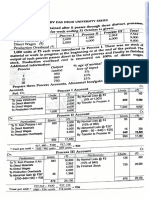

Cost Sheet

Cost Sheet

You might also like

- India's Top 1000 MFDsDocument40 pagesIndia's Top 1000 MFDsShyama Vallabha Dasa100% (1)

- Danone CaseDocument4 pagesDanone CaseThomas AtkinsNo ratings yet

- American Society of Mechanical Engineers-The Guide To Hydropower Mechanical Design-H C I Pubns (1996) PDFDocument384 pagesAmerican Society of Mechanical Engineers-The Guide To Hydropower Mechanical Design-H C I Pubns (1996) PDFUmesh Shrestha100% (3)

- The World of Mordillo 1 PDFDocument51 pagesThe World of Mordillo 1 PDFdvvtkd2007100% (1)

- Bagi Monitoring SparepartDocument6 pagesBagi Monitoring Sparepartwahyoe noegrohoNo ratings yet

- Dakshpatel CABDocument18 pagesDakshpatel CAB04 Daksh patelNo ratings yet

- Aos-Mod 1Document20 pagesAos-Mod 1Cz NiyasNo ratings yet

- Belasen, A. Corporate Communication. Cap. (6-7)Document15 pagesBelasen, A. Corporate Communication. Cap. (6-7)juanNo ratings yet

- Adobe Scan 16 Nov 2023Document1 pageAdobe Scan 16 Nov 2023gs hondaNo ratings yet

- CRM Chapter 3Document20 pagesCRM Chapter 3fafese7300No ratings yet

- Soal RMK Mankeu CH 21Document1 pageSoal RMK Mankeu CH 21Bilqist ZahraNo ratings yet

- Industrial Discipline and Grievance HandlingDocument22 pagesIndustrial Discipline and Grievance HandlingHarnitNo ratings yet

- Tusuwiin NegtgelDocument507 pagesTusuwiin NegtgelLeo Rich MongoliaNo ratings yet

- Scan 28 Jul. 2019Document1 pageScan 28 Jul. 2019Yanina VillalbaNo ratings yet

- Labour CostDocument26 pagesLabour CostShivangi JhawarNo ratings yet

- A World History of Architecture - Ch12 PDFDocument40 pagesA World History of Architecture - Ch12 PDFxstina100% (1)

- Es 4Document25 pagesEs 4Anil KumarNo ratings yet

- Emm Assessment-1Document6 pagesEmm Assessment-1AGASTHEESWAR BOMMARAJNo ratings yet

- Environmentalists of SignificanceDocument6 pagesEnvironmentalists of SignificanceChaitanya KhedekarNo ratings yet

- Hall Effect TheoryDocument6 pagesHall Effect TheorySekh AsifNo ratings yet

- CHEM KINETICS - ORDER N MOLECULARITY - 10 MayDocument8 pagesCHEM KINETICS - ORDER N MOLECULARITY - 10 Maysuri rayNo ratings yet

- Adobe Scan 01-Apr-2023Document2 pagesAdobe Scan 01-Apr-2023jsr vaastuNo ratings yet

- 26 de NotedDocument13 pages26 de NotedKaranNo ratings yet

- 26 de Noted PDFDocument13 pages26 de Noted PDFKaranNo ratings yet

- ClassificationDocument1 pageClassification973132No ratings yet

- Unit 2 Operating SystemDocument21 pagesUnit 2 Operating SystemSachin BhandariNo ratings yet

- صفاء سعدDocument3 pagesصفاء سعدahmed desokyNo ratings yet

- Case Studies ApproachDocument24 pagesCase Studies Approachmrarbazansari423No ratings yet

- Certificates CoursesDocument2 pagesCertificates CoursesNilesh SutradharNo ratings yet

