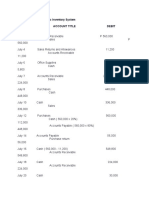

Merchandising 105 Answer Key Periodic

Merchandising 105 Answer Key Periodic

You might also like

- Accounting 1aDocument23 pagesAccounting 1aFaith Marasigan88% (16)

- Far 101 - Financial Accounting Process PDFDocument4 pagesFar 101 - Financial Accounting Process PDFReyn Saplad Perales100% (1)

- Assignment#1 ADRIANOCAÑADADocument4 pagesAssignment#1 ADRIANOCAÑADAADRIANO, Glecy C.78% (9)

- Module 7 - Merchandising Business Special TransactionsDocument40 pagesModule 7 - Merchandising Business Special TransactionsMaria Nicole OroNo ratings yet

- Post Test Receivables Answer Key PDFDocument9 pagesPost Test Receivables Answer Key PDFJOSCEL SYJONGTIANNo ratings yet

- SRCBAI ABM1 Q3M10 Merchandising Concern Part1Document14 pagesSRCBAI ABM1 Q3M10 Merchandising Concern Part1Jaye RuantoNo ratings yet

- Answer InventoryDocument7 pagesAnswer InventoryAllen Carl60% (5)

- Straight Line MethodDocument12 pagesStraight Line MethodN HasnaNo ratings yet

- Date Account Titles and Explanation P.R. Debit CreditDocument13 pagesDate Account Titles and Explanation P.R. Debit CreditNguyễn GiangNo ratings yet

- MerchandisingDocument13 pagesMerchandisingairanicolebrugada08No ratings yet

- General Journal Solution Exercises 3 PERPETUAL INVENTORY SYSTEMDocument3 pagesGeneral Journal Solution Exercises 3 PERPETUAL INVENTORY SYSTEMlemondaff1No ratings yet

- MERCHANDISING BUSINESS (Periodic Vs Perpetual)Document3 pagesMERCHANDISING BUSINESS (Periodic Vs Perpetual)Laurence Karl CurboNo ratings yet

- CB Niat 2019 Exam SolutionsDocument14 pagesCB Niat 2019 Exam Solutionsdean garciaNo ratings yet

- Case 1 For PrintDocument8 pagesCase 1 For PrintRichardDinongPascualNo ratings yet

- Inventory Systems ComparisonDocument2 pagesInventory Systems ComparisonRan CañeteNo ratings yet

- Intermediate Accounting Chapter 10 InventoriesDocument9 pagesIntermediate Accounting Chapter 10 InventoriesBlue SkyNo ratings yet

- Jornal MerchandiseDocument12 pagesJornal MerchandiseHannah Jane Toribio100% (1)

- FAR AssignmentDocument8 pagesFAR AssignmentpaololegardoNo ratings yet

- Castro Company ZABALLADocument11 pagesCastro Company ZABALLAHelping Five (H5)No ratings yet

- Pauline Anne R. Grana 11-ABM-A: To Record Purchase of Merchandise For CashDocument4 pagesPauline Anne R. Grana 11-ABM-A: To Record Purchase of Merchandise For CashPark EunbiNo ratings yet

- VertudezDocument4 pagesVertudezralph yapNo ratings yet

- Danielle Rachel Mina 1209 Male Q.4: Requirement ADocument4 pagesDanielle Rachel Mina 1209 Male Q.4: Requirement AWaz KaBoomNo ratings yet

- Myco Paque InventoriesDocument5 pagesMyco Paque InventoriesMYCO PONCE PAQUENo ratings yet

- Compute The Correct Amount of Inventory:: Problem 10-1 Amiable CompanyDocument83 pagesCompute The Correct Amount of Inventory:: Problem 10-1 Amiable CompanyIrish SungcangNo ratings yet

- Book Exercises 2Document20 pagesBook Exercises 2Ace Hulsey TevesNo ratings yet

- Merchandise Business Class Performance AnswersDocument14 pagesMerchandise Business Class Performance AnswersLerry RosellNo ratings yet

- Module VII Accounting Cycle of A Merchandising Business2Document3 pagesModule VII Accounting Cycle of A Merchandising Business2Marklein DumangengNo ratings yet

- Accounting For Merchandising BusinessDocument21 pagesAccounting For Merchandising BusinessJunel PlanosNo ratings yet

