument2 pagesFinal Exam Good GovernanceJoylyn CombongNo ratings yet

- Code of EthicsDocument5 pagesCode of EthicsAira Shynne AsperaNo ratings yet

- Code of Ethics: Prof. Zeus A. Aboy, CPA MBA EDL (Candidate)Document75 pagesCode of Ethics: Prof. Zeus A. Aboy, CPA MBA EDL (Candidate)Io AyaNo ratings yet

- The Code of Professional EthicsDocument33 pagesThe Code of Professional EthicsLaezelie PalajeNo ratings yet

- Code of Ethics For Professional Accountants: B&P Inter ConsultDocument12 pagesCode of Ethics For Professional Accountants: B&P Inter ConsultKalimullah KhanNo ratings yet

- Unit 2 Regulation of The Practice of Public Accountancy and Within The Accounting FirmDocument136 pagesUnit 2 Regulation of The Practice of Public Accountancy and Within The Accounting FirmDia Mae Ablao GenerosoNo ratings yet

- Mas Practice Standards and Ethical Considerations MAS Practice Standards Personal CharacteristicsDocument4 pagesMas Practice Standards and Ethical Considerations MAS Practice Standards Personal CharacteristicsRoderick RonidelNo ratings yet

- The Regulatory Framework, Ethics and Conceptual FrameworkDocument14 pagesThe Regulatory Framework, Ethics and Conceptual FrameworkMelvin AmohNo ratings yet

- Code of Ethics: For Professional AccountantsDocument130 pagesCode of Ethics: For Professional AccountantsSalvador BrionesNo ratings yet

- Code of Ethics For AccountantsDocument49 pagesCode of Ethics For AccountantsAlly CapacioNo ratings yet

- Accounting Ethics: Lect. Victor-Octavian Müller, PH.DDocument9 pagesAccounting Ethics: Lect. Victor-Octavian Müller, PH.DavalentinNo ratings yet

- Chapter One: Ethical Issues and Financial Statement Fraud in Advanced AccountingDocument74 pagesChapter One: Ethical Issues and Financial Statement Fraud in Advanced AccountingYismawNo ratings yet

- 08 Code of Ethics For CPAs in The PhilippinesDocument12 pages08 Code of Ethics For CPAs in The PhilippinesBack Up StorageNo ratings yet

- Code of Ethics of Professional AccountantsDocument3 pagesCode of Ethics of Professional AccountantsYamateNo ratings yet

- 210 Professional AppointmentDocument9 pages210 Professional AppointmentHendry TupaiNo ratings yet

- The Code of Professional EthicsDocument50 pagesThe Code of Professional EthicsMicaela MarimlaNo ratings yet

- 4 Quality ControlDocument10 pages4 Quality ControlMoffat MakambaNo ratings yet

- Auditors Independence Review - 1Document22 pagesAuditors Independence Review - 1Mohammad Abu Kawsar FcaNo ratings yet

- Code of Ethics For Professional Accountants in The PhilippinesDocument4 pagesCode of Ethics For Professional Accountants in The PhilippinesSarah GoNo ratings yet

- DEH-AC-2018-P-109 - M F F RusdhaDocument6 pagesDEH-AC-2018-P-109 - M F F Rusdhafathima rusdhaNo ratings yet

- Code of Ethics For Professional Accountants-2Document25 pagesCode of Ethics For Professional Accountants-2davidwijaya1986100% (1)

- Code of Ethics For Professional Accountants in The PhilippinesDocument3 pagesCode of Ethics For Professional Accountants in The Philippinesmac mercadoNo ratings yet

- 25.code of Ethics For Professional AccountantsDocument11 pages25.code of Ethics For Professional Accountantsbuxtone67% (3)

- Subject: - Law, Ethics and Management Bba Sem-VDocument31 pagesSubject: - Law, Ethics and Management Bba Sem-VsnehalNo ratings yet