- iJJLN-2.3: I.ope1Document2 pagesiJJLN-2.3: I.ope1Japheth CuaNo ratings yet

- Acc PG 64 PDFDocument1 pageAcc PG 64 PDFSatyaprasad KNo ratings yet

- I - F.,cii - LFZ ) :: Certificado de Inexistencia de Restos ArqueologicosDocument5 pagesI - F.,cii - LFZ ) :: Certificado de Inexistencia de Restos ArqueologicosJuan Bautista Rojas VillegasNo ratings yet

- Scan Nov 20, 2018Document8 pagesScan Nov 20, 2018Michael GrabdaNo ratings yet

- Twin Rotary PressesDocument24 pagesTwin Rotary PressesKyle McdonaldNo ratings yet

- Draft Exhibits Part14Document100 pagesDraft Exhibits Part14bhavikdas10No ratings yet

- (SMS) Sunstar Scanner CSE-IsE - System Modelling and SimulationDocument25 pages(SMS) Sunstar Scanner CSE-IsE - System Modelling and SimulationSahanaNo ratings yet

- Rent AgreementDocument3 pagesRent AgreementKaran PeshwaniNo ratings yet

- Adobe Scan Apr 08, 2024Document2 pagesAdobe Scan Apr 08, 2024mahimabajpai74No ratings yet

- CVE541 Stress Distribution in SoilDocument16 pagesCVE541 Stress Distribution in SoilRichards Ðånte WisdomNo ratings yet

- Automatic WaterpassDocument12 pagesAutomatic WaterpassFarell TanNo ratings yet

- FILE - 20221107 - 194543 - Chuong 1 - 2 KTVM2Document25 pagesFILE - 20221107 - 194543 - Chuong 1 - 2 KTVM2Phuong Anh TranNo ratings yet

- JBL Pulse 1 ManualDocument8 pagesJBL Pulse 1 Manualjev_ssNo ratings yet

- BoardConstitution NewDocument49 pagesBoardConstitution Newpmaljat26No ratings yet

- Story Telling Sma Khadijah Jatim Bimo AnggowoajiDocument1 pageStory Telling Sma Khadijah Jatim Bimo Anggowoajikurikulum smkn1mojokertoNo ratings yet

- Adobe Scan 07 Ago. 2020 PDFDocument5 pagesAdobe Scan 07 Ago. 2020 PDFDavid GarciaNo ratings yet

- Unit 2Document5 pagesUnit 2yugendran kumarNo ratings yet

- Chapter 3 IEDDocument8 pagesChapter 3 IEDpachaurimahakNo ratings yet

- Una Año de Amor - Luz CasalDocument1 pageUna Año de Amor - Luz CasalRodo chileNo ratings yet

- CD Unit-1Document20 pagesCD Unit-1jonej27163No ratings yet

- Lto MC-2020-2230 PmvicDocument3 pagesLto MC-2020-2230 PmvicAlcris BoquiaNo ratings yet

- Genital Sys. MCQDocument7 pagesGenital Sys. MCQOpen UserNo ratings yet

- UntitledDocument2 pagesUntitledANTHONY SCOTT BARRENECHEA RODRIGUEZNo ratings yet

- 872-08 09 15-លក្ខន្តិកៈគតិយុត្តនៃគ្រឹះស្ថានសាធារណៈរដ្ឋបាលDocument15 pages872-08 09 15-លក្ខន្តិកៈគតិយុត្តនៃគ្រឹះស្ថានសាធារណៈរដ្ឋបាលnyka495No ratings yet

- MEAssignment 4Document7 pagesMEAssignment 4VAKUL SINGHNo ratings yet

- 10 THDocument1 page10 THPragathi.NNo ratings yet

- Richards Jack C Bohlke David Speak Now 2 Student S BookDocument131 pagesRichards Jack C Bohlke David Speak Now 2 Student S BookFiorina Jaso50% (2)

- Adobe Scan 23 Dec 2021Document1 pageAdobe Scan 23 Dec 2021AFRAHNo ratings yet

- Xii Maths Activity 2.Document4 pagesXii Maths Activity 2.GangeshNo ratings yet

- B.SC (H) V Quantum Mechanics and Its Applications I-6216Document6 pagesB.SC (H) V Quantum Mechanics and Its Applications I-6216Pooja SharmaNo ratings yet