- Problem-10-4 FinalDocument2 pagesProblem-10-4 FinalAlyssa Faith NiangarNo ratings yet

- Fabm2 6a1 Books of AccountsDocument3 pagesFabm2 6a1 Books of AccountsRenz AbadNo ratings yet

- EdlynDocument10 pagesEdlynDona AdlogNo ratings yet

- Module 2Document11 pagesModule 2Deanne LumakangNo ratings yet

- Ms. Diaz Answer KeyDocument5 pagesMs. Diaz Answer KeysheeshquietNo ratings yet

- Handout No. 03 - Purchase TransactionsDocument4 pagesHandout No. 03 - Purchase TransactionsApril SasamNo ratings yet

- Accounting Cycle: 2. Recording of The Transactions in The Journal. (Journalizing)Document9 pagesAccounting Cycle: 2. Recording of The Transactions in The Journal. (Journalizing)Ada Janelle ManzanoNo ratings yet

- Answer: Problem 10-4: Requirement ADocument17 pagesAnswer: Problem 10-4: Requirement APatricia Nicole BarriosNo ratings yet

- Inventories (Financial Accounting)Document2 pagesInventories (Financial Accounting)Herlyn QuintoNo ratings yet

- Chapter 6 FAR Periodic Accounting CycleDocument5 pagesChapter 6 FAR Periodic Accounting CycleShaina Lane B. AmbataliNo ratings yet

- Chapter 4, 5, 6 AssignmentDocument23 pagesChapter 4, 5, 6 AssignmentSamantha Charlize VizcondeNo ratings yet

- Toaz - Info Adjusting Journal Entries Exercises3xlsx PRDocument22 pagesToaz - Info Adjusting Journal Entries Exercises3xlsx PRpau mejaresNo ratings yet

- Price and Quantity: Inventory Cost Flow Purchase CommitmentsDocument10 pagesPrice and Quantity: Inventory Cost Flow Purchase CommitmentsShane CalderonNo ratings yet

- Inventories (Problems)Document6 pagesInventories (Problems)IAN PADAYOGDOGNo ratings yet

- Merchandising Handout - Perpetual Vs PeriodicDocument1 pageMerchandising Handout - Perpetual Vs PeriodicTineNo ratings yet

- Calaguas AccountDocument5 pagesCalaguas AccountMargielene Taglinao-WabeNo ratings yet

- NIAT Review 3Document7 pagesNIAT Review 3April Joy InductaNo ratings yet

- ACC 101 - 3rd QuizDocument3 pagesACC 101 - 3rd QuizAdyangNo ratings yet

- Chapter 10 - Problem 2Document5 pagesChapter 10 - Problem 2Christy HabelNo ratings yet

- General Journal Date Particulars Folio DebitDocument6 pagesGeneral Journal Date Particulars Folio DebitJelaina AlimansaNo ratings yet

- CH 10 Merchandising BusinessDocument65 pagesCH 10 Merchandising BusinessKYLA RENZ DE LEONNo ratings yet

- Glamore MarketingDocument1 pageGlamore Marketingelijah daelNo ratings yet

- Midterms FAR Quiz 1Document15 pagesMidterms FAR Quiz 1mariejoyceaggabaoNo ratings yet

- Practice (Exer. 3)Document11 pagesPractice (Exer. 3)Anne Thea AtienzaNo ratings yet

- Merchandise InventoryDocument16 pagesMerchandise InventoryKristine San Luis PotencianoNo ratings yet

- PerpetualDocument23 pagesPerpetualPia SurilNo ratings yet

- Trading/Merchandising Business: DR CRDocument4 pagesTrading/Merchandising Business: DR CRshang HaiNo ratings yet

- Abad MarrietteJoyExcel Ex8Document13 pagesAbad MarrietteJoyExcel Ex8marriette joy abadNo ratings yet

- Course 1Document5 pagesCourse 1Lalaine Joyce PardiñasNo ratings yet

- Accounting Cycle For Merchandising ConcernDocument30 pagesAccounting Cycle For Merchandising ConcernMary100% (2)

- Practice Quiz - Quiz 2: Answer: Debit Accounts Receivable 26,250 Debit Freight Out 1,250 Credit Sales 27,500Document5 pagesPractice Quiz - Quiz 2: Answer: Debit Accounts Receivable 26,250 Debit Freight Out 1,250 Credit Sales 27,500Kieht catcherNo ratings yet

