Download as pdf or txt

You might also like

- Hotel InvoiceDocument1 pageHotel InvoiceJonas O100% (2)

- Inv 6818Document1 pageInv 6818AISHANI DASNo ratings yet

- KOTYARK UpdateDocument3 pagesKOTYARK UpdateLive TVNo ratings yet

- ELP Indirect Tax Newsletter November 2022Document6 pagesELP Indirect Tax Newsletter November 2022ELP LawNo ratings yet

- Old PO-80211001100555Document3 pagesOld PO-80211001100555ManojNo ratings yet

- A Govt CompanyDocument6 pagesA Govt Companyabhiramreddy3No ratings yet

- Hyderabad 22122022Document1 pageHyderabad 22122022Yakshit JainNo ratings yet

- KOTYARK OrdersDocument2 pagesKOTYARK OrdersHow ToNo ratings yet

- August 2022 NewsLetterDocument34 pagesAugust 2022 NewsLetterSabrina CanoNo ratings yet

- Inv 082306Document1 pageInv 082306suraj.kumarNo ratings yet

- Augusthyd 15092022Document1 pageAugusthyd 15092022Yakshit JainNo ratings yet

- Google Drive Renewal Payment ReceiptDocument2 pagesGoogle Drive Renewal Payment Receiptchouhangovind302No ratings yet

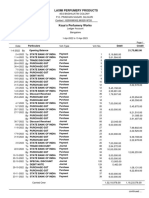

- Koyas PerfumeryDocument2 pagesKoyas PerfumeryTANUJ CHAKRABORTYNo ratings yet

- Chapter V: Assessments Relating To Agricultural Income: Report No. 9 of 2019 (Direct Taxes)Document26 pagesChapter V: Assessments Relating To Agricultural Income: Report No. 9 of 2019 (Direct Taxes)koshee namdevNo ratings yet

- Hyder 181122Document1 pageHyder 181122Yakshit JainNo ratings yet

- 2022 RECALIBRATED ANNUAL PLAN Revised RoseDocument5 pages2022 RECALIBRATED ANNUAL PLAN Revised RoseMaria CarmelaNo ratings yet

- Airtel 974Document1 pageAirtel 974OL RentNo ratings yet

- May 22Document3 pagesMay 22honey moneyNo ratings yet

- Independence Day Edition: Adv. (CA) Ranjan MehtaDocument10 pagesIndependence Day Edition: Adv. (CA) Ranjan MehtaCA Ranjan MehtaNo ratings yet

- Government Approval FinalDocument8 pagesGovernment Approval FinalfearlessronakNo ratings yet

- Aino Communique 110th Dec EditionDocument12 pagesAino Communique 110th Dec EditionSwathi JainNo ratings yet

- Tax Invoice: CIN:U72900DL2020PTC361314 GSTIN: 07AAFCE8193A1ZPDocument1 pageTax Invoice: CIN:U72900DL2020PTC361314 GSTIN: 07AAFCE8193A1ZPAbhijit SarkarNo ratings yet

- GST Recap 01.04.23 TO 07.04.23Document2 pagesGST Recap 01.04.23 TO 07.04.23Shranish KarNo ratings yet

- Telephone BillDocument4 pagesTelephone BillSankar SundaramNo ratings yet

- January 2023 NewsLetterDocument22 pagesJanuary 2023 NewsLetterSabrina CanoNo ratings yet

- Apr 22Document3 pagesApr 22honey moneyNo ratings yet

- Subject:: Reptuenbtives DawDocument19 pagesSubject:: Reptuenbtives DawurhanNo ratings yet

- Jul 22Document3 pagesJul 22honey moneyNo ratings yet

- Sinvoice 4000025727 9394530Document2 pagesSinvoice 4000025727 9394530ajit23nayakNo ratings yet

- Fiber Monthly Statement: This Month's SummaryDocument4 pagesFiber Monthly Statement: This Month's SummaryPi InfratechNo ratings yet

- Pmswa Nidhi DataDocument6 pagesPmswa Nidhi DataManish VermaNo ratings yet

- LICINSTAONLINEHGA4P0204F0354926299Document1 pageLICINSTAONLINEHGA4P0204F0354926299Suhas Renu85No ratings yet