- Wps 865 Saw 001Document8 pagesWps 865 Saw 001PRAVEENNo ratings yet

- The Maddest Idea: An Isaac Biddlecomb NovelFrom EverandThe Maddest Idea: An Isaac Biddlecomb NovelRating: 3.5 out of 5 stars3.5/5 (9)

- Adobe Scan 14 May 2022Document5 pagesAdobe Scan 14 May 2022Mary CharlesNo ratings yet

- Adobe Scan 18 May 2022Document6 pagesAdobe Scan 18 May 2022Mary CharlesNo ratings yet

- Data Collection MethodDocument5 pagesData Collection MethodMary CharlesNo ratings yet

- Adobe Scan 19 May 2022Document10 pagesAdobe Scan 19 May 2022Mary CharlesNo ratings yet

- Adobe Scan 14 May 2022Document2 pagesAdobe Scan 14 May 2022Mary CharlesNo ratings yet

- Adobe Scan 18 May 2022Document11 pagesAdobe Scan 18 May 2022Mary CharlesNo ratings yet

- Adobe Scan 18 May 2022Document6 pagesAdobe Scan 18 May 2022Mary CharlesNo ratings yet

- OperatingDocument5 pagesOperatingMary CharlesNo ratings yet

- Adobe Scan 18 May 2022Document1 pageAdobe Scan 18 May 2022Mary CharlesNo ratings yet

- GE IE2 PriorityDocument1 pageGE IE2 PriorityMary CharlesNo ratings yet

- IIMs and Their ProgramsDocument3 pagesIIMs and Their ProgramsMary CharlesNo ratings yet

- Organic + Inorganic Home Apparel KeywordsDocument7 pagesOrganic + Inorganic Home Apparel KeywordsMary CharlesNo ratings yet

- IkeaDocument17 pagesIkeaMary CharlesNo ratings yet

- 10 Year Cyber Law Part-4Document5 pages10 Year Cyber Law Part-4Mary CharlesNo ratings yet

- Organic Apparel Keywords (AHREFS)Document6 pagesOrganic Apparel Keywords (AHREFS)Mary CharlesNo ratings yet

- RC 16 Apr 2022Document7 pagesRC 16 Apr 2022Mary CharlesNo ratings yet

- Pillow CoversDocument2 pagesPillow CoversMary CharlesNo ratings yet

- ReconcellationDocument8 pagesReconcellationMary CharlesNo ratings yet

- 10 Year-1Document25 pages10 Year-1Mary CharlesNo ratings yet

- 10 Year Cyber Law Part-3Document8 pages10 Year Cyber Law Part-3Mary CharlesNo ratings yet

- Topics For Long Writing SkillsDocument2 pagesTopics For Long Writing SkillsMary CharlesNo ratings yet

- VARC 04 May 2022Document9 pagesVARC 04 May 2022Mary CharlesNo ratings yet

- VARC 08 Apr 2022Document11 pagesVARC 08 Apr 2022Mary CharlesNo ratings yet

- XAT VALR and DM Pratice 31122022 With AnswersDocument23 pagesXAT VALR and DM Pratice 31122022 With AnswersMary CharlesNo ratings yet

- CostDocument3 pagesCostMary CharlesNo ratings yet

- VARC 18 Apr 2022Document14 pagesVARC 18 Apr 2022Mary CharlesNo ratings yet

- Cat Quant Area Wise SplitDocument1 pageCat Quant Area Wise SplitMary CharlesNo ratings yet

- 4 5922368006893079595Document363 pages4 5922368006893079595Mary CharlesNo ratings yet

- VARC Practice 16 Mar 2022Document13 pagesVARC Practice 16 Mar 2022Mary CharlesNo ratings yet

