Download as pdf or txt

You might also like

- Food and Beverages at Southwestern University Football GamesDocument2 pagesFood and Beverages at Southwestern University Football Gamesarnel83% (6)

- Assignment SITXFIN004 Prepare and Monitor BudgetsDocument7 pagesAssignment SITXFIN004 Prepare and Monitor Budgetsmilan shresthaNo ratings yet

- Chapter 10, Question 1. ADocument25 pagesChapter 10, Question 1. AAnh ThưNo ratings yet

- Exercise 8.1 9.3Document8 pagesExercise 8.1 9.3debate dd100% (1)

- Cattle Fattening FinancialsDocument5 pagesCattle Fattening Financialsprince kupaNo ratings yet

- Business PlanDocument10 pagesBusiness PlanGlinore Rodriguez75% (4)

- Chapter 10, Question 1. ADocument22 pagesChapter 10, Question 1. ANeldybanik100% (2)

- Topic 6 - Test Your Skills Student WorksheetDocument6 pagesTopic 6 - Test Your Skills Student WorksheetPhương BùiNo ratings yet

- Topic 6 - Test Your Skills Student Worksheet 2Document6 pagesTopic 6 - Test Your Skills Student Worksheet 2Phương BùiNo ratings yet

- Case Study - FootballDocument21 pagesCase Study - FootballJemarse Gumpal100% (2)

- Case Study For Southwestern University Food Service RevenueDocument4 pagesCase Study For Southwestern University Food Service RevenuekngsniperNo ratings yet

- Efren Quesada SITXFI EXCELDocument4 pagesEfren Quesada SITXFI EXCELefrenquesada84No ratings yet

- Case Study-Food and Beverages at Southwestern University Football GamesDocument2 pagesCase Study-Food and Beverages at Southwestern University Football GamesMd.Arif MiahNo ratings yet

- Case Study Southwestern UniversityDocument4 pagesCase Study Southwestern Universitybobbyli0% (1)

- InancialDocument25 pagesInancialRaj ThakurNo ratings yet

- Coffee Shop Financial PlanDocument28 pagesCoffee Shop Financial PlangerardmacNo ratings yet

- Herjit Budget CateringDocument5 pagesHerjit Budget CateringAnaya RantaNo ratings yet

- Best LifeDocument11 pagesBest Lifeapi-654396911No ratings yet

- New Financial 333Document36 pagesNew Financial 333Mhar Bermudez Eulin JrNo ratings yet

- A Feasibility Study of Barbeque Store in Brgy. Atabay Hilongos, LeyteDocument14 pagesA Feasibility Study of Barbeque Store in Brgy. Atabay Hilongos, LeyteMary Jean ManlaweNo ratings yet

- SDocument13 pagesSdebate ddNo ratings yet

- Dyersville IA (Field of Dreams Stadium) UPDATED Pro Forma 211222Document18 pagesDyersville IA (Field of Dreams Stadium) UPDATED Pro Forma 211222A.W. CarrosNo ratings yet

- HCCDocument32 pagesHCCMico BolorNo ratings yet

- Assignment 1 10 %Document9 pagesAssignment 1 10 %HaRry sanghaNo ratings yet

- Review of Cost Percentage Formula: Numerator (E.g.cost $) Food Cost % Denominator (Sales $)Document3 pagesReview of Cost Percentage Formula: Numerator (E.g.cost $) Food Cost % Denominator (Sales $)Yu EnNo ratings yet

- Capestone Analysis ExcelDocument29 pagesCapestone Analysis Excelprajout2014No ratings yet

- Casino Visitation, Revenue, and Impact Assessment (11!19!19)Document87 pagesCasino Visitation, Revenue, and Impact Assessment (11!19!19)WSETNo ratings yet

- Sales Mix Tutorial Assignment StudentsDocument3 pagesSales Mix Tutorial Assignment StudentsYu EnNo ratings yet

- 420C14Document38 pages420C14Suhail100% (1)

- ECO101 PS1 Questions and SolutionsDocument13 pagesECO101 PS1 Questions and SolutionsshenyounanNo ratings yet

- Copy of Broiler FinancialsDocument5 pagesCopy of Broiler Financialskevior2No ratings yet

- FINANCIAL PLAN - DraftDocument5 pagesFINANCIAL PLAN - DraftJean LarsNo ratings yet

- ICE #3 - Break Even and Pricing (Semester 3)Document4 pagesICE #3 - Break Even and Pricing (Semester 3)Ava Farjad100% (1)

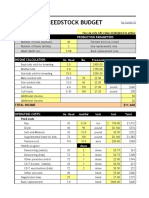

- 2016 Goat Seedstock Budget: Annual KiddingDocument8 pages2016 Goat Seedstock Budget: Annual KiddingGeros dienosNo ratings yet

- Beron - FinancialForecastingDocument25 pagesBeron - FinancialForecastingKat BeronNo ratings yet

- Critical Issues: Spring One of A Kind ShowDocument6 pagesCritical Issues: Spring One of A Kind ShowAmie NguyenNo ratings yet