- Inv Ka B1 76433376 102522632160 August 2022Document2 pagesInv Ka B1 76433376 102522632160 August 2022Chinta Rishi RaghavNo ratings yet

- Invoice: Page 1 of 2Document2 pagesInvoice: Page 1 of 2kawal oberoiNo ratings yet

- GST 12 To 18Document34 pagesGST 12 To 18Rajesh ChandelNo ratings yet

- LIC Combined ReceiptsDocument6 pagesLIC Combined Receiptssumanpal78No ratings yet

- HT2329I005080200Document4 pagesHT2329I005080200Aakash VyshnavNo ratings yet

- Sec 183Document1 pageSec 183goelshubham92No ratings yet

- Invoice: Page 1 of 2Document2 pagesInvoice: Page 1 of 2uday kumarNo ratings yet

- Tax Invoice RECIPIENT (Billed To) CONSIGNEE (Shipped To) ChhaattisgarhDocument9 pagesTax Invoice RECIPIENT (Billed To) CONSIGNEE (Shipped To) ChhaattisgarhSumedha SawniNo ratings yet

- Incident Report 40-2022 GSTDocument2 pagesIncident Report 40-2022 GSTAnshu MoryaNo ratings yet

- DGGI Annual Report 2022-23Document68 pagesDGGI Annual Report 2022-23KULDEEP SINGHNo ratings yet

- Accounting Voucher DisplayDocument1 pageAccounting Voucher DisplayShubhyansh SinghNo ratings yet

- DKSH Po 52 DT 06.09.2022Document1 pageDKSH Po 52 DT 06.09.2022Nova TransfersNo ratings yet

- Tax Invoice: Patel Material Handling Equipment-2324Document1 pageTax Invoice: Patel Material Handling Equipment-2324IMARAN PATELNo ratings yet

- Fiber Monthly Statement: This Month's SummaryDocument4 pagesFiber Monthly Statement: This Month's Summaryshamim ahmadNo ratings yet

- Medical InsuranceDocument1 pageMedical InsuranceMasood Ahmad100% (1)

- Tax Invoice: Karnataka, India Gstin/Uin: 29AURPB7606A1ZQ State Name: Karnataka, Code: 29Document1 pageTax Invoice: Karnataka, India Gstin/Uin: 29AURPB7606A1ZQ State Name: Karnataka, Code: 29sudheer kulkarniNo ratings yet

- 1-2150585510952 431765387 70080XXXXX 11 2022Document4 pages1-2150585510952 431765387 70080XXXXX 11 2022jagadishporichhaNo ratings yet

- Aino Communique 108th EditionDocument12 pagesAino Communique 108th EditionSwathi JainNo ratings yet

- Gasbill 4485709078 202207 20220828211011Document1 pageGasbill 4485709078 202207 20220828211011WaqasNo ratings yet

- Aug 22Document3 pagesAug 22honey moneyNo ratings yet

- ITC 08022024191957 SE FineDocument3 pagesITC 08022024191957 SE FineKarunakara ReddyNo ratings yet

- A 30 1 2013 Tariff Proposal FY 14 DGVCLDocument27 pagesA 30 1 2013 Tariff Proposal FY 14 DGVCLJimit ShahNo ratings yet

- Panuwat WancrueaDocument1 pagePanuwat WancrueaITNo ratings yet

- CompliancecalendarjanDocument24 pagesCompliancecalendarjanDsp VarmaNo ratings yet

- Invoice: Page 1 of 2Document2 pagesInvoice: Page 1 of 2Poonam PurohitNo ratings yet

- IshaanDocument2 pagesIshaanNikunjNanduNo ratings yet

- EfewaraweDocument1 pageEfewarawesunil kumarNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- GST Update120Document2 pagesGST Update120prathNo ratings yet

- Usermanual EwbDocument74 pagesUsermanual EwbprathNo ratings yet

- GSTUpdate 05022022Document22 pagesGSTUpdate 05022022prathNo ratings yet

- Latest Updates in GSTDocument6 pagesLatest Updates in GSTprathNo ratings yet

- Invoice PBT0922A00352890Document1 pageInvoice PBT0922A00352890Yusuf AnsariNo ratings yet

