Download as pdf or txt

You might also like

- Sample Motion To Reopen Discovery in CaliforniaDocument3 pagesSample Motion To Reopen Discovery in CaliforniaStan Burman60% (5)

- BFF Response To Release of State Audit - FINALDocument1 pageBFF Response To Release of State Audit - FINALSteve HawkinsNo ratings yet

- 4012 For 2017 ReturnsDocument349 pages4012 For 2017 ReturnsSarah EunJu LeeNo ratings yet

- Elizabeth Nungaray Complaint 6-22-21Document6 pagesElizabeth Nungaray Complaint 6-22-21Steve HawkinsNo ratings yet

- Return of Search WarrantDocument2 pagesReturn of Search WarrantDerek J McKnight0% (1)

- 2020 Disaster Loss How To Claim A State Tax Deduction: FTB PublicationDocument9 pages2020 Disaster Loss How To Claim A State Tax Deduction: FTB PublicationAdi PutraNo ratings yet

- US Internal Revenue Service: p514 - 1995Document31 pagesUS Internal Revenue Service: p514 - 1995IRSNo ratings yet

- 2008 Publication 553 Highlights of 2008 Tax ChangesDocument38 pages2008 Publication 553 Highlights of 2008 Tax ChangesgrosofNo ratings yet

- (And 1040-SR) : InstructionsDocument113 pages(And 1040-SR) : InstructionsRigid Tail 77No ratings yet

- 1060Document8 pages1060jbkmailNo ratings yet

- Instructions For 1120Document29 pagesInstructions For 1120Satish KumarNo ratings yet

- Canceled Debts, Foreclosures, Repossessions, and AbandonmentsDocument24 pagesCanceled Debts, Foreclosures, Repossessions, and AbandonmentsSalvador DavilaNo ratings yet

- US Internal Revenue Service: p929 - 1995Document24 pagesUS Internal Revenue Service: p929 - 1995IRSNo ratings yet

- Publication 54 - IRSDocument44 pagesPublication 54 - IRSabraham.caaNo ratings yet

- Tax Guide For U.S. Citizens and Resident Aliens Abroad: Publication 54Document38 pagesTax Guide For U.S. Citizens and Resident Aliens Abroad: Publication 54hey_hopNo ratings yet

- 2024 Texas Franchise Tax Report Information and InstructionsDocument32 pages2024 Texas Franchise Tax Report Information and Instructionsmohamedkadry abdelhmeedNo ratings yet

- IRS Pub 2194 - Disaster Relief Tax AddendumDocument136 pagesIRS Pub 2194 - Disaster Relief Tax AddendumdonlucekNo ratings yet

- Maverick Tax Express 941 W Pioneer Pkwy ARLINGTON, TX 76013-6369 817-261-6287Document19 pagesMaverick Tax Express 941 W Pioneer Pkwy ARLINGTON, TX 76013-6369 817-261-6287Vignesh EswaranNo ratings yet

- Tax Guide For U.S. Citizens and Resident Aliens Abroad: Publication 54Document38 pagesTax Guide For U.S. Citizens and Resident Aliens Abroad: Publication 54Muzammil HanifNo ratings yet

- Pub. 54. Tax Guide For U.S. Citizens and Resident Aliens AbroadDocument44 pagesPub. 54. Tax Guide For U.S. Citizens and Resident Aliens Abroadjoputa15No ratings yet

- 2011 Form 1041 K 1 InstructionsDocument37 pages2011 Form 1041 K 1 InstructionsEltech911100% (1)

- 2011 Pa-40 Fastfile BookDocument20 pages2011 Pa-40 Fastfile BookGaurav ShuklaNo ratings yet

- LCGS 2011 941Document2 pagesLCGS 2011 941Timothy Rampage RushNo ratings yet

- Casualties, Disasters, Thefts (p547)Document24 pagesCasualties, Disasters, Thefts (p547)Dann KopkoNo ratings yet

- US Internal Revenue Service: p523 - 1995Document24 pagesUS Internal Revenue Service: p523 - 1995IRSNo ratings yet