- Cash To AccrualDocument23 pagesCash To Accruallascona.christinerheaNo ratings yet

- 2018-0232 Beldia, Pitchie Mae G. ACT142: Auditing and Assurance: Concepts and Application 1Document8 pages2018-0232 Beldia, Pitchie Mae G. ACT142: Auditing and Assurance: Concepts and Application 1Melanie SamsonaNo ratings yet

- Acctg 112Document3 pagesAcctg 112Rathew Cassey PencilNo ratings yet

- Korean Business Dictionary: American and Korean Business Terms for the Internet AgeFrom EverandKorean Business Dictionary: American and Korean Business Terms for the Internet AgeNo ratings yet

- Macadat, Princess Heart L. - Task 8-Personal SWOTDocument2 pagesMacadat, Princess Heart L. - Task 8-Personal SWOTPrincess Heart MacadatNo ratings yet

- Macadat, Princess Heart L. - Cover Letter FormatDocument2 pagesMacadat, Princess Heart L. - Cover Letter FormatPrincess Heart MacadatNo ratings yet

- BSA1-C, Macadat, Princess Heart, L. - MyWeeklyMealPlanDocument9 pagesBSA1-C, Macadat, Princess Heart, L. - MyWeeklyMealPlanPrincess Heart MacadatNo ratings yet

- Macadat, Princess Heart, L. Assignment-FinalsDocument4 pagesMacadat, Princess Heart, L. Assignment-FinalsPrincess Heart MacadatNo ratings yet

- Macadat, Princess Heart, LDocument2 pagesMacadat, Princess Heart, LPrincess Heart MacadatNo ratings yet

- Symbol of Equal RightsDocument1 pageSymbol of Equal RightsPrincess Heart MacadatNo ratings yet

- Local StudiesDocument4 pagesLocal StudiesPrincess Heart MacadatNo ratings yet

- Chapter 5Document4 pagesChapter 5Princess Heart MacadatNo ratings yet

- 8 Source A4: 9706/33/INSERT/O/N/21 © UCLES 2021Document2 pages8 Source A4: 9706/33/INSERT/O/N/21 © UCLES 2021Ayesha sheikhNo ratings yet

- Project Sem6Document40 pagesProject Sem6Alisha riya FrancisNo ratings yet

- CHAI Pack Pack Order Form Aug-23-1Document32 pagesCHAI Pack Pack Order Form Aug-23-1Briltex IndustriesNo ratings yet

- Level Three Theory (Knowledge) ChoiceDocument17 pagesLevel Three Theory (Knowledge) ChoiceYaa Rabbii100% (1)

- YCOA Chart of AccountsDocument2,443 pagesYCOA Chart of Accountscarlos.vinklerNo ratings yet

- AIKEZ Retail Store General Journal For The Month of January 2021 Date Particulars F Debit CreditDocument20 pagesAIKEZ Retail Store General Journal For The Month of January 2021 Date Particulars F Debit CreditHasanah AmerilNo ratings yet

- Gr11 MODULE 7 ACCOUNTING BOOKSDocument24 pagesGr11 MODULE 7 ACCOUNTING BOOKSMissy EcleoNo ratings yet

- Investment in Associate 2Document2 pagesInvestment in Associate 2miss independent100% (1)

- 3.CFA财报分析 Financial Statement AnalysisDocument408 pages3.CFA财报分析 Financial Statement AnalysisliujinxinljxNo ratings yet

- Basic Accounting TerminologiesDocument25 pagesBasic Accounting TerminologiesRehan YousafNo ratings yet

- Valuation of GoodwillDocument7 pagesValuation of GoodwillRounaq Khanum284No ratings yet

- 2024 CalendarDocument48 pages2024 CalendarsathyanarayanaNo ratings yet

- Arshad Commerce: C-78 BDA KOHEFIZA, MOBILE 9893905143Document7 pagesArshad Commerce: C-78 BDA KOHEFIZA, MOBILE 9893905143Aaditya SaratheNo ratings yet

- Cibil Report RAM BABU VISHWKARMA1579275405637 PDFDocument7 pagesCibil Report RAM BABU VISHWKARMA1579275405637 PDFMONISH NAYARNo ratings yet