- 16th AprilDocument315 pages16th AprilMary CharlesNo ratings yet

- Far Ring TonDocument40 pagesFar Ring TonShane-Charles WenzelNo ratings yet

- T4 - Past Paper CombinedDocument53 pagesT4 - Past Paper CombinedU Abdul Rehman100% (1)

- HRTM 134 Course Outline, 2nd 2017-18Document4 pagesHRTM 134 Course Outline, 2nd 2017-18aireen cloresNo ratings yet

- Thank You For Your Order: Power & Signal Group PO BOX 856842 MINNEAPOLIS, MN 55485-6842Document1 pageThank You For Your Order: Power & Signal Group PO BOX 856842 MINNEAPOLIS, MN 55485-6842RuodNo ratings yet

- SMERADocument17 pagesSMERAChander ChellaniNo ratings yet

- RC 1Document12 pagesRC 1Chinmoy DasNo ratings yet

- PK - 9Document26 pagesPK - 9Rennya Lily KharismaNo ratings yet

- Back To Back Vs TransfersDocument4 pagesBack To Back Vs Transfersvkrm14No ratings yet

- At Io N at Et: The Polytechnic Ibadan IRSDocument1 pageAt Io N at Et: The Polytechnic Ibadan IRSadegbola hamzatNo ratings yet

- Session On ETL TALEND V2Document25 pagesSession On ETL TALEND V2Vijaya Krishna Bharata100% (1)

- Math 004 Worktex TcompleteDocument97 pagesMath 004 Worktex TcompleteJ-b Rivera67% (3)

- Banking IMCDocument7 pagesBanking IMCVishu ShahNo ratings yet

- Elena Pavel - CV Eng-6 PDFDocument2 pagesElena Pavel - CV Eng-6 PDFelena dragutzaNo ratings yet

- MP 402Document223 pagesMP 402Akanksha MalhotraNo ratings yet

- 2011-2012 Ivy Sports Symposium Media KitDocument13 pages2011-2012 Ivy Sports Symposium Media KitSports Symposium Inc.No ratings yet

- Business Plan SampleDocument28 pagesBusiness Plan SampleBeverly Ann Perez CuetoNo ratings yet

- Spinoff Splitoff Splitup CarveoutDocument2 pagesSpinoff Splitoff Splitup CarveouttransitxyzNo ratings yet

- Sir David TweedieDocument4 pagesSir David TweedieSaranpal SinghNo ratings yet

- Forensic Accounting in IndiaDocument9 pagesForensic Accounting in IndiaBhavesh Rathod0% (1)

- Asset and Liability Management: A Multiple Case Study in Brazilian Financial InstitutionsDocument13 pagesAsset and Liability Management: A Multiple Case Study in Brazilian Financial InstitutionsJohn MichaelNo ratings yet

- Oracle® Functional Testing PDFDocument260 pagesOracle® Functional Testing PDFupenderNo ratings yet

- Ppha NatconDocument1 pagePpha NatconKenny James MerinNo ratings yet

- Titan Company (TITIND) : Multiple Levers in Place To Drive Sales GrowthDocument5 pagesTitan Company (TITIND) : Multiple Levers in Place To Drive Sales Growthaachen_24No ratings yet

- Presentation Anil May-10Document215 pagesPresentation Anil May-10devgankaranNo ratings yet

- Hamza Akbar: 0308-8616996 House No#531A-5 O/S Dehli Gate MultanDocument3 pagesHamza Akbar: 0308-8616996 House No#531A-5 O/S Dehli Gate MultanTalalNo ratings yet

- PIYUSH HSE Engineer UpdatedDocument4 pagesPIYUSH HSE Engineer UpdatedPIYUSHBORKAR1988No ratings yet

- Thursday, September 13, 2012: Pune To Nashik Neeta Tours and TravelsDocument1 pageThursday, September 13, 2012: Pune To Nashik Neeta Tours and TravelsVaibhav ZawarNo ratings yet

