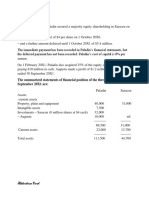

Cost Records

Cost Records

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Test Bank Accounting 25th Editon Warren Chapter 17 Financial Statement AnalysisDocument126 pagesTest Bank Accounting 25th Editon Warren Chapter 17 Financial Statement AnalysisJessa De GuzmanNo ratings yet

- Chapter 02 Ratio AnalysisDocument52 pagesChapter 02 Ratio AnalysisSunita YadavNo ratings yet

- Sap Fico Interview QuestionsDocument28 pagesSap Fico Interview QuestionsNeelesh KumarNo ratings yet

- Financial Reporting (FR) : Syllabus and Study GuideDocument18 pagesFinancial Reporting (FR) : Syllabus and Study GuidePatricio Villegas JungeNo ratings yet

- FABM Globe PaperDocument18 pagesFABM Globe PaperJulian AlbaNo ratings yet

- Brooks Financial Mgmt14 PPT Ch02Document37 pagesBrooks Financial Mgmt14 PPT Ch02Asylkhan NursultanNo ratings yet

- NETFLIX 17-21-Website-FinacialsDocument6 pagesNETFLIX 17-21-Website-FinacialsGreta RiveraNo ratings yet

- Statement of Income: P&L Account Can Also Be Named AsDocument5 pagesStatement of Income: P&L Account Can Also Be Named Asanand sanilNo ratings yet

- Indo Tambangraya Megah TBKDocument3 pagesIndo Tambangraya Megah TBKSolid DesignNo ratings yet

- Final Study Guide Accounting 101Document2 pagesFinal Study Guide Accounting 101Jonathan MoonNo ratings yet

- Accounting For Special TransactionsDocument43 pagesAccounting For Special TransactionsNezer VergaraNo ratings yet

- DepreciationDocument8 pagesDepreciationanjalikapoorNo ratings yet

- Clavax Power - TAR - 2023 - Provisional - 10.09Document7 pagesClavax Power - TAR - 2023 - Provisional - 10.09Naresh nath MallickNo ratings yet

- Sale of PartnershipDocument11 pagesSale of PartnershipJoel VargheseNo ratings yet

- Pag 91-110 Larson. Hostetler PRECÁLCULO SÉPTIMA EDICIÓNDocument20 pagesPag 91-110 Larson. Hostetler PRECÁLCULO SÉPTIMA EDICIÓNMiguelValdiviaNo ratings yet

- 375 PaladinDocument2 pages375 Paladinabdirahman farah AbdiNo ratings yet

- MGT401 Assignment SolutionDocument4 pagesMGT401 Assignment SolutionAhmar KhanNo ratings yet

- OracleDocument40 pagesOraclejaggaraju8No ratings yet

- Accounting Frameworks: The Conceptual FrameworkDocument4 pagesAccounting Frameworks: The Conceptual FrameworkShiza ArifNo ratings yet

- Bhumiworld Subsidy SchemeDocument10 pagesBhumiworld Subsidy SchemeShanky JainNo ratings yet

- A Cash Management in A Supper Market StoreDocument64 pagesA Cash Management in A Supper Market Storechukwu solomon67% (3)

- Financial Statement 1st PaperDocument24 pagesFinancial Statement 1st PaperMtNo ratings yet

- 123 - AS Question Bank by Rahul MalkanDocument182 pages123 - AS Question Bank by Rahul MalkanPooja GuptaNo ratings yet

- Cbse Questions Adm RetirementDocument19 pagesCbse Questions Adm RetirementDeepanshu kaushikNo ratings yet

- Declaration of Assets and Liabilities: AS ON DATE/MONTH/YEAR........................Document3 pagesDeclaration of Assets and Liabilities: AS ON DATE/MONTH/YEAR........................ServeX pluSNo ratings yet

- Saln Gerry MalgapoDocument2 pagesSaln Gerry MalgapogerrymalgapoNo ratings yet

- Velazquez FSDocument1 pageVelazquez FSBhenil Bon VelasquezNo ratings yet

- ACCA SBR Notes - AsraDocument69 pagesACCA SBR Notes - AsraReem JavedNo ratings yet

- IUBAV - Lecture 4 - Module 1 Common-Size and Trend Analysis (S2 2023 2024)Document6 pagesIUBAV - Lecture 4 - Module 1 Common-Size and Trend Analysis (S2 2023 2024)Vũ Trần Nhật ViNo ratings yet