- IC Accounts Payable Ledger Template Updated 8552Document2 pagesIC Accounts Payable Ledger Template Updated 8552M Monjur MobinNo ratings yet

- Overview of Accountancy: (Excerpted From The FINANCIAL ACCOUNTING Textbook by Conrado T. Valix)Document26 pagesOverview of Accountancy: (Excerpted From The FINANCIAL ACCOUNTING Textbook by Conrado T. Valix)angelika dijamcoNo ratings yet

- Steiner College S Statement of Financial Position For The Year EndedDocument1 pageSteiner College S Statement of Financial Position For The Year EndedMuhammad ShahidNo ratings yet

- Lesson 10 Intercompany Transactions Exercise 2 - Suggested AnswersDocument18 pagesLesson 10 Intercompany Transactions Exercise 2 - Suggested AnswersjvNo ratings yet

- Research Design: A Study On Comparative Analysis of Two Companies From FMCG Sector. - Itc and Tata ConsumerDocument6 pagesResearch Design: A Study On Comparative Analysis of Two Companies From FMCG Sector. - Itc and Tata ConsumerRishab MaluNo ratings yet

- Book NQN KeyDocument86 pagesBook NQN KeyQuỳnh Trần Thị DiễmNo ratings yet

- 7 Fin621 Final Term Papers Solved by YushaDocument90 pages7 Fin621 Final Term Papers Solved by YushaMuhammad Yusha100% (1)

- Chap 009Document110 pagesChap 009Shilpee Haldar MishraNo ratings yet

- Analisis Sumber Dan Penggunaan Kas Pada Pt. Sepatu Bata TBK Yang Terdaftar Di Bursa Efek Indonesia Tahun 2014 - 2018Document11 pagesAnalisis Sumber Dan Penggunaan Kas Pada Pt. Sepatu Bata TBK Yang Terdaftar Di Bursa Efek Indonesia Tahun 2014 - 2018Feby SinagaNo ratings yet

- 7 Daniel R. RandallDocument10 pages7 Daniel R. RandallKareishma ShroffNo ratings yet

- Fund Flow StatementDocument16 pagesFund Flow StatementRavi RajputNo ratings yet

- TML Standalone Results Sept 2023 1Document5 pagesTML Standalone Results Sept 2023 1NagendranNo ratings yet

Download as xlsx, pdf, or txt

You might also like

- Accounting 1aDocument23 pagesAccounting 1aFaith Marasigan88% (16)

- Far 101 - Financial Accounting Process PDFDocument4 pagesFar 101 - Financial Accounting Process PDFReyn Saplad Perales100% (1)

- Assignment#1 ADRIANOCAÑADADocument4 pagesAssignment#1 ADRIANOCAÑADAADRIANO, Glecy C.78% (9)

- Module 7 - Merchandising Business Special TransactionsDocument40 pagesModule 7 - Merchandising Business Special TransactionsMaria Nicole OroNo ratings yet

- Post Test Receivables Answer Key PDFDocument9 pagesPost Test Receivables Answer Key PDFJOSCEL SYJONGTIANNo ratings yet

- SRCBAI ABM1 Q3M10 Merchandising Concern Part1Document14 pagesSRCBAI ABM1 Q3M10 Merchandising Concern Part1Jaye RuantoNo ratings yet

- Answer InventoryDocument7 pagesAnswer InventoryAllen Carl60% (5)

- Straight Line MethodDocument12 pagesStraight Line MethodN HasnaNo ratings yet

- Date Account Titles and Explanation P.R. Debit CreditDocument13 pagesDate Account Titles and Explanation P.R. Debit CreditNguyễn GiangNo ratings yet

- MerchandisingDocument13 pagesMerchandisingairanicolebrugada08No ratings yet

- General Journal Solution Exercises 3 PERPETUAL INVENTORY SYSTEMDocument3 pagesGeneral Journal Solution Exercises 3 PERPETUAL INVENTORY SYSTEMlemondaff1No ratings yet

- MERCHANDISING BUSINESS (Periodic Vs Perpetual)Document3 pagesMERCHANDISING BUSINESS (Periodic Vs Perpetual)Laurence Karl CurboNo ratings yet

- CB Niat 2019 Exam SolutionsDocument14 pagesCB Niat 2019 Exam Solutionsdean garciaNo ratings yet