- BRM Assignment Done by Omar Gamal Tawfik 291800293: UnbiasedDocument2 pagesBRM Assignment Done by Omar Gamal Tawfik 291800293: UnbiasedOmar SoussaNo ratings yet

- The Revised Code of Ethics at A GlanceDocument11 pagesThe Revised Code of Ethics at A GlanceDan PatrickNo ratings yet

- Professional Accountant Ought To Be Straightforward and Honest in Conduct of All Professional Services IntegrityDocument17 pagesProfessional Accountant Ought To Be Straightforward and Honest in Conduct of All Professional Services IntegrityVictorNo ratings yet

- Audit Lecture #6 - Ethical ThreatsDocument9 pagesAudit Lecture #6 - Ethical ThreatsAkira CambridgeNo ratings yet

- 03.2 Handbook of The International Code of Ethics For Professional AccountantsDocument92 pages03.2 Handbook of The International Code of Ethics For Professional AccountantsnuggsNo ratings yet

- Code of Ethics Updated PDFDocument130 pagesCode of Ethics Updated PDFSalvador BrionesNo ratings yet

- Audit Chapter 14Document4 pagesAudit Chapter 14Areej AzharNo ratings yet

- Lecturer 2 (Ii) - Professional EthicsDocument41 pagesLecturer 2 (Ii) - Professional EthicskhooNo ratings yet

- Textbook of Urgent Care Management: Chapter 21, Employment Contracts and CompensationFrom EverandTextbook of Urgent Care Management: Chapter 21, Employment Contracts and CompensationNo ratings yet

- An Introduction to Anti-Bribery Management Systems (BS 10500): Doing right thingsFrom EverandAn Introduction to Anti-Bribery Management Systems (BS 10500): Doing right thingsNo ratings yet

- Chapter 7Document6 pagesChapter 7Mark Kenneth ParagasNo ratings yet

- Chapter 7 InuDocument4 pagesChapter 7 InuMark Kenneth ParagasNo ratings yet

- Chapter 10 IdenDocument4 pagesChapter 10 IdenMark Kenneth ParagasNo ratings yet

- Chapter 10Document8 pagesChapter 10Mark Kenneth ParagasNo ratings yet

- Management Science Chpt6Document16 pagesManagement Science Chpt6Mark Kenneth ParagasNo ratings yet

- Accounting Information SystemDocument12 pagesAccounting Information SystemMark Kenneth ParagasNo ratings yet

- Management Science chpt8Document20 pagesManagement Science chpt8Mark Kenneth ParagasNo ratings yet

- Management Science chpt9Document10 pagesManagement Science chpt9Mark Kenneth ParagasNo ratings yet

- Discussionquestions: Making Research DecisionsDocument2 pagesDiscussionquestions: Making Research DecisionsRodolfo Mapada Jr.No ratings yet

- Chapter 5-Indigo (Flamingo) NotesDocument10 pagesChapter 5-Indigo (Flamingo) NotesPrince PandeyNo ratings yet

- Who, Summary NotesDocument12 pagesWho, Summary NotesIvan Lohr100% (2)

- Shafer Landau Fundamentals5e Lectureppt Ch22Document11 pagesShafer Landau Fundamentals5e Lectureppt Ch22Pro GamerNo ratings yet

- Toyota Hiace 2017 01 Workshop Service ManualDocument22 pagesToyota Hiace 2017 01 Workshop Service Manualkatherineaguilar241202tne100% (116)

- Week 1 & 2 Module 1 & 2 - Social Issues & Professional PracticesDocument12 pagesWeek 1 & 2 Module 1 & 2 - Social Issues & Professional Practiceslynn may tanNo ratings yet

- B - Code of Ethics (Legal and Governance)Document15 pagesB - Code of Ethics (Legal and Governance)Pranshu SahasrabuddheNo ratings yet

- Universals and ParticularsDocument4 pagesUniversals and ParticularsFabioS ReportsNo ratings yet

