Download as pdf or txt

You might also like

- Participant's NoteDocument11 pagesParticipant's NoteaskNo ratings yet

- PGD-GST 2020 Batch - Paper I 26-09-2020Document31 pagesPGD-GST 2020 Batch - Paper I 26-09-2020hampaiahNo ratings yet

- GST in IndiaDocument46 pagesGST in IndiaSam RockerNo ratings yet

- Basics of GST PDFDocument23 pagesBasics of GST PDFmaxsoniiNo ratings yet

- Taxation 101 Amendment ActDocument6 pagesTaxation 101 Amendment Actnikitha chowdaryNo ratings yet

- TAX LAW II NotesDocument10 pagesTAX LAW II Notesaffan QureshiNo ratings yet

- GST - UNIT 1 (Updated 2022)Document130 pagesGST - UNIT 1 (Updated 2022)Krish GoelNo ratings yet

- GST - Uniting India: CA. Rajendra Kumar P, FCA, Chartered AccountantDocument3 pagesGST - Uniting India: CA. Rajendra Kumar P, FCA, Chartered AccountantMuhammed Aslam NVNo ratings yet

- Indirect Tax and GSTDocument124 pagesIndirect Tax and GSTPrasanna KumarNo ratings yet

- GST - Brief - Exports and RefundsDocument18 pagesGST - Brief - Exports and RefundsSteve MclarenNo ratings yet

- GST Notes For Sem 4Document7 pagesGST Notes For Sem 4prakhar100% (2)

- GST MaterialDocument17 pagesGST MaterialElisha grandhiNo ratings yet

- Unit-1: Introduction and Overview of GST Chapter 1: IntroductionDocument5 pagesUnit-1: Introduction and Overview of GST Chapter 1: IntroductionASHISH LOYANo ratings yet

- Tax Law IIDocument20 pagesTax Law IIaffan QureshiNo ratings yet

- Taxation Law GST NotesDocument125 pagesTaxation Law GST NotesHasnainNo ratings yet

- Background Material For 3days Refresher Course On GSTDocument34 pagesBackground Material For 3days Refresher Course On GSTDevika JauhariNo ratings yet

- Project 3 GST Returns-1Document56 pagesProject 3 GST Returns-1K.v. PriyankcaNo ratings yet

- GST - Concept & Status: For Departmental Officers OnlyDocument7 pagesGST - Concept & Status: For Departmental Officers Onlypatelpratik1972No ratings yet

- Bird Eye View of GST ActDocument34 pagesBird Eye View of GST ActNarayan KulkarniNo ratings yet

- Taxation 2Document5 pagesTaxation 2devang bhatiNo ratings yet

- GST PDFDocument7 pagesGST PDFShekhar singhNo ratings yet

- Presentation 1Document8 pagesPresentation 1AR Ananth Rohith BhatNo ratings yet

- GST - Introduction To GST & Concept of SupplyDocument40 pagesGST - Introduction To GST & Concept of Supplydeepak singhalNo ratings yet

- Study Notes 1Document10 pagesStudy Notes 1Devesh BalodhiNo ratings yet

- GST Notes Semester 6Document39 pagesGST Notes Semester 6Bhanu DangNo ratings yet

- GST - Concept & Status - September, 2016: For Departmental Officers OnlyDocument8 pagesGST - Concept & Status - September, 2016: For Departmental Officers OnlyRahul AkellaNo ratings yet

- Unit 3 GSTDocument51 pagesUnit 3 GSTMichael WellsNo ratings yet

- Cheat Sheet TaxDocument6 pagesCheat Sheet TaxShravan NiranjanNo ratings yet

- IGST (Integrated GST) : Based On The IGST Act, 2017 and The CGST Act, 2017Document85 pagesIGST (Integrated GST) : Based On The IGST Act, 2017 and The CGST Act, 2017Partha BhaskarNo ratings yet

- Legal Aspects GSTDocument46 pagesLegal Aspects GSTtharani1771_32442248No ratings yet

- SM GSTDocument12 pagesSM GSTPranav TejaNo ratings yet

- Revised Model GST LawDocument39 pagesRevised Model GST LawkshitijsaxenaNo ratings yet