- Case 1 For PrintDocument8 pagesCase 1 For PrintRichardDinongPascualNo ratings yet

- Inventory Systems ComparisonDocument2 pagesInventory Systems ComparisonRan CañeteNo ratings yet

- Intermediate Accounting Chapter 10 InventoriesDocument9 pagesIntermediate Accounting Chapter 10 InventoriesBlue SkyNo ratings yet

- Jornal MerchandiseDocument12 pagesJornal MerchandiseHannah Jane Toribio100% (1)

- FAR AssignmentDocument8 pagesFAR AssignmentpaololegardoNo ratings yet

- Castro Company ZABALLADocument11 pagesCastro Company ZABALLAHelping Five (H5)No ratings yet

- Pauline Anne R. Grana 11-ABM-A: To Record Purchase of Merchandise For CashDocument4 pagesPauline Anne R. Grana 11-ABM-A: To Record Purchase of Merchandise For CashPark EunbiNo ratings yet

- VertudezDocument4 pagesVertudezralph yapNo ratings yet

- Danielle Rachel Mina 1209 Male Q.4: Requirement ADocument4 pagesDanielle Rachel Mina 1209 Male Q.4: Requirement AWaz KaBoomNo ratings yet

- Myco Paque InventoriesDocument5 pagesMyco Paque InventoriesMYCO PONCE PAQUENo ratings yet

- Compute The Correct Amount of Inventory:: Problem 10-1 Amiable CompanyDocument83 pagesCompute The Correct Amount of Inventory:: Problem 10-1 Amiable CompanyIrish SungcangNo ratings yet

- Book Exercises 2Document20 pagesBook Exercises 2Ace Hulsey TevesNo ratings yet

- Merchandise Business Class Performance AnswersDocument14 pagesMerchandise Business Class Performance AnswersLerry RosellNo ratings yet

- Module VII Accounting Cycle of A Merchandising Business2Document3 pagesModule VII Accounting Cycle of A Merchandising Business2Marklein DumangengNo ratings yet

- Accounting For Merchandising BusinessDocument21 pagesAccounting For Merchandising BusinessJunel PlanosNo ratings yet

- Problem-10-4 FinalDocument2 pagesProblem-10-4 FinalAlyssa Faith NiangarNo ratings yet

- Fabm2 6a1 Books of AccountsDocument3 pagesFabm2 6a1 Books of AccountsRenz AbadNo ratings yet

- EdlynDocument10 pagesEdlynDona AdlogNo ratings yet

- Module 2Document11 pagesModule 2Deanne LumakangNo ratings yet

- Ms. Diaz Answer KeyDocument5 pagesMs. Diaz Answer KeysheeshquietNo ratings yet

- Handout No. 03 - Purchase TransactionsDocument4 pagesHandout No. 03 - Purchase TransactionsApril SasamNo ratings yet

- Accounting Cycle: 2. Recording of The Transactions in The Journal. (Journalizing)Document9 pagesAccounting Cycle: 2. Recording of The Transactions in The Journal. (Journalizing)Ada Janelle ManzanoNo ratings yet

- Answer: Problem 10-4: Requirement ADocument17 pagesAnswer: Problem 10-4: Requirement APatricia Nicole BarriosNo ratings yet

- Inventories (Financial Accounting)Document2 pagesInventories (Financial Accounting)Herlyn QuintoNo ratings yet

- Chapter 6 FAR Periodic Accounting CycleDocument5 pagesChapter 6 FAR Periodic Accounting CycleShaina Lane B. AmbataliNo ratings yet

- Chapter 4, 5, 6 AssignmentDocument23 pagesChapter 4, 5, 6 AssignmentSamantha Charlize VizcondeNo ratings yet

- Toaz - Info Adjusting Journal Entries Exercises3xlsx PRDocument22 pagesToaz - Info Adjusting Journal Entries Exercises3xlsx PRpau mejaresNo ratings yet

- Price and Quantity: Inventory Cost Flow Purchase CommitmentsDocument10 pagesPrice and Quantity: Inventory Cost Flow Purchase CommitmentsShane CalderonNo ratings yet

- Inventories (Problems)Document6 pagesInventories (Problems)IAN PADAYOGDOGNo ratings yet

- Merchandising Handout - Perpetual Vs PeriodicDocument1 pageMerchandising Handout - Perpetual Vs PeriodicTineNo ratings yet

