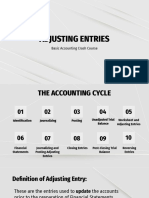

Adjusting Entries Notes

Adjusting Entries Notes

You might also like

- Basic Financial Accounting and Reporting (Bfar) : Philippine Based (Summary and Class Notes)Document17 pagesBasic Financial Accounting and Reporting (Bfar) : Philippine Based (Summary and Class Notes)LiaNo ratings yet

- Adjusting Account, WORK SHEET-FINALDocument43 pagesAdjusting Account, WORK SHEET-FINALChowdhury Mobarrat Haider Adnan100% (1)

- Strategic Management Final ExamDocument6 pagesStrategic Management Final Examsynwithg100% (1)

- Adjusting Journal Entry TugasDocument7 pagesAdjusting Journal Entry TugasLulu IstianahNo ratings yet

- Adjusting EntriesDocument2 pagesAdjusting Entriesitsayuhthing100% (1)

- M7C Adjusting Process Prepaid ExpensesDocument8 pagesM7C Adjusting Process Prepaid ExpensesCharles Eli AlejandroNo ratings yet

- Adjusting Entries IllustrationsDocument3 pagesAdjusting Entries IllustrationsHeeseung LeeNo ratings yet

- FOW 9 - PA - Notes Session 2Document15 pagesFOW 9 - PA - Notes Session 223006022No ratings yet

- Adjusting Process ValixDocument28 pagesAdjusting Process ValixjepsyutNo ratings yet

- ADJUSTING ENTRIES Part 3Document5 pagesADJUSTING ENTRIES Part 3MOCHI SSABELLENo ratings yet

- A3. Year End AdjustmentsDocument9 pagesA3. Year End AdjustmentsFrankNo ratings yet

- Topic 3 Lecture Notes - Accrual AccountingDocument23 pagesTopic 3 Lecture Notes - Accrual AccountingShiftussy Enjoyer (JoniXx)No ratings yet

- Solutions Totutorial 1-Fall 2022Document8 pagesSolutions Totutorial 1-Fall 2022chtiouirayyenNo ratings yet

- Receivables - AccountingDocument11 pagesReceivables - AccountingDairymple MendeNo ratings yet

- Adjusting Entries: Basic Accounting Crash CourseDocument77 pagesAdjusting Entries: Basic Accounting Crash CoursesmileseptemberNo ratings yet

- Unit 3: Current Liabilities and ContingenciesDocument22 pagesUnit 3: Current Liabilities and Contingenciesyebegashet100% (1)

- Unit 10 - Assignment LO2Document11 pagesUnit 10 - Assignment LO2Yasser ZayedNo ratings yet

- Topic 4 - Completing The Accounting CycleDocument52 pagesTopic 4 - Completing The Accounting CycleLA Syamsul100% (1)

- Fundamentals of ABM1 - Q4 - LAS1 DRAFTDocument17 pagesFundamentals of ABM1 - Q4 - LAS1 DRAFTSitti Halima Amilbahar AdgesNo ratings yet

- Exam Revision - Chapter 3 4Document6 pagesExam Revision - Chapter 3 4Vũ Thị NgoanNo ratings yet

- Accounting: Adjusting EntriesDocument11 pagesAccounting: Adjusting EntriesCamellia100% (2)

- Sas Certified Accounting Technician Level 1 Module 2Document29 pagesSas Certified Accounting Technician Level 1 Module 2Plame GaseroNo ratings yet

- LECTURE 7 Accounting For Merchandising Activities Periodic and Perpetual BSAFDocument40 pagesLECTURE 7 Accounting For Merchandising Activities Periodic and Perpetual BSAFShahzad C7No ratings yet

- Lecture Slides - Chapter 3 4Document82 pagesLecture Slides - Chapter 3 4Bùi Phan Ý Nhi100% (1)

- Exam Revision - 3 & 4 SolDocument6 pagesExam Revision - 3 & 4 SolNguyễn Minh ĐứcNo ratings yet

- 2023 Acc Term3 Revision MEMO ENG - 30.08.2023Document12 pages2023 Acc Term3 Revision MEMO ENG - 30.08.2023sisikelelwen05No ratings yet