- 2022 Instructions For Form 1041 and Schedules A, B, G, J, and K-1 - I1041Document52 pages2022 Instructions For Form 1041 and Schedules A, B, G, J, and K-1 - I1041Mr CutsforthNo ratings yet

- Returns: in This Chapter..Document12 pagesReturns: in This Chapter..aNo ratings yet

- Publication 721, Tax Guide To U.S. Civil Service Retirement Benefits (2021)Document33 pagesPublication 721, Tax Guide To U.S. Civil Service Retirement Benefits (2021)Dianna VenezianoNo ratings yet

- Woyming Investment IncentivesDocument31 pagesWoyming Investment IncentivesPaki12345No ratings yet

- 17 5402ezbkDocument64 pages17 5402ezbkPhylicia MorrisNo ratings yet

- US Internal Revenue Service: p3 - 1999Document25 pagesUS Internal Revenue Service: p3 - 1999IRSNo ratings yet

- Part I - Interim County RecommendationsDocument10 pagesPart I - Interim County RecommendationsNick ReismanNo ratings yet

- US Internal Revenue Service: p575 - 1996Document39 pagesUS Internal Revenue Service: p575 - 1996IRSNo ratings yet

- Irs New Form 1040Document2 pagesIrs New Form 1040ForkLogNo ratings yet

- Resident BookletDocument32 pagesResident BookletGopal GopinathNo ratings yet

- A Guide To Federal Tax Incentives For Brownfields RedevelopmentDocument28 pagesA Guide To Federal Tax Incentives For Brownfields RedevelopmentMark FowlerNo ratings yet

- Newcomers To Canada: Is This Pamphlet For You?Document16 pagesNewcomers To Canada: Is This Pamphlet For You?Toofan KhanNo ratings yet

- p4491 PDFDocument384 pagesp4491 PDFcatalin cretuNo ratings yet

- Instructions For Form 1040NR: What's NewDocument81 pagesInstructions For Form 1040NR: What's NewJohnNo ratings yet

- Instructions For Form 1120: Future DevelopmentsDocument32 pagesInstructions For Form 1120: Future DevelopmentsfatimazehranaqviNo ratings yet

- Guide For Corporations Starting Business in California: FTB Publication 1060Document6 pagesGuide For Corporations Starting Business in California: FTB Publication 1060jackyNo ratings yet

- Voluntary Disclosure User Guide Vat & Excise TaxDocument21 pagesVoluntary Disclosure User Guide Vat & Excise TaxHaider MalikNo ratings yet

- IRS Community PropertyDocument16 pagesIRS Community PropertygxperryNo ratings yet

- Instructions For Form 1041 and Schedules A, B, G, J, and K-1Document53 pagesInstructions For Form 1041 and Schedules A, B, G, J, and K-1Vincent BerryNo ratings yet

- US Internal Revenue Service: p523 - 1996Document27 pagesUS Internal Revenue Service: p523 - 1996IRSNo ratings yet

- Principles of Taxation Law Project 312Document16 pagesPrinciples of Taxation Law Project 312Gunjan GargNo ratings yet

- Maryland Mortgage Program - Recapture TaxDocument12 pagesMaryland Mortgage Program - Recapture TaxNishika JGNo ratings yet

- p4012 (2018)Document349 pagesp4012 (2018)Center for Economic Progress100% (1)

- Selling Your Home: Key PointsDocument23 pagesSelling Your Home: Key PointstechNo ratings yet

- 2023 Omnibus Notes - Part 2 - Taxation Law LawDocument18 pages2023 Omnibus Notes - Part 2 - Taxation Law LawAPRIL BETONIONo ratings yet

- A Guide To Federal Government ACH Payments and Collections: WWW - Fms.treas - Gov/greenbookDocument153 pagesA Guide To Federal Government ACH Payments and Collections: WWW - Fms.treas - Gov/greenbookGeeTheWhizzNo ratings yet

- A Guide To Federal Government ACH Payments and Collections: WWW - Fms.treas - Gov/greenbookDocument155 pagesA Guide To Federal Government ACH Payments and Collections: WWW - Fms.treas - Gov/greenbookncwazzyNo ratings yet