- 3 BMW Motorrad Price Compressed 2021Document2 pages3 BMW Motorrad Price Compressed 2021Dhaval WaghelaNo ratings yet

- Tax Invoice: Gstin/Uin: 24AABCY0257H1ZI State Name: Gujarat, Code: 24Document1 pageTax Invoice: Gstin/Uin: 24AABCY0257H1ZI State Name: Gujarat, Code: 24jayshah_26No ratings yet

- GST (Goods and Services Tax) Subcontracting ProcessDocument4 pagesGST (Goods and Services Tax) Subcontracting ProcessmaniNo ratings yet

- NITYA - Indirect Tax Bulletin: January 2022 - Week 1Document9 pagesNITYA - Indirect Tax Bulletin: January 2022 - Week 1swastik groverNo ratings yet

- Annexure BDocument11 pagesAnnexure BSonu JainNo ratings yet

- Ticketpdf 2022 07 20 00000005BB7ADocument2 pagesTicketpdf 2022 07 20 00000005BB7ASUNIL TVNo ratings yet

- Invoice: Deepnayan Scale CompanyDocument1 pageInvoice: Deepnayan Scale CompanyDssp StmpNo ratings yet

- Karneeti Part 382 - New Changes in ITR Forms and Tax Audit Report For F.Y. 2020-21Document8 pagesKarneeti Part 382 - New Changes in ITR Forms and Tax Audit Report For F.Y. 2020-21Komal ShahaNo ratings yet

- Invoice PDFDocument1 pageInvoice PDFbiswaNo ratings yet

- Skquot23 305Document2 pagesSkquot23 305SK EnterprisesNo ratings yet

- DC - Mixer MachinDocument1 pageDC - Mixer Machinvimalraj KNo ratings yet

- InvoiceDocument1 pageInvoiceArpan Feel KingNo ratings yet

- Invoice 9773221286Document1 pageInvoice 9773221286sivakumarNo ratings yet

- Estimate #2023-125963Document1 pageEstimate #2023-125963Karthik DNo ratings yet

- Agro 2022 23 Q 0854Document6 pagesAgro 2022 23 Q 0854Agro SolutionNo ratings yet

- 2020 TNPSC Indian Economy Questions Part 1 in EnglishDocument6 pages2020 TNPSC Indian Economy Questions Part 1 in EnglishVasan DivNo ratings yet

- IF23050633774478 InvoiceDocument1 pageIF23050633774478 InvoiceAnshum GuptaNo ratings yet

- Policy DocumentDocument4 pagesPolicy Documentnizamsagar tsgencoNo ratings yet

- TOPIC:-Background of GST, IGST, SGSTDocument12 pagesTOPIC:-Background of GST, IGST, SGSTshivendra singhNo ratings yet

- InvoiceDocument1 pageInvoiceRichest TechNo ratings yet

- A Study On Impact of GST On FMCG Companies in IndiaDocument4 pagesA Study On Impact of GST On FMCG Companies in IndiaShyamsunder SharmaNo ratings yet

- Circumstances Which Require ITC Reversal - Taxguru - inDocument3 pagesCircumstances Which Require ITC Reversal - Taxguru - inKaran MNo ratings yet

- Journal AssignmentDocument5 pagesJournal AssignmentNathan DavidNo ratings yet

- Feb 1-3613311284991 - BM2233I010340187Document7 pagesFeb 1-3613311284991 - BM2233I010340187Jihoon BongNo ratings yet

- Payment Invoice: GSTN Number:06AAHCP1178L1Z4 SAC Code:998551Document2 pagesPayment Invoice: GSTN Number:06AAHCP1178L1Z4 SAC Code:998551Jigyesh SharmaNo ratings yet

- For HDFC ERGO General Insurance Company Limited: Dear Priteshkumar Kanubhai VyasDocument3 pagesFor HDFC ERGO General Insurance Company Limited: Dear Priteshkumar Kanubhai VyasKrutarth VyasNo ratings yet

- Final Programme Bcom Sem 3 To 6 Oct 2017Document6 pagesFinal Programme Bcom Sem 3 To 6 Oct 2017Suraj PoptaniNo ratings yet

- RptSalesInvoice MorbiDocument1 pageRptSalesInvoice MorbiVishal JadavNo ratings yet