- Tony Annese's Clinic Presentation - MHSFCADocument50 pagesTony Annese's Clinic Presentation - MHSFCADougSamuels100% (6)

- Headquarters University of Rizal System - Morong, Pililla, Cardona Rotc Unit 405 (RZL) CDC, 4Rcdg, Arescom Brgy - San Juan, Morong, RizalDocument7 pagesHeadquarters University of Rizal System - Morong, Pililla, Cardona Rotc Unit 405 (RZL) CDC, 4Rcdg, Arescom Brgy - San Juan, Morong, RizalJohn Patric MangantiNo ratings yet

- Learning Outcome 2 Identify Own Role & Responsibility Within A Team ContentsDocument12 pagesLearning Outcome 2 Identify Own Role & Responsibility Within A Team ContentsEmelson VertucioNo ratings yet

- Contract of Sale of GoodsDocument4 pagesContract of Sale of GoodsVanessa Evans CruzNo ratings yet

- Philippine Fake News EssayDocument5 pagesPhilippine Fake News EssayZyrrich RobertNo ratings yet

- 5ta Tarea de Ingles Avanzado IIDocument30 pages5ta Tarea de Ingles Avanzado IIabiel jimenezNo ratings yet

- Model Draft For Written Statement in The Court - of Civil Judge (DISTRICT - ), - SUIT NO. - OF 20XXDocument3 pagesModel Draft For Written Statement in The Court - of Civil Judge (DISTRICT - ), - SUIT NO. - OF 20XXSwaJeet KaDamNo ratings yet

- Omnibus Motion (Motion To Re-Open, Admit Answer and Delist: Republic of The PhilippinesDocument6 pagesOmnibus Motion (Motion To Re-Open, Admit Answer and Delist: Republic of The PhilippinesHIBA INTL. INC.No ratings yet

- Learning Exercise 2.6: THE BASIC VALUES OF THE FILIPINOS (Good Citizenship Clusters)Document7 pagesLearning Exercise 2.6: THE BASIC VALUES OF THE FILIPINOS (Good Citizenship Clusters)AngelaOrosiaDenilaNo ratings yet

- 2004 - Koh - Organisational Ethics and Employee Satisfaction and CommitmentDocument20 pages2004 - Koh - Organisational Ethics and Employee Satisfaction and CommitmentGeorgianaDîdălNo ratings yet

- Business Ethics in Action Lecture & Seminar 2Document29 pagesBusiness Ethics in Action Lecture & Seminar 2Shanuka SapugodaNo ratings yet

- Silibus - Law507 - Admin Law For AuthoritiesDocument3 pagesSilibus - Law507 - Admin Law For AuthoritiesiraNo ratings yet

- Sample DissertationDocument52 pagesSample DissertationBelfacinoNo ratings yet

- The Story of The Seagull and The Cat Who Taught Her To FlightDocument2 pagesThe Story of The Seagull and The Cat Who Taught Her To FlightHiếu Lê ĐắcNo ratings yet

- Confidentiality and Privacy: This Is Page 1 of 7Document7 pagesConfidentiality and Privacy: This Is Page 1 of 7api-534908963No ratings yet

- Englis L ExerciseDocument42 pagesEnglis L ExerciseSneha SharmaNo ratings yet

- In The Hon'Ble District Consumer Disputes Redressal Commission, Mumbai at MumbaiDocument7 pagesIn The Hon'Ble District Consumer Disputes Redressal Commission, Mumbai at MumbaiYaashik HenrageNo ratings yet

- Quiz 4 - Morgia - March 9, 2022Document2 pagesQuiz 4 - Morgia - March 9, 2022Cristina Crong MorgiaNo ratings yet

- Near Miss ReportDocument5 pagesNear Miss ReportAakash GuptaNo ratings yet

- Unit 3 Tender and ContractDocument4 pagesUnit 3 Tender and ContractswathikaNo ratings yet

- School of Law and GovernanceDocument3 pagesSchool of Law and GovernanceMelody EngNo ratings yet