- Agriculture Law: RL31734Document16 pagesAgriculture Law: RL31734AgricultureCaseLawNo ratings yet

- Rental Property Tax LawsDocument31 pagesRental Property Tax LawsArnold GalvanNo ratings yet

- Instructions For Form IT-201: Full-Year Resident Income Tax ReturnDocument72 pagesInstructions For Form IT-201: Full-Year Resident Income Tax ReturntinpenaNo ratings yet

- t4037 Capital Gains Guide 2016Document48 pagest4037 Capital Gains Guide 2016sarb007No ratings yet

- Instructions For Form 1120Document31 pagesInstructions For Form 1120A.F. GRANADANo ratings yet

- FORM MO-1040A: Missouri Individual Income Tax Return Single/Married (Income From One Spouse) - Short FormDocument2 pagesFORM MO-1040A: Missouri Individual Income Tax Return Single/Married (Income From One Spouse) - Short Formpixel986No ratings yet

- US Internal Revenue Service: I1040c - 1996Document6 pagesUS Internal Revenue Service: I1040c - 1996IRSNo ratings yet

- Doing Business in The United States: A Guide To The Key Tax Issues 2020Document141 pagesDoing Business in The United States: A Guide To The Key Tax Issues 2020Jacques DelaigueNo ratings yet

- General Info Booklet-Rc4022-17eDocument89 pagesGeneral Info Booklet-Rc4022-17eZhen WeiNo ratings yet

- Agriculture Law: RL30600Document33 pagesAgriculture Law: RL30600AgricultureCaseLawNo ratings yet

- USDA ERS Err-252Document45 pagesUSDA ERS Err-252wsw31No ratings yet

- Fresno Police ComplaintDocument1 pageFresno Police ComplaintSteve HawkinsNo ratings yet

- Legal Services AgreementDocument20 pagesLegal Services AgreementSteve HawkinsNo ratings yet

- Hoover ReportDocument43 pagesHoover ReportSteve HawkinsNo ratings yet

- Charging Document - Formal Complaint FiledDocument2 pagesCharging Document - Formal Complaint FiledSteve HawkinsNo ratings yet

- Big Sur Coast Map SouthDocument1 pageBig Sur Coast Map SouthSteve HawkinsNo ratings yet

- Faisal Mohammad Part 2Document203 pagesFaisal Mohammad Part 2Steve HawkinsNo ratings yet

- Esparza ComplaintDocument8 pagesEsparza ComplaintSteve HawkinsNo ratings yet

- Cox IndictmentDocument25 pagesCox IndictmentSteve HawkinsNo ratings yet

- ACLU LawsuitDocument39 pagesACLU LawsuitSteve Hawkins100% (1)

- Ford PPE Poster NorCalDocument1 pageFord PPE Poster NorCalSteve HawkinsNo ratings yet

- America's Most Endangered Rivers®Document23 pagesAmerica's Most Endangered Rivers®Steve Hawkins0% (1)

- Governor Newsom Letter To President TrumpDocument17 pagesGovernor Newsom Letter To President TrumpSteve HawkinsNo ratings yet

- CO Appeal - RedactedDocument7 pagesCO Appeal - RedactedSteve HawkinsNo ratings yet

- Dr. Castro Settlement AgreementDocument7 pagesDr. Castro Settlement AgreementSteve HawkinsNo ratings yet

- Blueprint For A Safer EconomyDocument7 pagesBlueprint For A Safer EconomySteve HawkinsNo ratings yet

- Faisal Mohammad Part 1Document322 pagesFaisal Mohammad Part 1Steve HawkinsNo ratings yet

- Guidance Outdoor Hair Salons enDocument12 pagesGuidance Outdoor Hair Salons enSteve HawkinsNo ratings yet

- Fresno Unified School DistrictDocument1 pageFresno Unified School DistrictSteve HawkinsNo ratings yet

- Fresno County Health OrderDocument10 pagesFresno County Health OrderSteve HawkinsNo ratings yet

