Download as pdf or txt

You might also like

- Adjusting Entries Problems 2022 DahonogDocument2 pagesAdjusting Entries Problems 2022 DahonogBaltazar JustinianoNo ratings yet

- STUDENT Copy Chapter 1 Review of The Accounting CycleDocument28 pagesSTUDENT Copy Chapter 1 Review of The Accounting CycleKurt Latrell AlcantaraNo ratings yet

- 3 7BDocument3 pages3 7BFaraz FaisalNo ratings yet

- Anastasya Apriliani 008201705017 - POA CH5&6Document8 pagesAnastasya Apriliani 008201705017 - POA CH5&6Anas TasyaNo ratings yet

- Learning Journal Unit 2 Basic AccountingDocument7 pagesLearning Journal Unit 2 Basic Accountingjayward turpiasNo ratings yet

- Accounting NavjotDocument1 pageAccounting Navjotyour0samNo ratings yet

- ConsolidationDocument25 pagesConsolidationAEDRIAN LEE DERECHONo ratings yet

- 회계학원론 과제 P2.1Document1 page회계학원론 과제 P2.1yeopseo05No ratings yet

- 5532 $FDocument1 page5532 $FSarahNo ratings yet

- Financial StatementsDocument13 pagesFinancial Statementspriskilapangaila13No ratings yet

- Chapter 12Document2 pagesChapter 12Nguyen NguyenNo ratings yet

- AccountDocument4 pagesAccounthassan572.hrNo ratings yet

- Accounting Principles: Assignment - 02Document28 pagesAccounting Principles: Assignment - 02qasimtenNo ratings yet

- P1 Cash FlowDocument2 pagesP1 Cash FlowBeth Diaz LaurenteNo ratings yet

- DocxDocument6 pagesDocxVịt HoàngNo ratings yet

- Acw2491 Topic 2 WsDocument3 pagesAcw2491 Topic 2 WsSarah AngNo ratings yet

- Answer To Sample Question 2Document3 pagesAnswer To Sample Question 2Farid AbbasovNo ratings yet

- Jawaban Individual AssignmentDocument3 pagesJawaban Individual AssignmentAtoy SomarNo ratings yet

- Problem II-Analysis of AlternativesDocument6 pagesProblem II-Analysis of AlternativesChau Minh NguyenNo ratings yet

- Exercise 5 Chapter 6Document2 pagesExercise 5 Chapter 6chonabit.tNo ratings yet

- Exercise 5.1: Angtud, Mary Joy Bsma-3BDocument8 pagesExercise 5.1: Angtud, Mary Joy Bsma-3BKathlyn TajadaNo ratings yet

- GF) KFN Rf6 (8 (Psfpg6) G6/ +:yf: Chartered Accountancy Professional Cap-IDocument37 pagesGF) KFN Rf6 (8 (Psfpg6) G6/ +:yf: Chartered Accountancy Professional Cap-IsarojdawadiNo ratings yet

- Investment in Equity Securities (Prob 28-31)Document4 pagesInvestment in Equity Securities (Prob 28-31)Lorence Patrick LapidezNo ratings yet

- Chap 6 ExercisesDocument15 pagesChap 6 ExercisesQuokka KyuNo ratings yet

- Leone Lumber Company Trial Balance As of December 31 Debit CreditDocument3 pagesLeone Lumber Company Trial Balance As of December 31 Debit CreditMaitaNo ratings yet

- Closing and Post-Closing EntriesDocument13 pagesClosing and Post-Closing EntriesBrian Reyes GangcaNo ratings yet

- Assiment Salman KhanDocument6 pagesAssiment Salman Khanakber khan khanNo ratings yet

- HW CH2Document3 pagesHW CH2Minh Anh NguyễnNo ratings yet

- Problem #1: Adjusting EntriesDocument5 pagesProblem #1: Adjusting EntriesShahzad AsifNo ratings yet

- Consolidation ReportDocument10 pagesConsolidation Reportbabar zuberiNo ratings yet

- Name Assignment: Submitted To Department: Zarwah Butt AccountingDocument12 pagesName Assignment: Submitted To Department: Zarwah Butt AccountingZarwah ButtNo ratings yet