- Versita Open Access LicenseDocument2 pagesVersita Open Access LicenseMohamed YousufNo ratings yet

Download as pdf or txt

You might also like

- India's Top 1000 MFDsDocument40 pagesIndia's Top 1000 MFDsShyama Vallabha Dasa100% (1)

- Danone CaseDocument4 pagesDanone CaseThomas AtkinsNo ratings yet

- American Society of Mechanical Engineers-The Guide To Hydropower Mechanical Design-H C I Pubns (1996) PDFDocument384 pagesAmerican Society of Mechanical Engineers-The Guide To Hydropower Mechanical Design-H C I Pubns (1996) PDFUmesh Shrestha100% (3)

- The World of Mordillo 1 PDFDocument51 pagesThe World of Mordillo 1 PDFdvvtkd2007100% (1)

- Bagi Monitoring SparepartDocument6 pagesBagi Monitoring Sparepartwahyoe noegrohoNo ratings yet

- Dakshpatel CABDocument18 pagesDakshpatel CAB04 Daksh patelNo ratings yet

- Aos-Mod 1Document20 pagesAos-Mod 1Cz NiyasNo ratings yet

- Belasen, A. Corporate Communication. Cap. (6-7)Document15 pagesBelasen, A. Corporate Communication. Cap. (6-7)juanNo ratings yet

- Adobe Scan 16 Nov 2023Document1 pageAdobe Scan 16 Nov 2023gs hondaNo ratings yet

- CRM Chapter 3Document20 pagesCRM Chapter 3fafese7300No ratings yet

- Soal RMK Mankeu CH 21Document1 pageSoal RMK Mankeu CH 21Bilqist ZahraNo ratings yet

- Industrial Discipline and Grievance HandlingDocument22 pagesIndustrial Discipline and Grievance HandlingHarnitNo ratings yet

- Tusuwiin NegtgelDocument507 pagesTusuwiin NegtgelLeo Rich MongoliaNo ratings yet

- Scan 28 Jul. 2019Document1 pageScan 28 Jul. 2019Yanina VillalbaNo ratings yet

- Labour CostDocument26 pagesLabour CostShivangi JhawarNo ratings yet

- A World History of Architecture - Ch12 PDFDocument40 pagesA World History of Architecture - Ch12 PDFxstina100% (1)

- Es 4Document25 pagesEs 4Anil KumarNo ratings yet

- Emm Assessment-1Document6 pagesEmm Assessment-1AGASTHEESWAR BOMMARAJNo ratings yet

- Environmentalists of SignificanceDocument6 pagesEnvironmentalists of SignificanceChaitanya KhedekarNo ratings yet

- Hall Effect TheoryDocument6 pagesHall Effect TheorySekh AsifNo ratings yet

- CHEM KINETICS - ORDER N MOLECULARITY - 10 MayDocument8 pagesCHEM KINETICS - ORDER N MOLECULARITY - 10 Maysuri rayNo ratings yet

- Adobe Scan 01-Apr-2023Document2 pagesAdobe Scan 01-Apr-2023jsr vaastuNo ratings yet

- 26 de NotedDocument13 pages26 de NotedKaranNo ratings yet

- 26 de Noted PDFDocument13 pages26 de Noted PDFKaranNo ratings yet

- ClassificationDocument1 pageClassification973132No ratings yet

- Unit 2 Operating SystemDocument21 pagesUnit 2 Operating SystemSachin BhandariNo ratings yet

- صفاء سعدDocument3 pagesصفاء سعدahmed desokyNo ratings yet

- Case Studies ApproachDocument24 pagesCase Studies Approachmrarbazansari423No ratings yet

- Certificates CoursesDocument2 pagesCertificates CoursesNilesh SutradharNo ratings yet