- Diy-Exercises (Questionnaires)Document31 pagesDiy-Exercises (Questionnaires)May RamosNo ratings yet

- FABM1 Q4 M1 Preparing-Adjusting-EntriesDocument14 pagesFABM1 Q4 M1 Preparing-Adjusting-EntriesXedric JuantaNo ratings yet

- B124 Book 3 CH 2+3+4 + Book 5 CH 1Document81 pagesB124 Book 3 CH 2+3+4 + Book 5 CH 1بث مباشر فورت نايت سيرفر خاصNo ratings yet

- Basic Accounting Practice - Adjusting Entries-3Document34 pagesBasic Accounting Practice - Adjusting Entries-3randel10caneteNo ratings yet

- Lesson 3b Adjusting The AccountsDocument3 pagesLesson 3b Adjusting The AccountsBenedict CladoNo ratings yet

- POA WK 7 LECT 2 VER 1 28032021 115402am 17112022 110442am 06052023 101809amDocument65 pagesPOA WK 7 LECT 2 VER 1 28032021 115402am 17112022 110442am 06052023 101809ammuhammad atifNo ratings yet

- Unit 5: Current Liabilities and ContingenciesDocument21 pagesUnit 5: Current Liabilities and Contingenciessamuel kebedeNo ratings yet

- Business Transactions and Their Analysis As Applied To The Accounting Cycle of A Service Business (Part Ii-A)Document9 pagesBusiness Transactions and Their Analysis As Applied To The Accounting Cycle of A Service Business (Part Ii-A)Tumamudtamud, JenaNo ratings yet

- FABM1 LAS 7 Adjusting-EntriesDocument12 pagesFABM1 LAS 7 Adjusting-EntriesVenus AriateNo ratings yet

- Accounting Concepts and PrinciplesDocument30 pagesAccounting Concepts and PrinciplesKristine Lei Del MundoNo ratings yet

- Handouts ACCOUNTING-2Document39 pagesHandouts ACCOUNTING-2Marc John IlanoNo ratings yet

- Unit - TWO EdtdDocument14 pagesUnit - TWO EdtdHaileNo ratings yet

- Unit 3Document23 pagesUnit 3Nigussie BerhanuNo ratings yet

- Chapter 4Document16 pagesChapter 4Jonh BekaNo ratings yet

- Acc 201 CH3Document7 pagesAcc 201 CH3Trickster TwelveNo ratings yet

- 1st Semester Dec 2021 PDFDocument8 pages1st Semester Dec 2021 PDFroshanNo ratings yet

- Adjusting EntriesDocument14 pagesAdjusting EntriesSeri CrisologoNo ratings yet

- Accounts Receivable Handout PDFDocument2 pagesAccounts Receivable Handout PDFChristine Joy Rapi MarsoNo ratings yet

- Fundamentals of Accountancy Business and Management 1 11 FourthDocument4 pagesFundamentals of Accountancy Business and Management 1 11 FourthPaulo Amposta CarpioNo ratings yet

- Accounting Chaprter 3Document49 pagesAccounting Chaprter 3rashmiaakshaNo ratings yet

- Module 2 Concept of IncomeDocument3 pagesModule 2 Concept of IncomeNormel DecalaoNo ratings yet

- Chapter 3 Current Liability PayrollDocument39 pagesChapter 3 Current Liability PayrollAbdi Mucee Tube100% (1)

- Exam Revision - Chapter 9 10Document7 pagesExam Revision - Chapter 9 10Vũ Thị NgoanNo ratings yet

- Chapter Two Current Liabilities and ContingenciesDocument10 pagesChapter Two Current Liabilities and ContingenciesBlack boxNo ratings yet

- Exam Revision - 9 & 10 SolDocument7 pagesExam Revision - 9 & 10 SolNguyễn Minh ĐứcNo ratings yet

- Adjusting The Book of AccountsDocument33 pagesAdjusting The Book of Accountsjoshua zabala100% (1)

