Download as docx, pdf, or txt

You might also like

- Nation Wide BankDocument1 pageNation Wide BankShaggy ShagNo ratings yet

- Assignment - Chapter 4 - SolutionDocument9 pagesAssignment - Chapter 4 - SolutionQuỳnh Nguyễn0% (1)

- Accounting Test Bank - Bank ReconciliationDocument2 pagesAccounting Test Bank - Bank ReconciliationAyesha RGNo ratings yet

- Quiz Chapter+3 Bonds+PayableDocument3 pagesQuiz Chapter+3 Bonds+PayableRena Jocelle NalzaroNo ratings yet

- Problem: Sorsogon State UniversityDocument3 pagesProblem: Sorsogon State UniversityHector OcampoNo ratings yet

- Inacct3 Module 3 QuizDocument7 pagesInacct3 Module 3 QuizGemNo ratings yet

- Cost Concept, Terminologies and BehaviorDocument8 pagesCost Concept, Terminologies and BehaviorANDREA NICOLE DE LEONNo ratings yet

- Quiz LeasesDocument2 pagesQuiz LeasesCyra de LemosNo ratings yet

- Business Law Atty. Macmod, CPA 2018 Edition Obligations - 01 I. Identification (Basic Concept/Principles)Document9 pagesBusiness Law Atty. Macmod, CPA 2018 Edition Obligations - 01 I. Identification (Basic Concept/Principles)bobo kaNo ratings yet

- III. Law On Pledge Mortgage Recto Law Maceda Law PD 957 and Assignment of Credit PDFDocument17 pagesIII. Law On Pledge Mortgage Recto Law Maceda Law PD 957 and Assignment of Credit PDFseya dummyNo ratings yet

- Quiz Chapter+2 Notes+payable+-+Document2 pagesQuiz Chapter+2 Notes+payable+-+Rena Jocelle NalzaroNo ratings yet

- Nfjpia Frontliners RFBT 2019Document19 pagesNfjpia Frontliners RFBT 2019Risalyn BiongNo ratings yet

- Practice Quiz NonFinlLiabDocument15 pagesPractice Quiz NonFinlLiabIsabelle GuillenaNo ratings yet

- C. Update Valid Vendor File: Multiple-Choice Questions 1Document8 pagesC. Update Valid Vendor File: Multiple-Choice Questions 1DymeNo ratings yet

- Break-Even Analysis: Cost-Volume-Profit AnalysisDocument64 pagesBreak-Even Analysis: Cost-Volume-Profit AnalysisKelvin LeongNo ratings yet

- Accounting Information System: Midterm ExaminationDocument9 pagesAccounting Information System: Midterm ExaminationLaezelie SorianoNo ratings yet

- Review 105 - Day 4 Theory of AccountsDocument13 pagesReview 105 - Day 4 Theory of Accountschristine anglaNo ratings yet

- Job CostingDocument19 pagesJob CostingSteven HouNo ratings yet

- Chapter-3-6 Testbank AisDocument33 pagesChapter-3-6 Testbank AisAngela Erish CastroNo ratings yet

- Finals Financial ManagementDocument22 pagesFinals Financial Managementsammie helsonNo ratings yet

- Current LiabDocument24 pagesCurrent LiabSamantha Marie ArevaloNo ratings yet

- Qualifying - Exam Business LawDocument12 pagesQualifying - Exam Business LawGodwin De GuzmanNo ratings yet

- University of San Carlos School of Business and Economics Department of Accountancy AC 1103 3rd Long Exam Name: - Schedule: - CourseDocument7 pagesUniversity of San Carlos School of Business and Economics Department of Accountancy AC 1103 3rd Long Exam Name: - Schedule: - CourseChristine NionesNo ratings yet

- Quiz Chapter 7 Leases Part 1 2021Document2 pagesQuiz Chapter 7 Leases Part 1 2021Jennifer Reloso100% (1)

- Seatwork 02 InvestmentsDocument2 pagesSeatwork 02 InvestmentsJella Mae YcalinaNo ratings yet

- Questionnaire: Act112 - Intermediate Accounting IDocument20 pagesQuestionnaire: Act112 - Intermediate Accounting IMichaelNo ratings yet