- iJJLN-2.3: I.ope1Document2 pagesiJJLN-2.3: I.ope1Japheth CuaNo ratings yet

- Acc PG 64 PDFDocument1 pageAcc PG 64 PDFSatyaprasad KNo ratings yet

- I - F.,cii - LFZ ) :: Certificado de Inexistencia de Restos ArqueologicosDocument5 pagesI - F.,cii - LFZ ) :: Certificado de Inexistencia de Restos ArqueologicosJuan Bautista Rojas VillegasNo ratings yet

- Scan Nov 20, 2018Document8 pagesScan Nov 20, 2018Michael GrabdaNo ratings yet

- Twin Rotary PressesDocument24 pagesTwin Rotary PressesKyle McdonaldNo ratings yet

- Draft Exhibits Part14Document100 pagesDraft Exhibits Part14bhavikdas10No ratings yet

- (SMS) Sunstar Scanner CSE-IsE - System Modelling and SimulationDocument25 pages(SMS) Sunstar Scanner CSE-IsE - System Modelling and SimulationSahanaNo ratings yet

- Rent AgreementDocument3 pagesRent AgreementKaran PeshwaniNo ratings yet

- Adobe Scan Apr 08, 2024Document2 pagesAdobe Scan Apr 08, 2024mahimabajpai74No ratings yet

- CVE541 Stress Distribution in SoilDocument16 pagesCVE541 Stress Distribution in SoilRichards Ðånte WisdomNo ratings yet

- Automatic WaterpassDocument12 pagesAutomatic WaterpassFarell TanNo ratings yet

- FILE - 20221107 - 194543 - Chuong 1 - 2 KTVM2Document25 pagesFILE - 20221107 - 194543 - Chuong 1 - 2 KTVM2Phuong Anh TranNo ratings yet

- JBL Pulse 1 ManualDocument8 pagesJBL Pulse 1 Manualjev_ssNo ratings yet

- BoardConstitution NewDocument49 pagesBoardConstitution Newpmaljat26No ratings yet

- Story Telling Sma Khadijah Jatim Bimo AnggowoajiDocument1 pageStory Telling Sma Khadijah Jatim Bimo Anggowoajikurikulum smkn1mojokertoNo ratings yet

- Adobe Scan 07 Ago. 2020 PDFDocument5 pagesAdobe Scan 07 Ago. 2020 PDFDavid GarciaNo ratings yet

- Unit 2Document5 pagesUnit 2yugendran kumarNo ratings yet

- Chapter 3 IEDDocument8 pagesChapter 3 IEDpachaurimahakNo ratings yet

- Una Año de Amor - Luz CasalDocument1 pageUna Año de Amor - Luz CasalRodo chileNo ratings yet

- CD Unit-1Document20 pagesCD Unit-1jonej27163No ratings yet

- Lto MC-2020-2230 PmvicDocument3 pagesLto MC-2020-2230 PmvicAlcris BoquiaNo ratings yet

- Genital Sys. MCQDocument7 pagesGenital Sys. MCQOpen UserNo ratings yet

- UntitledDocument2 pagesUntitledANTHONY SCOTT BARRENECHEA RODRIGUEZNo ratings yet

- 872-08 09 15-លក្ខន្តិកៈគតិយុត្តនៃគ្រឹះស្ថានសាធារណៈរដ្ឋបាលDocument15 pages872-08 09 15-លក្ខន្តិកៈគតិយុត្តនៃគ្រឹះស្ថានសាធារណៈរដ្ឋបាលnyka495No ratings yet

- MEAssignment 4Document7 pagesMEAssignment 4VAKUL SINGHNo ratings yet

- 10 THDocument1 page10 THPragathi.NNo ratings yet

- Richards Jack C Bohlke David Speak Now 2 Student S BookDocument131 pagesRichards Jack C Bohlke David Speak Now 2 Student S BookFiorina Jaso50% (2)

- Adobe Scan 23 Dec 2021Document1 pageAdobe Scan 23 Dec 2021AFRAHNo ratings yet

- Xii Maths Activity 2.Document4 pagesXii Maths Activity 2.GangeshNo ratings yet

- B.SC (H) V Quantum Mechanics and Its Applications I-6216Document6 pagesB.SC (H) V Quantum Mechanics and Its Applications I-6216Pooja SharmaNo ratings yet