- Homework Ch2Document19 pagesHomework Ch2salehin1969No ratings yet

Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Test Bank Accounting 25th Editon Warren Chapter 17 Financial Statement AnalysisDocument126 pagesTest Bank Accounting 25th Editon Warren Chapter 17 Financial Statement AnalysisJessa De GuzmanNo ratings yet

- Chapter 02 Ratio AnalysisDocument52 pagesChapter 02 Ratio AnalysisSunita YadavNo ratings yet

- Sap Fico Interview QuestionsDocument28 pagesSap Fico Interview QuestionsNeelesh KumarNo ratings yet

- Financial Reporting (FR) : Syllabus and Study GuideDocument18 pagesFinancial Reporting (FR) : Syllabus and Study GuidePatricio Villegas JungeNo ratings yet

- FABM Globe PaperDocument18 pagesFABM Globe PaperJulian AlbaNo ratings yet

- Brooks Financial Mgmt14 PPT Ch02Document37 pagesBrooks Financial Mgmt14 PPT Ch02Asylkhan NursultanNo ratings yet

- NETFLIX 17-21-Website-FinacialsDocument6 pagesNETFLIX 17-21-Website-FinacialsGreta RiveraNo ratings yet

- Statement of Income: P&L Account Can Also Be Named AsDocument5 pagesStatement of Income: P&L Account Can Also Be Named Asanand sanilNo ratings yet

- Indo Tambangraya Megah TBKDocument3 pagesIndo Tambangraya Megah TBKSolid DesignNo ratings yet

- Final Study Guide Accounting 101Document2 pagesFinal Study Guide Accounting 101Jonathan MoonNo ratings yet

- Accounting For Special TransactionsDocument43 pagesAccounting For Special TransactionsNezer VergaraNo ratings yet

- DepreciationDocument8 pagesDepreciationanjalikapoorNo ratings yet

- Clavax Power - TAR - 2023 - Provisional - 10.09Document7 pagesClavax Power - TAR - 2023 - Provisional - 10.09Naresh nath MallickNo ratings yet

- Sale of PartnershipDocument11 pagesSale of PartnershipJoel VargheseNo ratings yet

- Pag 91-110 Larson. Hostetler PRECÁLCULO SÉPTIMA EDICIÓNDocument20 pagesPag 91-110 Larson. Hostetler PRECÁLCULO SÉPTIMA EDICIÓNMiguelValdiviaNo ratings yet

- 375 PaladinDocument2 pages375 Paladinabdirahman farah AbdiNo ratings yet

- MGT401 Assignment SolutionDocument4 pagesMGT401 Assignment SolutionAhmar KhanNo ratings yet

- OracleDocument40 pagesOraclejaggaraju8No ratings yet

- Accounting Frameworks: The Conceptual FrameworkDocument4 pagesAccounting Frameworks: The Conceptual FrameworkShiza ArifNo ratings yet

- Bhumiworld Subsidy SchemeDocument10 pagesBhumiworld Subsidy SchemeShanky JainNo ratings yet

- A Cash Management in A Supper Market StoreDocument64 pagesA Cash Management in A Supper Market Storechukwu solomon67% (3)

- Financial Statement 1st PaperDocument24 pagesFinancial Statement 1st PaperMtNo ratings yet

- 123 - AS Question Bank by Rahul MalkanDocument182 pages123 - AS Question Bank by Rahul MalkanPooja GuptaNo ratings yet

- Cbse Questions Adm RetirementDocument19 pagesCbse Questions Adm RetirementDeepanshu kaushikNo ratings yet

- Declaration of Assets and Liabilities: AS ON DATE/MONTH/YEAR........................Document3 pagesDeclaration of Assets and Liabilities: AS ON DATE/MONTH/YEAR........................ServeX pluSNo ratings yet

- Saln Gerry MalgapoDocument2 pagesSaln Gerry MalgapogerrymalgapoNo ratings yet

- Velazquez FSDocument1 pageVelazquez FSBhenil Bon VelasquezNo ratings yet

- ACCA SBR Notes - AsraDocument69 pagesACCA SBR Notes - AsraReem JavedNo ratings yet

- IUBAV - Lecture 4 - Module 1 Common-Size and Trend Analysis (S2 2023 2024)Document6 pagesIUBAV - Lecture 4 - Module 1 Common-Size and Trend Analysis (S2 2023 2024)Vũ Trần Nhật ViNo ratings yet

- Homework Ch2Document19 pagesHomework Ch2salehin1969No ratings yet