- Long Quiz 2 Lease Answer KeyDocument3 pagesLong Quiz 2 Lease Answer KeyMia FayeNo ratings yet

- PAS 36 Impairment of AssetsDocument8 pagesPAS 36 Impairment of AssetswalsondevNo ratings yet

- Bl2: The Law On Private Corporation Final Examination General InstructionsDocument4 pagesBl2: The Law On Private Corporation Final Examination General InstructionsShaika HaceenaNo ratings yet

- Partnership Diagnostic ExercisesDocument24 pagesPartnership Diagnostic ExercisesBrithney TurlaNo ratings yet

- Quiz Finma 0920Document5 pagesQuiz Finma 0920Danica RamosNo ratings yet

- Toaz - Info Quiz 3 PRDocument25 pagesToaz - Info Quiz 3 PRAprille Xay TupasNo ratings yet

- Govt Acctg - Semi FinalsDocument5 pagesGovt Acctg - Semi Finalsrustylopez1112No ratings yet

- Exercise 1 For Time Value of MoneyDocument8 pagesExercise 1 For Time Value of MoneyChris tine Mae MendozaNo ratings yet

- PFRS 14 15 16Document3 pagesPFRS 14 15 16kara mNo ratings yet

- Cpa Review School of The Philippines ManilaDocument5 pagesCpa Review School of The Philippines ManilaAljur SalamedaNo ratings yet

- Qualifying Exam Reviewer - ObliconDocument10 pagesQualifying Exam Reviewer - ObliconFee100% (1)

- Acrev 422 AfarDocument19 pagesAcrev 422 AfarAira Mugal OwarNo ratings yet

- 1ST Grading ExamDocument12 pages1ST Grading ExamJEFFERSON CUTENo ratings yet

- Seeds of The Nations Review-MidtermsDocument9 pagesSeeds of The Nations Review-MidtermsMikaela JeanNo ratings yet

- ACTG 431 QUIZ Week 2 Theory of Accounts Part 2 - FINANCIAL ASSET AT AMORTIZED COST QUIZDocument4 pagesACTG 431 QUIZ Week 2 Theory of Accounts Part 2 - FINANCIAL ASSET AT AMORTIZED COST QUIZMarilou Arcillas PanisalesNo ratings yet

- FAR REVIEWER Part 1Document7 pagesFAR REVIEWER Part 1jessamae gundanNo ratings yet

- ToaDocument18 pagesToaMJ YaconNo ratings yet

- Microsoft Word - FAR02 - Accounting For Debt InvestmentsDocument4 pagesMicrosoft Word - FAR02 - Accounting For Debt InvestmentsDisguised owl0% (1)

- Theories LeasesDocument11 pagesTheories LeasesMinie KimNo ratings yet

- Assignment 01 Bonds PayableDocument6 pagesAssignment 01 Bonds PayableMinie KimNo ratings yet

- CVP MC 1920 W KeyDocument6 pagesCVP MC 1920 W KeyGale RasNo ratings yet

- Department of Accountancy: Prepared By: Mohammad Muariff S. Balang, CPA, Second Semester, AY 2012-2013Document8 pagesDepartment of Accountancy: Prepared By: Mohammad Muariff S. Balang, CPA, Second Semester, AY 2012-2013Jaliyah IslaNo ratings yet

- Employee Benefits Questions 2Document1 pageEmployee Benefits Questions 2Ronnah Mae FloresNo ratings yet

- Midterms Conceptual Framework and Accounting StandardsDocument9 pagesMidterms Conceptual Framework and Accounting StandardsMay Anne MenesesNo ratings yet

- Studet Practical Accounting Ch17 PPE AcquisitionDocument16 pagesStudet Practical Accounting Ch17 PPE Acquisitionsabina del monteNo ratings yet

- Answer Key For Week 1 To 3 ULO 8 To 10Document7 pagesAnswer Key For Week 1 To 3 ULO 8 To 10Margaux Phoenix KimilatNo ratings yet

- Three Methods of Estimating Doubtful AccountsDocument8 pagesThree Methods of Estimating Doubtful AccountsJay Lou PayotNo ratings yet

- MODULE 5-Part 1Document5 pagesMODULE 5-Part 1Mary Joy CabilNo ratings yet

- Midterm Examination BSAISDocument11 pagesMidterm Examination BSAISAlexis Kaye DayagNo ratings yet