- BGM For GST PDFDocument341 pagesBGM For GST PDFPriya SafayaNo ratings yet

- Meaning and Introduction of GSTDocument6 pagesMeaning and Introduction of GSTAshish BomzanNo ratings yet

- Unit-1: Introduction and Overview of GST Chapter 1: IntroductionDocument6 pagesUnit-1: Introduction and Overview of GST Chapter 1: IntroductionrajneeshkarloopiaNo ratings yet

- GST - Concept & Status - May, 2016: For Departmental Officers OnlyDocument6 pagesGST - Concept & Status - May, 2016: For Departmental Officers Onlydroy21No ratings yet

- Taxation LawDocument19 pagesTaxation LawMayank SarafNo ratings yet

- GST NotesDocument18 pagesGST NotesNasmaNo ratings yet

- Taxation Unit-3 and 4Document38 pagesTaxation Unit-3 and 4GITANJALI MISHRANo ratings yet

- Tax Laws Indirect Taxes For December 2020 ExamDocument53 pagesTax Laws Indirect Taxes For December 2020 ExamprofessorrlakshmikanthNo ratings yet

- Activating GST For Your Company: Tally ERP Material Unit - 3 GSTDocument47 pagesActivating GST For Your Company: Tally ERP Material Unit - 3 GSTMichael Wells100% (1)

- Unit-Ii GSTDocument28 pagesUnit-Ii GSTVaibhav ArwadeNo ratings yet

- GSTDocument3 pagesGSTvaishnavvktNo ratings yet

- Ca Suraj Satija Ssguru Charge of GSTDocument12 pagesCa Suraj Satija Ssguru Charge of GSTSunny YadavNo ratings yet

- LLB Taxation Law Unit-3 Part - 1-1 PDFDocument44 pagesLLB Taxation Law Unit-3 Part - 1-1 PDFravi kumarNo ratings yet

- GST AssignmentDocument16 pagesGST AssignmentDroupathyNo ratings yet

- Module 1Document3 pagesModule 1namonamy3No ratings yet

- Further To Amend The Constitution of IndiaDocument11 pagesFurther To Amend The Constitution of IndiaUJJAL SAHUNo ratings yet

- This Content Downloaded From 117.232.123.74 On Tue, 21 Jul 2020 05:00:34 UTCDocument10 pagesThis Content Downloaded From 117.232.123.74 On Tue, 21 Jul 2020 05:00:34 UTCNarendra Singh RathoreNo ratings yet

- Indian GST Reference ManualDocument594 pagesIndian GST Reference ManualY M Shah & Co100% (5)

- Chapter I: Implementation of GSTDocument23 pagesChapter I: Implementation of GSTTax NatureNo ratings yet

- Final Draft TAXATION IIDocument13 pagesFinal Draft TAXATION IIAryanNo ratings yet

- GST Concept and StatusDocument11 pagesGST Concept and Statusichchhit srivastavaNo ratings yet

- Circular No (1) - 16 Dt.16 Nov 09 For GSTDocument3 pagesCircular No (1) - 16 Dt.16 Nov 09 For GSTSeemaNaikNo ratings yet

- Yashada-Workshop-How To Read GST LawDocument57 pagesYashada-Workshop-How To Read GST LawRajendra D AdsulNo ratings yet

- Compendium On GSTDocument5 pagesCompendium On GSTSumit KumarNo ratings yet

- GSTDocument23 pagesGSTjamal ahmadNo ratings yet

- Assignment-1: BY: NIKHIL KUMAR (05814901718)Document5 pagesAssignment-1: BY: NIKHIL KUMAR (05814901718)nikhilNo ratings yet

- GST in India by Puneet Agrawal PDFDocument75 pagesGST in India by Puneet Agrawal PDFSaNo ratings yet

- GST Rahul 1 Project WorkDocument29 pagesGST Rahul 1 Project Workanjali baria100% (5)

- C4 Fiscal PolicyDocument6 pagesC4 Fiscal PolicyPhong Lê Trần ĐăngNo ratings yet

- Swiss Market Index (Smi) FinalDocument28 pagesSwiss Market Index (Smi) Finalvijay dhondiyalNo ratings yet