- Wps 865 Saw 001Document8 pagesWps 865 Saw 001PRAVEENNo ratings yet

- The Maddest Idea: An Isaac Biddlecomb NovelFrom EverandThe Maddest Idea: An Isaac Biddlecomb NovelRating: 3.5 out of 5 stars3.5/5 (9)

- Adobe Scan 14 May 2022Document5 pagesAdobe Scan 14 May 2022Mary CharlesNo ratings yet

- Adobe Scan 18 May 2022Document6 pagesAdobe Scan 18 May 2022Mary CharlesNo ratings yet

- Data Collection MethodDocument5 pagesData Collection MethodMary CharlesNo ratings yet

- Adobe Scan 19 May 2022Document10 pagesAdobe Scan 19 May 2022Mary CharlesNo ratings yet

- Adobe Scan 14 May 2022Document2 pagesAdobe Scan 14 May 2022Mary CharlesNo ratings yet

- Adobe Scan 18 May 2022Document11 pagesAdobe Scan 18 May 2022Mary CharlesNo ratings yet

- Adobe Scan 18 May 2022Document6 pagesAdobe Scan 18 May 2022Mary CharlesNo ratings yet

- OperatingDocument5 pagesOperatingMary CharlesNo ratings yet

- Adobe Scan 18 May 2022Document1 pageAdobe Scan 18 May 2022Mary CharlesNo ratings yet

- GE IE2 PriorityDocument1 pageGE IE2 PriorityMary CharlesNo ratings yet

- IIMs and Their ProgramsDocument3 pagesIIMs and Their ProgramsMary CharlesNo ratings yet

- Organic + Inorganic Home Apparel KeywordsDocument7 pagesOrganic + Inorganic Home Apparel KeywordsMary CharlesNo ratings yet

- IkeaDocument17 pagesIkeaMary CharlesNo ratings yet

- 10 Year Cyber Law Part-4Document5 pages10 Year Cyber Law Part-4Mary CharlesNo ratings yet

- Organic Apparel Keywords (AHREFS)Document6 pagesOrganic Apparel Keywords (AHREFS)Mary CharlesNo ratings yet

- RC 16 Apr 2022Document7 pagesRC 16 Apr 2022Mary CharlesNo ratings yet

- Pillow CoversDocument2 pagesPillow CoversMary CharlesNo ratings yet

- ReconcellationDocument8 pagesReconcellationMary CharlesNo ratings yet

- 10 Year-1Document25 pages10 Year-1Mary CharlesNo ratings yet

- 10 Year Cyber Law Part-3Document8 pages10 Year Cyber Law Part-3Mary CharlesNo ratings yet

- Topics For Long Writing SkillsDocument2 pagesTopics For Long Writing SkillsMary CharlesNo ratings yet

- VARC 04 May 2022Document9 pagesVARC 04 May 2022Mary CharlesNo ratings yet

- VARC 08 Apr 2022Document11 pagesVARC 08 Apr 2022Mary CharlesNo ratings yet

- XAT VALR and DM Pratice 31122022 With AnswersDocument23 pagesXAT VALR and DM Pratice 31122022 With AnswersMary CharlesNo ratings yet

- CostDocument3 pagesCostMary CharlesNo ratings yet

- VARC 18 Apr 2022Document14 pagesVARC 18 Apr 2022Mary CharlesNo ratings yet

- Cat Quant Area Wise SplitDocument1 pageCat Quant Area Wise SplitMary CharlesNo ratings yet

- 4 5922368006893079595Document363 pages4 5922368006893079595Mary CharlesNo ratings yet

- VARC Practice 16 Mar 2022Document13 pagesVARC Practice 16 Mar 2022Mary CharlesNo ratings yet