- CS SportCalendarDocument1 pageCS SportCalendarSteve HawkinsNo ratings yet

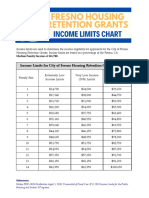

- Fresno Housing Retention Grants Income Limits ChartDocument1 pageFresno Housing Retention Grants Income Limits ChartSteve HawkinsNo ratings yet

- COVID-19 Industry Guidance:: Schools and School-Based ProgramsDocument19 pagesCOVID-19 Industry Guidance:: Schools and School-Based ProgramsSteve Hawkins100% (1)

- Emergency Rule 4 - EXCEPTIONS - 061920Document5 pagesEmergency Rule 4 - EXCEPTIONS - 061920Steve HawkinsNo ratings yet

- Guidance Hair SalonsDocument10 pagesGuidance Hair SalonsSteve HawkinsNo ratings yet

- Thaddeus SranDocument2 pagesThaddeus SranSteve HawkinsNo ratings yet

- A Doctor A Day Letter - SignedDocument10 pagesA Doctor A Day Letter - SignedFox News86% (95)

- Guidance Places of WorshipDocument13 pagesGuidance Places of WorshipBakersfieldNowNo ratings yet

- Tulare CountyDocument3 pagesTulare CountySteve HawkinsNo ratings yet

- Donald Ray Bass v. David Graham, Assistant Warden H.H. Hardy, Laundry Supervisor J. Lafoon, R.N. Doctor Thompson, 14 F.3d 593, 4th Cir. (1994)Document2 pagesDonald Ray Bass v. David Graham, Assistant Warden H.H. Hardy, Laundry Supervisor J. Lafoon, R.N. Doctor Thompson, 14 F.3d 593, 4th Cir. (1994)Scribd Government DocsNo ratings yet

- 1 Daez v. Ca DigestDocument2 pages1 Daez v. Ca DigestSJ Normando Catubay67% (3)

- Form 941X-745287Document7 pagesForm 941X-745287Catori-Dakoda Eil100% (1)

- United States v. O'Dell, 4th Cir. (2006)Document4 pagesUnited States v. O'Dell, 4th Cir. (2006)Scribd Government DocsNo ratings yet

- United States v. Darius Brooks, 4th Cir. (2011)Document3 pagesUnited States v. Darius Brooks, 4th Cir. (2011)Scribd Government DocsNo ratings yet

- S & A Capital Partners V American Bank 2017-018899-CA-01, 11th Cir FL Miami-Dade County FinalDocument4 pagesS & A Capital Partners V American Bank 2017-018899-CA-01, 11th Cir FL Miami-Dade County Finallarry-612445No ratings yet

- United States v. Monte Moore, 4th Cir. (2014)Document6 pagesUnited States v. Monte Moore, 4th Cir. (2014)Scribd Government DocsNo ratings yet

- Riches v. Bridges Et Al - Document No. 3Document2 pagesRiches v. Bridges Et Al - Document No. 3Justia.comNo ratings yet

- Texas Attorney General Ruling On Pentkowski AutopsyDocument2 pagesTexas Attorney General Ruling On Pentkowski AutopsyIsabelle PasciollaNo ratings yet

- Ehinger v. United States of America Et Al - Document No. 17Document3 pagesEhinger v. United States of America Et Al - Document No. 17Justia.comNo ratings yet

- Filed: Patrick FisherDocument3 pagesFiled: Patrick FisherScribd Government DocsNo ratings yet

- Tinker v. DMICSDDocument3 pagesTinker v. DMICSDSamantha VaccaNo ratings yet

- Torres vs. DalanginDocument2 pagesTorres vs. DalanginNypho PareñoNo ratings yet

- Torbov v. Murphy ReportDocument4 pagesTorbov v. Murphy ReportNorthern District of California BlogNo ratings yet