- Intermediate Accounting 1 First Grading Examination: Name: Date: Professor: Section: ScoreDocument20 pagesIntermediate Accounting 1 First Grading Examination: Name: Date: Professor: Section: ScoreJulia Andrea Yting100% (3)

- Fabm1 PPT Q2W3Document43 pagesFabm1 PPT Q2W3giselle100% (2)

- Introduction To Accounting - Adjusting EntriesDocument39 pagesIntroduction To Accounting - Adjusting EntriesRon Hoover Mercene100% (1)

- Adjusting EntriesDocument18 pagesAdjusting EntriesAmie Jane MirandaNo ratings yet

- DMBA104Document8 pagesDMBA104chetan kansalNo ratings yet

- IntAcc-1 Accounting For ReceivablesDocument13 pagesIntAcc-1 Accounting For ReceivablesShekainah BNo ratings yet

- Financial Accounting Chapter 9: Accounts Receivable: Classification of ReceivablesDocument2 pagesFinancial Accounting Chapter 9: Accounts Receivable: Classification of ReceivablesMay Grethel Joy PeranteNo ratings yet

- Accounts Receivable: Total Trade Receivables Total Current ReceivablesDocument4 pagesAccounts Receivable: Total Trade Receivables Total Current ReceivablesSano ManjiroNo ratings yet

- Chap12 Insurance ContractDocument2 pagesChap12 Insurance ContractwingNo ratings yet

- AP InventoriesDocument7 pagesAP InventorieswingNo ratings yet

- Book Value Per Share (Problems)Document3 pagesBook Value Per Share (Problems)wingNo ratings yet

- AUDIT OF SHAREHOLDERS (Probs)Document4 pagesAUDIT OF SHAREHOLDERS (Probs)wingNo ratings yet

- KLBF 30 Sept 2022Document147 pagesKLBF 30 Sept 2022asdasNo ratings yet

- Strategic Analysis - Harley DavidsonDocument12 pagesStrategic Analysis - Harley DavidsonSimran PoptaniNo ratings yet

- Risk RegisterDocument5 pagesRisk Registerfavour Golden Entertainment starkidNo ratings yet

- New Arambagh Trading - PCG1408Document1 pageNew Arambagh Trading - PCG1408AvijitSinharoyNo ratings yet

- Project Report - Capital MarketDocument33 pagesProject Report - Capital MarketPragati DixitNo ratings yet

- Export Import Procedures and DocumentationDocument11 pagesExport Import Procedures and DocumentationTeena RawatNo ratings yet

- Vol 141Document104 pagesVol 141Rendi100% (1)

- Foreign Exchange Rates (3070)Document10 pagesForeign Exchange Rates (3070)Ahmad vlogsNo ratings yet

- Cma Cia 3Document12 pagesCma Cia 3DIVYANG AGARWAL 2023291No ratings yet

- OFFER LETTER - Aman YadavDocument3 pagesOFFER LETTER - Aman YadavAman YadavNo ratings yet

- Strategy For Sustainable ConstructionDocument64 pagesStrategy For Sustainable ConstructionDanang Desfri AbdilahNo ratings yet

- Description: S&P/Asx All Technology IndexDocument6 pagesDescription: S&P/Asx All Technology IndexSuhasNo ratings yet

- Affidavit of Consolidation..Document2 pagesAffidavit of Consolidation..Sa LeeNo ratings yet

- Module 3 Market Sizing IntermediateDocument14 pagesModule 3 Market Sizing IntermediateBas KelderNo ratings yet

- IMPACT OF REPROGRAPHIC MACHINE STUDENT 039 CorrDocument55 pagesIMPACT OF REPROGRAPHIC MACHINE STUDENT 039 CorrIfeji u. johnNo ratings yet

- FORMAT-Revised IAR - QualifiedDocument2 pagesFORMAT-Revised IAR - QualifiedGier Rizaldo BulaclacNo ratings yet

- Inventory ModelsDocument30 pagesInventory ModelsAmarendra Sharma ChennapragadaNo ratings yet

- Competition Law - PALS Lecture PDFDocument37 pagesCompetition Law - PALS Lecture PDFMaying Dadula RaymundoNo ratings yet