- Calaguas AccountDocument5 pagesCalaguas AccountMargielene Taglinao-WabeNo ratings yet

- NIAT Review 3Document7 pagesNIAT Review 3April Joy InductaNo ratings yet

- ACC 101 - 3rd QuizDocument3 pagesACC 101 - 3rd QuizAdyangNo ratings yet

- Chapter 10 - Problem 2Document5 pagesChapter 10 - Problem 2Christy HabelNo ratings yet

- General Journal Date Particulars Folio DebitDocument6 pagesGeneral Journal Date Particulars Folio DebitJelaina AlimansaNo ratings yet

- CH 10 Merchandising BusinessDocument65 pagesCH 10 Merchandising BusinessKYLA RENZ DE LEONNo ratings yet

- Glamore MarketingDocument1 pageGlamore Marketingelijah daelNo ratings yet

- Midterms FAR Quiz 1Document15 pagesMidterms FAR Quiz 1mariejoyceaggabaoNo ratings yet

- Practice (Exer. 3)Document11 pagesPractice (Exer. 3)Anne Thea AtienzaNo ratings yet

- Merchandise InventoryDocument16 pagesMerchandise InventoryKristine San Luis PotencianoNo ratings yet

- PerpetualDocument23 pagesPerpetualPia SurilNo ratings yet

- Trading/Merchandising Business: DR CRDocument4 pagesTrading/Merchandising Business: DR CRshang HaiNo ratings yet

- Abad MarrietteJoyExcel Ex8Document13 pagesAbad MarrietteJoyExcel Ex8marriette joy abadNo ratings yet

- Course 1Document5 pagesCourse 1Lalaine Joyce PardiñasNo ratings yet

- Accounting Cycle For Merchandising ConcernDocument30 pagesAccounting Cycle For Merchandising ConcernMary100% (2)

- Practice Quiz - Quiz 2: Answer: Debit Accounts Receivable 26,250 Debit Freight Out 1,250 Credit Sales 27,500Document5 pagesPractice Quiz - Quiz 2: Answer: Debit Accounts Receivable 26,250 Debit Freight Out 1,250 Credit Sales 27,500Kieht catcherNo ratings yet

- Cash To AccrualDocument23 pagesCash To Accruallascona.christinerheaNo ratings yet

- 2018-0232 Beldia, Pitchie Mae G. ACT142: Auditing and Assurance: Concepts and Application 1Document8 pages2018-0232 Beldia, Pitchie Mae G. ACT142: Auditing and Assurance: Concepts and Application 1Melanie SamsonaNo ratings yet

- Acctg 112Document3 pagesAcctg 112Rathew Cassey PencilNo ratings yet

- Korean Business Dictionary: American and Korean Business Terms for the Internet AgeFrom EverandKorean Business Dictionary: American and Korean Business Terms for the Internet AgeNo ratings yet

- Macadat, Princess Heart L. - Task 8-Personal SWOTDocument2 pagesMacadat, Princess Heart L. - Task 8-Personal SWOTPrincess Heart MacadatNo ratings yet

- Macadat, Princess Heart L. - Cover Letter FormatDocument2 pagesMacadat, Princess Heart L. - Cover Letter FormatPrincess Heart MacadatNo ratings yet

- BSA1-C, Macadat, Princess Heart, L. - MyWeeklyMealPlanDocument9 pagesBSA1-C, Macadat, Princess Heart, L. - MyWeeklyMealPlanPrincess Heart MacadatNo ratings yet

- Macadat, Princess Heart, L. Assignment-FinalsDocument4 pagesMacadat, Princess Heart, L. Assignment-FinalsPrincess Heart MacadatNo ratings yet

- Macadat, Princess Heart, LDocument2 pagesMacadat, Princess Heart, LPrincess Heart MacadatNo ratings yet

- Symbol of Equal RightsDocument1 pageSymbol of Equal RightsPrincess Heart MacadatNo ratings yet

- Local StudiesDocument4 pagesLocal StudiesPrincess Heart MacadatNo ratings yet

- Chapter 5Document4 pagesChapter 5Princess Heart MacadatNo ratings yet

- 8 Source A4: 9706/33/INSERT/O/N/21 © UCLES 2021Document2 pages8 Source A4: 9706/33/INSERT/O/N/21 © UCLES 2021Ayesha sheikhNo ratings yet