- Lesson 3Document29 pagesLesson 3Anh MinhNo ratings yet

- Sesion 09 RemovedDocument1 pageSesion 09 Removedalan WalkerNo ratings yet

- Maxi's Grocery MartDocument2 pagesMaxi's Grocery MartCaden HustonNo ratings yet

- Part A - Task 1 - DRAFT BudgetDocument1 pagePart A - Task 1 - DRAFT BudgetNadeeka sanjeewaniNo ratings yet

- Labong Ice CreamDocument15 pagesLabong Ice Creamdelacruzmarklloyd14No ratings yet

- Monthly Sales: PriceDocument5 pagesMonthly Sales: PriceChicken NoodlesNo ratings yet

- JollibeeDocument2 pagesJollibeeDon PePeNo ratings yet

- Case SolutionDocument12 pagesCase Solutionsoniasogreat100% (1)

- Giovanni Slack - HEALTH REPORTDocument6 pagesGiovanni Slack - HEALTH REPORTGiovanni SlackNo ratings yet

- Goal Seek ProblemDocument8 pagesGoal Seek ProblemAntline Rishone J RNo ratings yet

- Azarcon Bryan FinancialPlanDocument6 pagesAzarcon Bryan FinancialPlanazarcon.bryanNo ratings yet

- Project NPV Sensitivity AnalysisDocument54 pagesProject NPV Sensitivity AnalysisAsad Mehmood100% (3)

- Place and RevenueDocument10 pagesPlace and Revenuechandra kiranNo ratings yet

- Final BudgetDocument6 pagesFinal Budgetapi-272111619No ratings yet

- Business-Plan FormatDocument9 pagesBusiness-Plan FormatIT'z YOU're MISS INFINITYNo ratings yet

- Cafe CostingDocument2 pagesCafe CostingTrina BastanNo ratings yet

- Feasibility For Title ResearchDocument11 pagesFeasibility For Title Researchpeppagab24No ratings yet

- 08 ENMA302 InflationExamplesDocument8 pages08 ENMA302 InflationExamplesMotazNo ratings yet

- MacabacusEssentialsDemoComplete 210413 104622Document21 pagesMacabacusEssentialsDemoComplete 210413 104622Pratik PatwaNo ratings yet

- Loan Amount $ 100,000.00 Term in Months 180 Interest Rate PaymentDocument6 pagesLoan Amount $ 100,000.00 Term in Months 180 Interest Rate PaymentabcdNo ratings yet

- Millions of Dollars Except Per-Share DataDocument17 pagesMillions of Dollars Except Per-Share DataWasp_007_007No ratings yet

- Specialty Canned Food Products World Summary: Market Values & Financials by CountryFrom EverandSpecialty Canned Food Products World Summary: Market Values & Financials by CountryNo ratings yet

- 15.0 Statistical Quality ControlDocument14 pages15.0 Statistical Quality ControlKEZIAH REVE B. RODRIGUEZNo ratings yet

- CaseStudy WTVXDocument4 pagesCaseStudy WTVXKEZIAH REVE B. RODRIGUEZNo ratings yet

- 10.0 Integer - Goal - and - NonLinear - ProgrammingDocument19 pages10.0 Integer - Goal - and - NonLinear - ProgrammingKEZIAH REVE B. RODRIGUEZNo ratings yet

- Case26 - Merck & Co., IncDocument6 pagesCase26 - Merck & Co., IncKEZIAH REVE B. RODRIGUEZNo ratings yet

- Case04 - AirTran AirwaysDocument13 pagesCase04 - AirTran AirwaysKEZIAH REVE B. RODRIGUEZNo ratings yet

- 5.0 ForecastingDocument23 pages5.0 ForecastingKEZIAH REVE B. RODRIGUEZNo ratings yet

- Case13 - Starbucks CorporationDocument19 pagesCase13 - Starbucks CorporationKEZIAH REVE B. RODRIGUEZNo ratings yet

- Case02 - Merryland Amusement ParkDocument9 pagesCase02 - Merryland Amusement ParkKEZIAH REVE B. RODRIGUEZNo ratings yet

- Risk and Return - Capital Marketing TheoryDocument19 pagesRisk and Return - Capital Marketing TheoryKEZIAH REVE B. RODRIGUEZNo ratings yet

- Asset Allocation in The Era of High InflationDocument12 pagesAsset Allocation in The Era of High InflationKEZIAH REVE B. RODRIGUEZNo ratings yet

- Financial Forecasting and PlanningDocument13 pagesFinancial Forecasting and PlanningKEZIAH REVE B. RODRIGUEZNo ratings yet

- 1.2 Analyzing The External Environment of The FirmDocument18 pages1.2 Analyzing The External Environment of The FirmKEZIAH REVE B. RODRIGUEZNo ratings yet

- Chilean Pension SystemDocument5 pagesChilean Pension SystemKEZIAH REVE B. RODRIGUEZNo ratings yet