- Affect of Green Marketing On ConsumersDocument17 pagesAffect of Green Marketing On Consumersjuan felipe betancourt lopezNo ratings yet

- Differentiate Fiscal and Calendar Year: 2. Define Adjusting EntriesDocument9 pagesDifferentiate Fiscal and Calendar Year: 2. Define Adjusting EntriesGmef Syme FerreraNo ratings yet

- MUKANDDocument2 pagesMUKANDmakrand87No ratings yet

- Chapter 5: Accounting For Merchandising Operations: Question 1 A, B & CDocument3 pagesChapter 5: Accounting For Merchandising Operations: Question 1 A, B & CTyra CoyNo ratings yet

- Principles of Accounts For CSEC®: 2nd EditionDocument20 pagesPrinciples of Accounts For CSEC®: 2nd EditionVeronica BaileyNo ratings yet

- LH 9 - Final Accounts ProblemsDocument29 pagesLH 9 - Final Accounts ProblemsHarshavardhanNo ratings yet

- OjiFS SR 2019 Print VersionDocument50 pagesOjiFS SR 2019 Print VersionVirginia MainardiNo ratings yet

- Economics For Today 5th Edition Layton Solutions ManualDocument10 pagesEconomics For Today 5th Edition Layton Solutions Manualcassandracruzpkteqnymcf100% (39)

- Supply Chain Performance: Achieving Strategic Fit and ScopeDocument24 pagesSupply Chain Performance: Achieving Strategic Fit and ScopeRahul VermaNo ratings yet

- NM1607R - S2 2022 (For S1 2022 Students) RESIT EXAM Question PAPERDocument9 pagesNM1607R - S2 2022 (For S1 2022 Students) RESIT EXAM Question PAPERrecovaNo ratings yet

- Analisis Pengendalian Kualitas Proses Pengelasan (Welding) Dengan Pendekatan Six Sigma Pada Proyek Pt. XyzDocument13 pagesAnalisis Pengendalian Kualitas Proses Pengelasan (Welding) Dengan Pendekatan Six Sigma Pada Proyek Pt. Xyzaprillia rizkyNo ratings yet

Download as docx, pdf, or txt

You might also like

- Basic Financial Accounting and Reporting (Bfar) : Philippine Based (Summary and Class Notes)Document17 pagesBasic Financial Accounting and Reporting (Bfar) : Philippine Based (Summary and Class Notes)LiaNo ratings yet

- Adjusting Account, WORK SHEET-FINALDocument43 pagesAdjusting Account, WORK SHEET-FINALChowdhury Mobarrat Haider Adnan100% (1)

- Strategic Management Final ExamDocument6 pagesStrategic Management Final Examsynwithg100% (1)

- Adjusting Journal Entry TugasDocument7 pagesAdjusting Journal Entry TugasLulu IstianahNo ratings yet

- Adjusting EntriesDocument2 pagesAdjusting Entriesitsayuhthing100% (1)

- M7C Adjusting Process Prepaid ExpensesDocument8 pagesM7C Adjusting Process Prepaid ExpensesCharles Eli AlejandroNo ratings yet

- Adjusting Entries IllustrationsDocument3 pagesAdjusting Entries IllustrationsHeeseung LeeNo ratings yet

- FOW 9 - PA - Notes Session 2Document15 pagesFOW 9 - PA - Notes Session 223006022No ratings yet

- Adjusting Process ValixDocument28 pagesAdjusting Process ValixjepsyutNo ratings yet

- ADJUSTING ENTRIES Part 3Document5 pagesADJUSTING ENTRIES Part 3MOCHI SSABELLENo ratings yet

- A3. Year End AdjustmentsDocument9 pagesA3. Year End AdjustmentsFrankNo ratings yet

- Topic 3 Lecture Notes - Accrual AccountingDocument23 pagesTopic 3 Lecture Notes - Accrual AccountingShiftussy Enjoyer (JoniXx)No ratings yet

- Solutions Totutorial 1-Fall 2022Document8 pagesSolutions Totutorial 1-Fall 2022chtiouirayyenNo ratings yet