- COST EXAM2 (Compiled by Gail)Document17 pagesCOST EXAM2 (Compiled by Gail)Mildred Angela DingalNo ratings yet

- Activity Chapter 4: Ans. 2,320 SolutionDocument2 pagesActivity Chapter 4: Ans. 2,320 SolutionRandelle James FiestaNo ratings yet

- RFBTDocument5 pagesRFBTTakuriNo ratings yet

- Job Order CostingDocument20 pagesJob Order CostingIrish Te-odNo ratings yet

- HBL MID Partnership and CorporationDocument2 pagesHBL MID Partnership and CorporationginalynNo ratings yet

- Chapter 3 Problems - Ia Part 2Document16 pagesChapter 3 Problems - Ia Part 2KathleenCusipagNo ratings yet

- ch3 Not EditedDocument14 pagesch3 Not EditedDM MontefalcoNo ratings yet

- Group 1 BLK 2 Questions On Types of Valuation MultiplesDocument5 pagesGroup 1 BLK 2 Questions On Types of Valuation MultiplesMicah ErguizaNo ratings yet

- FS Analysis - Answer KeyDocument1 pageFS Analysis - Answer KeyMicah ErguizaNo ratings yet

- Erguiza, Micah - World LiteratureDocument2 pagesErguiza, Micah - World LiteratureMicah ErguizaNo ratings yet

- Finman Q1Document5 pagesFinman Q1Micah ErguizaNo ratings yet

- DocumentDocument2 pagesDocumentMicah ErguizaNo ratings yet

- FS Analysis Activity #1Document2 pagesFS Analysis Activity #1Micah ErguizaNo ratings yet

- Types of Conflicts (Activity)Document2 pagesTypes of Conflicts (Activity)Micah ErguizaNo ratings yet

- Caec 16Document5 pagesCaec 16Micah ErguizaNo ratings yet

- CrashingDocument1 pageCrashingMicah ErguizaNo ratings yet

- SBA - Semis ERGUIZA, MICAHDocument3 pagesSBA - Semis ERGUIZA, MICAHMicah ErguizaNo ratings yet

- Udd - Pre01 - Auditing and Assurance Principle - Midterm ExaminationDocument9 pagesUdd - Pre01 - Auditing and Assurance Principle - Midterm ExaminationMicah ErguizaNo ratings yet

- FM - Quiz #1Document7 pagesFM - Quiz #1Micah ErguizaNo ratings yet

- Law On Sale My LectureDocument35 pagesLaw On Sale My LectureMicah ErguizaNo ratings yet

- KA SET A Cost Accounting and ControlDocument11 pagesKA SET A Cost Accounting and ControlMicah ErguizaNo ratings yet

- Finals PerformanceDocument1 pageFinals PerformanceMicah ErguizaNo ratings yet

- Financial Management by AdorDocument6 pagesFinancial Management by AdorMicah ErguizaNo ratings yet

- Rizal Midterm HandoutDocument13 pagesRizal Midterm HandoutMicah ErguizaNo ratings yet

- Semi-Final - Movie Review - Erguiza, Micah (31-Bsa-01)Document5 pagesSemi-Final - Movie Review - Erguiza, Micah (31-Bsa-01)Micah ErguizaNo ratings yet

- Hbo Midterms ExamDocument10 pagesHbo Midterms ExamMark AdrianNo ratings yet

- Contemporary Dance ResearchDocument3 pagesContemporary Dance ResearchMicah ErguizaNo ratings yet

- Chapter 8 - Reviewing Internal Control Over Financial ReportingDocument9 pagesChapter 8 - Reviewing Internal Control Over Financial ReportingMicah ErguizaNo ratings yet

- DocumentDocument3 pagesDocumentMicah ErguizaNo ratings yet

- Chapter - 8 Banker and Customer RelationshipDocument26 pagesChapter - 8 Banker and Customer RelationshipMd Mohsin AliNo ratings yet

- MBR517 Lect 01Document30 pagesMBR517 Lect 01Updyfitah TahlilNo ratings yet

- ReferencesDocument9 pagesReferencesBông GấuNo ratings yet

- Jun 22Document3 pagesJun 22honey moneyNo ratings yet

- STD 8 TH Maths Bridge CourseDocument65 pagesSTD 8 TH Maths Bridge CourseDeepak TerseNo ratings yet