- Poa HWDocument3 pagesPoa HW赵宇哲No ratings yet

- Chapter 23 Ppe 1Document64 pagesChapter 23 Ppe 1Alliyah NasuenNo ratings yet

- AFR Session 4 ExercisesDocument10 pagesAFR Session 4 ExercisesSherif KhalifaNo ratings yet

- Problem 13.4 & 13.5Document2 pagesProblem 13.4 & 13.5Kanishka KartikeyaNo ratings yet

- Last Name, Given Name, Middle NameDocument3 pagesLast Name, Given Name, Middle NameDe chavez, John carlo R.No ratings yet

- Transactions: Balance Sheet Income StatementDocument5 pagesTransactions: Balance Sheet Income StatementKothari InvestmentsNo ratings yet

- BibDocument2 pagesBibVivian TamerayNo ratings yet

- Recording Process Illustrated Ledger JournalDocument3 pagesRecording Process Illustrated Ledger JournalCem KaradumanNo ratings yet

- Solved Gloria Detoya and Esterlina Gevera Have Operated A Successful... - Course HeroDocument4 pagesSolved Gloria Detoya and Esterlina Gevera Have Operated A Successful... - Course HeroeannetiyabNo ratings yet

- ACCT 2010 Asm2Document3 pagesACCT 2010 Asm2蛋卷 PsyvidNo ratings yet

- Activity 3Document8 pagesActivity 3Angeline Gonzales PaneloNo ratings yet

- Chap 13 - 6 To 8Document2 pagesChap 13 - 6 To 8Buenaventura, Lara Jane T.No ratings yet

- M Enterprises: Financial Statements/ReportsDocument30 pagesM Enterprises: Financial Statements/ReportsAishah Mae M. AtomarNo ratings yet

- Soal 3Document1 pageSoal 3nara kimNo ratings yet

- Name Roll No Program: Hamza Iqbal 2021-25-0001 Financial ManagementDocument9 pagesName Roll No Program: Hamza Iqbal 2021-25-0001 Financial ManagementHamza IqbalNo ratings yet

- Adjusting Entries LectureDocument13 pagesAdjusting Entries LectureJNo ratings yet

- Assignment ACC705 T2 2017Document5 pagesAssignment ACC705 T2 2017babar zuberiNo ratings yet

- Tabular AnalysisDocument3 pagesTabular Analysissilva yunizaNo ratings yet

- APC Ch9solDocument7 pagesAPC Ch9solBaymad67% (3)

- APC Ch9sol PDFDocument7 pagesAPC Ch9sol PDFBaymadNo ratings yet

- Syllabus AnswerDocument24 pagesSyllabus AnswerasdfNo ratings yet

- Investments in Financial Instruments CompleteDocument34 pagesInvestments in Financial Instruments CompleteDenise CruzNo ratings yet

- Tugas 4 - ELRISKA TIFFANI - 142200111Document6 pagesTugas 4 - ELRISKA TIFFANI - 142200111Elriska Tiffani75% (4)

- Alpha Graphics CompanyDocument2 pagesAlpha Graphics CompanyMira FebriasariNo ratings yet

- PR Pertemuan 1 - Yoga RamdhaniDocument7 pagesPR Pertemuan 1 - Yoga RamdhaniShafa Anggitar AzhariNo ratings yet

- Inventories (Problems)Document6 pagesInventories (Problems)IAN PADAYOGDOGNo ratings yet

- Chapter 4 Exercise Recording TransactionDocument4 pagesChapter 4 Exercise Recording TransactionHusen ChaabanNo ratings yet

- Putri Amalia Fillah - AKL II - Assignment 2Document3 pagesPutri Amalia Fillah - AKL II - Assignment 2Amalia FillahNo ratings yet

- Corporate Laws: Certified Finance and Accounting Professional (CFAP)Document1 pageCorporate Laws: Certified Finance and Accounting Professional (CFAP)SR TGNo ratings yet

- D) The Main Differences Between ML and TF AreDocument1 pageD) The Main Differences Between ML and TF AreSR TGNo ratings yet