- BA205 EssayAssignment TheShiftToRemoteWorkLessensWageGrowthPressures RodriguezDocument5 pagesBA205 EssayAssignment TheShiftToRemoteWorkLessensWageGrowthPressures RodriguezKEZIAH REVE B. RODRIGUEZNo ratings yet

- World Economic OutlookDocument6 pagesWorld Economic OutlookKEZIAH REVE B. RODRIGUEZNo ratings yet

- Singapore - Working Towards ProsperityDocument13 pagesSingapore - Working Towards ProsperityKEZIAH REVE B. RODRIGUEZNo ratings yet

- Money and The Central Bank SystemDocument9 pagesMoney and The Central Bank SystemKEZIAH REVE B. RODRIGUEZNo ratings yet

- Behavioral Economics and Game TheoryDocument11 pagesBehavioral Economics and Game TheoryKEZIAH REVE B. RODRIGUEZNo ratings yet

- Research 2 Final Defense Thesis Defended Cutie Copy AnnDocument12 pagesResearch 2 Final Defense Thesis Defended Cutie Copy AnnCher Angeline Rico RodriguezNo ratings yet

- Marketing Food PandaDocument12 pagesMarketing Food PandaMd Kausar KhanNo ratings yet

- Ch08 ITMDocument27 pagesCh08 ITMAbdulkadir JeilaniNo ratings yet

- 07 Rawlbolts Plugs AnchorsDocument1 page07 Rawlbolts Plugs AnchorsLincolnNo ratings yet

- NH73034207108458 Finance InvoiceDocument1 pageNH73034207108458 Finance InvoiceNaresh kumarNo ratings yet

- Introduction To Business To Business Marketing - 1Document12 pagesIntroduction To Business To Business Marketing - 1HassanNo ratings yet

- Relationship of Bank and CustomerDocument7 pagesRelationship of Bank and CustomerSelvenderan RamasamyNo ratings yet

- FLANSI CAP SONDA CatalogsDocument30 pagesFLANSI CAP SONDA CatalogsTeodor Ioan Ghinet Ghinet DorinaNo ratings yet

- Hydrogen: Opening Up New Possibilities With The Highest Thermal Conductivity and Pressure of All Fuel GasesDocument2 pagesHydrogen: Opening Up New Possibilities With The Highest Thermal Conductivity and Pressure of All Fuel GasesThasarathan RavichandranNo ratings yet

- InternsDocument7 pagesInternsSadath KhanNo ratings yet

- Employee Training and Development Chap02Document25 pagesEmployee Training and Development Chap02han zaiNo ratings yet

- Risk-Based Approach in Financial Crime Mitigation: A CookbookDocument11 pagesRisk-Based Approach in Financial Crime Mitigation: A Cookbookwiwid permamaNo ratings yet

- 97-Article Text-154-1-10-20200328Document12 pages97-Article Text-154-1-10-20200328023RATIH WULANDARINo ratings yet

- Personal Leave Policy TemplateDocument3 pagesPersonal Leave Policy TemplateGEETHA LAKSHMI HNo ratings yet

- Vinra Group PortfolioDocument40 pagesVinra Group PortfolioDerlyn RichardNo ratings yet

- ZeriaDocument16 pagesZeriaBhaskar KulkarniNo ratings yet

- Entrepreneurship in NursingDocument14 pagesEntrepreneurship in Nursingmplanner127No ratings yet

- Strategy, Value Innovation, Knowledge Economy ReviewDocument3 pagesStrategy, Value Innovation, Knowledge Economy ReviewDiana Leonita FajriNo ratings yet

- Simple Interest Complete ChapterDocument81 pagesSimple Interest Complete ChapterarobindatictNo ratings yet

- Tourism Good Practice Guide PDFDocument38 pagesTourism Good Practice Guide PDFEva MarieNo ratings yet

- Blohm + Voss Oil Tools: Automated-Multi-Pipe ElevatorsDocument241 pagesBlohm + Voss Oil Tools: Automated-Multi-Pipe Elevatorsfreddi04No ratings yet

- Factory Talk Pharma SuiteDocument2 pagesFactory Talk Pharma SuiteAdel AdelNo ratings yet

- Data Mining - Sunny ShahDocument12 pagesData Mining - Sunny ShahArun YashodharanNo ratings yet

- Project 1Document20 pagesProject 1pandurang parkarNo ratings yet

- CPSPM 51119392 1715007813Document29 pagesCPSPM 51119392 1715007813Nittu SharmaNo ratings yet

- EQT AB Year-End Report 2023Document33 pagesEQT AB Year-End Report 2023Ftu NGUYỄN THỊ NGỌC MINHNo ratings yet

- Manifestación de 15 Minutos ReviewDocument4 pagesManifestación de 15 Minutos ReviewCarlos AlmeidaNo ratings yet

- Project Innovation Egg FingersDocument11 pagesProject Innovation Egg FingersPpatrick Pingol CNo ratings yet

- Solving Construction Estimating Puzzle - Guide 1Document12 pagesSolving Construction Estimating Puzzle - Guide 11983dgNo ratings yet

- Chapter 2 TourismDocument38 pagesChapter 2 TourismstarNo ratings yet