- Project Sem6Document40 pagesProject Sem6Alisha riya FrancisNo ratings yet

- CHAI Pack Pack Order Form Aug-23-1Document32 pagesCHAI Pack Pack Order Form Aug-23-1Briltex IndustriesNo ratings yet

- Level Three Theory (Knowledge) ChoiceDocument17 pagesLevel Three Theory (Knowledge) ChoiceYaa Rabbii100% (1)

- YCOA Chart of AccountsDocument2,443 pagesYCOA Chart of Accountscarlos.vinklerNo ratings yet

- AIKEZ Retail Store General Journal For The Month of January 2021 Date Particulars F Debit CreditDocument20 pagesAIKEZ Retail Store General Journal For The Month of January 2021 Date Particulars F Debit CreditHasanah AmerilNo ratings yet

- Gr11 MODULE 7 ACCOUNTING BOOKSDocument24 pagesGr11 MODULE 7 ACCOUNTING BOOKSMissy EcleoNo ratings yet

- Investment in Associate 2Document2 pagesInvestment in Associate 2miss independent100% (1)

- 3.CFA财报分析 Financial Statement AnalysisDocument408 pages3.CFA财报分析 Financial Statement AnalysisliujinxinljxNo ratings yet

- Basic Accounting TerminologiesDocument25 pagesBasic Accounting TerminologiesRehan YousafNo ratings yet

- Valuation of GoodwillDocument7 pagesValuation of GoodwillRounaq Khanum284No ratings yet

- 2024 CalendarDocument48 pages2024 CalendarsathyanarayanaNo ratings yet

- Arshad Commerce: C-78 BDA KOHEFIZA, MOBILE 9893905143Document7 pagesArshad Commerce: C-78 BDA KOHEFIZA, MOBILE 9893905143Aaditya SaratheNo ratings yet

- Cibil Report RAM BABU VISHWKARMA1579275405637 PDFDocument7 pagesCibil Report RAM BABU VISHWKARMA1579275405637 PDFMONISH NAYARNo ratings yet

- IC Accounts Payable Ledger Template Updated 8552Document2 pagesIC Accounts Payable Ledger Template Updated 8552M Monjur MobinNo ratings yet

- Overview of Accountancy: (Excerpted From The FINANCIAL ACCOUNTING Textbook by Conrado T. Valix)Document26 pagesOverview of Accountancy: (Excerpted From The FINANCIAL ACCOUNTING Textbook by Conrado T. Valix)angelika dijamcoNo ratings yet

- Steiner College S Statement of Financial Position For The Year EndedDocument1 pageSteiner College S Statement of Financial Position For The Year EndedMuhammad ShahidNo ratings yet

- Lesson 10 Intercompany Transactions Exercise 2 - Suggested AnswersDocument18 pagesLesson 10 Intercompany Transactions Exercise 2 - Suggested AnswersjvNo ratings yet

- Research Design: A Study On Comparative Analysis of Two Companies From FMCG Sector. - Itc and Tata ConsumerDocument6 pagesResearch Design: A Study On Comparative Analysis of Two Companies From FMCG Sector. - Itc and Tata ConsumerRishab MaluNo ratings yet

- Book NQN KeyDocument86 pagesBook NQN KeyQuỳnh Trần Thị DiễmNo ratings yet

- 7 Fin621 Final Term Papers Solved by YushaDocument90 pages7 Fin621 Final Term Papers Solved by YushaMuhammad Yusha100% (1)

- Chap 009Document110 pagesChap 009Shilpee Haldar MishraNo ratings yet

- Analisis Sumber Dan Penggunaan Kas Pada Pt. Sepatu Bata TBK Yang Terdaftar Di Bursa Efek Indonesia Tahun 2014 - 2018Document11 pagesAnalisis Sumber Dan Penggunaan Kas Pada Pt. Sepatu Bata TBK Yang Terdaftar Di Bursa Efek Indonesia Tahun 2014 - 2018Feby SinagaNo ratings yet

- 7 Daniel R. RandallDocument10 pages7 Daniel R. RandallKareishma ShroffNo ratings yet

- Fund Flow StatementDocument16 pagesFund Flow StatementRavi RajputNo ratings yet

- TML Standalone Results Sept 2023 1Document5 pagesTML Standalone Results Sept 2023 1NagendranNo ratings yet