- SaDocument1 pageSaSR TGNo ratings yet

- Vi. Foreign Currency RiskDocument1 pageVi. Foreign Currency RiskSR TGNo ratings yet

- A.8 A) There Are Two Issues of Which Evaluation Is Below: InventoryDocument1 pageA.8 A) There Are Two Issues of Which Evaluation Is Below: InventorySR TGNo ratings yet

- SaDocument1 pageSaSR TGNo ratings yet

- SaDocument1 pageSaSR TGNo ratings yet

- Audit, Assurance and Related Services: A.1 I. Fraud Risk FactorsDocument1 pageAudit, Assurance and Related Services: A.1 I. Fraud Risk FactorsSR TGNo ratings yet

- B) Impact On Audit Report: Effect On The Audit Report of TitmanDocument1 pageB) Impact On Audit Report: Effect On The Audit Report of TitmanSR TGNo ratings yet

- Rs. Million: The HISAB School of AccountancyDocument1 pageRs. Million: The HISAB School of AccountancySR TGNo ratings yet

- Audit, Assurance and Related Services: Mock Examination Certified Finance and Accounting Professional StageDocument1 pageAudit, Assurance and Related Services: Mock Examination Certified Finance and Accounting Professional StageSR TGNo ratings yet

- RequiredDocument1 pageRequiredSR TGNo ratings yet

- SaDocument1 pageSaSR TGNo ratings yet

- RequiredDocument1 pageRequiredSR TGNo ratings yet

- CFAP04 - Business Finance Decisions - Page 6Document1 pageCFAP04 - Business Finance Decisions - Page 6SR TGNo ratings yet

- CFAP04 - Business Finance Decisions - Page 8Document1 pageCFAP04 - Business Finance Decisions - Page 8SR TGNo ratings yet

- Required:: (End of Paper)Document1 pageRequired:: (End of Paper)SR TGNo ratings yet

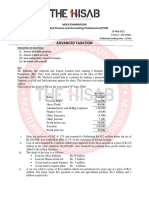

- Advanced Taxation: Certified Finance and Accounting Professional (CFAP)Document1 pageAdvanced Taxation: Certified Finance and Accounting Professional (CFAP)SR TGNo ratings yet

- Gearing: CFAP04 - Business Finance Decisions - Page 12Document1 pageGearing: CFAP04 - Business Finance Decisions - Page 12SR TGNo ratings yet

- CFAP04 - Business Finance Decisions - Page 3Document1 pageCFAP04 - Business Finance Decisions - Page 3SR TGNo ratings yet

- Interest Coverage: CFAP04 - Business Finance Decisions - Page 13Document1 pageInterest Coverage: CFAP04 - Business Finance Decisions - Page 13SR TGNo ratings yet

- Q5. Marking Scheme: CFAP04 - Business Finance Decisions - Page 11Document1 pageQ5. Marking Scheme: CFAP04 - Business Finance Decisions - Page 11SR TGNo ratings yet

- CFAP04 - Business Finance Decisions - Page 4Document1 pageCFAP04 - Business Finance Decisions - Page 4SR TGNo ratings yet

- CFAP04 - Business Finance Decisions - Page 9Document1 pageCFAP04 - Business Finance Decisions - Page 9SR TGNo ratings yet

- CFAP04 - Business Finance Decisions - Page 2Document1 pageCFAP04 - Business Finance Decisions - Page 2SR TGNo ratings yet

- Business Finance Decisions (Solution Set)Document1 pageBusiness Finance Decisions (Solution Set)SR TGNo ratings yet

- SL AL: The HISAB School of AccountancyDocument1 pageSL AL: The HISAB School of AccountancySR TGNo ratings yet

- Business Finance DecisionsDocument1 pageBusiness Finance DecisionsSR TGNo ratings yet

- The HISAB School of Accountancy: CFAP04 - Business Finance Decisions - Page 4Document1 pageThe HISAB School of Accountancy: CFAP04 - Business Finance Decisions - Page 4SR TGNo ratings yet

- The HISAB School of Accountancy: CFAP04 - Business Finance Decisions - Page 2Document1 pageThe HISAB School of Accountancy: CFAP04 - Business Finance Decisions - Page 2SR TGNo ratings yet