- United States Ex Rel. Joseph Randazzo v. Hon. Harold W. Follette, Warden, Green Haven Prison, Stormville, New York, 444 F.2d 625, 2d Cir. (1971)Document6 pagesUnited States Ex Rel. Joseph Randazzo v. Hon. Harold W. Follette, Warden, Green Haven Prison, Stormville, New York, 444 F.2d 625, 2d Cir. (1971)Scribd Government DocsNo ratings yet

- In Re Arc Energy Corporation, Debtor. Colstar Petroleum Corporation Charlese. Colburn, III v. Arc Energy Corporation, 30 F.3d 128, 4th Cir. (1994)Document2 pagesIn Re Arc Energy Corporation, Debtor. Colstar Petroleum Corporation Charlese. Colburn, III v. Arc Energy Corporation, 30 F.3d 128, 4th Cir. (1994)Scribd Government DocsNo ratings yet

- Not PrecedentialDocument4 pagesNot PrecedentialScribd Government DocsNo ratings yet

- Barbyq Dire IrsDocument2 pagesBarbyq Dire IrsrolfNo ratings yet

- Shapiro, Bernstein & Co., Inc. v. Jerry Vogel Music Co., Inc., 223 F.2d 252, 2d Cir. (1955)Document3 pagesShapiro, Bernstein & Co., Inc. v. Jerry Vogel Music Co., Inc., 223 F.2d 252, 2d Cir. (1955)Scribd Government DocsNo ratings yet

- Coleman v. Thompson, 501 U.S. 722 (1991)Document42 pagesColeman v. Thompson, 501 U.S. 722 (1991)Scribd Government DocsNo ratings yet

- Summary of The Bakke CaseDocument2 pagesSummary of The Bakke CaseJan Aldrin AfosNo ratings yet

- United States v. Heywood Monroe Bell, 4th Cir. (2000)Document3 pagesUnited States v. Heywood Monroe Bell, 4th Cir. (2000)Scribd Government DocsNo ratings yet

- Get Kaisered V AKT Franchisel 120-Cv-01037-CFC-JLH - Doc 218 - Finalized SettlementDocument1 pageGet Kaisered V AKT Franchisel 120-Cv-01037-CFC-JLH - Doc 218 - Finalized SettlementFuzzy PandaNo ratings yet

- United States Court of Appeals, Fourth CircuitDocument2 pagesUnited States Court of Appeals, Fourth CircuitScribd Government DocsNo ratings yet

- Florente vs. FlorenteDocument2 pagesFlorente vs. FlorentetrishaNo ratings yet

- Juan Martinez-Alvarez, A200 759 323 (BIA May 29, 2014)Document5 pagesJuan Martinez-Alvarez, A200 759 323 (BIA May 29, 2014)Immigrant & Refugee Appellate Center, LLCNo ratings yet

- Thomas Ostrowski v. Con-Way Freight Inc, 3rd Cir. (2013)Document7 pagesThomas Ostrowski v. Con-Way Freight Inc, 3rd Cir. (2013)Scribd Government DocsNo ratings yet

- In Re Freeman Dale Crabtree, Linda A. Crabtree, Catherine Dianne Crabtree Trust, David Lynn Crabtree Trust, the Orchard Company, Debtors. Freeman Dale Crabtree, Linda A. Crabtree, Catherine Dianne Crabtree Trust, David Lynn Crabtree Trust, the Orchard Company v. Bobbie G. Bayless, Trustee, Myers D. Campbell, Patricia M. Campbell, Jerry Tubb, Theta Juan Bernhardt, 930 F.2d 32, 10th Cir. (1991)Document2 pagesIn Re Freeman Dale Crabtree, Linda A. Crabtree, Catherine Dianne Crabtree Trust, David Lynn Crabtree Trust, the Orchard Company, Debtors. Freeman Dale Crabtree, Linda A. Crabtree, Catherine Dianne Crabtree Trust, David Lynn Crabtree Trust, the Orchard Company v. Bobbie G. Bayless, Trustee, Myers D. Campbell, Patricia M. Campbell, Jerry Tubb, Theta Juan Bernhardt, 930 F.2d 32, 10th Cir. (1991)Scribd Government DocsNo ratings yet