- INTERMEDIATE ACCOUNTING Vol. 1 (2021 Edition) - Valix, Peralta & Valix - XLSX Chapter 3Document4 pagesINTERMEDIATE ACCOUNTING Vol. 1 (2021 Edition) - Valix, Peralta & Valix - XLSX Chapter 3Rodolfo ManalacNo ratings yet

- Ms8-Set A Midterm - With AnswersDocument5 pagesMs8-Set A Midterm - With AnswersOscar Bocayes Jr.No ratings yet

- Statement of Axis Account No:914010049504553 For The Period (From: 23-01-2019 To: 02-09-2020)Document4 pagesStatement of Axis Account No:914010049504553 For The Period (From: 23-01-2019 To: 02-09-2020)Chandrani ChatterjeeNo ratings yet

- International TradingDocument13 pagesInternational TradingchikaNo ratings yet

- Alliance Bank Malaysia Berhad: MaintainDocument5 pagesAlliance Bank Malaysia Berhad: MaintainZhi_Ming_Cheah_8136No ratings yet

- Invoice - Billing - Billing Monthly Group 60 - For Period 2024.02.01 To 2024.02.29 - ZH22-WEST BENGAL - C004286996 - 1.2.2024 - 29.2.2024Document38 pagesInvoice - Billing - Billing Monthly Group 60 - For Period 2024.02.01 To 2024.02.29 - ZH22-WEST BENGAL - C004286996 - 1.2.2024 - 29.2.2024Bidyut ManaNo ratings yet

- Keko - Final ThesisDocument82 pagesKeko - Final Thesisberhanu seyoumNo ratings yet

- Resolution: Republic of The Philippines Department of Justice Office of The City Prosecutor Baguio CityDocument5 pagesResolution: Republic of The Philippines Department of Justice Office of The City Prosecutor Baguio CitySui JurisNo ratings yet

- Recording TransactionsDocument45 pagesRecording TransactionsKei TamundongNo ratings yet

- Full FSA ST - Vol IIIDocument421 pagesFull FSA ST - Vol IIIVîkter VîshváNo ratings yet

- Chap 1 - Islamic BankingDocument7 pagesChap 1 - Islamic BankinghanimudaNo ratings yet

- Description From Currency To Currency Recipient Receive Exchange Rate Amount DueDocument1 pageDescription From Currency To Currency Recipient Receive Exchange Rate Amount DueJOMBANG TIMOERNo ratings yet

- CDO and Synthetic CDODocument3 pagesCDO and Synthetic CDOJIGYASA KUMARINo ratings yet

- General Accounting TutorialDocument3 pagesGeneral Accounting TutorialMiocnou Didier chautyNo ratings yet

- TIẾNG ANH CHUYÊN NGÀNH TÀI CHÍNH-NGÂN HÀNGDocument6 pagesTIẾNG ANH CHUYÊN NGÀNH TÀI CHÍNH-NGÂN HÀNG35. Lê Thị Việt NgânNo ratings yet

- Final Submission Project Work 2020Document104 pagesFinal Submission Project Work 2020Nana Yaw MarfoNo ratings yet

- Half Year Report 2023 1Document92 pagesHalf Year Report 2023 1Neha NadeemNo ratings yet

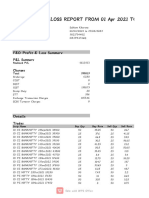

- Fno Profit & Loss Report From 01 Apr 2021 ToDocument8 pagesFno Profit & Loss Report From 01 Apr 2021 ToSourabh AhujaNo ratings yet

- Visa Credit Card BillDocument2 pagesVisa Credit Card BillLodjuaNo ratings yet

- SahooCommittee Ecbreport 20150225Document109 pagesSahooCommittee Ecbreport 20150225advpreetipundirNo ratings yet

- Term Paper of FM&INSDocument13 pagesTerm Paper of FM&INSKetema AsfawNo ratings yet

- Indian Financial SystemDocument38 pagesIndian Financial SystemNikita DakiNo ratings yet

- Vision January 2023 - EnglishDocument8 pagesVision January 2023 - EnglishRajat KushwahNo ratings yet