- 16th AprilDocument315 pages16th AprilMary CharlesNo ratings yet

- Far Ring TonDocument40 pagesFar Ring TonShane-Charles WenzelNo ratings yet

- T4 - Past Paper CombinedDocument53 pagesT4 - Past Paper CombinedU Abdul Rehman100% (1)

- HRTM 134 Course Outline, 2nd 2017-18Document4 pagesHRTM 134 Course Outline, 2nd 2017-18aireen cloresNo ratings yet

- Thank You For Your Order: Power & Signal Group PO BOX 856842 MINNEAPOLIS, MN 55485-6842Document1 pageThank You For Your Order: Power & Signal Group PO BOX 856842 MINNEAPOLIS, MN 55485-6842RuodNo ratings yet

- SMERADocument17 pagesSMERAChander ChellaniNo ratings yet

- RC 1Document12 pagesRC 1Chinmoy DasNo ratings yet

- PK - 9Document26 pagesPK - 9Rennya Lily KharismaNo ratings yet

- Back To Back Vs TransfersDocument4 pagesBack To Back Vs Transfersvkrm14No ratings yet

- At Io N at Et: The Polytechnic Ibadan IRSDocument1 pageAt Io N at Et: The Polytechnic Ibadan IRSadegbola hamzatNo ratings yet

- Session On ETL TALEND V2Document25 pagesSession On ETL TALEND V2Vijaya Krishna Bharata100% (1)

- Math 004 Worktex TcompleteDocument97 pagesMath 004 Worktex TcompleteJ-b Rivera67% (3)

- Banking IMCDocument7 pagesBanking IMCVishu ShahNo ratings yet

- Elena Pavel - CV Eng-6 PDFDocument2 pagesElena Pavel - CV Eng-6 PDFelena dragutzaNo ratings yet

- MP 402Document223 pagesMP 402Akanksha MalhotraNo ratings yet

- 2011-2012 Ivy Sports Symposium Media KitDocument13 pages2011-2012 Ivy Sports Symposium Media KitSports Symposium Inc.No ratings yet

- Business Plan SampleDocument28 pagesBusiness Plan SampleBeverly Ann Perez CuetoNo ratings yet

- Spinoff Splitoff Splitup CarveoutDocument2 pagesSpinoff Splitoff Splitup CarveouttransitxyzNo ratings yet

- Sir David TweedieDocument4 pagesSir David TweedieSaranpal SinghNo ratings yet

- Forensic Accounting in IndiaDocument9 pagesForensic Accounting in IndiaBhavesh Rathod0% (1)

- Asset and Liability Management: A Multiple Case Study in Brazilian Financial InstitutionsDocument13 pagesAsset and Liability Management: A Multiple Case Study in Brazilian Financial InstitutionsJohn MichaelNo ratings yet

- Oracle® Functional Testing PDFDocument260 pagesOracle® Functional Testing PDFupenderNo ratings yet

- Ppha NatconDocument1 pagePpha NatconKenny James MerinNo ratings yet

- Titan Company (TITIND) : Multiple Levers in Place To Drive Sales GrowthDocument5 pagesTitan Company (TITIND) : Multiple Levers in Place To Drive Sales Growthaachen_24No ratings yet

- Presentation Anil May-10Document215 pagesPresentation Anil May-10devgankaranNo ratings yet

- Hamza Akbar: 0308-8616996 House No#531A-5 O/S Dehli Gate MultanDocument3 pagesHamza Akbar: 0308-8616996 House No#531A-5 O/S Dehli Gate MultanTalalNo ratings yet

- PIYUSH HSE Engineer UpdatedDocument4 pagesPIYUSH HSE Engineer UpdatedPIYUSHBORKAR1988No ratings yet

- Thursday, September 13, 2012: Pune To Nashik Neeta Tours and TravelsDocument1 pageThursday, September 13, 2012: Pune To Nashik Neeta Tours and TravelsVaibhav ZawarNo ratings yet

- Versita Open Access LicenseDocument2 pagesVersita Open Access LicenseMohamed YousufNo ratings yet