- Receivables - AccountingDocument11 pagesReceivables - AccountingDairymple MendeNo ratings yet

- Adjusting Entries: Basic Accounting Crash CourseDocument77 pagesAdjusting Entries: Basic Accounting Crash CoursesmileseptemberNo ratings yet

- Unit 3: Current Liabilities and ContingenciesDocument22 pagesUnit 3: Current Liabilities and Contingenciesyebegashet100% (1)

- Unit 10 - Assignment LO2Document11 pagesUnit 10 - Assignment LO2Yasser ZayedNo ratings yet

- Topic 4 - Completing The Accounting CycleDocument52 pagesTopic 4 - Completing The Accounting CycleLA Syamsul100% (1)

- Fundamentals of ABM1 - Q4 - LAS1 DRAFTDocument17 pagesFundamentals of ABM1 - Q4 - LAS1 DRAFTSitti Halima Amilbahar AdgesNo ratings yet

- Exam Revision - Chapter 3 4Document6 pagesExam Revision - Chapter 3 4Vũ Thị NgoanNo ratings yet

- Accounting: Adjusting EntriesDocument11 pagesAccounting: Adjusting EntriesCamellia100% (2)

- Sas Certified Accounting Technician Level 1 Module 2Document29 pagesSas Certified Accounting Technician Level 1 Module 2Plame GaseroNo ratings yet

- LECTURE 7 Accounting For Merchandising Activities Periodic and Perpetual BSAFDocument40 pagesLECTURE 7 Accounting For Merchandising Activities Periodic and Perpetual BSAFShahzad C7No ratings yet

- Lecture Slides - Chapter 3 4Document82 pagesLecture Slides - Chapter 3 4Bùi Phan Ý Nhi100% (1)

- Exam Revision - 3 & 4 SolDocument6 pagesExam Revision - 3 & 4 SolNguyễn Minh ĐứcNo ratings yet

- 2023 Acc Term3 Revision MEMO ENG - 30.08.2023Document12 pages2023 Acc Term3 Revision MEMO ENG - 30.08.2023sisikelelwen05No ratings yet

- Diy-Exercises (Questionnaires)Document31 pagesDiy-Exercises (Questionnaires)May RamosNo ratings yet

- FABM1 Q4 M1 Preparing-Adjusting-EntriesDocument14 pagesFABM1 Q4 M1 Preparing-Adjusting-EntriesXedric JuantaNo ratings yet

- B124 Book 3 CH 2+3+4 + Book 5 CH 1Document81 pagesB124 Book 3 CH 2+3+4 + Book 5 CH 1بث مباشر فورت نايت سيرفر خاصNo ratings yet

- Basic Accounting Practice - Adjusting Entries-3Document34 pagesBasic Accounting Practice - Adjusting Entries-3randel10caneteNo ratings yet

- Lesson 3b Adjusting The AccountsDocument3 pagesLesson 3b Adjusting The AccountsBenedict CladoNo ratings yet

- POA WK 7 LECT 2 VER 1 28032021 115402am 17112022 110442am 06052023 101809amDocument65 pagesPOA WK 7 LECT 2 VER 1 28032021 115402am 17112022 110442am 06052023 101809ammuhammad atifNo ratings yet

- Unit 5: Current Liabilities and ContingenciesDocument21 pagesUnit 5: Current Liabilities and Contingenciessamuel kebedeNo ratings yet

- Business Transactions and Their Analysis As Applied To The Accounting Cycle of A Service Business (Part Ii-A)Document9 pagesBusiness Transactions and Their Analysis As Applied To The Accounting Cycle of A Service Business (Part Ii-A)Tumamudtamud, JenaNo ratings yet

- FABM1 LAS 7 Adjusting-EntriesDocument12 pagesFABM1 LAS 7 Adjusting-EntriesVenus AriateNo ratings yet

- Accounting Concepts and PrinciplesDocument30 pagesAccounting Concepts and PrinciplesKristine Lei Del MundoNo ratings yet

- Handouts ACCOUNTING-2Document39 pagesHandouts ACCOUNTING-2Marc John IlanoNo ratings yet