- OpTransactionHistoryTpr02 08 2022Document46 pagesOpTransactionHistoryTpr02 08 2022sanket enterprisesNo ratings yet

- Market Report Manish ShitlaniDocument22 pagesMarket Report Manish ShitlanimanisjiNo ratings yet

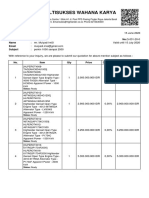

- Pt. Multisukses Wahana Karya: To No.Q-031-20-0 Name Email SubjectDocument2 pagesPt. Multisukses Wahana Karya: To No.Q-031-20-0 Name Email SubjectPrana HartadiNo ratings yet

- Train Law Bane or BoonDocument1 pageTrain Law Bane or BoonJunel PlanosNo ratings yet

- Busn 11th Edition Kelly Test BankDocument19 pagesBusn 11th Edition Kelly Test BankAnthonyJacksonekdpb100% (16)

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument5 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceVishal JainNo ratings yet

- Forex JuthiDocument16 pagesForex JuthiShamsun NaharNo ratings yet

- Invoice CT-2237192Document2 pagesInvoice CT-2237192ABALUNo ratings yet

- FieoDocument31 pagesFieoparidhi9No ratings yet

- Wealth Management Assignment Idfc: About The CompanyDocument2 pagesWealth Management Assignment Idfc: About The CompanyManmeet MalikNo ratings yet

- Reliance Power Limited - List of Installed & Planned Power ProjectsDocument1 pageReliance Power Limited - List of Installed & Planned Power ProjectsZahoor AhmedNo ratings yet

- Bangladesh's Graduation From LDC: Policies That Have Already Been Taken and The Government's PlanDocument14 pagesBangladesh's Graduation From LDC: Policies That Have Already Been Taken and The Government's PlanRafid AbrarNo ratings yet

- OpTransactionHistory11 11 2022Document12 pagesOpTransactionHistory11 11 2022Bharath ANo ratings yet

- PM Ch04 Managing in The Global ArenaDocument17 pagesPM Ch04 Managing in The Global ArenaPhạm Văn HuyNo ratings yet

- Evaluacion Final - Escenario 8 - PRIMER BLOQUE-TEORICO - PRACTICO - GLOBALIZACION Y COMPETITIVIDAD - (GRUPO B01)Document7 pagesEvaluacion Final - Escenario 8 - PRIMER BLOQUE-TEORICO - PRACTICO - GLOBALIZACION Y COMPETITIVIDAD - (GRUPO B01)liliana rinconNo ratings yet

- Textiles 2Document4 pagesTextiles 2Mazine QalbaouiNo ratings yet

- The Contemporary WorldDocument19 pagesThe Contemporary WorldDaniellaNo ratings yet

- The Future of Real Estate and Construction 2022Document39 pagesThe Future of Real Estate and Construction 2022rfbechtel2021No ratings yet

- Resolution No. 15-Adopting The 1% BCPCDocument2 pagesResolution No. 15-Adopting The 1% BCPCBarangay MambaliliNo ratings yet

- Statement 1568002244543Document10 pagesStatement 1568002244543krishna aNo ratings yet

- Outsourcing in Apparel IndustryDocument13 pagesOutsourcing in Apparel IndustryPriyanshu GuptaNo ratings yet

- Quiz1 KeyDocument6 pagesQuiz1 Keyproject44No ratings yet

- Lecture 4 - Export and Import TaxDocument27 pagesLecture 4 - Export and Import TaxHai Bui thiNo ratings yet

- Indian Economy Unit III Balance of Payment / Trade Notes By: Dr. Neelam TandonDocument13 pagesIndian Economy Unit III Balance of Payment / Trade Notes By: Dr. Neelam TandonAmit MishraNo ratings yet

- Intra-Industry TradeDocument15 pagesIntra-Industry TradePrashant RampuriaNo ratings yet

- Salary Slip Deepak Upadhyay: Daewoo ST India Private LimitedDocument1 pageSalary Slip Deepak Upadhyay: Daewoo ST India Private LimitedDeepak UpadhayayNo ratings yet

- Transition Finance ABC Methodology C5210d6c-EnDocument54 pagesTransition Finance ABC Methodology C5210d6c-EnTRYNo ratings yet