- Unit - TWO EdtdDocument14 pagesUnit - TWO EdtdHaileNo ratings yet

- Unit 3Document23 pagesUnit 3Nigussie BerhanuNo ratings yet

- Chapter 4Document16 pagesChapter 4Jonh BekaNo ratings yet

- Acc 201 CH3Document7 pagesAcc 201 CH3Trickster TwelveNo ratings yet

- 1st Semester Dec 2021 PDFDocument8 pages1st Semester Dec 2021 PDFroshanNo ratings yet

- Adjusting EntriesDocument14 pagesAdjusting EntriesSeri CrisologoNo ratings yet

- Accounts Receivable Handout PDFDocument2 pagesAccounts Receivable Handout PDFChristine Joy Rapi MarsoNo ratings yet

- Fundamentals of Accountancy Business and Management 1 11 FourthDocument4 pagesFundamentals of Accountancy Business and Management 1 11 FourthPaulo Amposta CarpioNo ratings yet

- Accounting Chaprter 3Document49 pagesAccounting Chaprter 3rashmiaakshaNo ratings yet

- Module 2 Concept of IncomeDocument3 pagesModule 2 Concept of IncomeNormel DecalaoNo ratings yet

- Chapter 3 Current Liability PayrollDocument39 pagesChapter 3 Current Liability PayrollAbdi Mucee Tube100% (1)

- Exam Revision - Chapter 9 10Document7 pagesExam Revision - Chapter 9 10Vũ Thị NgoanNo ratings yet

- Chapter Two Current Liabilities and ContingenciesDocument10 pagesChapter Two Current Liabilities and ContingenciesBlack boxNo ratings yet

- Exam Revision - 9 & 10 SolDocument7 pagesExam Revision - 9 & 10 SolNguyễn Minh ĐứcNo ratings yet

- Adjusting The Book of AccountsDocument33 pagesAdjusting The Book of Accountsjoshua zabala100% (1)

- Intermediate Accounting 1 First Grading Examination: Name: Date: Professor: Section: ScoreDocument20 pagesIntermediate Accounting 1 First Grading Examination: Name: Date: Professor: Section: ScoreJulia Andrea Yting100% (3)

- Fabm1 PPT Q2W3Document43 pagesFabm1 PPT Q2W3giselle100% (2)

- Introduction To Accounting - Adjusting EntriesDocument39 pagesIntroduction To Accounting - Adjusting EntriesRon Hoover Mercene100% (1)

- Adjusting EntriesDocument18 pagesAdjusting EntriesAmie Jane MirandaNo ratings yet

- DMBA104Document8 pagesDMBA104chetan kansalNo ratings yet

- IntAcc-1 Accounting For ReceivablesDocument13 pagesIntAcc-1 Accounting For ReceivablesShekainah BNo ratings yet

- Financial Accounting Chapter 9: Accounts Receivable: Classification of ReceivablesDocument2 pagesFinancial Accounting Chapter 9: Accounts Receivable: Classification of ReceivablesMay Grethel Joy PeranteNo ratings yet

- Accounts Receivable: Total Trade Receivables Total Current ReceivablesDocument4 pagesAccounts Receivable: Total Trade Receivables Total Current ReceivablesSano ManjiroNo ratings yet

- Chap12 Insurance ContractDocument2 pagesChap12 Insurance ContractwingNo ratings yet

- AP InventoriesDocument7 pagesAP InventorieswingNo ratings yet

- Book Value Per Share (Problems)Document3 pagesBook Value Per Share (Problems)wingNo ratings yet

- AUDIT OF SHAREHOLDERS (Probs)Document4 pagesAUDIT OF SHAREHOLDERS (Probs)wingNo ratings yet

- KLBF 30 Sept 2022Document147 pagesKLBF 30 Sept 2022asdasNo ratings yet

- Strategic Analysis - Harley DavidsonDocument12 pagesStrategic Analysis - Harley DavidsonSimran PoptaniNo ratings yet

- Risk RegisterDocument5 pagesRisk Registerfavour Golden Entertainment starkidNo ratings yet

- New Arambagh Trading - PCG1408Document1 pageNew Arambagh Trading - PCG1408AvijitSinharoyNo ratings yet

- Project Report - Capital MarketDocument33 pagesProject Report - Capital MarketPragati DixitNo ratings yet

- Export Import Procedures and DocumentationDocument11 pagesExport Import Procedures and DocumentationTeena RawatNo ratings yet

- Vol 141Document104 pagesVol 141Rendi100% (1)

- Foreign Exchange Rates (3070)Document10 pagesForeign Exchange Rates (3070)Ahmad vlogsNo ratings yet

- Cma Cia 3Document12 pagesCma Cia 3DIVYANG AGARWAL 2023291No ratings yet

- OFFER LETTER - Aman YadavDocument3 pagesOFFER LETTER - Aman YadavAman YadavNo ratings yet

- Strategy For Sustainable ConstructionDocument64 pagesStrategy For Sustainable ConstructionDanang Desfri AbdilahNo ratings yet

- Description: S&P/Asx All Technology IndexDocument6 pagesDescription: S&P/Asx All Technology IndexSuhasNo ratings yet

- Affidavit of Consolidation..Document2 pagesAffidavit of Consolidation..Sa LeeNo ratings yet

- Module 3 Market Sizing IntermediateDocument14 pagesModule 3 Market Sizing IntermediateBas KelderNo ratings yet

- IMPACT OF REPROGRAPHIC MACHINE STUDENT 039 CorrDocument55 pagesIMPACT OF REPROGRAPHIC MACHINE STUDENT 039 CorrIfeji u. johnNo ratings yet

- FORMAT-Revised IAR - QualifiedDocument2 pagesFORMAT-Revised IAR - QualifiedGier Rizaldo BulaclacNo ratings yet

- Inventory ModelsDocument30 pagesInventory ModelsAmarendra Sharma ChennapragadaNo ratings yet

- Competition Law - PALS Lecture PDFDocument37 pagesCompetition Law - PALS Lecture PDFMaying Dadula RaymundoNo ratings yet

- Affect of Green Marketing On ConsumersDocument17 pagesAffect of Green Marketing On Consumersjuan felipe betancourt lopezNo ratings yet

- Differentiate Fiscal and Calendar Year: 2. Define Adjusting EntriesDocument9 pagesDifferentiate Fiscal and Calendar Year: 2. Define Adjusting EntriesGmef Syme FerreraNo ratings yet

- MUKANDDocument2 pagesMUKANDmakrand87No ratings yet

- Chapter 5: Accounting For Merchandising Operations: Question 1 A, B & CDocument3 pagesChapter 5: Accounting For Merchandising Operations: Question 1 A, B & CTyra CoyNo ratings yet

- Principles of Accounts For CSEC®: 2nd EditionDocument20 pagesPrinciples of Accounts For CSEC®: 2nd EditionVeronica BaileyNo ratings yet

- LH 9 - Final Accounts ProblemsDocument29 pagesLH 9 - Final Accounts ProblemsHarshavardhanNo ratings yet

- OjiFS SR 2019 Print VersionDocument50 pagesOjiFS SR 2019 Print VersionVirginia MainardiNo ratings yet

- Economics For Today 5th Edition Layton Solutions ManualDocument10 pagesEconomics For Today 5th Edition Layton Solutions Manualcassandracruzpkteqnymcf100% (39)

- Supply Chain Performance: Achieving Strategic Fit and ScopeDocument24 pagesSupply Chain Performance: Achieving Strategic Fit and ScopeRahul VermaNo ratings yet

- NM1607R - S2 2022 (For S1 2022 Students) RESIT EXAM Question PAPERDocument9 pagesNM1607R - S2 2022 (For S1 2022 Students) RESIT EXAM Question PAPERrecovaNo ratings yet

- Analisis Pengendalian Kualitas Proses Pengelasan (Welding) Dengan Pendekatan Six Sigma Pada Proyek Pt. XyzDocument13 pagesAnalisis Pengendalian Kualitas Proses Pengelasan (Welding) Dengan Pendekatan Six Sigma Pada Proyek Pt. Xyzaprillia rizkyNo ratings yet